What Did We Know — And When Did We Know It?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a huge economic calendar and the first of three scheduled Presidential debates. The employment report will be the last one before the election, so I expect it to get special attention. Most of the other important economic data will also be reported during the week.

The data provide an opportunity for investors to assess what they can reasonably conclude about the state of the economy and investment prospects. We should all be asking,

What do we know ……and when did we know it?

Last Week Recap

In my last installment of WTWA, I emphasized the investor need for evidence on key elements of the economy. I also noted that this attention to data might well be overtaken by politics and the Supreme Court vacancy.

I was half right.

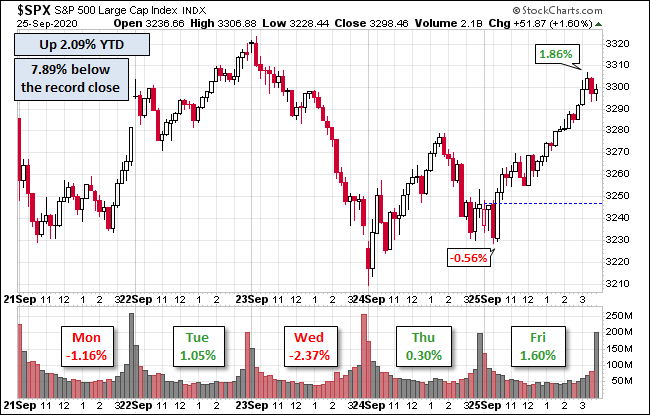

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version of the prior week. The callouts also show the large range of Friday trading.

The market declined 0.6% on the week. Despite the choppy look of the chart, the trading range was only 3.5%. I provide regular updates of historical and expected volatility in my Indicator Snapshot (below).

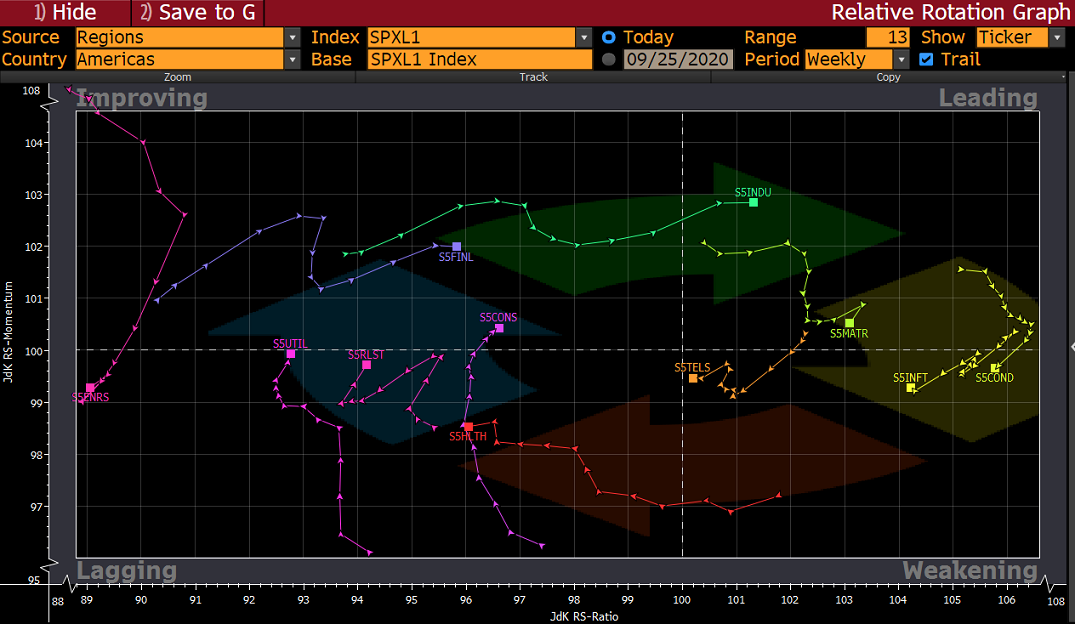

The weekly sector chart shows the sources of the action.

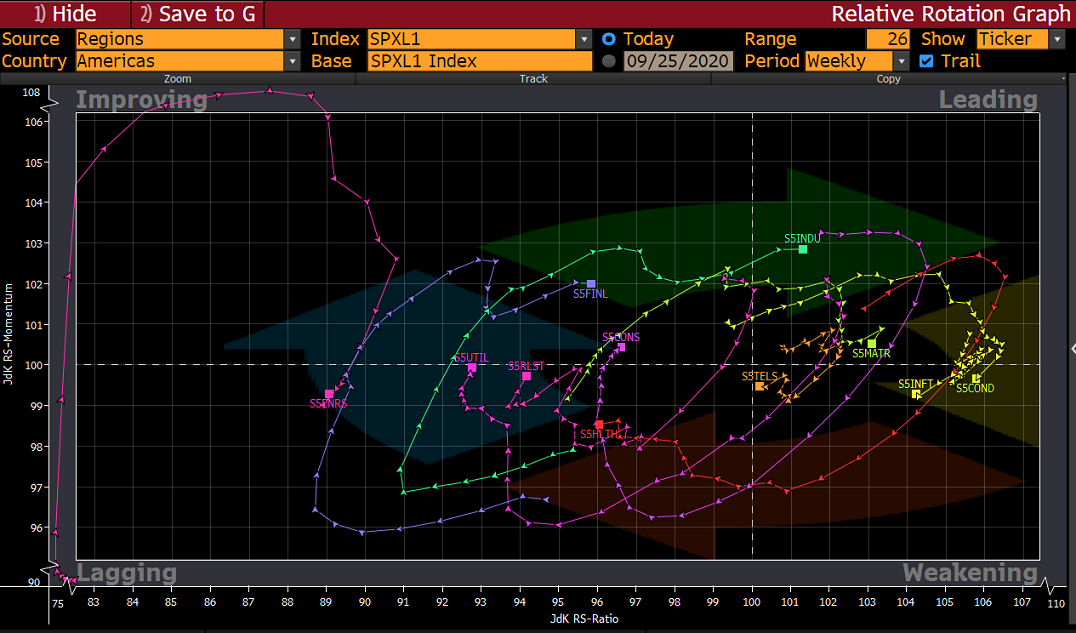

Some readers asked whether we could do this chart in a longer time frame. Here is one for twice the length of time, 26 weeks. Let me know which you prefer or whether I should alternate.

My trading team has passed along more information about the source of this chart. I know that many readers like it, so you may with to read some blog posts by Julius de Kempenaer. I especially recommend his 9/21/20 edition, Daily Rotations Look Erratic.

Juan Luque, the member of our trading team who works most closely with these trends is back this week with his current interpretation.

In this week’s longer range RRG -we went from 13 to 26 weeks- the trends’ clockwise paths are easily seen. The energy sector looks like the most beaten down as it failed to move into the leading quadrant and fell back down into the lagging one. We can also see that the weakness in the sector is more than just a few weeks. The financial sector seems like the most promising as it moves towards the leading quadrant. The health care sector shows weakness while the utilities, consumer, and real estate get closer to the improving quadrant. The sectors showing improving strength represent the “shopping list,” as Mr. Kempenaer, creator of the RRG, would refer to it.

(The sector names are here. The Bloomberg symbols add “S5” at the start of the name. The small square is the current value and other points are the history).

Noteworthy

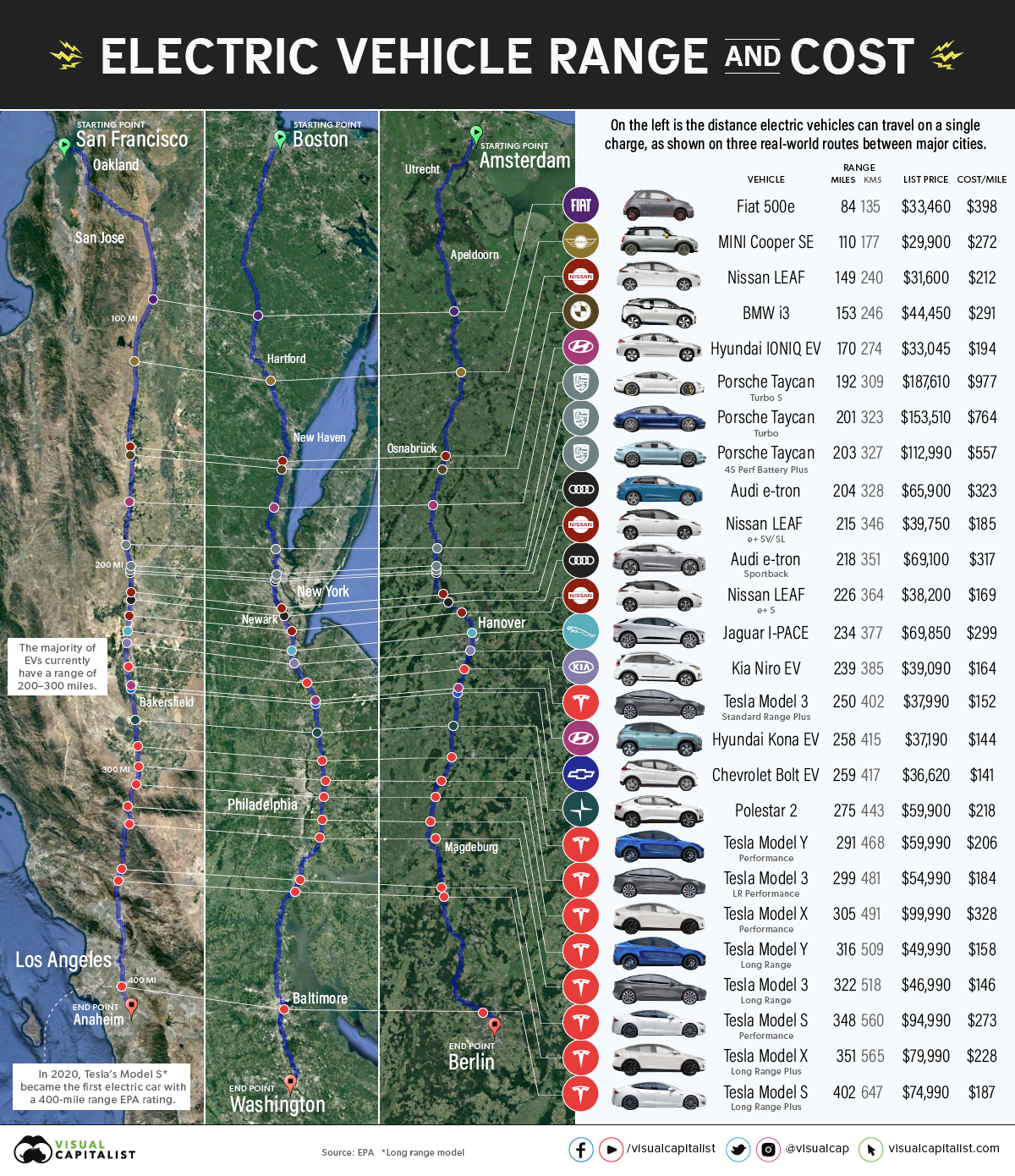

The Visual Capitalist considers the trend toward EV’s. This graphic combines two key questions:

- How far can you go on a single charge?

- How much will it cost?

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

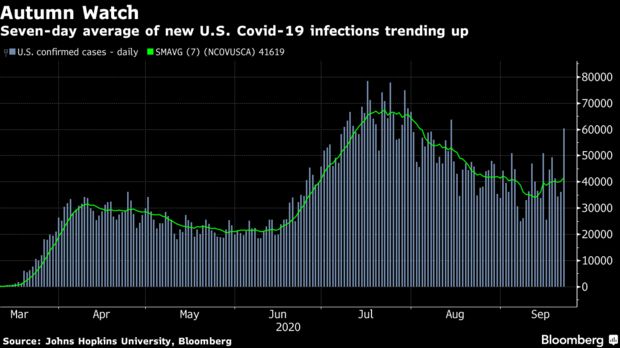

New Deal Democrat’s high frequency indicators are more important than ever. As we look for turning points and the sustainability of the rebound, these are the earliest clues. His latest update shows all three of his time frames remain in positive territory. He remains concerned about consumer spending in the absence of more Congressional emergency aid. And of course, the lack of progress on COVID-19 issues.

There are now many “competitors” on the high-frequency indicator front. There is an important difference between most approaches and that of NDD. He developed a method that created a logical variation in time frames and tested his choices. The efforts I now see most commonly scoop up any report that is relatively contemporary and plugs it in. There is no vetting, checking of methodology, or testing against prior eras. It is a demonstration of one of my key data principles: When there is a large appetite to know about something, the market will uncritically accept whatever is offered. The chart below, for example, is interesting in a general way, but a challenge to extrapolate to the broader economy.

The Good

- MBA Mortgage Applications rose 6.8% versus last week’s 2.5% decline. (Calculated Risk).

- New home sales for August increased to a SAAR of 1011K, beating expectations of 875K and above July’s 965K (revised up from 901K). Calculated Risk observes as follows:

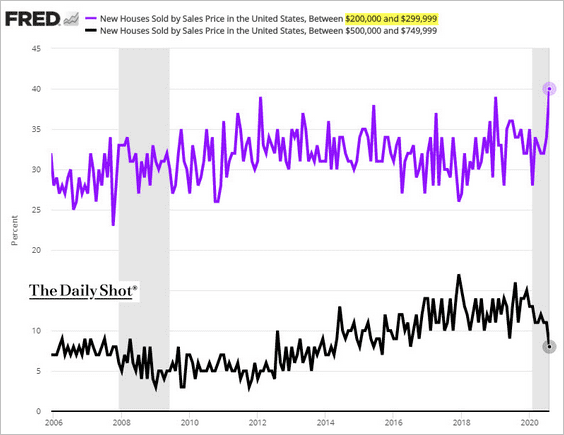

This was well above consensus expectations, and this was the highest sales rate since 2006. Clearly low mortgages rates, low existing home supply, and low sales in March and April (due to the pandemic) have led to a strong increase in sales. Favorable demographics (something I wrote about many times over the last decade) and a surging stock market have probably helped new home sales too.

Part of the improvement is the result of builders’ adaptation to demand.

- Rail traffic contracting, but at a slower pace. Steven Hansen (GEI) tracks the data via his economically intuitive sectors concept. He also uses year-over-year comparisons as one of the tests and a rolling four-week moving average to smooth the series.

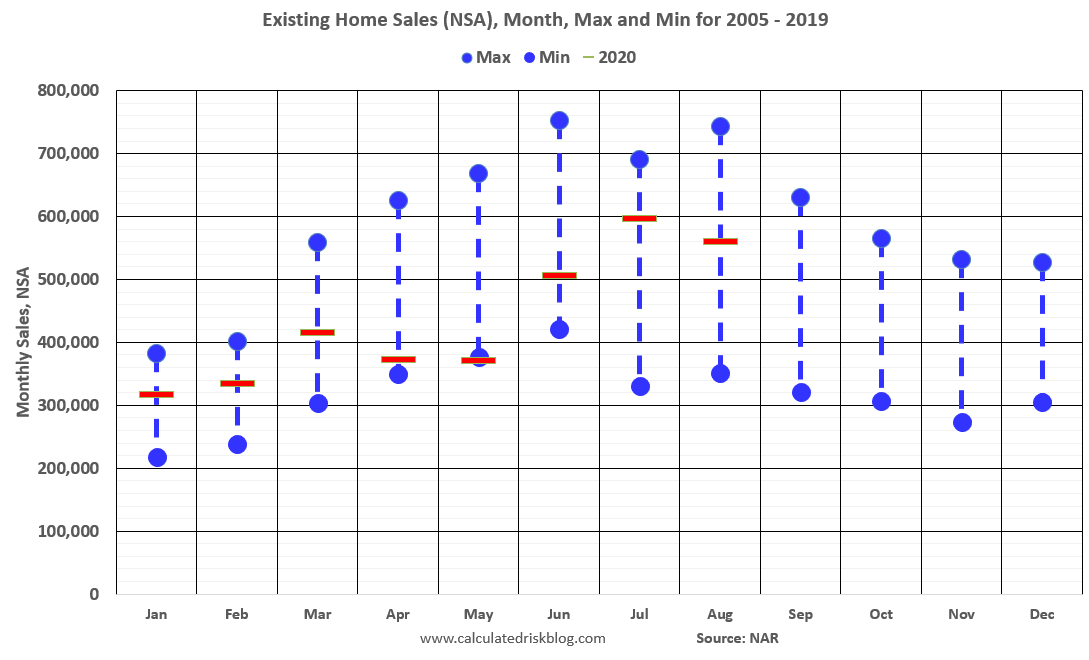

- Existing home sales for August recorded a 6.00M (SAAR), in line with expectations but an improvement of July’s 5.86M. Calculated Risk notes that future comparisons will be challenging, since 2019 sales improved with lower interest rates. Here is an interesting chart that shows multi-year comparisons.

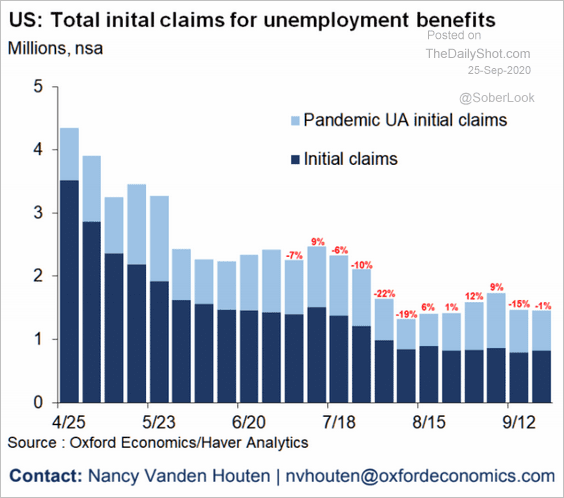

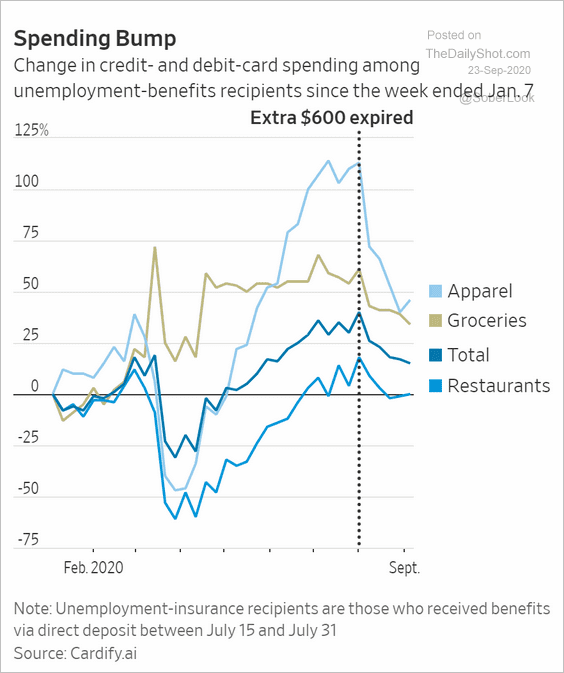

- Continuing jobless claims improved to 12.580M, better than the prior week’s (upwardly revised) 12.747 M.

- Fewer mortgage loans are in forbearance. (Calculated Risk). It is now the lowest level in five months.

The Bad

- Initial jobless claims increased to 870K, worse than expectations of 825K, but in line with the prior week’s 866K.

- Durable goods orders for August increased 0.45, worse than expectations of 0.9% and much worse than July’s (upwardly revised) gain of 11.7%.

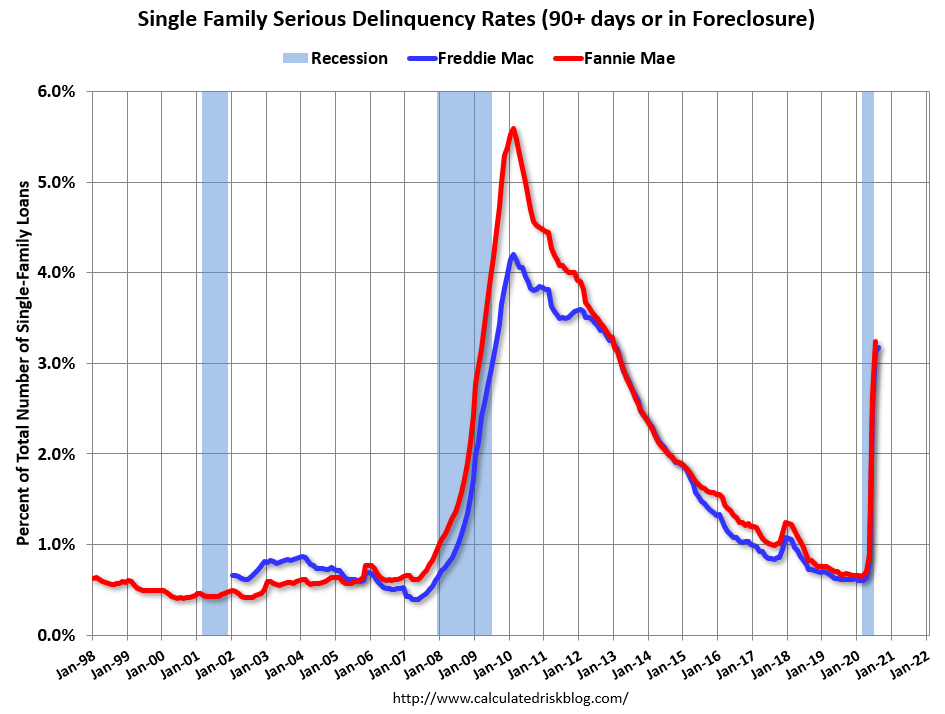

- Mortgage serious delinquency rate increases. Calculated Risk writes that it is the highest since 2013.

- Insiders are selling stock. (Hajric and Wang via Advisor Perspectives).

Corporate executives and officers at S&P 500 companies were busy unloading shares of their own firms over the last four weeks. The selling picked up so much versus buying that a measure of insider velocity tracked by Sundial Capital Research pointed to the fastest exit from stocks since 2012.

While factors other than valuations can influence insiders’ decisions to sell, the action from this cohort — likely the most-knowledgeable about their own businesses — is hardly encouraging news in a market where the S&P 500 is heading for its worst September since the global financial crisis. The index’s 2.4% plunge on Wednesday extended its retreat from the Sept. 2 record to 9.6% and left it little changed in 2020.

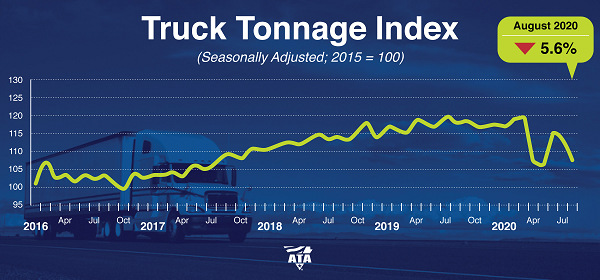

- Trucking remains in contraction. Steven Hansen (GEI) emphasizes the importance of consistency among the various freight indicators. The full post examines the data in detail, but the ATA chart is a hint of the situation.

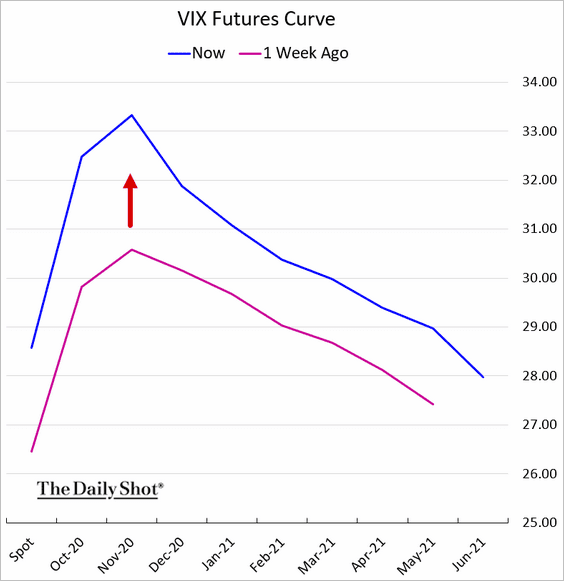

- More volatility ahead? The VIX futures curve measures volatility expectations. The election effect is clear.

The Ugly

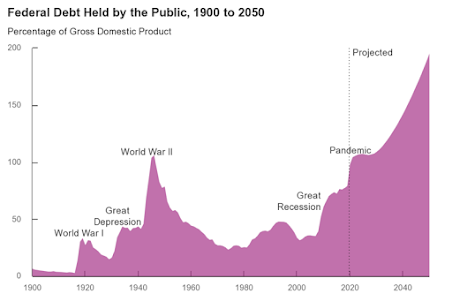

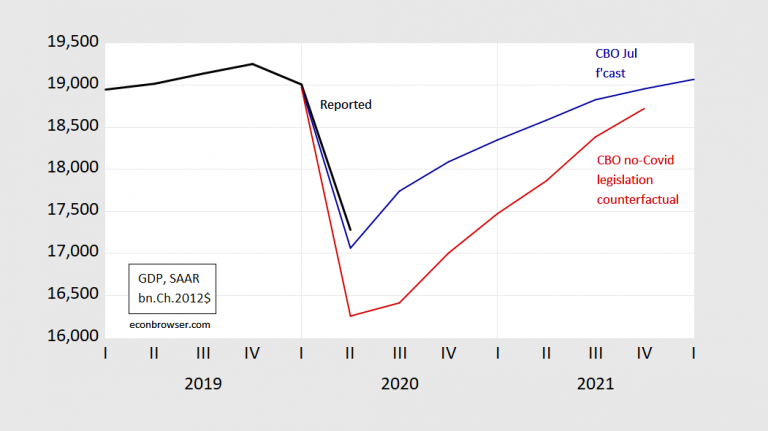

Federal debt scenarios. Driving the tough choices between social distancing safety and economic needs is the growing realization that there will eventually be a real limit to debt. The CBO released its most recent forecasts. Here is the ugly picture. (Conversable Economist).

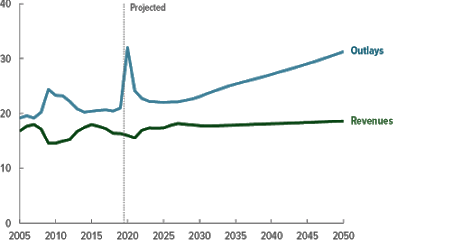

And the underlying balance (or lack thereof) in outlays and revenues shows up clearly, with an extra burst of spending for pandemic measures.

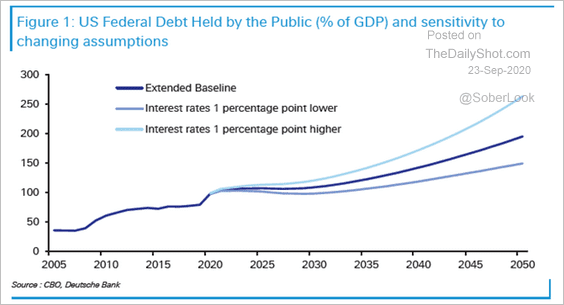

These projections make some optimistic assumptions about interest rates. The CBO report also shows the sensitivity of the results to the interest rate assumptions.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

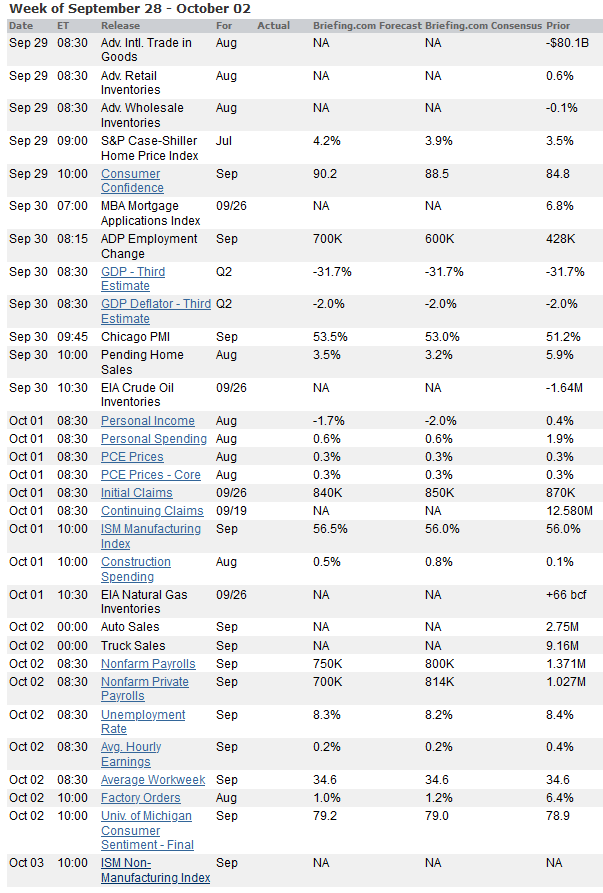

We have a huge economic calendar. All of the most important reports are on tap, with an emphasis on employment – the official employment situation report, the ADP private payrolls, and the weekly jobless claim data. We also get confidence data from the University of Michigan as well as the Conference Board.

And that is just for starters! The ISM manufacturing and non-manufacturing reports are important reads on the current month. Personal income and spending are good signs of consumer health and the accompanying PCE indicator is the Fed’s favorite inflation indicator. We should also not ignore construction spending and factory orders.

They final estimate of Q2 GDP is not expected to change much, and it will be treated as “old news.”

Employment is the biggest news for most people, and this is the last report before the election. It will get even more attention than usual.

The first Presidential debate is scheduled for Tuesday evening. It will command a lot of attention, but probably will not be a market-moving event.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The big data week would normally be enough to occupy the attention of each pundit and media personage. This who found that boring could wade into the political waters to speculate about the Supreme Court and the Presidential debate.

At some point I will do a standalone piece on the election implications for investors. Most of what I have seen so far is not very good, but there are some fresh approaches. I naturally have some ideas of my own.

Despite the economic agenda, I see the most important challenge is gaining some perspective on how events have affected our portfolios. We can summarize what we know now, but it is more interesting to ask:

What do we know —-and when did we know it?

Background

As one who constantly watches markets and relevant news, most of what is currently happening is no surprise. It is easy to forget that my readership is not like a class where everyone has seen all the material (and is ready for the exam). I was pondering this point out loud when Mrs. OldProf suggested that my readers might not finish each 4000-word article. When I frowned, she said that some might even miss an issue or two. When my brow wrinkled further, she confessed that sometimes she did a little skimming, just to see if she had been quoted.

Quelle surprise! Since I avoid repetition on key themes, I decided that a little refresher might be helpful. Here is what we knew as the pandemic market developed.

Chronology

February 22nd: After summarizing some expert market opinions I wrote, “The key question for the market remains: Will this be a contained, mostly China event lasting a couple of months? Or is a pandemic in store?”

In my more worried about section I wrote, “The coronavirus expansion into new countries. This deserves constant attention.”

March 1st: I asked about the “message of the markets.”

The first problem in answering this week’s question is figuring out what the message really is? This speculation will be undertaken by historians pretending to be economists, economists who claim expertise in epidemiology, and technical analysts who know not only what people are currently thinking, but what they will think next week. There is plenty of information, but it is a disorganized mess of unsound opinions, myths, along with solid research. It is not very helpful to the average investor.

My objective is to organize and report the best of what I read last week, placing emphasis on the problems of the individual investor. A logical framework is a great starting point. I’ll separate discussion into several important topics including:

Facts

Problems with data

Potential for a “solution”

Leadership needs

Economic effects

Earnings

Wildcards

Investment implications

I also stated that I had reduced the position size in my lead program but warned long-term investors not to go all-in or all-out. This was my first effort to pull these effects together for investors. It has been accurate.

March 7th: I emphasized the importance of time frames. The economic data did not reflect the coronavirus impact.

Regular reporting of data releases makes it easy to forget that the “news” is often weeks old. When events are breaking fast and markets responding to headlines, this is important to keep in mind. We may still be two months away, or even longer, before we begin to get data which we can treat as important.

I then looked at the virus, the economic effects, policy proposals, and stock prices analyzing contrasting the immediate impacts and those that might happen within a year.

March 15th: I reprised the prior week’s list, but this time looking at new information and what investors should look for. I took note of elevated volatility and the opportunity in covered call strategies (including my own of course). I also highlighted excellent posts from Vitaliy Katsenelson and Jason Zweig applying the work of Ben Graham to the current market.

The prices you see on your screen today are the transitory manic depressive opinions of the often mentally unstable Mr. Market. (If I have offended Mr. Market, my apologies). Mr. Market did not carefully value your companies today and decided that they are now worth less. No, he woke up in a grumpy mood and indiscriminately marked them down as if they were overripe bananas at the grocery store. (You cannot have enough metaphors here.)

The stock prices on your screen say nothing about what these companies are worth. Nothing at all. But that is all that is going to matter in the long run. I promise you one thing: The value of your companies doesn’t change 8% a day, day after day.

In my “less worried” section I cited “Epidemic containment. In the last week there has been a major move in the right direction.”

April 4th: I took up a quixotic topic. My impossible dream was to explain the importance of systematic modeling in a few paragraphs. This may have been my most important post of the “pandemic series” but I was not changing many minds. Those who reject models have no experience in using them and do not even understand the purpose.

This topic was important because there were many models, each with a somewhat different purpose, data inputs, and flaws. Unless you understood something about the process, which hardly anyone did, valuable analysis would be lost in a cacophony of dueling experts.

The most important aspects of modeling are the following, none of which is a single point forecast of an outcome!

Carefully reviewing all of the factors involved. Decide whether something is relevant and whether it fits into the model. This keeps you focused on the right problems.

Making reasonable assumptions for each factor. This requires study.

Providing the ability to adjust assumptions to test sensitivity of the results. If an input has little effect, you can give it less study. If it has a big impact, you know where to focus.

Briefly put, a good model forces you to think about the problem in a disciplined fashion, consider the relevant assumptions, and identify the range of possible outcomes.

Part of the current confusion is that amateurs seize upon a “model result” without considering any of the relevant elements. It is no wonder that model developers are amazed at finding themselves quoted concerning very specific predictions about fatalities.

Sadly, the model interpretation problem has played out as I expected. Here is a frequent example. A model predicts some large number of deaths – say one million. Government policy changes to limit the virus expansion. The number of deaths is greatly reduced. The model may well have stimulated policymakers to take the problem more seriously.

Amazingly, many observers simply conclude that the model was wrong!

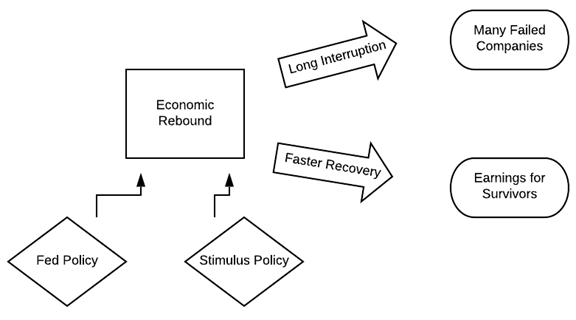

Here was my first pass at laying out the key factors. It provided the basis for my Great Reset approach.

I also showed that the pandemic effect created the unavoidable backdrop for the economic rebound model. I identified intensity, timing of the peak, social distancing, timing for a treatment or vaccine, and the need for an effective play for returning to work. There was little information available on any of these key indicators, but investors at least knew what to be watching.

I opined that I was less worried about “Another Great Depression or Great Recession. In a recent update, JP Morgan’s Dr. David Kelly cited a crucial difference. This time we know there will be an end. It may not come until someone has an effective vaccine, but the economic weakness will not drag on indefinitely with no end in sight. I also like his fall, stall, and surge description for market action.”

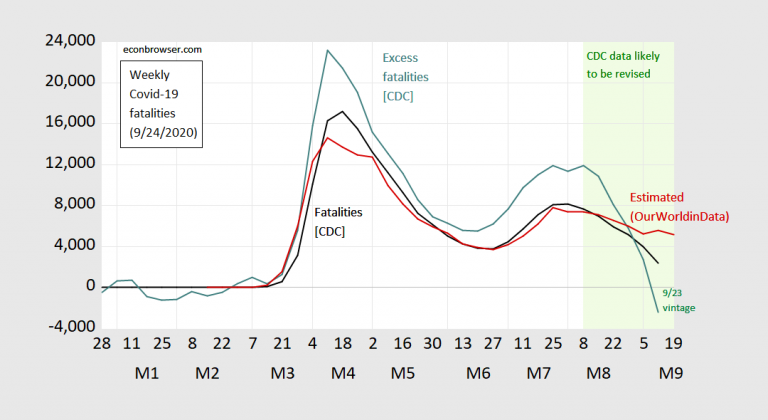

UPDATE: We cannot even agree on how to count lives lost. Menzie Chinn analyzes the best method, excess facilities.

April 19th: The enthusiasm for reopening the economy was building. I wrote:

The return to normalcy has taken on a political cast. Many of our leaders (mostly Republicans) are looking at the facts right in front of them and conclude that the problem is over-stated. Several of my respected economic sources are describing the economic shutdown as a costly waste. The cost is definitely great. The consequences of the alternative are the result of controversial estimates.

The opponents of this viewpoint (mostly Democrats) place more emphasis on the pubic safety issue and have more confidence in the scientific analyses.

A third group is happy to step into the financial gap, but especially worried about mounting debt.

Weeks ago, I concluded that this was not a time to listen to everyone, treating all opinions as equal. Sticking with the tradition of my work, I am seeking out the best experts on several important questions. This means creating four different models and finding a way to link them together– Pandemic, Economy, Corporate Earnings, and only then, Stock Prices. There is no sound way to skip ahead in the chain.

{emphasis added}

I continued by describing the criteria for reopening, drawing upon several respected sources. I concluded with this advice:

Be optimistic about science, cautious about politics, suspicious of economic forecasts, and open-minded about the future economy.

May 16th: I warned that there were no shortcuts.

Dr. Anthony Fauci: “…(Y)ou’ve got to understand that you don’t make the timeline, the virus makes the timeline.”

The virus timeline ripples through the pace of reopening, the economic impact, the need for government action, corporate earnings. And finally, of course, financial markets.

That was back when it was still non-controversial to quote Dr. Fauci.

I did some special coverage on the pace of reopening and the phases recommended by various experts. I also cited an expert on coronavirus spread through the air, one who started with no political agenda. I was amazed at how many criticized this study. Here is a still shot from his video.

May 23rd: I introduced the need for balance as we reopened the economy. I studied the tension between state (un)readiness for reopening, the economic pressures, and the vaccine hope. A negative note was the skepticism about Americans taking a vaccine. My own research also revealed persistent skepticism in mask-wearing, social distancing, testing, and tracing. It revealed a challenge for those seeking a balance.

May 30th: This “vacation post” included a great source about simulations, What Happens Next. If you missed this one, I encourage reading it now and trying the interactive “playable simulations.”

June 16th: I reacted skeptically to the rebound trend. The reasons offered were even weaker than usual. I suggested some facts and sources to consider.

June 20th: I focused on the mixed market message and the continuing lame efforts at explanation. My own interpretation was the skepticism about the “message.” It was my first warning about relying on directional indicators (think diffusion measures) rather than those showing levels of economic activity.

Properly interpreted, economic data show a modest and expected rebound from the lows. Something is to be expected from the economic reopening. Stock prices have become unhinged from a long-term view of economic growth and earnings.

Personal Note

This is about halfway through my “Pandemic Series.” I sincerely hope that readers will review some of these posts. I think the analysis has held up well. I have provided enough information for you to choose some that seem important.

In the remaining posts I provide some updates on these themes as well as some specific investment advice. I will review those in my next WTWA installment.

I have a few additional observations in today’s Final Thought.

Ideas for Investors

I have switched the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. It has turned out to be more comprehensive than it was as a part of WTWA, and more difficult to do. It is important to include the Great Reset concept as well. I am starting to see more ideas worthy discussing. I may not be able to do this weekly, and it might be a bit shorter.

Quant Corner and Risk Analysis

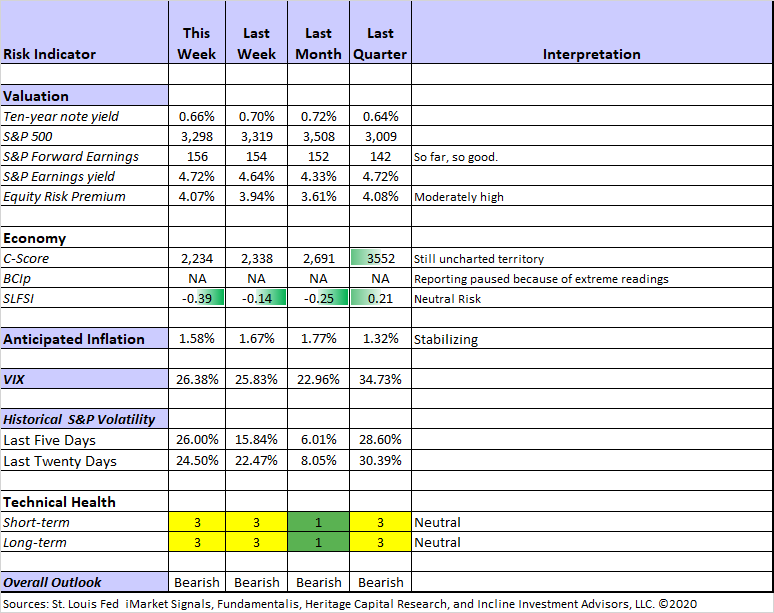

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

The technical indicators are hovering around key levels – negative as of Thursday’s close but back to neutral on Friday. My overall rating of “Bearish” is based on expectations for long-term investors. My key risk avoidance method is lightening up positions when I expect a recession. Hello? That is where we are. It is not a time for aggressive action by long-term investors.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. When we are able to separate the two, it will provide more guidance on the timing and extent of the recovery. Dr. Dieli has forwarded a proposal which we are considering.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian also takes note of the improvement in corporate credit spreads.

David Moenning: Developer and “keeper” of the Indicator Wall.

Georg Vrba: Business cycle indicator and market timing tools.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. The most important are summarized effectively in the Big Four.

Guest Commentary

Menzie Chinn takes a look at the CBO on the Macro Impact of Pandemic Recovery Packages Thus Far. He provides several interesting tables accompanied by excellent analysis. The counterfactual case, the economy in the absence of these programs, is important to keep in mind when assessing the cost.

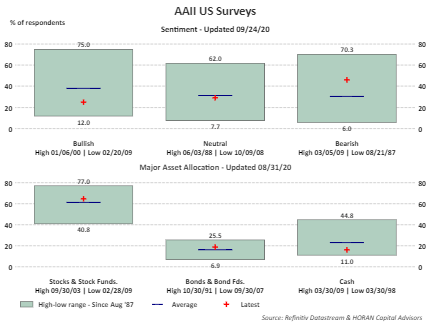

David Templeton (HORAN) reports, Individual Investor Sentiment Not Matching Actions.

He compares sentiment readings with the percentage of investment dollars allocated to stocks—65%, just above the long term average.

Final Thought

We have known a lot about the problems faced, possible solutions, and what we needed to do. There is always a debate over policy alternatives, but this one turned into a disagreement about basic facts. As you can see from the timeline, it began in in April.

It is a continuing source of frustration for my work on this series. Mrs. OldProf reports that I am sometimes a little grumpy. Hard to believe. New readers do not have the background and assume that I am arguing a political case. My causal chain is what yours should be: Evidence -> Analysis -> Investment Conclusion. I can then choose whether to vote my pocketbook.

These days so many have this causal chain: Politics-> Evidence and Analysis-> Strongly held conclusions.

I have had a long career with many stretches of market irrationality – exuberant or otherwise. I have never seen a time when it was so difficult to focus on investments.

My Current Conclusions

- Pandemic. The problem is not “solved.” Rapid reopening will lead to a level of illness and death that many citizens and leaders will not accept. This means continuing restrictions until other mitigation becomes effective.

- Economy. It has stalled after a modest recovery. Most of the data is directional, not a measure of magnitude. The exceptions are retail sales (helped by government aid) and employment, which I believe to be significantly overstated.

- Earnings. Holding a good level based on stated company guidance and analyst forecasts. We shall see.

- Stocks. Vulnerable for the above reasons and the narrow market leadership.

I cannot change anyone’s politics, nor do I wish to do so. My goal has been political agnosticism – making good returns regardless of who is in power. I know it is a familiar refrain, but I strongly urge all investors:

Look at data! Find some solid neutral sources to help in interpreting it. Make your investment decisions on that basis, not on how you plan to vote.

A Special Opportunity

Whenever there is an especially important issue, I generate a white paper. Recently I focused on finding and measuring portfolio risk. I think you will find my method to be helpful and timely. Please also consider joining the Great Reset group. This drives my own investment analysis, and (I hope) inspires others. Join in my Wisdom of Crowds surveys. I need more wise participants! The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

There is no charge and no obligation for either the Portfolio Risk paper or the Great Reset Group. Just make your request at my resource page.

I’m more worried about

- Pandemic expansion at the sites of natural disasters. Each is a problem by itself. In this case the sum is more than the parts.

- Cooperation on needed policies like more unemployment help and aid to local governments.

- Post-voting social unrest.

- Government funding. The agreement for a “clean” bill is not holding. (Reuters).

I’m less worried about

- The formal transition of power in the event of a Trump loss. Republican lawyers brush off Trump’s election comments

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All