Should Investors Change Course Because of the POTUS Diagnosis?

Membership required

Membership is now required to use this feature. To learn more:

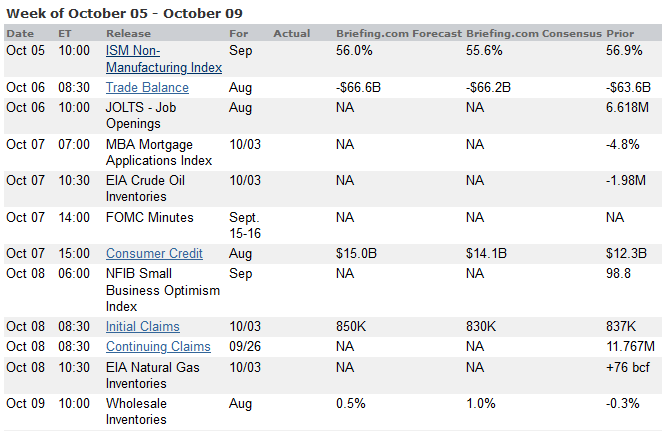

View Membership BenefitsWe have a modest economic calendar including the ISM non-manufacturing index, JOLTS, jobless claims data, and the NFIB index. The Fed minutes from September’s meeting will be released. The Vice-Presidential debate is set for Wednesday.

None of this will lead the daily news headlines as everyone monitors President Trump’s condition. This is important for many important reasons not the least of which are national security and the economy. That said, investment decisions can have long-lasting significance and decisions are in our own hands. It is important to ask:

Should investors change course because of the President’s illness?

Last Week Recap

In my last installment of WTWA, I began a review of key elements during the pandemic emphasizing what knowledge was available at each stage. I also wrote, “The first Presidential debate is scheduled for Tuesday evening. It will command a lot of attention, but probably will not be a market-moving event.”

There certainly was plenty of attention as pundits of all stripes described how terrible it was. Opinions were reinforced on both sides as everyone claimed victory. By Friday, this did not matter either, as attention turned to Pres. Trump’s COVID-19 diagnosis.

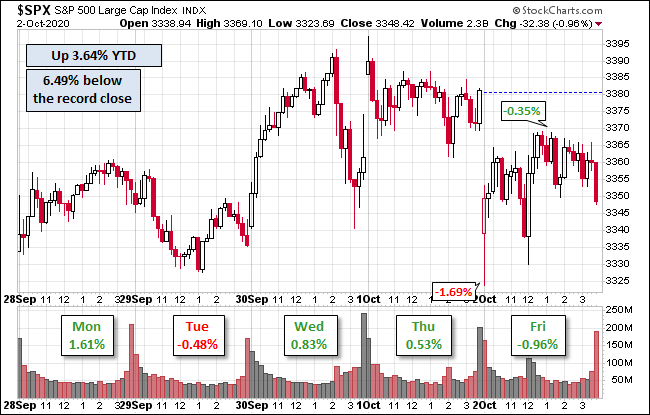

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version of the prior week. The callouts also show the large range of Friday trading after the POTUS COVID announcement.

The market gained 1.5% on the week. The trading range was 5.3%, higher than in recent weeks. To help readers keep perspective, I provide regular updates of historical and expected volatility in my Indicator Snapshot (below).

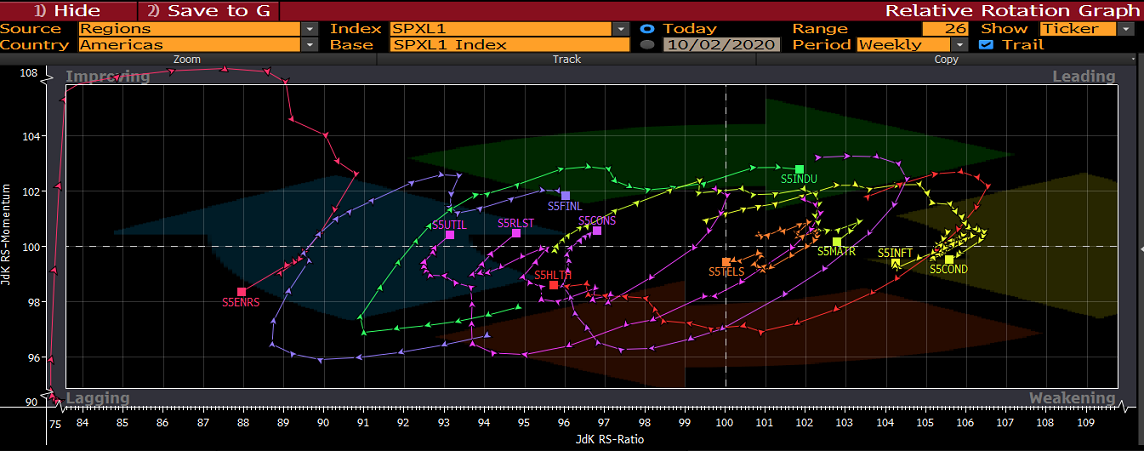

The weekly sector chart shows the sources of the action. Readers seemed to prefer the longer time frame, so I am showing the 26-week version.

Juan Luque, the member of our trading team who works most closely with these trends, provides some additional interpretive information this week. (I am doing only light edits to these comments so that readers can learn official “traderspeak.”)

Many readers might wonder how these charts are made and what they measure. As I have mentioned before, the RRGs are the visual representation of the performance of instruments relative to a benchmark. The Horizontal axis is the RS-Ratio, which measures the trend and its relative strength. The Vertical axis is the RS-Momentum, which measures the rate of change of the trend. The lines in the chart have different colors all with a defined meaning. In traffic lights Red means stop and Green means go. Similarly, in the RRG the sectors in redish fonts represent weak momentum and weakness and Green represents strong momentum and relative strength. The background colored arrows show the theoretical movement around the benchmark and are also displayed in the same color arrangements.

This week shows the continuation of gained momentum and strength for utilities, real estate, and consumer as they have crossed to the improving quadrant. Financials and industrials maintained their strength. It is interesting to see the energy sector trapped yet one more week in the lagging with no sign of recovering.

(The sector names are here. The Bloomberg symbols add “S5” at the start of the name. The small square is the current value and other points are the history).

Noteworthy

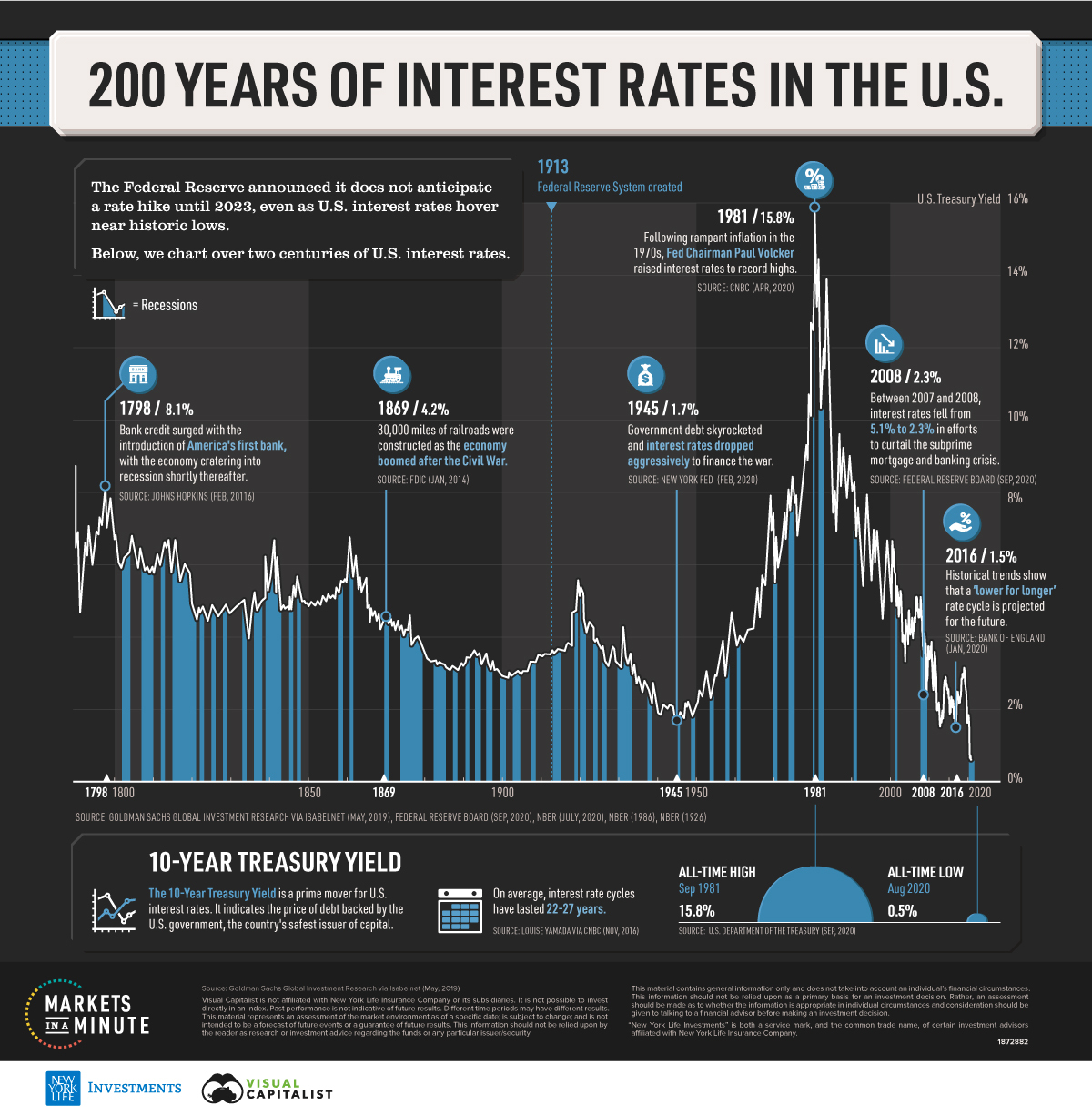

The current investment climate is anchored by extremely low interest rates and low inflation. The Visual Capitalist illustrates just how rare this is.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are more important than ever. As we look for turning points and the sustainability of the rebound, these are the earliest clues. His latest update shows all three of his time frames firmly in positive territory. Among his conclusions he emphasizes the “decisive” importance of the pandemic and also notes the following:

Consumer spending in my opinion remains the single most important metric of economic progress under the pandemic. So far, surprisingly, it has held up, even after the termination of emergency Congressional assistance.

The Good

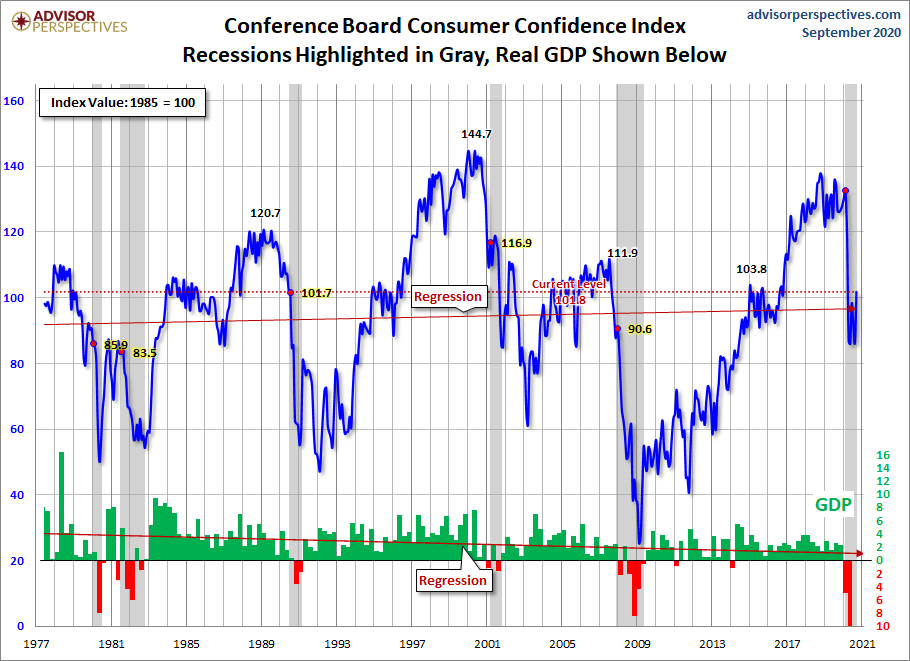

- Consumer Confidence for September from the Conference Board was 101.8, much higher than the expected 88.5 or August’s (upwardly revised) 86.3). Jill Mislinski has the best chart on consumer confidence and a good post on past data and interpretation.

- Rail traffic continues to improve reports Steven Hansen (GEI). While carloads are deep in contraction “rail is on an improving trendline.”

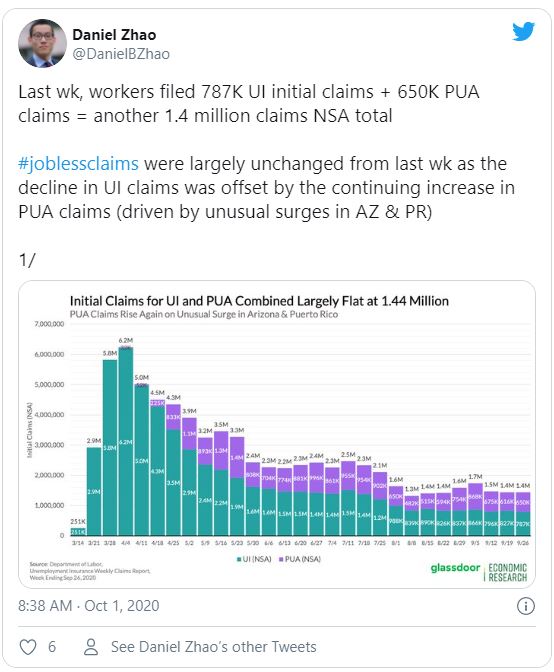

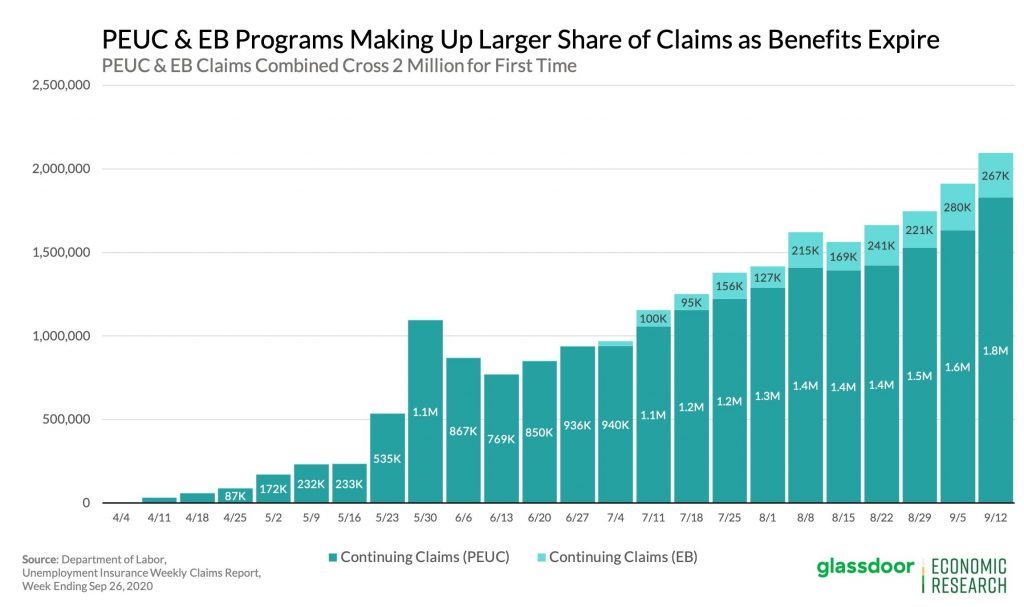

- Initial jobless claims decreased to 837K, better than expectations of 850K, and the prior week’s 873K. UPFINA (via GEI) reminds us that California is not currently accepting claims, so there may well be an increase when the state resumes claim processing. The post includes the informative chart from Daniel Zhao’s Twitter feed.

- Continuing claims decreased to 11.767M from the prior week’s (upwardly revised) 12.747M. (also from UPFINA and @DanielBZhao).

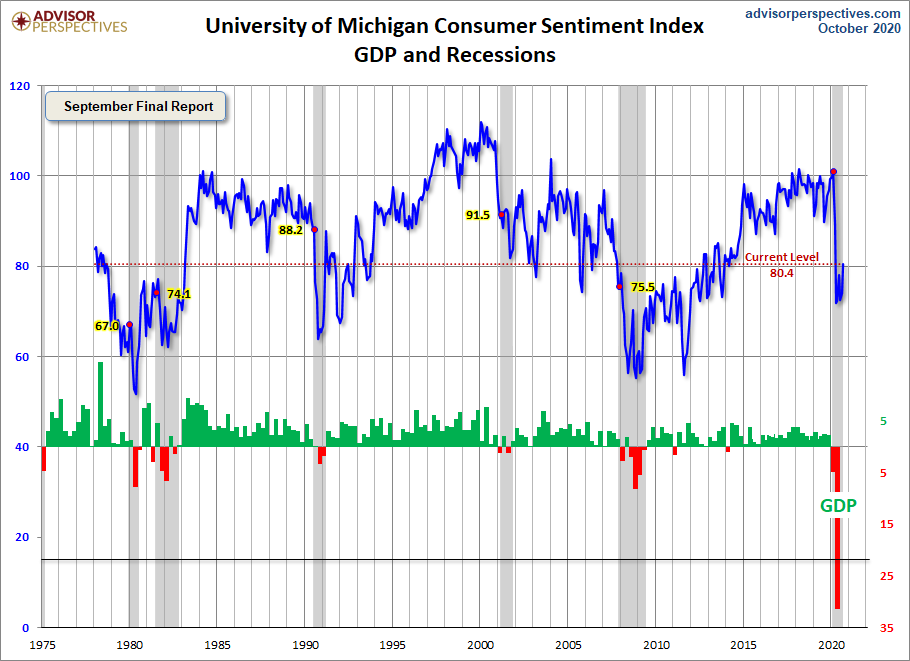

- Michigan Sentiment for September showed continued strength with a reading of 80.4. This beat expectations of 79.0 and the preliminary read of 78.9. Jill Mislinski’s chart helps us keep this in perspective.

- ADP Private Employment for September increased by 749K, beating expectations of 600k and August’s 481K (which was revised up from 428K).

- A government shutdown has been avoided, at least until December 11th. (Vox).

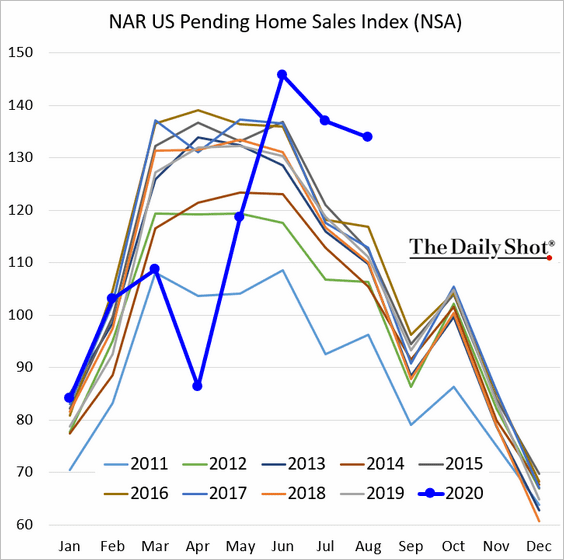

- Pending home sales for August showed an increase of 8.8%, much better than the expectations of a 3.2% gain and July’s 5.9%. (Calculated Risk).

- Construction spending for August increased 1.4%, beating expectations of 0.8% and July’s 0.7% (revised up from 0.1%).

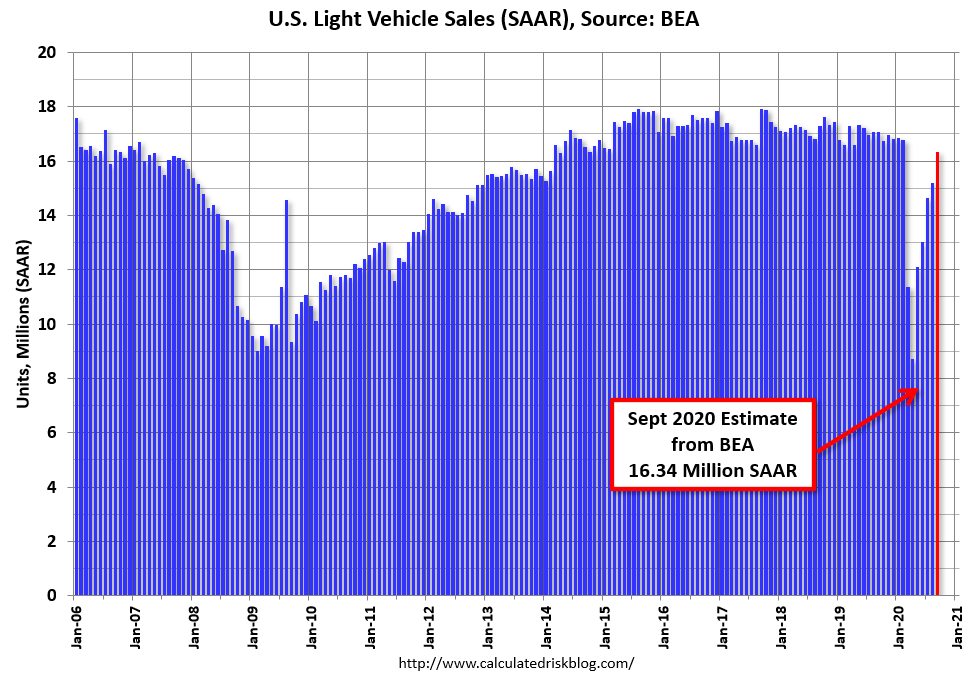

- Light vehicle sales for September increased 7.6% from the August rate to 16.34 million (SAAR). (Calculated Risk).

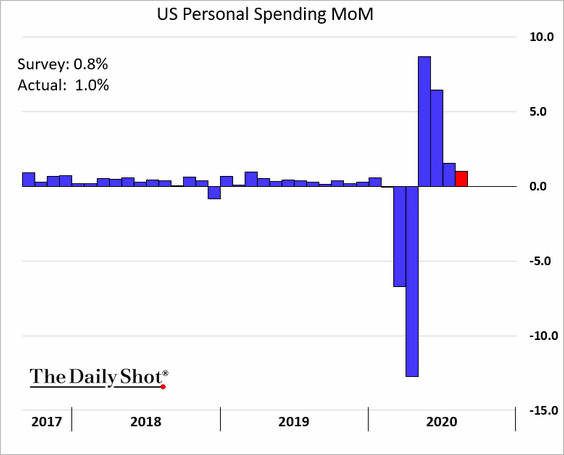

- Personal spending for August increased 1.0% beating expectations of 0.6% but weaker than July’s 1.5% (downwardly revised from 1.9%).

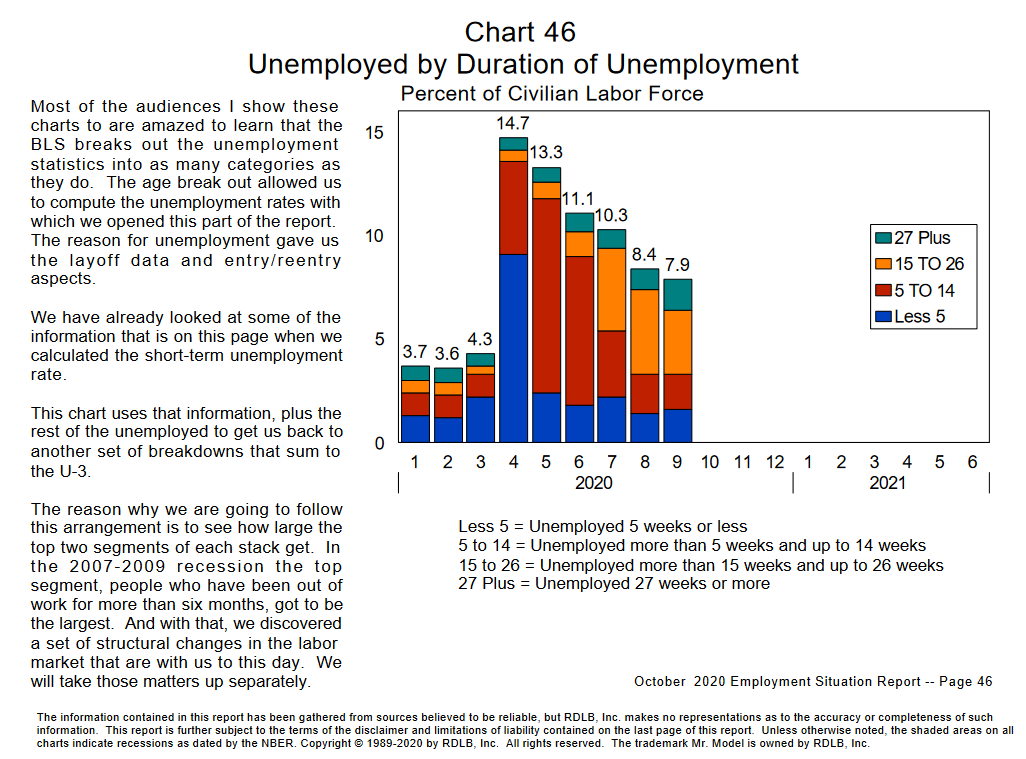

- September Unemployment declined to 7.9%, beating expectations of 8.2% and the August rate of 8.4%. Bob Dieli’s excellent monthly report on employment highlights the most important factor in this data series: how long people are out of work.

The Bad

- The ISM Manufacturing Index for September registered 55.4%, slightly worse than expectations of 56.0% which was also August’s level.

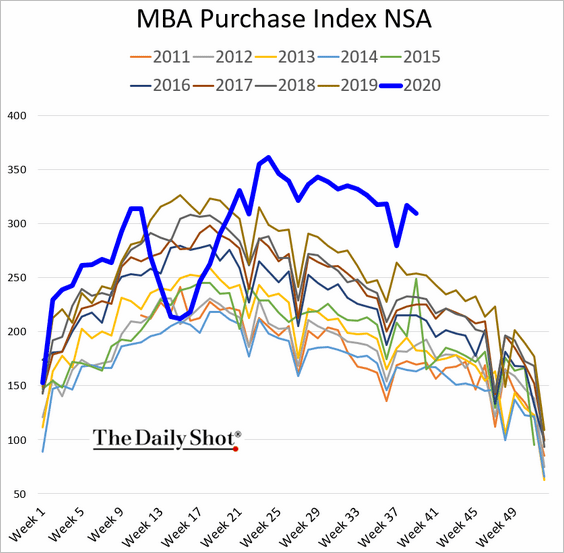

- MBA Mortgage Applications rose 6.8% versus last week’s 2.5% decline. The overall pace still looks good. (Calculated Risk).

- Hotel occupancy has declined further to 48.7%, down 31.5% year-over-year. Calculated Risk highlights the combined effect of natural disasters and the pandemic.

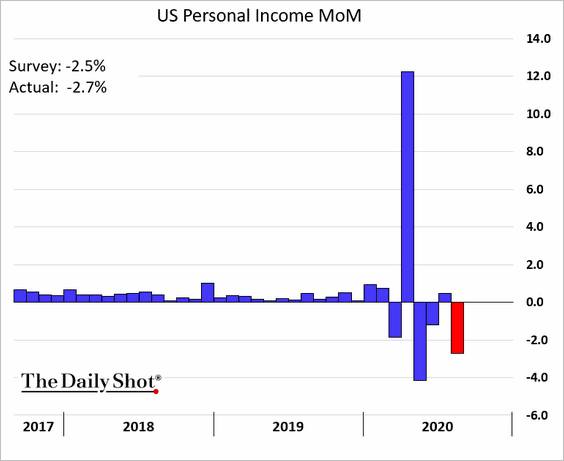

- Personal Income for August declined 2.7%, worse than the expected 2.0% drop. July’s gain was 0.5%, revised up from 0.4%.

Part of this decline relates to benefit payments.

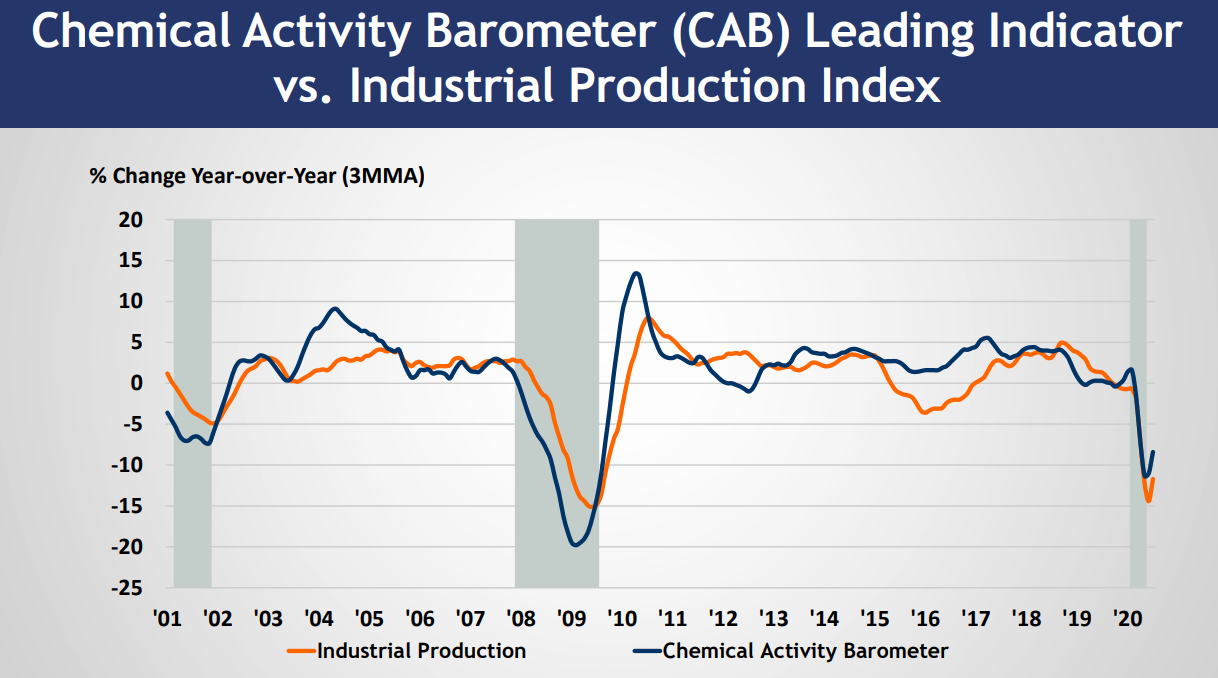

- The Chemical Activity Barometer remains in recession territory. Steven Hansen (GEI) shows the relationship with industrial production.

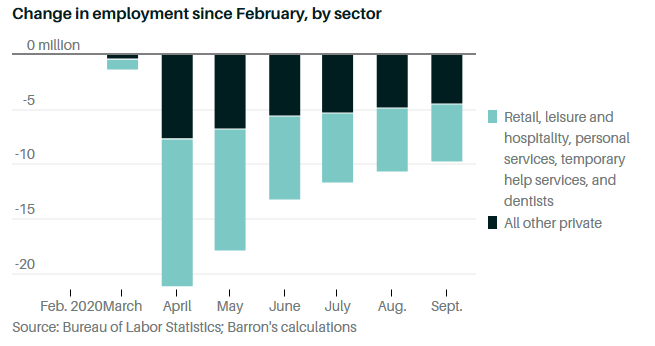

- Non-farm payrolls for September increased by 661K missing expectations for a gain of 800K and much lower than the (upwardly revised) gain of 1.489M in August. Private payroll gains were a little stronger. Barron’s Matthew C. Klein concludes, The Jobs Recovery Has Ended—and May Be Reversing.

Concerning government policy effects, he writes as follows:

Government policy has been compounding the woes of the private sector. First, the boost from Census hiring has already begun to unwind even though the job of counting Americans hasn’t finished. Meanwhile, the collapse in state and local tax revenue—and the federal government’s failure to make up the shortfall—is leading to massive cuts in employment. Public schools and universities have shed about 8% of their staffs, while cities and municipalities have also shed more than 5% of their other workers. Overall, government employment other than the Census has dropped by 1.2 million people since February—about 10% of the jobs lost since February.

Perhaps most important has been the end of government income support since the end of July, with enhanced unemployment benefits and forgivable loans for businesses no longer available. Even though more people are working, the lack of aid has subtracted tens of billions of dollars of income from Americans’ pockets each week.

All this means less spending—and fewer jobs—than there otherwise would be. We are already seeing the impact in the new rounds of layoffs and furloughs announced by companies such as Allstate, Walt Disney, Marathon Petroleum, and the airlines. Those job losses won’t show up in the government data until later in the year, but they will eventually lead to lower revenues for businesses and lower incomes for workers, further sapping the recovery of momentum and perpetually leading to a new downturn—unless the government chooses to make workers and businesses whole with a new round of aid.

The Ugly

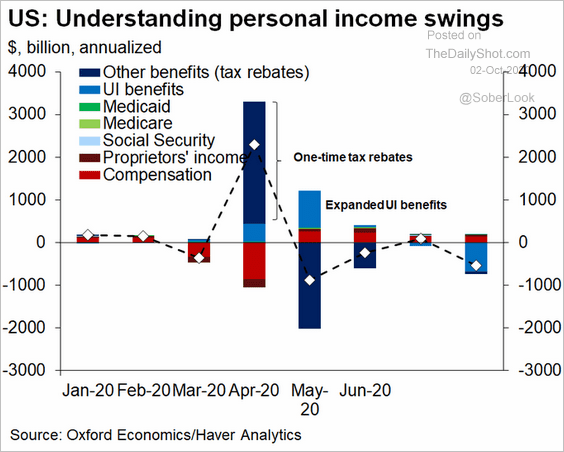

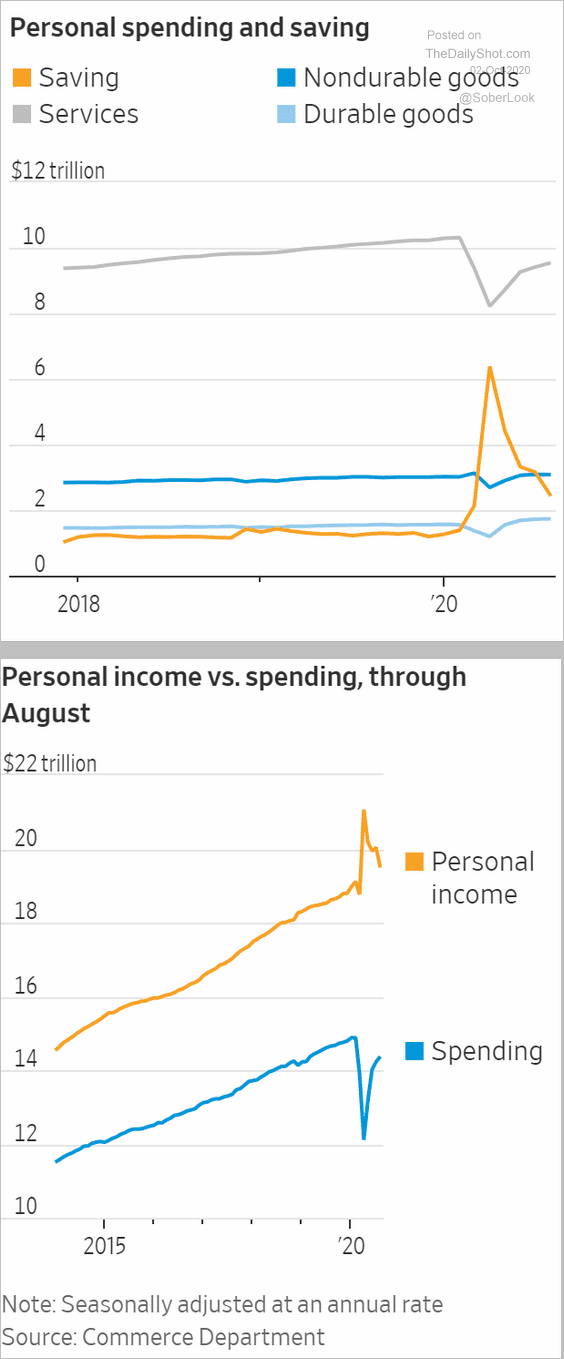

Personal spending, income, and saving. It does not add up any better for individuals than it does for government.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

We have a relatively small economic calendar featuring ISM non-manufacturing and the NFIB small business optimism index. Unemployment claims data and mortgage applications provide a high frequency read on two key economic indicators. Some will try to interpret JOLTS as showing something about job creation, but it is not useful for that purpose. The Fed-obsessed will try to squeeze a little more information from the FOMC minutes.

The first Vice-Presidential debate is scheduled for Wednesday night. In the absence of some horrific blunder, I do not expect a significant market reaction.

None of this will matter much in an environment where everyone is concerned about the President’s condition.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

None of the regular market threads will matter until there is more clarity about the President’s condition. The implications are broad — national security, the economy, and current policy initiatives. The duration of his illness is crucial.

It is uncomfortable to think and write about our personal interests in such a time, but we really have no choice. The big issues are out of our control; our investments are not. When there are important events there is nothing wrong about stopping to think about the personal implications. In fact, it is a responsibility to avoid the potential for live-changing mistakes. This brings us to the necessary but awkward question:

Should investors change course because of the President’s illness?

Background

This is not a political article! It is focused, as always, on helping readers find the best investments.

Sometimes political events are the key drivers of public policy and the economy. It is foolish for an investor to ignore such effects. It is equally foolish to allow our opinions about candidates to determine how we will invest.

My intention here is to analyze the current situation in the same dispassionate way that I approach housing stocks, free trade, or the Fed. I use my training and experience to find the best sources on the subject. I draw and share my own conclusions and allow readers to evaluate evidence for themselves.

Not the Topic

I am not writing about the current state of the President’s health. I wish him, and the First Lady a speedy and successful recovery – the same sentiment I have for everyone in this situation. I will follow the updates with hope, as will everyone else.

I will not engage in recriminations, finger-pointing, timeline tracing, speculation about conspiracies, or anything else of that ilk.

I am writing about what it means for investments. I know that many will not agree with my conclusions. After fifteen years of writing, I am familiar with objections and criticism. I ask only one thing:

As you read, try to substitute a neutral economic term like “housing market” or “employment.”

Analysis

As you would expect, I have read many articles and listened to plenty of pundits on the implications of the President’s COVID diagnosis. Most of them were awful. As always happens in situations like this the interviewer asks the subject the question of the moment, regardless of the subject’s expertise. Naturally, he has an opinion and is willing to provide it.

One of the stronger CNBC anchors was interviewing an excellent economist and former Fed member whom I have followed for many years. She asked what he thought about the election. He said he did not know who would win but it would be very close. She asked who won the debate. He said that he listened with the sound off and went by body language, the way most people did! He felt the President had won.

My problem with this is that the interviewee spoke knowledgeably and at length about subjects in his wheelhouse. The casual listener could be forgiven for giving similar credit to the final remarks, even though they are subjects about which he knows absolutely nothing! His opinion is just like that of a Letterman man on the street.

That is the challenge of trying to bring any clarity to this subject.

The Most Important Issues

National security

The message sent to the rest of the world is the most important consideration. Even the hint that no one is in control or that the country is especially vulnerable should be avoided. This carries with it some corollaries. From Justsecurity.org.

What procedures for a temporary transition of power are in place? The most important is the 25th Amendment of the Constitution. The President can voluntarily pass control, which some have done while undergoing surgery. There is also a provision for an involuntary passage of power:

Section Four of the Amendment has drawn particular attention in the popular media and news commentary alike in recent months. This provision provides a strikingly compressed constitutional process whereby nine government officials could separate the President from his powers and duties, with the Vice President immediately becoming Acting President. If the President should contest this declaration of inability, the amendment requires both houses of Congress to assemble within 48 hours, and then (by a two-thirds vote of each body) to resolve the question of inability within three weeks. Depending on the vote, the President may resume his official duties, or the Vice President may continue to serve as Acting President.

There is no experience or precedent for this provision, including whether these actions are justiciable. Read the source for a lot more detail. For national security purposes, it is probably enough that a procedure is in place if there is a need for a speedy decision.

Updated information

Who should know how the President is doing? Roger Pilon, founding director emeritus for Cato Institute’s Robert A. Levy Center for Constitutional Studies and former Reagan advisor opines that the White House has every right to manage information. He cites personal protections about health information and the precedent from prior Administrations.

[Jeff – This power might be used quite wisely. The point is not about curiosity, but leadership continuity. It might not always be helpful. Consider, for example, the infamous claim by Gen. Alexander Haig, Chief of Staff for Pres. Reagan at the time of the Presidential assassination attempt. Stepping up to the podium at a news conference, he stated:

Constitutionally, gentlemen, you have the president, the vice president and the secretary of state, in that order, and should the president decide he wants to transfer the helm to the vice president, he will do so. As for now, I’m in control here, in the White House, pending the return of the vice president and in close touch with him. If something came up, I would check with him, of course.]

What about the rest of the campaign?

The election is already underway. For now, the President’s schedule does not include any in-person events. That is not true for Vice-President Pence, but that might be revised.

The second Presidential debate is near the end of the President’s quarantine period, so it is also doubtful.

What if the President must withdraw?

There are procedures in place for all possibilities, but it depends on the timing. The election has already begun for millions of mail-in voters. It is too late to change the name on the ballot. We should remember, however, that despite the name on the ballot, voters are choosing a slate of electors pledged to that candidate. They will vote at the meeting of the electoral college.

- If a change is needed before the election, both parties have provisions for the National Committees to choose a replacement. This has never happened.

- After Election Day, the question is whether the candidate is the “president-elect.”

- If so, the vice president-elect becomes president. This is clear if it occurs after the Electoral College votes on December 14th.

- It might also be true if it occurred before the Congress officially counts on the votes on January 6, 2021.

- There could be a challenge of electors in various states. Any decision there would inevitable be appealed to the Supreme Court.

What if he cannot finish the campaign? What if Biden cannot?

What if a candidate wins the election, even if incapacitated? Or becomes incapacitated between election day and the inauguration. It then depends upon how the electors vote and whether they are bound by state law prohibiting “faithless electors.” (Good summary of possibilities in the Washington Post).

- Some are free to vote as they wish.

- Some are required to vote for the candidate on the ballot, no matter what.

- Some are required to vote for the party of the candidate on the ballot.

What if the election is challenged in the streets?

The recent clashes between demonstrators has heightened concern about the possibility for a violent mass rejection of the election outcome. No one can predict this with certainty, but there is some research available. Here is an academic perspective from Ore Koren of Indiana University. He examines the factors behind past electoral violence and reaches these conclusions:

Is post-election violence impossible in 2020 America? No.

However, data suggests it is unlikely.

Ninety-five percent of the 12,607 political demonstrations in the U.S. between May 24 and Sept. 19, 2020, were peaceful. There were 351 other kinds of incidents, including imposing curfews and perpetrating physical attacks. In 29 of those, there was violence against civilians, where 12 people were killed, nine of them by the police. And in an additional five drive-by shootings, three police officers were killed by the extremist group the Boogaloo Bois.

Considering the number of people involved in the recent Black Lives Matter and COVID-19 protests, and the fact that many were heavily armed, these casualty figures are surprisingly low. According to the data, the majority of deaths were caused by police, not vigilantes or protesters, and all of the perpetrators (with the exception of two drive-by shooters), police and civilians alike, were taken into custody.

What if this goes to a Supreme Court decision?

The issue would probably begin with challenges in state courts. The Supreme Court would act swiftly to stay within the election and inauguration timeline. No one really knows how it would turn out.

Investment Implications

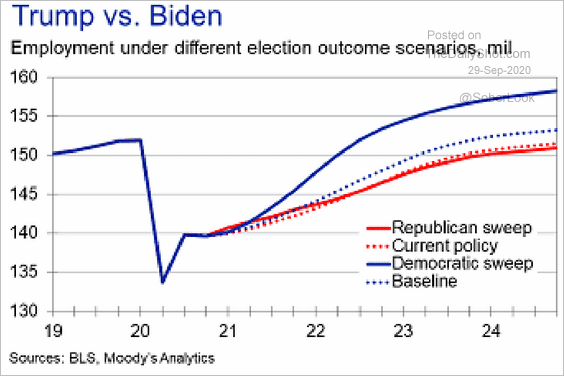

To answer this question, the investor needs to decide several things – the winner, the policy differences, the Congressional support, and the chance that proposals will be passed.

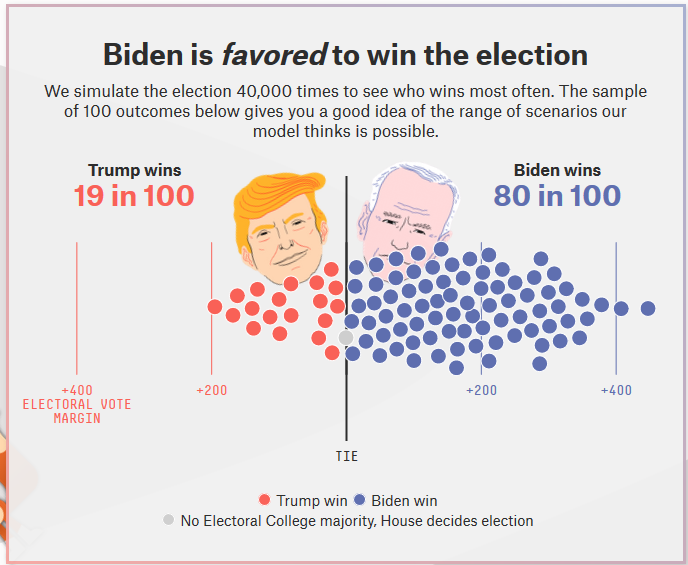

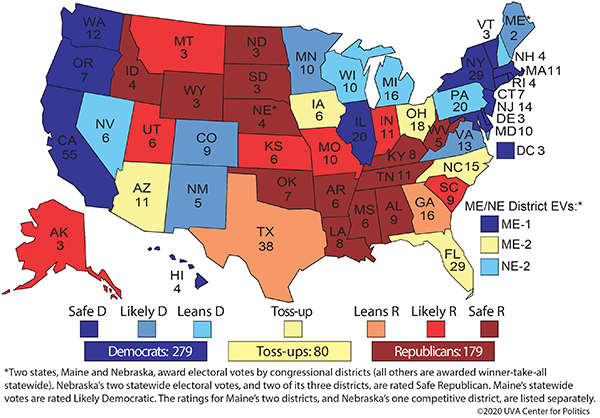

- The winner is likely to be Biden, possibly in a landslide. The best sources on election forecasting are FiveThirtyEight and Center for politics led by Dr. Larry J. Sabato.

- FiveThirtyEight’s current forecast, based on analyzing state-level polls and simulating results:

- Dr. Sabato’s forecast, also using state-level polling.

Does this really matter in the short run?

Even if you knew the election outcome, the policy effects are uncertain. People overreact to the election of a candidate they do not favor. In fact, the overall stock returns vary little by party.

Most would be surprised by the likely result of a Democratic sweep, for example. The logic behind this conclusion is the increased chance of a significant stimulus bill.

As always, I have tried to separate my personal conclusions. I’ll highlight those in today’s Final Thought.

Ideas for Investors

I have switched the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. It has turned out to be more comprehensive than it was as a part of WTWA, and more difficult to do. It is important to include the Great Reset concept as well. I am starting to see more ideas worthy discussing. I may not be able to do this weekly, and it might be a bit shorter.

I have given this a lower priority because there is no rush. The conclusion of our research so far is that long-term investors have many months. Traders might want to show some agility.

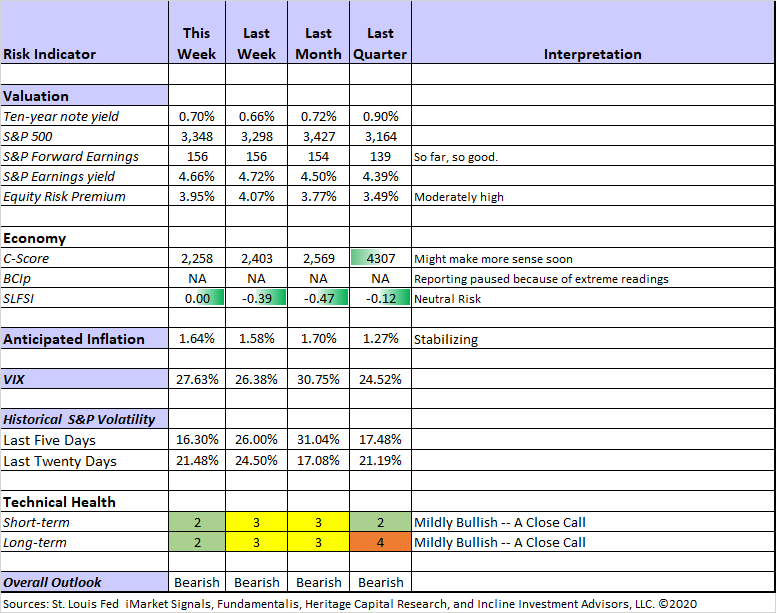

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

The technical indicators have moved slightly above key levels. A modest decline could send them back into neutral territory. My overall rating of “Bearish” is based on expectations for long-term investors. My key risk avoidance method is lightening up positions when I expect a recession. Economic indicators remain in recession territory, so it is wise to be wary.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. I expect to have an improved interpretation for this soon. Currently it is not providing much help about when we will see the end of the recession.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian also takes note of the improvement in corporate credit spreads.

David Moenning: Developer and “keeper” of the Indicator Wall.

Georg Vrba: Business cycle indicator and market timing tools.

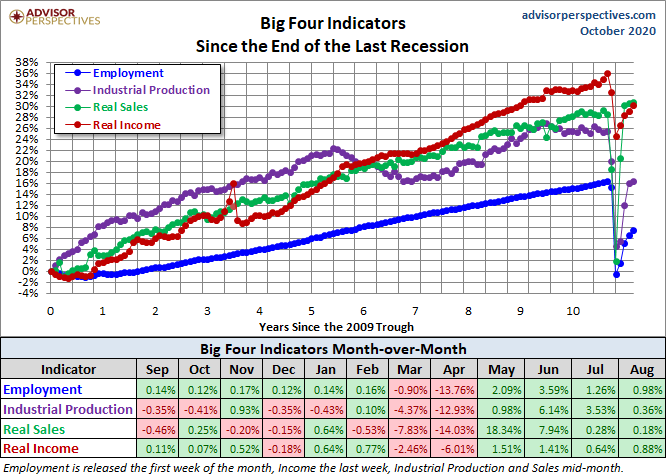

Doug Short and Jill Mislinski: Regular updating of an array of indicators. The most important are summarized effectively in the Big Four.

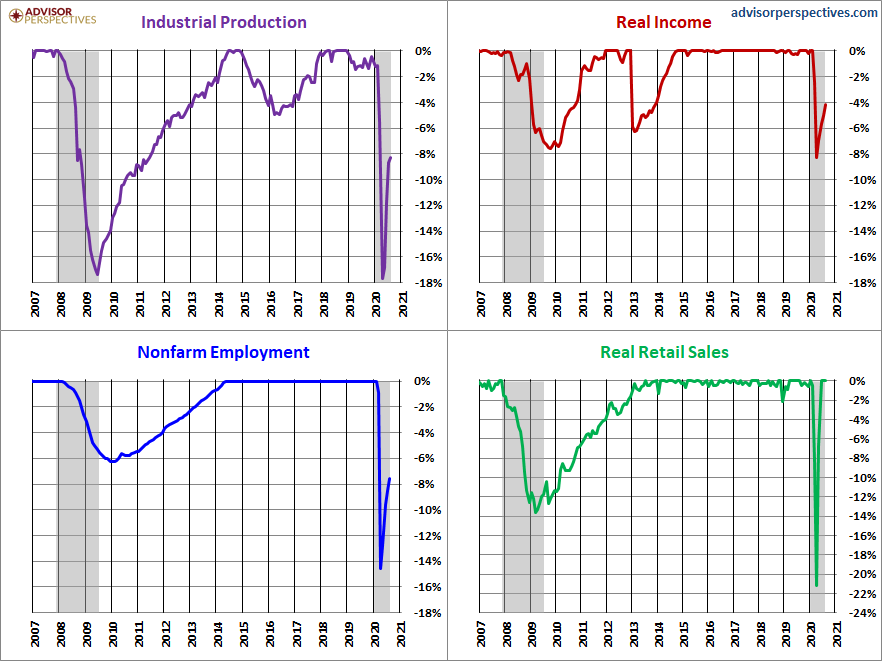

The chart and table show an impressive four-month block that is all green. It underscores the directional shift in all indicators after the policy response to the initial COVID shutdown. It is important to consider magnitude as well as direction. This chart illustrates the disparity in the rebound among the Big Four.

Only retail sales has regained prior levels. Other indicators show plenty of work ahead of us.

Guest Commentary

I strongly recommend J.P. Morgan’s Guide to the Markets. It is a terrific source of data. Page through it and you will find yourself seeing some fresh ideas.

I always listen to Dr. David Kelly’s quarterly presentation. He covered many of the topics I am citing today. While I make my own decisions, I am delighted to have experts on my side of key issues.

Our regularly featured source, Brian Gilmartin, also shows how his own work links to the “Guide to the Market” update.

Personal Note

This post was a special challenge. I know that some who disagree will take it as a reason for a political diatribe. I always try to respond constructively and politely to comments, but I am not interested in arguing politics. It is stressful enough.

Mrs. OldProf asked me if there were not an easier way to blog. I told her that two of the most popular writers featured dark viewpoints, conspiracy theories, and reinforcement for what people already believed. These were stories that were easier to produce. She asked me if they were profitable, and I admitted that they were the two leading moneymakers. She then asked if I could do it, and if it would be fun. I said I certainly could, and it might be fun, but not very helpful to investors. Her line of questioning stopped.

If WTWA disappears and you see a new blogger highlighting themes out of fictional thrillers and movies, pounding on current investor worries while using a lot of schmooze, soliciting a lot of lightweight fluff pieces to build page views— well, you might have spotted my new approach to “semi-retirement.”

Final Thought

I will take up the key points of the investment issue, explain which evidence is most persuasive, and provide some investment implications.

- Most of the issues are linked to a close election result, which is unlikely. Dr. David Kelly’s presentation said that this might happen when one state made the difference, something that had only happened once in history. Like me, he wanted to avoid discussing a personal preference, but he stated that a sweep in either direction would be market friendly. As I noted above, I have more expertise on this than he does, but I like having him on my side. [Confidence level – high].

- Why cite polls that were “wrong” in 2016? This might be the biggest investor mistake, something that has rippled through many fields in the last four years. You have a choice. Methods that have worked well for decades? Or Facebook and hunches? I read and analyze them all. A few key points:

- 538 gave Trump a 30% chance. That does not mean that they “called” the election. The Packers have a 30% chance of losing tomorrow, but I sure hope they do not. Mrs. OldProf is always very unhappy when that happens, and it is the early game. Nonetheless, 30% events happen – and they happen about 30% of the time. A forecast is “wrong” if it extrapolates a 70% probability to 100%.

- It is popular to disparage polling, discussing the “hidden” Trump vote and unreliability of answers. Pollsters paid attention to the 2016 results. Their methods improve. There is also a big difference in respondent willingness to say “Trump” now than in 2016. It is a mistake to take one event and make a broad inference about methodology.

- The COVID diagnosis reduces Trump’s chance of victory. It restricts his campaign style and highlights an issue that helps Biden.

- As an investor, I am not worried about the election of either candidate. We know what a Trump Administration is like. A Biden Administration would initially focus on improving the economy. Think stimulus and tax increases on the very high-income people. Health care and regulation would eventually change of course, but gradually.

- The average observer overestimates the chance of a President to pass legislation. There are many obstacles. In a Biden victory, the key thing to watch will be the filibuster. Traditionally, many Democrats have opposed any changes. Should that change, a Democratic sweep would have more policy implications

What Should Investors Do?

I continue my bearish posture for long-term investors, but it does not relate to the election odds. I believe that the magnitude of the economic recovery has been significantly overstated. The number of jobs created, and jobs lost do not properly equate.

The market is betting too much on a near-term vaccine and widespread usage.

Caution does not mean an “all out” decision. Look for a cautious course, partial allocations, or hedges. There will be much better entry points soon, and the best stocks will not be the current leaders.

Investors have no control over important events, but they can manage their own reactions.

A Special Opportunity

Whenever there is an especially important issue, I generate a white paper. Recently I focused on finding and measuring portfolio risk. If you have not requested your copy, I strongly recommend it. Please also consider joining the Great Reset group. This drives my own investment analysis, and (I hope) inspires others. Join in my Wisdom of Crowds surveys. I need more wise participants! The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

There is no charge and no obligation for either the Portfolio Risk paper or the Great Reset Group. Just make your request at my resource page.

I’m more worried about

- A second pandemic wave. Whether on campus or in areas where people have been too confident. I am worried about my many friends and relatives in Wisconsin.

- Impulsive overreaction to the President’s illness.

- Continued stalemates on needed assistance. There are too many issues and poor setting of priorities.

I’m less worried about

- The formal transition of power in the event of a Trump loss and complaints about an “unfair” election. If the claim is narrow – a specific issue in one state, the Supreme Court might do anything. A broad-based claim of cheating citing mail-in ballots or the like, has no chance in the Supreme Court. People over-estimate the politics of the justices. There is no way that Justice Roberts will lead a decision that undermines more than two centuries of electoral principles. He is much more likely to lead the Court to a near-unanimous decision. He would go down in history as one who saved the foundation of American democracy. I would expect a vote of 8-1.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All