“Veil after veil of thin dusky gauze is lifted, and by degrees the forms and colours of things are restored to them, and we watch the dawn remaking the world in its antique pattern.”

“Veil after veil of thin dusky gauze is lifted, and by degrees the forms and colours of things are restored to them, and we watch the dawn remaking the world in its antique pattern.”

The Picture of Dorian Gray Oscar Wilde (1854 – 1900) Irish poet and playwright

The world feels topsy turvy. We are in the midst of the sharpest recession since the Great Depression, businesses are closing left and right, and yet for many it doesn’t seem like a recession at all... and the stock market is booming? The virus, and the responses to it, have turned the world upside down. Let’s straighten out what we can.

In the hard-hit U.S., while life is creeping toward normalcy, case levels nevertheless remain elevated. Europe, which had a more vigorous response and locked down harder, initially reduced cases to low levels, but is now seeing a major resurgence. This uptrend is spooking markets which fear a return to lockdowns1.

The good news is that in both regions, as we predicted, death rates have decoupled from case rates and mortality remains below March levels. This is largely due to the improved treatments we described last quarter, a different profile of the infected (generally younger), and more extensive testing picking up more cases2. The bad news is that the experts we trust most are forecasting an increase in cases, due to the rolling back of restrictions, as well as colder weather forcing many indoors where the virus survives longer and spreads more easily. All signs indicate that we remain far away from natural herd immunity.

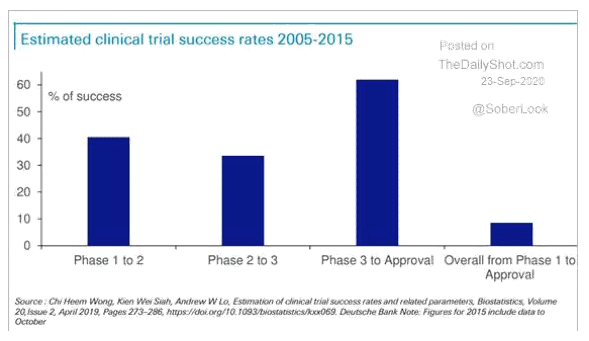

Fortunately, we are bullish on a vaccine. There are four vaccines in Phase 3 trials (the final phase) in the United States alone, with a fifth starting in October. Given the typical Phase 3 vaccine approval rates shown at right3, this seems very promising.

The experts we listen to generally seem cautiously optimistic and it would not be surprising to see at least one vaccine approval in either October or November (while approval in either month would generate an opposite political conspiracy theory, we have full expectation of a science-based process). However, we caution that the approval of a vaccine does not mean an immediate end to the pandemic. It will take a lot of time to manufacture and distribute enough doses for everyone, and even then not everyone will be willing to take it and the first vaccine may not be 100% effective4.

We are confident enough in the vaccine progress to date to make a prediction: virus-wise, things will be 90% back to normal by the middle of the third quarter 20215. By then we think a vaccine will be effective in very large swathes of the population. Even absent a vaccine, the pandemic will be eighteen months old, which is similar to the duration of historical pandemics6. Finally, monoclonal antibody treatments (like the one the President just received) are likely to be out in volume by the end of 2020 and will begin making an impact. Thus, we believe the march towards normalcy is well under way. While we have not completely built the investment portfolio around this “return to normalcy” prediction, we have indeed executed trades with this forecast in mind.

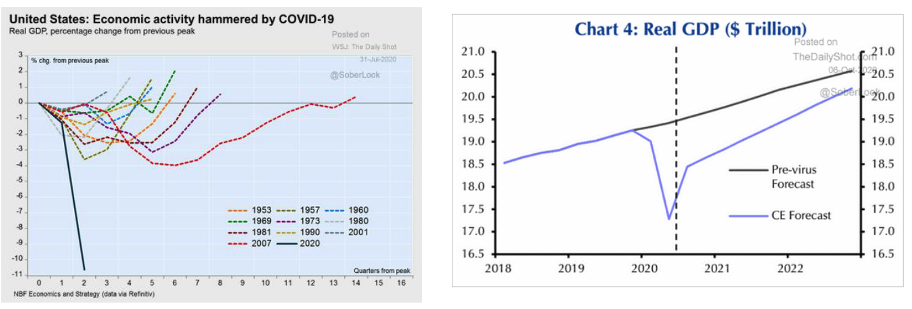

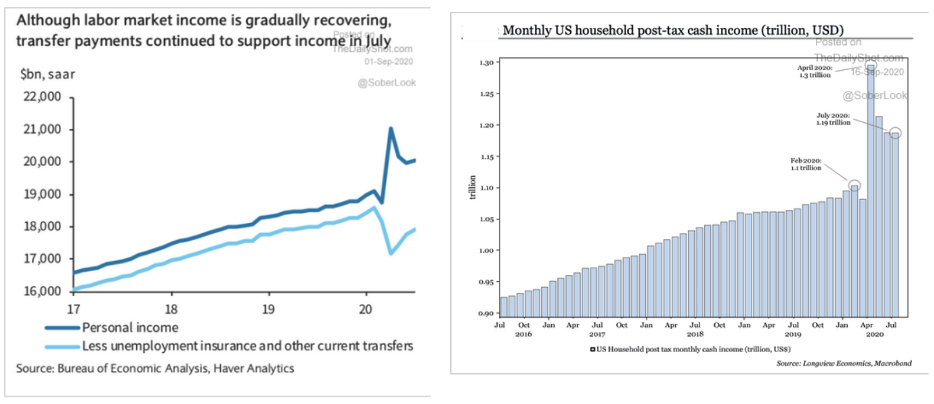

For the time being, however, we are dealing with a severe recession. In terms of GDP, the second quarter was one of the worst in U.S. history, as shown in the graphs below. Estimates are that third quarter GDP was in strong recovery mode, though not enough to make up all the lost ground, and doubts about the speed of the recovery going forward abound.

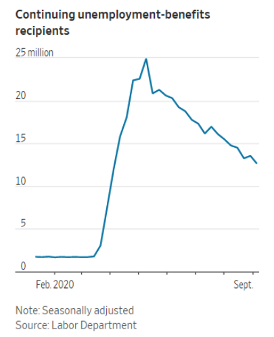

The chart below shows the damage inflicted on the labor market, and how it is healing. For context, there were 8.8 million people unemployed at the depth of the Great Recession.

No one seems to have told the stock market about all these troubles. This quarter the S&P 500 blasted to new all-time highs, thereby cementing the fastest bear market recovery in history. Despite its pullback in September, the index delivered a stellar eight percent return in Q3.

In fact, the market has been so strong it is starting to look a little unhinged; signs of excess abound. We will stick to three examples: the obvious, the egregious, and the enormous.

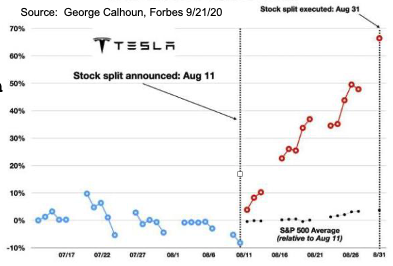

The obvious: this quarter, Tesla announced a stock split, an action with absolutely no economic consequences. Nevertheless, Tesla stock soared a staggering 70% in the twenty days after announcement. This is equivalent to slicing a pizza into sixteen slices instead of eight, and then seeing customers pay 70% more for that same pizza.

The egregious: Nikola, an aspiring producer of electric and hydrogen fueled trucks with absolutely no functional products and zero revenue was valued in excess of $30 billion after its reverse merger SPAC IPO.

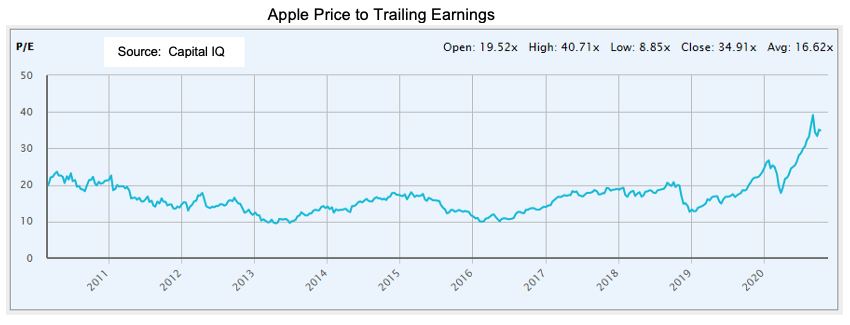

The enormous: the ascent of Apple. Observe the above chart showing the ratio of Apple’s price to last year’s earnings (P/E). For nine years, this important measure of value remained dutifully between approximately ten and twenty. A few times over the years, in tax-deferred accounts where we were free to do so, we appropriately trimmed Apple when the ratio was “high” and bought more when it was “low”. In 2019 Apple’s price in relation to its earnings started heading up... and up... and up. What changed? Certainly not Apple’s aggregate revenues or earnings, which have hardly grown over the past six years. Absent any big changes in its business, the market in Q3 2020 decided Apple was worth a cool 40 times trailing earnings and Apple became worth more than the entire Russell 2000 Index of 2,000 smaller U.S. public companies and also worth more than the FTSE 100, an index of the 100 largest public companies in the United Kingdom.

While we remain Apple fans, we have become sellers of the stock.7

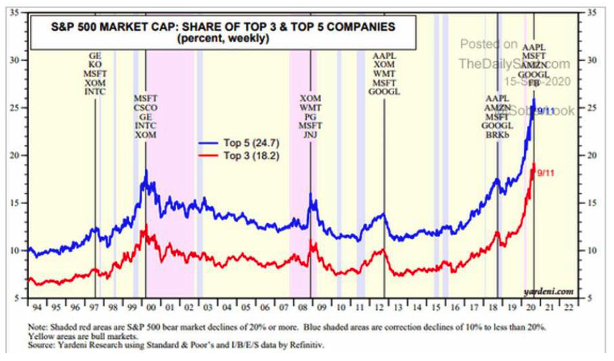

Apple is not the only stock to experience an “ever rising price” phenomenon. It is no secret that the overall market continues to be led by the bigger, techier companies. In fact, they have become so big a component of the market, they can push the entire index up while other stocks languish or lose ground. The following graph shows how the largest five stocks make up a bigger proportion of the S&P 500 than they ever have before.

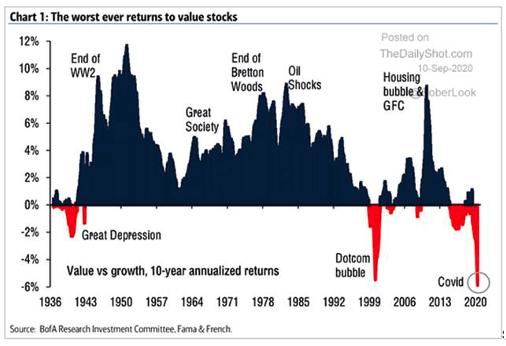

The continuing appreciation of large tech stocks has led to the greatest ten-year outperformance of growth stocks versus value stocks of all time. As you can see from the graph to the left, this is not the typical experience.

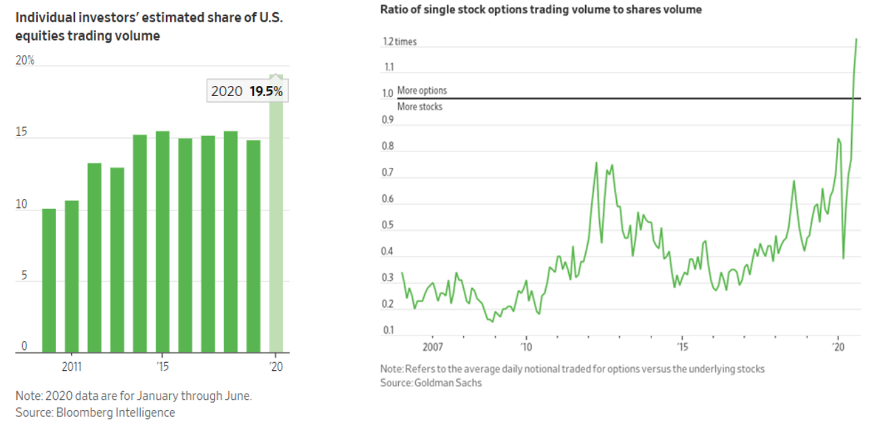

A simple and obvious explanation for some of these extremes is that individual investors are gambling and chasing stocks higher. It makes sense that with many people stuck at home, perhaps with some extra cash (and no sports to watch or bet on until recently), some would turn to the market for entertainment. It certainly didn’t hurt that most major brokerages recently eliminated trading commissions for retail investors, making this gambling activity “free”. We submit these retail investors are bidding market darlings higher and higher. Not only has retail investor trading volume increased dramatically, but the ratio of stock option trading volume relative to regular stock trading volume has spiked. When one is hooked on gambling on stocks, one soon prefers to trade options instead of regular shares because the gains and losses are so much more extreme.

The biggest reason the stock market is still booming is that this recession does not feel like the last recession. This is largely because the government response completely dwarfs the actions taken during the Great Recession. 2020 has witnessed, by far, the biggest government cash giveaway of all time. People remember the $1,200 checks mailed out to average citizens at the height of the pandemic, but the PPP “loans” were many times larger8. That they were called “loans” at all is an incredible piece of marketing since the vast majority never had to be repaid. Many businesses needed this money to survive or keep their workers employed. Other businesses (including some of our competitors) requested these giveaways when they had no interruption to their business. The free money dropped straight to the bottom line. Another important economic boost came from the extra $600 per week9 in unemployment benefits, which resulted in the majority of unemployed people earning more on unemployment than from their lost jobs. Put all these government programs together and what is the result? The first recession where the personal income of Americans actually went UP!

Remarkably, the government handed out so much money that, despite the worst unemployment this country has ever seen outside the Great Depression, personal income increased at a 12% rate. Thus, while GDP (what we produce) plummeted, personal consumption spending rose! The end result is a recession that doesn’t feel as crushing as the last one, and a stock market that has quickly recovered its losses10.

How is it possible that the government can spend this much money? One answer is that there has been a change in thinking and now both political parties are on board with massive deficit spending11. Another answer is that the government spending has been enabled by central bank money printing.

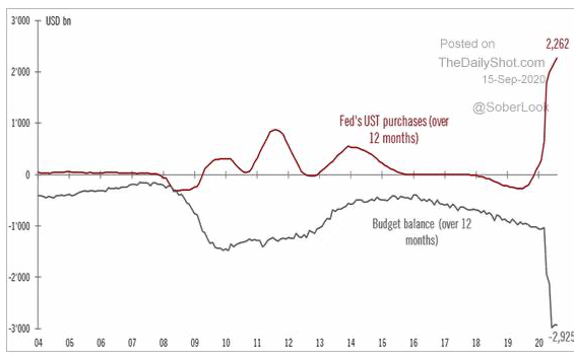

During this recession, the Fed has both put newly-printed money into the hands of investors via buying bonds that already existed12, and put newly-printed money into the hands of the government by buying new bonds that the government is creating and selling. This is illustrated beautifully by the following chart which shows the magnitude of recent government action. The blue line represents U.S. government issuance of new bonds, i.e. the debt it must issue to finance its deficit spending. As you can see, the deficit exploded by an additional $2 trillion over the $1 trillion deficit it was already running pre-Covid. The red line is the

Federal Reserve’s purchase of Treasury bonds. The Fed purchased bonds with newly printed money to the tune of about $2.3 trillion dollars over the past year. Note the degree to which both activities (money printing and government deficit spending) greatly surpassed what took place during the Great Recession and Global Financial Crisis.

The balances reflected above indicate the entire increase in government spending was paid for by printing money, and there was still some newly printed money left over to buy pre-existing government bonds13.

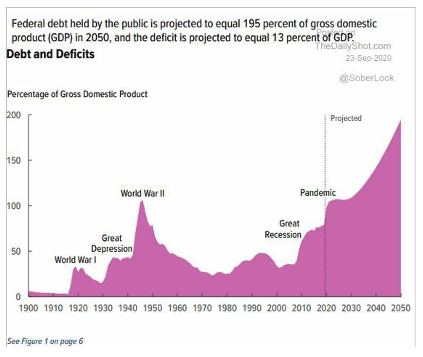

What we outlined is complicated. Just know the result: a lot of new cash and a lot of new government debt. The latter surpassed 100% of GDP for the first time since WWII and only the second time in the nation’s history14.

The implications of this debt build-up are beyond the scope of this letter, but suffice it to say we will be dealing with the repercussions long after the virus has been defeated. This year’s debt issuance is clearly unsustainable. However, just because something is unsustainable does not mean it will stop within a timeframe short enough to impact your investment decisions.

We suspect “unsustainable” can go on longer than many expect15.

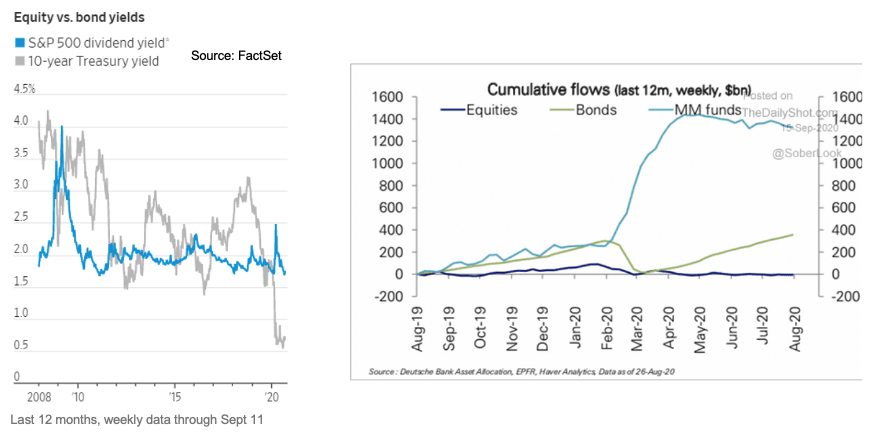

In this letter we’ve covered a lot of topics, many of them negative. However, it is important to keep the big picture in mind: stocks are still cheap compared to bonds and the Fed just printed a bajillion dollars, many of which are sitting in money market funds earning zero percent interest. These dollars will ultimately make their way into other asset classes.

The world may feel topsy turvy but we assure you it is still spinning. The virus will pass and our government and economy will still run. Companies will continue to earn profits, and the owners of those businesses (i.e. you) will continue to benefit.

We thank you for the continued trust you place in us.

Sincerely,

John G. Prichard

Miles E. Yourman

Kurt Beimfohr

Jeff Vieth

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 So far, only partial steps have been taken, as European governments seek to avoid a return to full lockdowns. Returns to major lockdowns have, however, already been seen in Israel and Australia’s Melbourne. Interestingly, both of those countries are governed by right of center parties, illustrating that political affiliation doesn’t necessarily have to dictate the virus response.

2 The death count clearly indicates Latin America as the hardest hit region on the graph (India is not shown, though it is well on its way to being a disaster). The fact that Latin America’s reported cases remain below that of the United States probably reflects the lack of extensive testing in that region.

3 Focus on the 60% success rate for Phase 3 vaccine candidates getting to approval. That said, each vaccine candidate probably shouldn’t be seen as having a completely independent probability of working since many candidates are based on the same idea: producing antibodies to the protein “spike” on the virus.

4 A vaccine that is only 50% effective and is taken by only 50% of the population will only provide protection to 25%.

5 We say “virus-wise” because some things may never completely go back to the way they were before (more work from home/less business travel).

6 The famous 1918 flu pandemic, for which they had no effective vaccine, lasted from February 1918 to April 1920.

7 In taxable accounts, we decided that the position is so highly appreciated, and the future of Apple sufficiently bright, that even if the stock is overvalued, it isn’t worth selling. This large position which we intend to hold for tax reasons helped performance in taxable accounts this year but may detract from returns vis a vis tax-exempt accounts in the future, especially if Apple’s price to earnings ratio falls back to more historical levels.

8 The $1,200 stimulus checks amounted to $180 billion in total whereas the PPP funneled $500 billion to businesses and business owners.

9 This expired in August but was extended for six weeks at $300 per week by Trump’s executive order.

10 The one-year forbearance on mortgage payments and patchwork moratoria on foreclosures and evictions went a long way as well.

11 A potentially ignored election risk to the stock market is that a Democratic

White House means Congressional Republicans suddenly “remember” they are staunchly against government overspending.

12 This was the main topic of last quarter’s letter. Quick recap: the Fed electronically “prints” dollars into existence, and then buys financial assets. This leaves the asset-owning class with extra dollars on their hands. And what does the asset owning class do with the extra dollars? They buy more assets! Thus raising asset prices.

13 This is basically Modern Monetary Theory (MMT) in action (though none of the participants admit to it). We wrote about MMT last Spring, thinking it would be tacitly adopted by the government because it is politically expedient to spend without taxing. We had no idea the adoption would be this fast.

14 For context, the Revolutionary War debt amounted to just 30% of GDP at the time.

15 After all, life on earth is ultimately unsustainable, as scientists say the sun is due to explode a few billion years from now. This isn’t something we typically worry about just yet.

© Knightsbridge Asset Management, LLC

Read more commentaries by Knightsbridge Asset Management

“Veil after veil of thin dusky gauze is lifted, and by degrees the forms and colours of things are restored to them, and we watch the dawn remaking the world in its antique pattern.”

“Veil after veil of thin dusky gauze is lifted, and by degrees the forms and colours of things are restored to them, and we watch the dawn remaking the world in its antique pattern.”