Coming into Focus

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsRoughly two months have passed since my last memo, Time for Thinking, and still not much has changed in the economy or the markets. The toll from Covid-19 continues to rise, the economic outlook is largely the same, vaccines remain some time off, and the S&P 500 is back where it was in early August. So I’ll repeat what I said then: it’s mainly been time for thinking. Fortunately, the more I’ve thought about the issues, the more things have come into focus for me. Thus, I’m going to use this memo to go into greater detail on a few topics.

The Prerequisite

In Time for Thinking I talked about the fact that I don’t consider this year’s developments to be cyclical. You could say, “Why not? The economy and the markets went down, and now they’re recovering. Isn’t that a cycle?” What I really mean is that this is very different from a normal cycle, and I’ve figured out a way to better explain that, borrowing a bit of what I said in my 2018 book, Mastering the Market Cycle.

Most of the up-cycles I’ve witnessed occurred because things were going well in the economy, causing psychology and decision-making to become increasingly optimistic and eventually euphoric. Corporations favored expansion, stock prices rose and financial innovation became possible, even encouraged. Eventually, productive capacity exceeded what was needed, stock prices exceeded underlying value, and shaky investment innovations were embraced. When these trends outstripped the fundamentals and became unsustainable, the result was a downturn. Often a recession triggered a market correction, and sometimes the impact of that recession was reinforced by negative exogenous events that further darkened the previously-blue skies.

A good example is the first non-investment grade debt crisis Bruce Karsh and I managed through, in 1990-91. There was a recession, exacerbated by the shock of going to war to help Kuwait repel an invasion by Iraq. The newly developed high yield bond market experienced its first major spate of defaults, the result of a recession and credit crunch and exacerbated by the prosecution of Michael Milken and the failure of Drexel Burnham, precluding remedial bond exchanges that otherwise might have helped companies stay alive. Stocks declined, but high yield bonds went into free-fall. Notably, many of the prominent LBOs of the 1980s – which had been financed with perhaps 95% or so of debt – went bankrupt. Investor psychology collapsed and bondholders headed for the exits.

A collapsing economy needs a good dose of stimulus to pull it out of its swoon, and that’s what occurred. Usually that’s enough. Eventually the economy recovers; consumers resume buying; investors regain their equilibrium – some even sense the bargains that have been made available; and the upswing takes the economy back toward good health . . . and the cyclical process continues.

So, most of the time, downturns stem primarily from economic weakness, and they are repaired with economic tools. But this episode is different. It was caused by an exogenous, non-economic development, the pandemic. The recession – rather than being the cause – was the result: a closure of business induced intentionally in order to minimize inter-personal contact and halt the spread of the disease.

Thus, this down-cycle cannot be fully cured merely through the application of economic stimulus. Rather, the root cause has to be repaired, and that means the disease has to be brought under control. An effective vaccine will do this – in time – but healthy behavior will be required in the meantime. Spikes like much of Europe is seeing represent something of a step backward in this regard.

And even with the disease controlled, economic stimulus is unlikely to reverse all the damage. The trauma has been deep, and the impact may not be easily shaken off. Large firms will continue to automate and streamline. Large numbers of smaller businesses – such as restaurants, bars and shops – will never re-open. Thus millions of people will not be rehired into the jobs they formerly held. For this reason, the expectations with regard to economic recovery have to be realistic. To me, as I’ve said, “V-shape” has too positive a connotation.

The Need for Further Assistance

One of the things weighing on the recovery is the matter of help from Washington. Whereas the Treasury was able to announce aggressive spending programs in the spring, there has been no new package here in the fall. Partisan differences have arisen regarding the size of a package and its contents. Further, we’re so close to the upcoming election – less than a month away – that neither side wants to give the other anything that might be described as a victory.

But this is not an academic matter. The trillions of dollars paid out thus far were not stimulus payments, but support. They weren’t made to get the recipients to spend so much as to keep them and the economy alive. In short, the amounts distributed – to the unemployed, families with incomes below $100,000, companies and institutions – were designed to replace lost income and maintain, rather than stimulate, the economy. Individuals got money so they could buy the necessities of life. Companies got money to replace lost revenues, so they could continue to employ people. These needs have not dried up, even as the disease has ground on and the supplemental unemployment benefits have expired.

As one of my Oaktree colleagues wrote me last week, “I was chatting today with the owner of a small movie theater chain. One wouldn’t trade places. All of their theaters in California are closed; the ones out of state are operating with high costs and no patrons; and there is virtually no product to attract audiences. And the lenders and landlords are banging on the door.”

Individuals have problems, too. According to Morning Brew on September 25:

With the economy still in the basement, people are straining to pay their mortgages. According to industry analyst Keith Jurow, “several million” people will have gone nine months without making a payment when the Federal Housing Finance Agency’s foreclosure and eviction moratorium expires at the end of the year.

17% of FHA-insured mortgages were delinquent in July, per the Department of Housing and Urban Development. In NYC, 27.2% of mortgages were.

Another pressing need can be found at state and local governments. Their revenues have withered as the take from taxes and fees has declined. But their need to spend is unabated – they’re not enjoying any savings in connection with the slower economy – and in fact it has grown. Police, firefighters and EMTs are no less essential, and the need for health care and family services has only increased. And yet, unlike the federal government, cities and states can’t engage in unlimited deficit spending since they can’t print money or issue seemingly unlimited amounts of debt. Like companies and individuals, they need significant aid.

On September 24, The Wall Street Journal reported on Fed officials’ testimony to Congress:

The recovery would move along faster “if there is support coming both from Congress and from the Fed,” Chairman Jerome Powell said during the second of three days of congressional testimony Wednesday.

Chicago Fed President Charles Evans told reporters that his projection that the unemployment rate would fall below 6% by the end of next year had been premised on around $1 trillion in additional fiscal relief.

“If that doesn’t happen, then I think it’s going to be a lot harder, and much more unlikely that we make that much progress,” he said. . . .

“The power of fiscal policy is really unequaled by anything else,” Mr. Powell told lawmakers on a House panel overseeing the U.S. response to the coronavirus. (Emphasis added)

The same day, Dennis DeBusschere of Evercore ISI wrote:

On monetary policy, the Fed is not out of bullets and still has quasi-fiscal programs like the Main Street Lending Program (MLSP) and the Municipal Liquidity Facility (MLF). But as our friends at Macro Policy Partners pointed out, “Powell all but waved the white flag on those programs in his remarks, which is troubling. The Fed has already adopted a ‘set it and forget it’ stance on rates and QE, and these tools are not as well-suited to the current economic challenges as MSLP and MLF.” So either there is a fiscal package soon and risk assets move higher, or inflation expectations trend lower, forcing the Fed to use more bullets. Our hunch is the Fed will be forced to react. (Emphasis added)

The economic recovery everyone’s counting on is not an independent event, unaffected by developments. Rather, it is highly dependent on progress against the disease, as described above, but also on the continuation of fiscal expenditures in the interim. Sadly, the outlook for action in this latter regard is not good. Partisan enmity is at a level I’ve never seen before, especially given the fight over the Supreme Court nomination. With the two houses of Congress in the hands of warring parties, I’d be pleasantly surprised if they can agree on anything before the election.

The bipartisan Problem Solvers Caucus in the House restarted the negotiations a couple of weeks ago by surfacing a proposal that would come out in the middle between the Democrats’ target of $3 trillion and the Republicans’ willingness to spend $500 million, and compromise on the individual components as well. [Note: I’m a national co-chair of No Labels, the organization that supports the caucus and the goal of bipartisan cooperation.] Let’s be hopeful that something can be done to appropriate needed aid even while the election campaign is underway.

The Power of Interest Rates

One of the biggest financial stories of 2020 is the powerful market rally that began in late March and quickly caused the equity indices to regain the ground they had lost and in some cases reach new highs. And the more I think about it, the more credit I attribute to the low level of interest rates.

As you know, the Fed reduced the fed funds rate – the base rate that influences many other interest rates – by a half-percent on March 3, from 1.50-1.75% to 1.00-1.25%, and by an additional percent on March 15, to 0-0.25%. Low rates like those of today exert influence in a broad variety of ways. I touched on a few of them in my last memo, but I’m going to undertake a fuller treatment of the subject here.

First, there’s the stimulative effect of low interest rates. This is probably the aspect people think of first when there’s a rate cut. In short, everything that entails financing is made more attractive. It becomes cheaper to buy a house because the monthly mortgage payment is smaller. Ditto for cars and boats. Monthly payments on existing adjustable-rate mortgages decline, leaving consumers more disposable income. Corporate interest expense declines as well, reducing the cost of a new factory or production line. A faster-growing economy improves the general mood and makes transactions more likely. And fear of missing out on the low rates gives people a reason to act now, accelerating transactions that might otherwise have taken place in the future.

Second, lower rates increase the discounted present value of future cash flows. In the most theoretical sense, the current value of an asset is the discounted present value of the cash flows it will produce in the future. We discount future cash flows because a dollar to be received in the future isn’t worth a dollar today: money invested today should bring back more in the future. If you demand a return of 7%, you’ll pay $0.51 today for $1 to be received in ten years.

(Discounted cash flow, or “DCF,” is widely used to quantify the potential return from investments. The discount rate that sets the estimated future cash flows equal to the initial investment is the return the investment will produce if the flows materialize as expected. Thus, reversing the sentence just above, if you can put up $0.51 today and get back $1 in ten years, the implied return is 7%.)

The rate at which we discount future cash flows depends on the risks involved in waiting for them. These include the risk of actual loss as well as the loss of purchasing power to inflation. If something’s risky, we should demand a high return and thus use a high discount rate. However, the rate we use is also a function of prevailing interest rates and the returns available on other investments (opportunity costs). When those things are low, a low discount rate will be used. And the lower the discount rate, the higher the resulting present value. Thus low interest rates raise the DCF value of all investments.

Third, a low risk-free rate brings down demanded returns all along the capital market line. The yield on the 30-day Treasury bill is often referred to as the risk-free rate. There’s no credit risk, since the obligor is the government (which can print all the money it needs for repayment), and there’s no risk of losing purchasing power to inflation, since repayment at maturity is only days away.

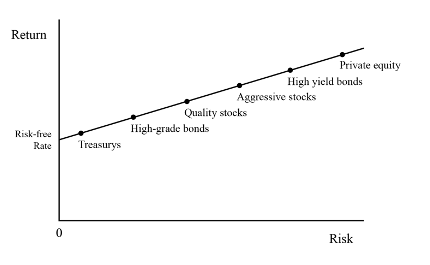

Since the risk-free rate can be earned with complete safety, and most people prefer safety over risk (all else being equal), investors shouldn’t take risk without being compensated for doing so. As investments increase in terms of the level of uncertainty, an incremental “risk premium” should be incorporated in their potential returns. Thus the notion of the “capital market line” that slopes upward and to the right, showing the relationship between risk and return, as follows:

In this graphic, the capital market line shows a coherent relationship between expected return and expected risk. When I studied at the University of Chicago business school, they called this “equilibrium”: as perceived risk increases, each asset class appears to offer a higher a priori return, such that the prospective risk-adjusted return on each asset is fair relative to the others. Nothing else makes sense in a market that’s functioning well.

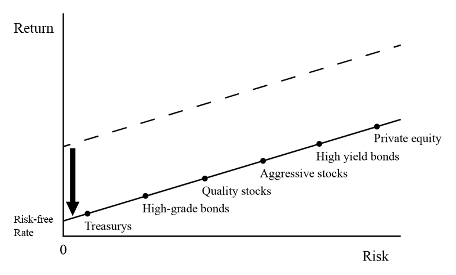

But in March, the Fed lowered the fed funds rate by 1.5%. Predictably, other interest rates, bond yields and prospective returns generally followed suit, as suggested in the next graphic.

The risk/return relationships among asset classes are still reasonable, but all prospective returns are much lower in the absolute. Thus, in general, the lower the point at which the capital market line originates, the lower all returns will be.

Or to get away from the graphic and say it in words, when I began to manage high yield bonds in late 1978, the fed funds rate and the yield on the ten-year Treasury note both stood around 9%. As a result, high yield bonds had to offer yields above 12% in order to attract capital (and yet few investors were willing to buy them because of the stigma and because they didn’t need yields that high to reach their return goals). But today, with the fed funds rate and yield on the ten-year well below 1%, people are flocking to high yield bonds paying 5-6% like it’s free money. The point is that the lower the risk-free rate, the lower the prospective return needed to attract capital to other asset classes.

So the lower the fed funds rate is, the lower bond yields will be, meaning outstanding bonds with higher interest rates will appreciate. And lower yields on bonds means they offer less competition to stocks, so stocks don’t have to be cheap to attract buying. They, too, will appreciate. And if high-quality assets become high-priced and thus offer low prospective returns, then low-quality assets will see buying – implying rising prices and falling prospective returns – because they look cheap relative to high-quality assets.

Most decisions in investing are relative decisions. Investors try to find the most attractive opportunity so as to be able to achieve the highest risk-adjusted return. Thus a great deal of the selection process is comparative. “I’m considering buying X. How does its risk/return proposition compare with the one on Y?” That means the lower the return is on Y, the less X has to offer to be the superior investment. And if X is to offer less return, the way it gets that way is through an increase in its price. Thus, assets and asset classes are inherently interconnected. Money moves from one asset class to the next in search of the best bargains, which get bought up until they’re at equilibrium with everything else. Changing the risk-free rate has the potential to reset the returns on everything.

Fourth, lower demanded returns lead directly to higher valuations. When Treasury notes yield a more normal 3%, investors might demand a return of, say, 6½% (incorporating an “equity premium” of 350 basis points) if they’re to invest in the S&P 500 instead of Treasurys. The S&P offers such an “earnings yield” when its earnings represent 6½% of its price, which written as a fraction is 6½/100. The ratio of earnings to price is obviously the inverse of the ratio of price to earnings, or the p/e ratio. An earnings yield of 6½/100 equates to a p/e ratio of 100/6½, or 15.4, which is a rough approximation of the S&P’s average p/e ratio since World War II.

Now let’s assume a Treasury yield like today’s 1%. To offer the same 350 basis point equity risk premium, the earnings yield only has to be 4½%. And an earnings yield of 4½/100 implies a p/e ratio of 22.2. So, in theory, assuming S&P earnings are unchanged, a reduction of the required earnings yield from to 6½% to 4½% calls for an increase in the p/e ratio, and thus in the price, of 44%. This is another way to describe the impact of lower interest rates on asset prices. Lower rates mean higher prices for stocks, just as they do for bonds. (Note: since companies’ earnings generally grow while bonds’ interest coupons don’t, it can be argued that required return on stocks should be even lower, meaning p/e ratios can be even higher.)

Fifth, the Fed also has the ability to lower yields by buying bonds. This is really an extension of the point just above. In addition to lowering the fed funds rate, the Fed can goose the markets by buying Treasury bonds and notes and other types of securities. If the Fed buys securities, that lifts the prices of those securities. When their prices go up, their expected yield to maturity goes down. And when the yield on bonds goes down, other assets can attract capital without offering as much prospective return as they used to, so their prices can rise, too.

Further, when the Fed buys securities, it puts money into the hands of the people who sell them to the Fed, and that money will be spent or loaned (helping the economy) or reinvested (driving up asset prices). In the four months from mid-March to mid-July of this year, the Fed bought mostly Treasury bonds and notes, but also other securities, to the tune of more than $2.3 trillion. That was roughly 20 times what it bought in 18 months during the Global Financial Crisis.

Sixth, low interest rates and the resultant low prospective returns encourage risk tolerance and reaching for return. When a lower risk-free rate pulls down the capital market line as shown above, most assets promise less return than they used to. That means people who in the past got the return they want or need from an asset with a given level of risk now have to move out the risk curve to riskier assets in order to try for that same return.

Today, many U.S. institutional investors are saddled with target returns (in the case of endowments) or actuarial assumptions for return (for defined-benefit pension funds) in the area of 7%, give or take. Unfortunately, these needed returns have not come down nearly as much as interest rates (and thus prospective investment returns) have fallen. For return targets to decline as much as interest rates, universities and charities would have to be content with receiving reduced support from their endowments, and pension plan sponsors would have to come up with increased funding.

The investments one might have made in the past now promise far less return than they used to. With prospective returns on cash near zero, the ten-year Treasury at 0.7%, high grade bonds yielding 2-3% and stocks expected to return 5-6%, what’s an investor needing 7% to do? The usual answer is to take on more risk in pursuit of the higher returns that riskier investments appear to promise.

In this way, low rates make risk aversion a challenging thing to practice and risk taking much more palatable. The alternative is to accept today’s lower promised returns. But most people opt for the former, and that means risky asset classes become crowded with eager capital, something that’s not beneficial for risk-adjusted returns. Bad things tend to happen when FOMO – the fear of missing out – takes over from risk aversion, or the fear of losing money.

Seventh, the need to put money to work causes the capital markets to reopen. In most financial crises, the “credit window” slams shut because people with capital (a) are nursing losses on the assets they own and (b) are terrified about the future of the environment. Those two factors make them reluctant to provide new financing, and that in turn means capital is unavailable – even to deserving companies and potentially lucrative projects. That, in turn, means risk assets decline in price, causing prospective risk-adjusted returns to rise.

But today, the Fed and Treasury have reassured investors that they will ride to the rescue, that large amounts will be made available to companies and other participants in the economy, and that they can depend on a prompt recovery. This has enabled investors to “look across the valley” to better times. This in turn has enabled low rates to coerce sources of capital to provide generous levels of financing.

Thus, today, credit is liberally available, and bond issuance has equaled or eclipsed many prior records. For example, despite the biggest quarterly decline in GDP in recorded history and the closure of the capital markets for a while, $345.6 billion of U.S. high yield bonds have been issued so far this year, according to S&P. That’s more than the record $344.8 billion issued in all of 2012.

In all these ways, a low risk-free rate makes even low investment returns seem attractive. Thus, today, it seems to me that most assets are offering expected returns that are fair relative to their expected risk, relative to everything else. But the prospective returns on everything are about the lowest they’ve ever been.

Changes in the Composition of the Stock Market

In Time for Thinking, I also mentioned the increased bifurcation of the U.S. equity market. In short, the leading tech and software companies (a) have become more different from other companies as the role and power of technology have expanded and (b) have become a much larger part of equity indices as such companies have grown and become more highly valued, and as indices like the S&P 500 have changed their composition to remain relevant. While I’m no expert, I’m going to cite a few of the arguments regarding the significance and implications of this trend. (Thus I pass on these appealing arguments; I don’t endorse them).

First, the attributes and returns on the two groups of stocks have become more differentiated.

- The gap between the growth outlook for FAAMG (Facebook, Apple, Amazon, Microsoft and Google) and similar companies and that for the rest (in the slow-growing 21st century) is huge and expanding.

- The adoption of technology has been pulled forward by the pandemic. Thus virtual meetings, ecommerce and cloud computing are now commonplace, not the exception.

- Current profits severely understate the tech leaders’ potential. They currently choose to spend aggressively on new product development to expand share and head off competition, voluntarily suppressing profit margins. Thus enormous potential exists for the tech companies to increase profit margins in the future when they become willing to moderate their growth rates.

- Their addressable markets are larger than ever and growing, giving them greater “runway.” For example, at the end of 1999, during the tech bubble, there were 248 million Internet users in the world. Now there are more than that in the U.S. alone and almost 5 billion worldwide. Thus 62% of the world’s population carries a computer with Internet connectivity in his or her pocket.

- Finally, it’s easier than ever to scale these businesses. In the past, one would have to go to a dealer to buy software on a disc, take it home and install it. Now we download apps from the web in seconds.

For these reasons, a large differential in terms of p/e ratios is warranted.

Second, these groups will not merely coexist and perform differently. Rather, the tech companies have the potential to negatively impact some of the non-tech companies. The common term for this phenomenon is “disruption.” Amazon has endangered brick-and-mortar retailers. Netflix has challenged the traditional TV and movie ecosystem. Facebook has cut into newspapers and other traditional media – industries thought to be protected by moats and thus “defensive.” Tesla has revolutionized the auto industry and outperformed the incumbents in developing electric vehicles. The list of industries immune to technological change – in terms of profitability if not their essential nature – is limited.

Finally, it’s argued that the leading tech companies of today are stronger than the Nifty Fifty of the late 1960s. Today’s leaders are often compared to the Nifty Fifty, but they’re much better companies: larger; faster growing with greater potential for prolonging that growth; capable of higher gross margins (since in many cases there’s no physical cost of production); more dominant in their respective markets (because of scale, greater technological superiority and “lock in,” or impediments to switching solutions); more able to grow without incremental investment (since they don’t require much in the way of factories or working capital to make their products); and possibly valued lower as a multiple of future profits. This argues for a bigger valuation gap and is perhaps the most provocative element in the pro-tech argument.

Of course, many of the Nifty Fifty didn’t prove to be as powerful as had been thought. Xerox and IBM lost the lead in their markets and experienced financial difficulty; the markets for the products of Kodak and Polaroid disappeared, and they went bankrupt; AIG required a government bailout to avoid bankruptcy; and who’s heard from Simplicity Pattern lately? Today’s tech leaders appear much more powerful and unassailable.

But fifty years ago, the Nifty Fifty appeared impregnable too; people were simply wrong. If you invested in them in 1968, when I first arrived at First National City Bank for a summer job in the investment research department, and held them for five years, you lost almost all your money. The market fell in half in the early 1970s, and the Nifty Fifty declined much more. Why? Because investors hadn’t been sufficiently price-conscious. In fact, in the opinion of the banks (which did much of the institutional investing in those days) they were such good companies that there was “no price too high.” Those last four words are, in my opinion, the essential component in – and the hallmark of – all bubbles. To some extent, we might be seeing them in action today. Certainly no one’s valuing FAAMG on current income or intrinsic value, and perhaps not on an estimate of e.p.s. in any future year, but rather on their potential for growth and increased profitability in the far-off future.

And note that a lot of the strength and potential of today’s tech leaders derives from their dominant market shares and market power. This same element creates one of their greatest vulnerabilities: potential exposure to anti-trust action. Bigness and the successful tactics that led to it are enough to make some people call for constraints on the incumbents. Here’s what Barclays reported on October 7:

Yesterday, US large-cap technology stocks (i.e. Facebook, Amazon, Google and Apple) came under pressure after the House antitrust subcommittee released a 449-page report proposing far-reaching antitrust reforms. Recommendations include structural separation, prohibiting a dominant platform from operating in competition with the firms dependent on it and line-of-business restrictions, limiting the markets in which a dominant firm can engage.

There are two groups of stocks in the indices, and the representation of tech stocks is large and expanding. In the S&P 500, for example, roughly one-quarter by value consists of tech and software companies that are fast growing and have the ability to increase both revenues and profit margins, and the remaining three-quarters is slow growing and already enjoying maximum margins. Today’s tech leaders are more superior than ever to run-of-the-mill companies, rendering indices that include both types of company less relevant than ever. Or so it’s argued. Regardless of where you come out on that question, if an index consists 25% of great growth companies at high multiples (up roughly 30% this year as of the end of September) and 75% more pedestrian companies at low multiples (up 4%), the average figures in terms of growth, valuation and performance might not be meaningful enough to support conclusions about “the stock market.”

A Different Kind of Crisis

One question I’m often asked nowadays is how the coronavirus crisis of 2020 differs from the past crises we’ve managed through:

- the high yield bond crisis of 1990-91, when many prominent LBOs of the ‘80s went bankrupt,

- the telecom/scandal company meltdown in 2001-02, and

- the Global Financial Crisis of 2008-09, brought on by the implosion of sub-prime mortgages and marked by the meltdown of financial institutions.

The clear difference I want to cover here relates to the characteristics of the current go-round. The best way to start might be to describe the crises of the past:

- In each of the three crises listed above, recessions caused or exacerbated economic weakness.

- Negative economic and corporate developments, collapsing markets and rising fear caused a credit crunch in which financing became impossible to obtain.

- The combination of economic weakness and the unavailability of financing led to vastly increased defaults and bankruptcies.

- Asset prices cratered.

- Companies and investment entities marked by asset/liability mismatches and/or high levels of leverage experienced margin calls and meltdowns.

- The downward spiral seemed unstoppable.

- Pessimism ran rampant, leading to soaring risk aversion.

- This led to panic selling of assets and rendered most investors absolutely unwilling to buy.

- Because of all the above, it was possible to purchase assets at prices from which extremely high returns could be achieved, often with low attendant risk.

Now, contrast that with the events of 2020. In mid-February, developments regarding the coronavirus pandemic and the lockdown implemented to fight it began to hammer the markets. Prices for equities and credit fell, and the mood turned darkly negative. From the all-time high reached on February 19, the S&P 500 fell 34% in only 33 days. The prices of high yield bonds and leveraged loans were hard-hit as well. Security issuance stopped cold. The pieces were in place for a crisis just like those described above, and things were moving in that direction in March.

But as everyone knows, the Treasury and Fed announced rescue programs in mid-March and an enlarged Fed program during the week of March 23: zero interest rates, bond buying, grants, loans and significantly enhanced unemployment payments. The total ran to multiple trillions of dollars. And the authorities made it clear that there was more behind that: that the available resources were unlimited.

- People accepted that the recession would end and a recovery take its place in short order.

- With short-term interest rates near zero, investors lined up to buy bonds in the quest for return. Thus rather than a credit crunch, there’s been record amounts of capital available.

- Even though the rescue provided “liquidity but not solvency,” whole industries (like the airlines) were saved from sure bankruptcy.

- There were none of the spectacular implosions that mark most crises.

- Ditto for panic selling.

- Pessimism was replaced by willingness to think about better times ahead.

- With interest rates at zero, investors couldn’t afford to be risk averse. They had to embrace risk assets in order to have a shot at returns above the low single digits.

- Thus asset prices recovered.

To illustrate the effect, since April 1, investors in distressed debt have had opportunities to make large rescue loans to companies or entities needing a quick response to problems related to illiquidity or pending debt maturities, and there’s still a good pipeline. But with investor optimism reinforced, competition to lend has increased, and the ultra-low returns available on safe assets have made the possibility of double-digit returns something people compete to achieve. The sum of all this has kept prospective returns far lower than is usual in times of crisis.

Thus this is an unusual crisis: one marked by a non-financial, exogenous cause and a lack of lasting pain for most investors . . . and not by widespread opportunities for bargain hunters. Great investments are often made when an investor is willing to buy something no one else will touch at any price. We were able to do just that in past crises, because what you needed was money to spend and the nerve to spend it, and we had those things when most didn’t. Other investors’ lack of money and nerve in past crises made them great times for buying. Today, thanks to the Fed and Treasury, everyone’s got a lot of both. That makes things much tougher.

But what happens if people exhaust the support payments they’ve received, Washington fails to deliver sufficient additional assistance, widespread layoffs ensue (as seems to be beginning) and business slows again? Mightn’t we see a rise in defaults and bankruptcies and a softening of investor psychology and thus asset prices?

The Potential Downside of the Rescue

Along with the sweep of the Covid-19 epidemic and the magnitude of the recession that resulted from combatting it, the size and success of the Fed/Treasury rescue effort is one of the big stories of 2020. In the Global Financial Crisis, it took the authorities months to figure out what to do and do it. But this year, they dusted off the 2008 playbook and implemented it in a couple of weeks.

We’ve never seen an economic environment like the one brought on by the lockdown. Many industries (plus other entities and institutions) with zero activity and no revenues, but still high costs. And millions of people without jobs or incomes. There’s a belief (never documented) that a large part of the American population lacks resources with which to survive a $400 emergency. How would they survive months without paychecks? Without paychecks, how would they patronize merchants? Without making sales, how would merchants pay their rent? Or their taxes? Without rental income, how would property owners service their debt? Without income from debt service, how would lenders stay solvent? Without tax revenues, how would state and local governments pay their employees and continue to provide services? And how would developed nations purchase the exports that emerging economies need to make to survive? The picture we faced in mid-March was truly the worst I’ve seen. Global depression seemed possible.

But the Fed and Treasury brought their massive concerted effort, simulating the activity of the economy and replacing a good bit of the lost cash flows. It succeeded to a startling degree. Most investment markets recovered, and the economy has shown surprising strength. Thus the next thing I want to discuss are the possible ramifications of the rescue. I’ve touched on this before, but it’s one more thing on which I want to go into greater depth.

First, what are the policy implications of zero rates? To me, the most obvious one is that there’s no more room to cut. (Fed officials insist they won’t take rates into negative territory, and negative rates certainly can’t be said to have rekindled economic growth in Japan and Europe.) Thus the question is how the Fed would counter an economic relapse connected with something like a second wave of Covid-19 and resultant second lockdown.

Second, rescues and bailouts have the potential to cause moral hazard. When the government saves people from losses, it teaches that it’s okay to make risky investments: if they work out, you get rich; if they don’t work, you’ll be bailed out. That’s a bad lesson. This year, for example, lifelines have been thrown to industries that over-borrowed, over-expanded and/or spent too much of their cash on stock-buybacks. Yet it was decided that they wouldn’t be permitted to go bankrupt.

Further, by dramatically lifting the markets, the Fed may have caused some people to believe that it will always do so – that there’s a “Powell put” that can be counted on to keep things humming. (Think back to the tantrum the stock market threw in the fourth quarter of 2018, when the yield on the ten-year Treasury got up to 3.25%. It was enough to end the program of interest rate increases that Janet Yellen had initiated and bring on a series of cuts instead.) If investors believe the Fed can always be counted on to keep the markets aloft, that will encourage dangerous behavior. And, anyway, it seems like an impossible task and, in my opinion, a questionable goal for the Fed.

Third, the kneejerk reaction to trillions of dollars of deficit spending on the part of the Treasury and further trillions of dollars of bond buying by the Fed is worry about inflation. The injection into the economy of trillions in added liquidity would seem to have the potential to create too much money chasing too little in the way of goods, causing prices to rise (as it has done for assets). Further, as a result of the rescue measures, we’re running a multi-trillion-dollar deficit and adding trillions to the national debt, which as a percentage of GDP now approaches the high established after World War II.

Printing large amounts of money has had severe consequences in the past. One wonders whether the 2020 version might bring about some of the things traditionally associated with currency debasement:

- undesirably high inflation,

- weakness of the U.S. dollar,

- a downgrade of the U.S. credit rating,

- an increase in the cost of borrowing to cover the increased deficit,

- rising interest rates generally, adding further to the cost of debt service, and thus to the deficit and debt,

- the allocation of an increasing share of the federal budget to debt service, and

- the dollar’s loss of status as the world’s reserve currency.

Of course, there are rejoinders:

- We’ve been engaged in deficit spending for a long time without any rekindling of inflation or other ill effects. (Of course, this can be likened to the frog sitting in the pot of water that’s being heated. It doesn’t notice the gradually rising temperature until it’s too late.)

- Nations have been trying to create 2% inflation for years without success. Thus (a) inflation isn’t easily ignited and (b) inflation isn’t the problem – the lack of it is.

- Modern Monetary Theory says (over-simplifying) that deficits and debts don’t matter. (But most economists disagree, and common sense suggests it’s unlikely a country can spend beyond its means to an unlimited degree without repercussions.)

- Finally, there’s no obvious candidate to replace the dollar as the reserve currency.

All I know is that (a) the Fed and Treasury seem unworried about the possibility of any of the above and (b) anyway, they consider continuing the program indispensable.

Fourth, what the Fed does worry about is anemic growth. It will certainly take a fair while – a year or more following the low reached in the second quarter of this year – for GDP to regain the level achieved in 2019 and what it was supposed to be in 2020. A stagnant economy would fail to put people back to work who lost their jobs as a result of the lockdown, and it certainly wouldn’t provide jobs for a growing population.

“The risk here is a downward spiral,” [Lael Brainard, a Fed governor, noted in a recent speech], warning that the economy could be trapped in a vicious cycle of low interest rates, muted inflation and weak growth.

Long-term trends such as disappointing productivity gains and limited labor force growth are sapping the economy’s potential. In July, the Congressional Budget Office said the U.S. economy could expand in the long run at an average annual rate of just 1.8 percent — down from more than 4 percent in 2000. (The Washington Post, October 3)

Because this is the Fed’s prime concern, it’s less worried about the risks entailed in its efforts to rescue and stimulate the economy as described above. It is perfectly willing to see inflation at 2%, something that it hasn’t been for years. In fact, it recently announced an averaging approach under which monetary policy will remain loose and rates low until inflation averages 2%. That is to say it will be permitted to run above 2% for a while as a way to bring the average up to 2%.

Some say the worst of all worlds would be stagflation, which I lived through in the 1970s: high inflation and economic weakness. Certainly it was a dismal decade. But others think economic sluggishness is more likely to lead to disinflation (declining inflation) or even deflation, a phenomenon so rare we know little about it.

The secular deterioration in economic growth has created a condition of excess resources and disinflation. (Hoisington Quarterly Review and Outlook, Third Quarter 2020)

My answer is that I have no idea whether we’ll see inflation, stagflation, stagnation, disinflation or deflation, and Oaktree won’t bet on any of them. It’s one of the tenets of our investment philosophy that our investment decisions aren’t driven by macro forecasts. Not that it wouldn’t be nice to know what the future holds in these regards; rather it’s simply that most investors – and certainly we – aren’t capable of superior judgments about the macro. So why bet?

Finally, I want to state clearly that nothing I’ve written on the subject of the rescue and its possible ramifications is intended to be critical of the Fed and Treasury and their actions. I put it simply: just because something has potential negative consequences doesn’t mean you shouldn’t do it. In the case of the pandemic and associated recession, there was absolutely no alternative. While not perfect, the policy response has been brilliant.

Further Exposing Inequality

Especially in this environment of heightened attention to social and racial justice, I can’t end this memo without touching on some of the many ways in which the recent experience has shed additional light on inequality in our society:

- People further down the economic ladder have had less in terms of financial resources to fall back on during the lockdown, and they generally haven’t benefitted from the increase in asset prices that’s been driven by the reduction of interest rates.

- Low-income workers have been more likely to lose their jobs due to the lockdown and recession.

- Those who’ve kept their jobs (often in industries like food production, retail and hospitals) are more likely to be essential workers, required to work and put in harm’s way. White-collar and administrative employees, on the other hand, are much more likely to be able to work from home.

- Low-income people are more likely to live in cramped quarters and crowded neighborhoods, giving them a lower quality of life if working from home and an increased chance of contracting the disease.

- For all these reasons, the incidence of Covid-related sickness and death has been disproportionately high among these populations.

- People with lower incomes are more dependent on the schools to help with childcare. Thus school closings have had a greater impact on lower-income families, which are less able to keep kids home when given the choice. Rather they have to send them to school, where they are exposed to contracting the disease and bringing it home to parents and grandparents.

- Finally, women are more exposed to this phenomenon than men: they make up a higher percentage of single parents, their wages may be lower than those of male partners, and they’re often expected to be the ones shouldering the responsibility for childcare.

Of course, “lower income” is disproportionately synonymous with “non-white.” Taken together, I believe there’s been a “tale of two cities.” The overall experience of lower-income Americans during the pandemic – and thus of Blacks and Hispanics – has been a far cry from that of whites and those with higher incomes and greater financial resources. These observations are likely to be part of the conversation on equality of opportunity that lies ahead for our country.

What It All Means for the Markets

For years leading up to 2020, I described the investment environment as follows:

- An unusually high level of uncertainty (mostly exogenous and geopolitical)

- The lowest prospective returns ever

- Asset prices that were full to excessive

- Pro-risk behavior being engaged in by investors trying for high returns

Taken together, these things told me we were living in a low-return world in which the promised returns didn’t fully compensate for the risks. It wasn’t a bubble, characterized by absurdly high prices. And there was no way to say for sure when the good times would end or why. It was merely the absence of justification for taking full risk.

Thus Oaktree operated under the mantra “Move forward, but with caution.” We invested, and we tried to be fully invested. But we endeavored to do so “with caution.” And since we always take a cautious approach to our risk-asset strategies, it really meant “more caution than usual.” Being fully invested in a cautious portfolio caused us to lag the benchmarks a bit in some of the asset classes where we have them, as it turned out that caution generally wasn’t needed – until this year.

Our cautious stance was rewarded in the difficult first quarter of 2020. The conditions I described above made the markets vulnerable to exogenous shock, and we got a doozy. Importantly, that caution enabled us to approach our portfolios calmly, generally unconcerned about price declines and not burdened with widespread problems requiring remediation. In drawdown funds with capital available, we were able to act affirmatively, picking up bargains when their availability peaked in March.

Now, however, I think we’ve returned to the market conditions I used to go on about.

- The same uncertainties exist as were present last year (except that the recession and ending of the bull market that were considered ultimately inevitable have come and gone). In addition, we have some new uncertainties. The full list includes the battle against Covid-19, the shape of the recovery, the implications of the election and whether it will go smoothly, worry about higher taxes and more redistribution, the divisiveness in our country, and the outlook for racial harmony.

- If prospective returns were low in the last few years, they’re even lower today thanks to the reduction of interest rates. A near-zero return on cash, 2% on investment grade debt, 5% on high yield bonds, 5-6% expected from equities – at the same time as lots of capital is eager to be put to work. Adequate returns are likely to be hard to come by.

- The stock market is back near the high reached in February and selling at an above average valuation (as described earlier). The only things that appear to be low-priced are the ones that appear fundamentally most risky, such as oil & gas, retailers and retail real estate, office buildings and hotels, and low-rated tranches of structured credit. As I said earlier, everything appears to be fairly priced relative to everything else, but nothing is cheap thanks to the low base interest rate.

- Thus, after a brief foray into bargain-land in March, we’re back to a low-return world. But since most investors haven’t reduced their required or targeted returns, they have to engage in elevated risk in order to pursue them.

In my view, the low interest rates represent the dominant characteristic of the current financial environment, creating the dominant consideration for investors: the lowest prospective returns in history (for the reasons described on pages 4-6). Thus I’ve dusted off a presentation I’ve been giving in recent years called “Investing in a Low-Return World.” At its end, after laying out much of the above, I conclude by enumerating the strategic alternatives for investors:

- Invest as you always have and expect your historic returns. Actually, this one’s a red herring. The things you used to own are now priced to provide much lower returns.

- Invest as you always have and settle for today’s low returns. This one’s realistic, although not that exciting a prospect.

- Reduce risk in deference to the high level of uncertainty and accept even-lower returns. That makes sense, but then your returns will be lower still.

- Go to cash at a near-zero return and wait for a better environment. I’d argue against this one. Going to cash is extreme and certainly not called for now. And you’d have a return of roughly zero while you wait for the correction. Most institutions can’t do that.

- Increase risk in pursuit of higher returns. This one is “supposed” to work, but it’s no sure thing, especially when so many investors are trying the same thing. The high level of uncertainty tells me this isn’t the time for aggressiveness, since the low absolute prospective returns don’t appear likely to compensate.

- Put more into special niches and special investment managers. In other words, move into alternative, private and “alpha” markets where there might be more potential for bargains. But doing so introduces illiquidity and manager risk. It’s certainly not a free lunch.

None of these alternatives is completely satisfactory and free from downside. But in my view there are no others.

To put it into the terms I’ve been using over the last several years, how should the balance be set today between aggressiveness and defensiveness? How should you “calibrate” the riskiness of your portfolio? Should it be at your normal level; titled toward offense to try to wrest high returns from a low-return world; or tilted toward defense in deference to the uncertainties, requiring you to settle for lower returns?

As I’m sure is my bias, I lean toward defense at this time. In my view, when uncertainty is high, asset prices should be low, creating high prospective returns that are compensatory. But because the Fed has set rates so low, returns are just the opposite. Thus the odds aren’t on the investor’s side, and the market is vulnerable to negative surprises. This is how I described the prior years, and I’m back to saying it again. The case isn’t extreme – prices aren’t grievously high (assuming interest rates stay low, which they’re likely to do for several years). But it’s hard in this context to find anything mouth-watering.

October 13, 2020

Legal Information and Disclosures

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All