Russ discusses the appeal of the middle area when choosing growth versus value stocks.

During the past week the cyclical/value trade suddenly flipped. After an unusual period of value leadership, tech stocks rallied while some of the more aggressive manifestations of the cyclical trade, such as materials, stalled. For investors exhausted by these seemingly fickle rotations back-and-forth, there may be a solution: Focus on the middle of the growth/value spectrum.

Rather than trying to exclusively time sudden shifts in growth versus value, a better strategy may be to focus on high quality companies for which the valuation is in sync with earnings, a style often referred to as “Growth at a Reasonable Price,” or GARP. Most of these names are neither pure growth or deep value but tend to fall in between.

No longer just a growth market

Looking at the past three months, U.S. growth continues to outperform. That said, there are a few nuances to note. The differential between value and growth has narrowed, at least compared to the earlier stages of the rally. It is also worth highlighting that parts of the cyclical space, which tends to be more tilted towards value, are doing particularly well. For example, industrial and material stocks are outperforming the broader market.

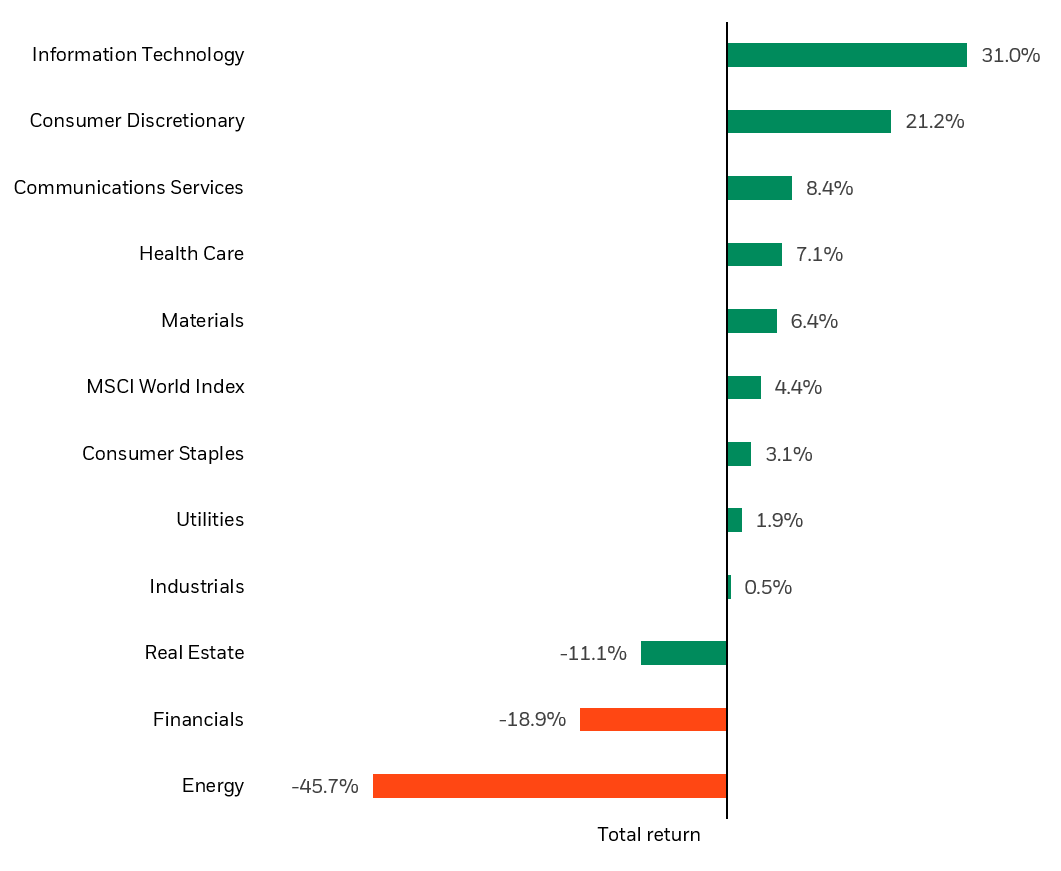

At the same time, many of the “deep value” names continue to struggle. Parts of value facing secular challenges, from big oil to financials, are still underperforming (see Chart 1). And while tech continues to dominate, many previous leaders have stalled, with several mega-cap internet names trading below their summer peaks.

Global sector performance - year to date