First Trust Focus Five Model: A Case Study for Relative Strength Investing

On October 21st, 2020, the First Trust Focus Five Model FTRUST5 turns 11 years old. While many investors have been following this model for years, those of you who have not can read more about the model’s methodology in the First Trust Focus Five Model Fact Sheet, which includes a detailed account of the methodology, the inventory, and performance numbers that go back to inception. Whether you access this strategy through the model, which is to say through the five individual holdings as published in the First Trust ETF Report and the Models page on the Nasdaq Dorsey Wright Research Platform, or through the First Trust Dorsey Wright Focus 5 ETF FV, which became available in March 2014, the methodology is based around the same premise and objective. Simply stated, it is designed to own five of the strongest sector trends within the US equity market.

11 Years of Returns

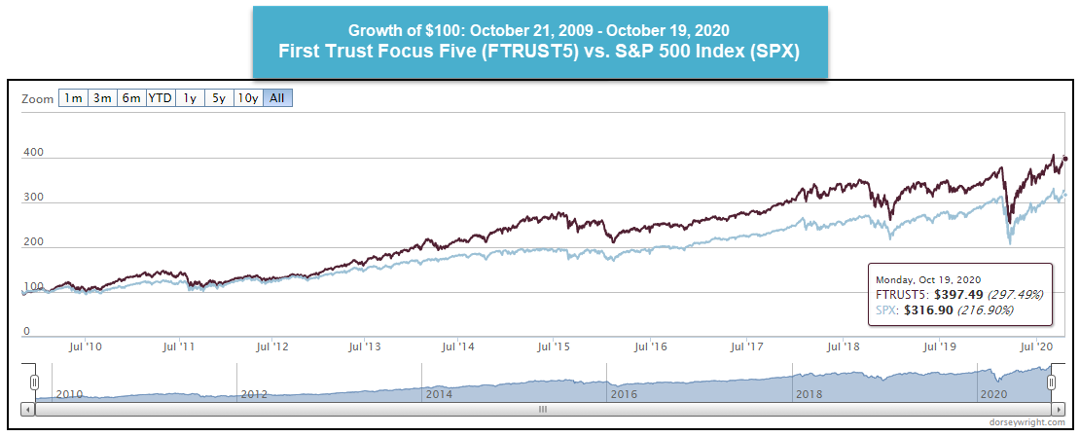

After 11 years of returns, multiple corrections, and presidents, and some years with little or a lot of sector rotation, the Focus Five strategy has delivered on its investment mandate. We do not expect relative strength to be strong at all times, but we do expect it to deliver better outcomes over time. The graph below shows the growth of $100, starting October 21, 2009. Over this period, the FTRUST5 has risen 297.49%, compared to 216.90% for the S&P 500 Index SPX. This comes out to an average annualized return of 13.36% for the Focus Five model since inception versus 11.05% for the S&P 500 Index.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

Perspective on Performance

Through the years we have answered many questions as it relates to portfolio management practices, specifically those that are grounded in relative strength. Many of those questions have been along the lines of "why isn't everyone doing this?" It is certainly a common question, especially when someone new is introduced to this methodology. For those that have been utilizing the Point & Figure methodology and relative strength for years, you understand that it takes discipline and patience which are not necessarily attributes that come easy in this business. Nonetheless, we have been able to hone in on a couple of key reasons that everyone is not doing it. There will be periods where the Focus Five strategy will lag the benchmark, such as 2011, 2015-2016, or even periods within the past couple of years. There will also be periods when it outperforms. That said, the strategy is not designed to outperform every single day, week, or month, but rather, over time the strategy should provide investors with a way of harnessing the predominant areas of sector leadership within the market. These results simply serve to reiterate the fact that the First Trust Focus Five model is designed to outperform over long periods.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

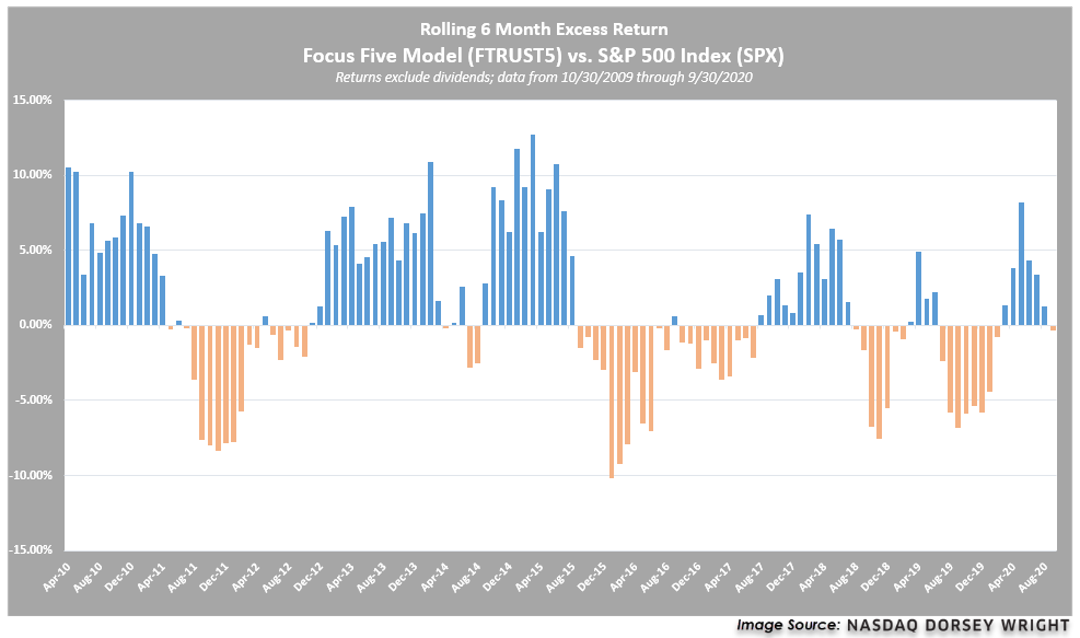

In the table above, we show the rolling six-month excess returns of the Focus Five Model versus the S&P 500, illustrating a tendency toward outperformance over the past 11 years. Of the 126 "six-month" monthly periods examined, the model has outperformed in 69, or 54.76% of the time. The worst stretch for the model was the 2015-2016 period, as was the case for relative strength in general, as volatility was high, and trends were very short-lived for much of that year. That said, however, through strong RS periods and weak ones, the eleven-year record for the Focus Five strategy speaks to the robust nature of this trend-following methodology over time.

Focus Five Exposure

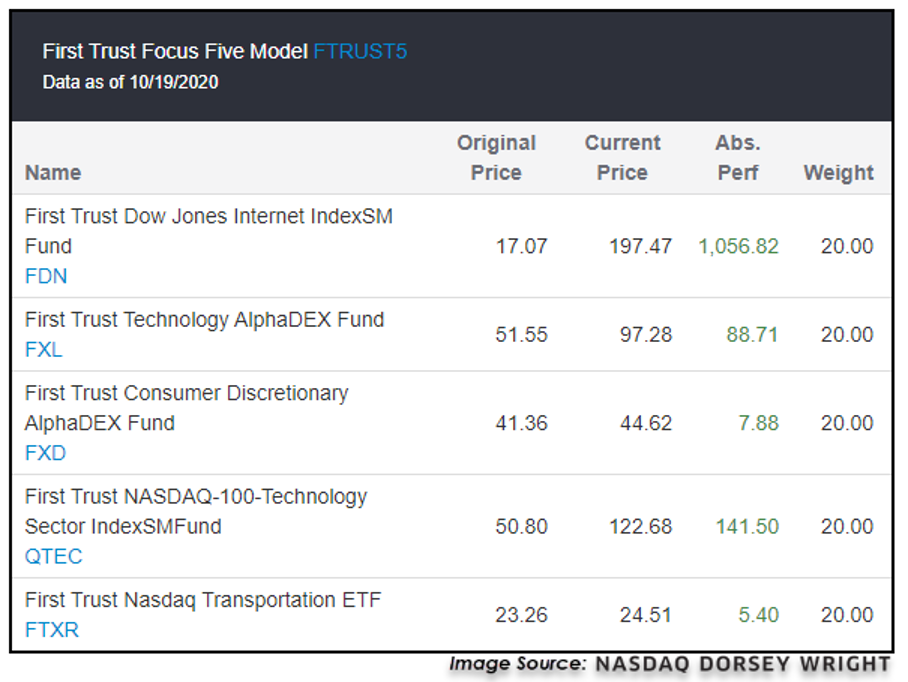

For the past couple of years, the Focus Five strategy has been heavily allocated towards technology, while also experiencing rotation among other sectors, ranging from banks to energy. The most recent change occurred last month when transportation FTXR replaced energy FXN on September 8. Consumer discretionary has been a holding in the model since June 9, 2020. Meanwhile, technology FXL and Nasdaq 100 Technology QTEC have been in the model since November 7, 2017, and November 8, 2016, respectively. Internet FDN has been a holding since the October 2009 inception.

Focus Five Allocation Ideas

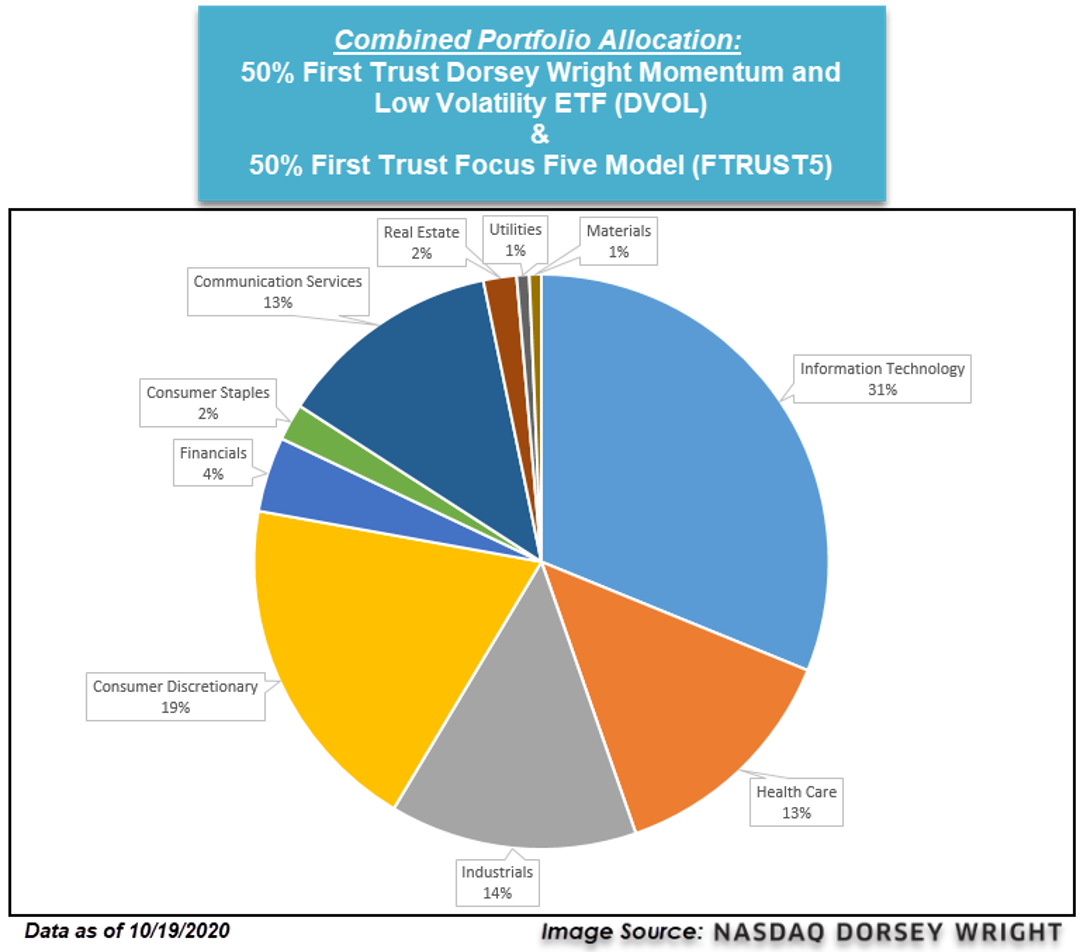

There are a variety of different ways that the Focus Five strategy can be employed in a portfolio. This could include using the model as a tactical complement to a broad-based core domestic equity fund or using the model in concert with another domestic equity-focused model, such as a size & style approach. One method that we have seen used more frequently as of late has been to combine the model with another factor, such as low volatility. This ensures the portfolio maintains exposure towards the higher relative strength sectors while smoothing out the sometimes bumpy ride that can come with sector rotation strategies. This will also serve to further diversify your domestic equity exposure, as the low volatility factor will often overweight different areas than strictly momentum-based relative strength. As an example, we will take a look at combining the First Trust Focus Five Model with the First Trust Dorsey Wright Momentum & Low Volatility ETF DVOL, using a 50/50 portfolio split. Below, we take a look at the combined portfolio allocation using the GICS sector breakdown of each of the holdings within FTRUST5 paired with the underlying holdings of DVOL.

As we discussed above, the Focus Five strategy is currently overweight technology at 60%, with the remaining exposure split between consumer discretionary and transportation. This is quite different from DVOL, which is more diverse in and of itself as it is not tied down to exposure in five specific areas. The Momentum Plus approach employed by DVOL looks at first filtering through the starting universe for those areas of positive relative strength and then ranking those names by a factor score to determine areas for investment. In this case, that means choosing the 50 stocks from that ranking with the lowest trailing volatility. DVOL is currently overweight healthcare at 25%, followed by technology (16.6%), communication services (13.8%), and a tie between consumer discretionary & industrials (13.1%). The slightly more defensive-minded posture of the names within DVOL complements the high-RS names of the FTRUST5 well, helping to limit the potential risk that could be associated with any single specific sector. Adding an additional factor such as low volatility can assist the portfolio in weathering the storm while relative strength works to find those new areas of outperformance.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.