By almost any measure, 2020 has been one of the most volatile years for the market in recent memory. Through the first week of September, the S&P 500 SPX had more daily moves of +/- 2% or more this year than in any full calendar year since 2009. While the CBOE SPX Volatility Index VIX is nowhere near the peak levels it reached in March, it currently sits around 29, well above its long-term average, and has not fallen below 21 since February.

Protecting their portfolio from turbulent markets is one of the primary reasons that many investors look to low volatility funds. Somewhat paradoxically, however, low vol has been one of the worst-performing factors through the first three quarters of the year. Year-to-date on a total return basis (through 10/21/20) the Invesco S&P 500 Low Volatility ETF SPLV has returned -2.42%, while the S&P 500 Total Return Index TR.SPXX has gained 7.94% for a difference of over 10%. In the small cap space, the difference has been even more pronounced as the Invesco S&P Small Cap Low Volatility ETF XSLV is down -27.49%, underperforming the total return of the Russell 2000 by almost 25% and the S&P 600 by about 18%. The index that SPLV is based on consists of the 100 securities from the S&P 500 with the lowest realized volatility over the past 12 months. XSLV’s index is constructed in a similar fashion as it consists of 120 out of 600 small-capitalization securities from the S&P 600 with the lowest realized volatility over the past 12 months.

From a size & style perspective, SPLV’s portfolio is 33% large cap value, 28%, large cap blend, and just 6% large cap growth (Source: Invesco), which has been the strongest size & style box this year. SPLV also has an 8.7% weight to mid cap value, 10.95%, mid-cap blend, and 13% allocation to mid cap growth. XSLV has a significantly smaller allocation to value at 15.08%. However, growth only makes up a little more than a third of the portfolio as the largest allocation is small cap blend at 47.15%, while small cap growth is 36.79%.

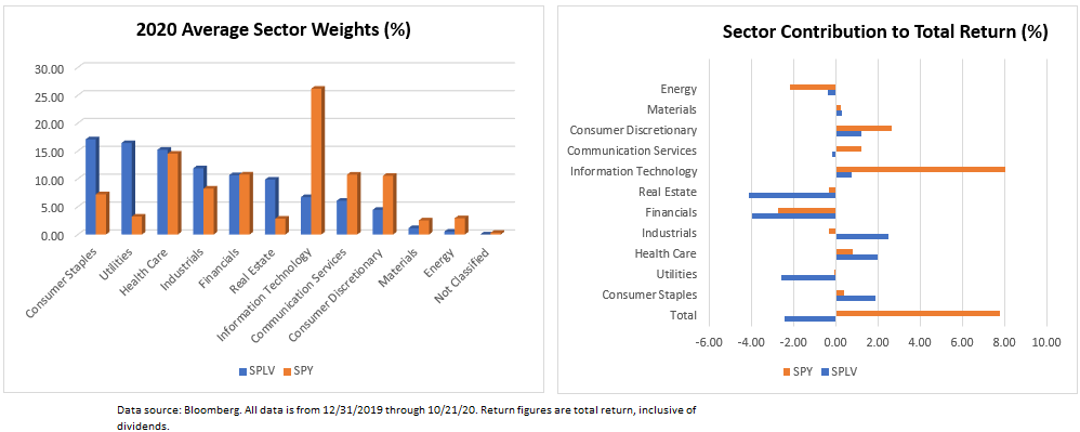

The technology sector has been the best performing sector in 2020 and it is by far the largest portion of the SPDR S&P 500 Trust SPY portfolio, with an average weight year-to-date of 26% (through 10/21). SPLV’s average weight to the technology sector is just 6.71%, an underweight of about 19.5%. So, while SPY’s technology allocation has contributed 8% to its total YTD return, SPLV’s technology allocation has contributed just 0.76%, the largest single source of SPLV’s underperformance from a sector perspective. SPLV’s three largest overweights are utilities, consumer staples, and real estate at +13.20%, +9.86%, and +7.02%, respectively, which have been relatively weak in 2020. Real estate was the second largest contributor to SPLV’s underperformance relative to SPY at -3.82%, while utilities contributed -2.51%.

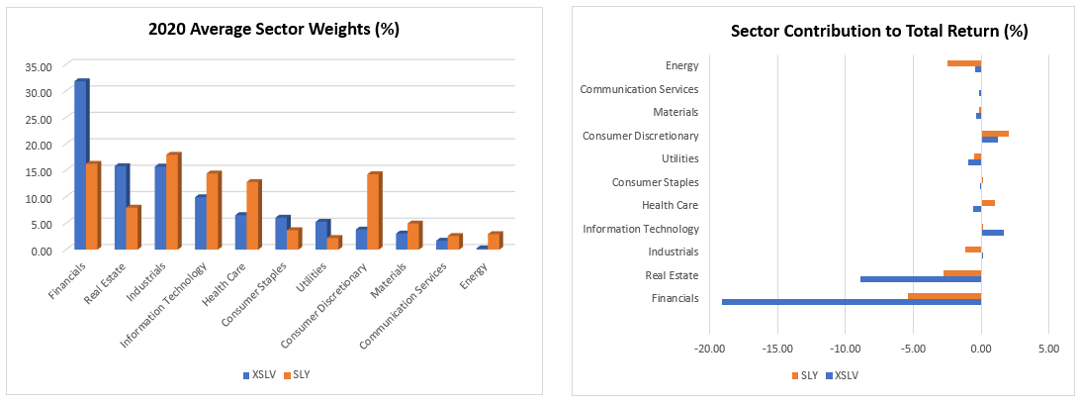

Its large overweight to financials – the sector has had an average weight of 31.85% in the XSLV portfolio vs. 16.23% in SLY – has been by far the biggest source of XSLV’s underperformance, accounting for 13.68% of XSLV’s 18.31% deficit vs. the S&P 600 Small Cap ETF SLY. XSLV’s overweight to real estate has been another significant source of drag on its performance. XSLV’s largest area of positive relative performance was energy, where it is underweight more than 2.5% relative to SLY, contributing just over 2% of outperformance.

Looking at the relative performance contributions, it appears that the index construction methodology of these funds may be the ultimate cause of their underperformance in 2020. Perhaps unsurprisingly, it seems that stocks with low standard deviations – the funds’ method for measuring volatility – are more heavily concentrated in some sectors, especially traditional “defensive” sectors like utilities and consumer staples, which have generally underperformed this year. Meanwhile, there are far fewer of these stocks in sectors like technology. This may also explain why other low volatility funds like the iShares MSCI USA Min Vol Factor ETF USMV, which attempts to build a portfolio with the lowest overall volatility as opposed to selecting individual stocks for their low standard deviation, or the First Trust Dorsey Wright Momentum & Low Volatility ETF DVOL which utilizes a relative strength overlay seeking to avoid areas of weakness, have fared better in 2020. On a price return basis, USMV is down -1.51% year-to-date, while DVOL has gained 3.73%.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.