Executive Summary

History does not repeat, but it rhymes, as Mark Twain observed. As such, we are struck by the eerie and dangerous parallels between today’s markets and the markets back in 1999. Back then, Value investing and Value managers were under the gun for having underperformed their Growth brethren for too long. Valuation spreads between the U.S. and Emerging Market equities were wide, the U.S. was witnessing speculative and “bubbly” behavior on the part of retail investors, and, yes, GMO was looking stupid for still believing that valuations mattered and the gravitational pull of mean reversion would eventually work. While it is, of course, not 1999, we see ominously similar market phenomenon today. And for that reason, our advice is clear – it’s time to leave the party like it’s 1999.

Let’s state the obvious: it is not 1999. True, stock market valuations in the U.S. are ridiculous today, but they are not yet at the absurd levels reached in the late 90s. Further, many of the largest tech companies today, the so-called FAANGS, are likely not part of the bubble problem: these companies are real and large global businesses, highly profitable, and millions, even billions, of people use their products and services every day.1 These behemoths are nothing like Pets.Com, WebVan, and other infamous Super Bowl ad buyers from the dot.com bubble era. Too, interest rates are significantly lower today and, while a debatable point, many argue that lower rates ipso facto should lead to higher equity valuations.2 So, again, this is not exactly 1999 all over again. But history never exactly repeats, it merely rhymes, as Mark Twain thoughtfully pointed out. And today, there are some eerily similar and dangerous rhymes echoing in our ears.

Avoid the Conventional 60/40 Portfolio…Just Like 1999

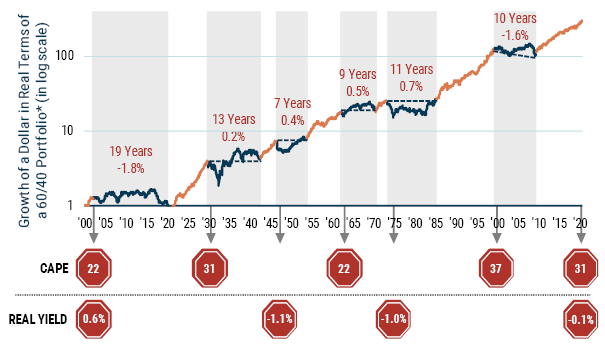

Currently, we are advising all our clients to invest as differently as they can from the conventional 60% stock/40% bond mix, just as we were advising them in 1999. Back then, we were forecasting a decade-long negative return for U.S. large cap equities. And that is exactly what happened. Today, the warning is actually more dire. U.S. stock valuations are at ridiculous levels against a backdrop of a global pandemic and global recession, and CAPE3 levels are well above 2007 levels, within shouting distance of the foreboding highs reached in October 1929. But it gets worse. U.S. Treasury bonds – typically a reliable counterweight to risky equities in a market sell-off – are the most expensive they’ve been in U.S. history, and very unlikely to provide the hedge that investors have relied upon.4 We believe the chances of a lost decade for a traditional asset mix are dangerously high. Exhibit 1 lays out the long and sad history of these numerous lost decades for 60/40 portfolios. What they all had in common was that each began with stocks or bonds being expensive. Today, stocks and bonds are pricey. This frightens us and it should frighten you. Few investors want to hear this because the 60/40 portfolio has worked so wonderfully for the past 10 years. Unfortunately, they were saying the same thing back in 1999, right before it failed them for a decade.

EXHIBIT 1: 60/40 “LOST DECADES” ARE MORE COMMON THAN YOU THINK

Most started with expensive stocks or bonds – today, both are

As of 9/30/20 | Source: Bloomberg, Global Financial Data (early history), Factset (S&P 500 returns and CPI), J.P. Morgan (J.P. Morgan GBI United States Traded), Shiller data; real yields are the yield on the 10-Year U.S. Treasury minus the 12-month trailing CPI.

*60% U.S. Equities (S&P 500), 40% U.S. Bonds (U.S. Treasuries) rebalanced monthly. Past Performance is not indicative of future results.

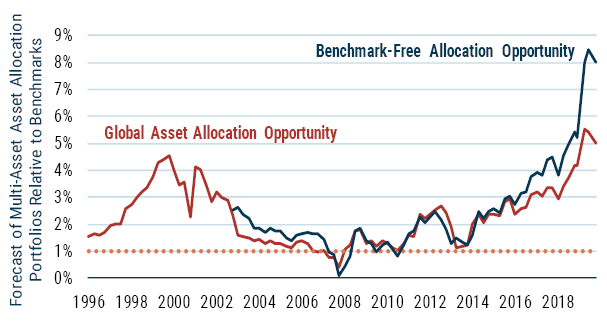

Framed more positively, we think this is the perfect time to look unconventional, just like 1999. In May of this year, Ben Inker dusted off a thought experiment that he had conducted in the TMT bubble era.5 In it, he took the GMO forecasts of the late 90s/early 2000 period and calculated an expected return for the GMO Global Asset Allocation Strategy (in which the actual asset allocation had been deviating significantly from its traditional benchmark). Then, he calculated the expected return of the traditional benchmark. Exhibit 2 plots the month-by-month delta, or difference, between these two expected returns. It is a measure of how good the opportunity set has looked and changed through time. In 1999, the delta between the two portfolios was over 450 bps annualized. Ben wrote to clients at the time that it was highly unlikely we would ever see such an amazing opportunity again. Fast forward to today’s valuation spreads, and on our data the opportunity set is actually even better. And for those portfolios that are essentially benchmark-agnostic, like our GMO Benchmark-Free Allocation Strategy, we believe the opportunity set is the best we’ve seen in our working careers.

EXHIBIT 2: BEST OPPORTUNITY SET SINCE 1999

As of 9/30/20 | Source: GMO

Opportunity is difference between forecast return of portfolio and benchmark given GMO forecasts at the time. 10-year forecasts are translated to “7-year equivalent” by multiplying by 10/7. Dotted lines are our long-term expectations of likely achievable alpha from asset allocation. Benchmark-Free Asset Allocation is compared to a 60% MSCI ACWI / 40% U.S. Government Bond portfolio.

Growth Trouncing Value Today…Just Like 1999

In the late 1990s, Value managers were on the defensive. The Value style had been out of favor for more than half a decade. Well-known Value firms were losing clients and going out of business. Clients had been led to believe that “in the long run, Value wins.” Yet by 1999, the Russell 1000 Value Index had underperformed its growth cousin in 7 of the preceding 11 years, and by huge margins. Countless academic papers were proclaiming the “Death of Value.” Ultimately, of course, mean reversion worked, and Value went on to trounce Growth seven years in a row; despite the early pain, patient investors were ultimately rewarded for their perseverance. From 1999 to 2006, Value beat Growth by a cumulative 99%.

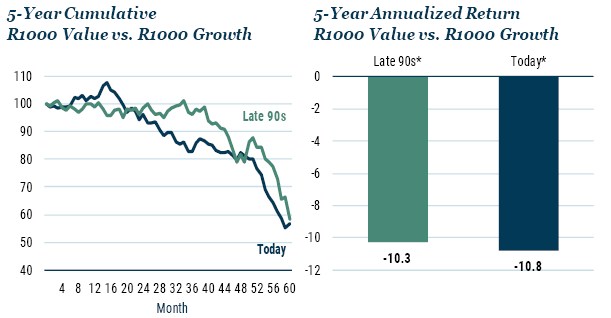

Fast forward to today and the same rhymes are echoing. Well-known and established Value shops are calling it quits.6 The pain for Value investors has lasted even longer and performance spreads are even worse: Value has lost to Growth in 8 of the last 11 calendar years and by even wider margins. Exhibit 3 focuses on the last 5 years, drawing eerie parallels between today and 1999.

EXHIBIT 3: U.S. VALUE VS. GROWTH PERFORMANCE IS EERILY SIMILAR TO LATE 90S

Source: FTSE Russell

*The “Late 90s” reference is to 5 years ending February 2000; the “Today” reference is to 5 years ending September 2020.

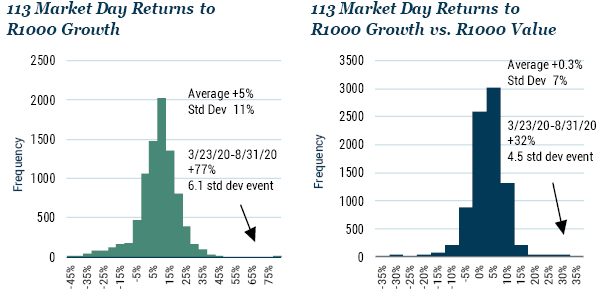

Not painful enough? Enter the Covid-19 Growth rally of 2020, which started on March 23 and continued all summer. From March 23 to August 31 – a 113-day run – Growth was up 77%, beating Value by a soul-crushing 32% cumulatively (a 4.5 sigma event, which officially happens once every 403 years; see Exhibit 4). This outperformance of Growth, importantly, has not been justified by the fundamentals, resulting in one of the widest valuation spreads we’ve ever witnessed. We believe this is a time for leaning into Value, not away from it. When mean reversion ultimately occurs, just as it did in the post-1999 period, investors will want to be on the right side of that trade.

EXHIBIT 4: AN UNPRECEDENTED RUN FOR U.S. GROWTH VS. VALUE THIS SPRING AND SUMMER

Data is from 9/30/1985 to 3/23/2020 and from 3/23/2020-8/31/2020 | Source: FTSE Russell, GMO

Emerging Market Equities Look Amazingly Cheap Today…Just Like 1999

Back in 1999, GMO was not all gloom and doom. True, we were pointing out the dangers of a Growth stock bubble in the U.S., but we were just as passionately pointing out the amazing opportunity set in Emerging Market (EM) equities. Just like today, however, clients were nervous about EM equities. Back then, they had just been put through the ringer: the Thai baht crisis and Asian contagion, Russia’s financial crisis (which was the trigger for the Long-Term Capital debacle), and more. EM equities had underperformed the U.S. by over 26% annually for 5 years, leaving them cheap. How cheap? Our official forecast was that they were priced to deliver over 8% real (this stood in contrast to a -2% real forecast for the S&P 500). Basically, we were saying that EM equities were about to outperform the U.S. by close to 11% per year for the next 10-year cycle. And that is exactly what happened.7 Mean reversion works.

Fast forward to today, where history is not exactly repeating, but it’s a close rhyme. This time, the Value half of EM equities has been the perennial disappointment. Over the last 6 years, the MSCI Emerging Value Index has actually delivered negative returns, while the S&P 500 has been delivering 12.5% annually. Ouch. EM equities have been weighed down by a host of fears and worries: trade wars, slowing economic growth in China, etc. The nature of the concerns are not exact repeats of 1999, but can you hear the rhyming?

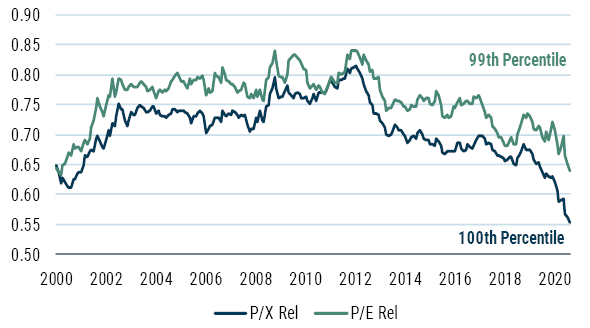

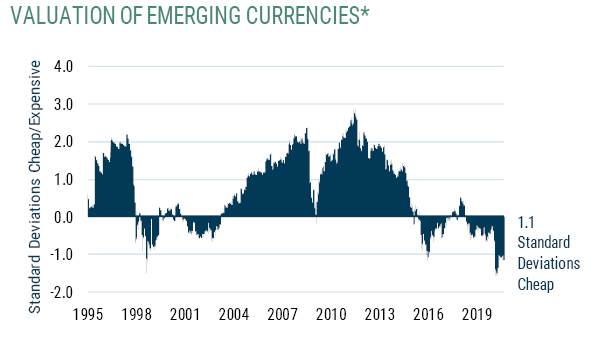

This underperformance of EM Value stocks – despite that fundamentals have performed quite well, actually – leave the asset class looking quite cheap. Our forecast today is close to 10% real over the next 7 years. The forecast delta between EM Value and the S&P 500 is eerily similar to what it was in 1999. We have put together a diversified portfolio of emerging value stocks that are trading at P/E multiples hovering between 9 and 10, priced at roughly 1.1x book value, and with dividend yields north of 5% (and NOT because we are loading up on banks). These stocks are the cheapest we’ve seen since 1999, by a host of metrics (see Exhibit 5). But the story gets even better. First, this basket of companies has lower debt-to-equity ratios than do typical EM companies. They have not gone on debt binges as their U.S. counterparts have. Second, GMO’s EM team has done an interesting analysis8 that demonstrates that many of the largest EM countries are better prepared and better able to manage the effects of Covid-19 than most other developed countries. Finally, their currencies are cheap, another possible tailwind to performance (see Exhibit 6). We believe EM Value is poised to outperform the U.S. by generously wide margins for the next cycle, just as it did in the post-1999 era.

EXHIBIT 5: EMERGING VALUE STOCKS CHEAPEST SINCE 1999

Emerging Value vs. Emerging relative P/E and price/multiple measures of capital (X)

As of 8/31/20 | Source: GMO

Based on GMO forecast universes.

EXHIBIT 6: EMERGING CURRENCIES CHEAPEST SINCE 1999

Adjusted for their productivity gains, Emerging currencies are cheap

As of 9/30/20 | Source: J.P. Morgan, Datastream, GMO

*Equally weighted index of Brazil, China, Indonesia, India, Korea, Malaysia, Mexico, Russia, Taiwan, and South Africa.

U.S. IS IN A BUBBLE TODAY…JUST LIKE 1999

From a strict valuation perspective, the run-up of U.S. stocks, Growth stocks in particular, was worrying to us all during the 2016-19 timeframe. Price movements were getting way ahead of earnings, and that’s never a good thing. But we were hesitant to call it an official bubble because not all of the ingredients were there. First, the economy itself was in pretty good shape as was the U.S. consumer, with unemployment numbers improving steadily over the last decade to reach historic lows. The optimistic mood of the markets was understandable. Also, we were missing many of the more conspicuous “tells” of a bubbly market, i.e., silly behavior on the part of retail investors like what we witnessed ad nauseum in 1999.

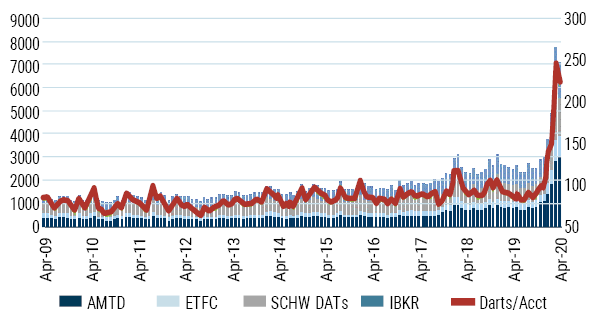

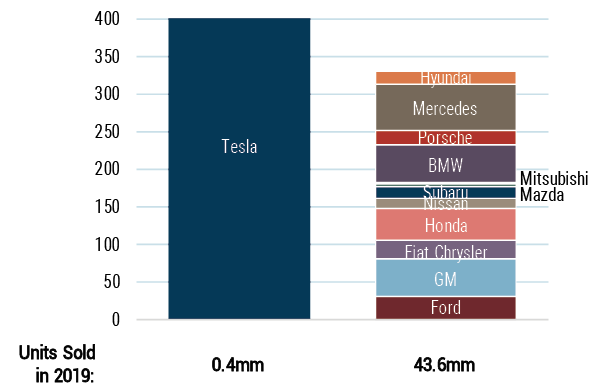

Both of those things changed dramatically in 2020. First, the economy was destroyed by Covid-19; unemployment went from historic lows to historic highs in a matter of weeks. That should have reasonably dampened the market’s optimistic mood. But it didn’t (after the initial shock of March). The current valuation of the S&P 500 is actually higher than it was pre-Covid-19, which is dangerously odd given the sheer amount of uncertainty that exists (e.g., the shape of the economic recovery, the availability and efficacy of a vaccine, the risk of a second wave, U.S. citizens not adopting safety protocols, just to name a few). The real worrisome signs, however, are the increasing silly behaviors of a speculative market. Exhibit 7 is a prime example of the aggressive trading activity of retail investors. Though relatively calm for over a decade, this past spring awakened their animal spirits: daily trading activity increased nearly seven-fold over three short months. Bankrupted Hertz rallied 896% in May even though its own management team and the SEC said the company was likely worthless. Nikola, an electric truck maker with no actual earnings, no actual revenue, and…it’s true….no actual manufacturing facility to even make trucks, rallied 692% from April to early June. And then there was Tesla, which was bid up to $400 billion in market cap, making it more valuable than 12 established car companies, combined (see Exhibit 8). The “You just don’t get it, GMO” taunts, the justifications, the mental gymnastics, the outrageous growth assumptions one needs to make to rationalize prices…it is all just too eerily reminiscent of 1999.

EXHIBIT 7: TRADING VOLUME WAS RELATIVELY STEADY FOR 10 YEARS…AND THEN, BOOM!

As of: 5/19/20 | Source: GS Research Division, Will A. Nance

DART is Daily Average Revenue Trade.

EXHIBIT 8: ANIMAL SPIRITS, JUST LIKE 1999

Market Cap of Tesla vs. 12 Global Auto Makers

Source: Bloomberg, Statista, annual reports | Market cap data as of September 30, 2020

Asset Allocation Is Looking Stupid Today…Just Like 1999

The final parallel between today and 1999 is painful to write about. Asset Allocation positioning is looking stupid today. Our Value bias, our underweight to U.S. equities, and our overweight to EM equities have not worked as we had hoped, as expensive assets have gotten more expensive and cheap assets have gotten cheaper. Our clients are losing patience, exactly as they did in 1999, that eerily similar and painful episode in GMO’s history. In fact, this late 90s episode was featured at the Harvard Business School, which teaches its classes using the case method. GMO literally became a case study because Harvard was so intrigued by GMO’s insistence on sticking to its conviction about overpriced Growth stocks and internet dot.coms even though the firm had been fired, ridiculed, and pilloried in the financial press (see Exhibit 9). Clients were tired of hearing about mean reversion, tired of hearing about prices and valuations mattering. And they lost patience. Though many held on, just as many fired us. At exactly the wrong time.

EXHIBIT 9: GMO | A CASE STUDY IN CAREER RISK

Value Investing Is a Paradox…Just Like 1999

Value investing is full of paradoxes. First, the relationship between a Value manager and its client is sadly and tragically paradoxical: clients tend to fire us at the very moment they need us the most, and they need to hire us exactly when they are least likely to do so. Then there’s the paradox of the business model itself because clients will be perennially unhappy! In rapidly rising markets, Value styles lose in a relative sense; and then in down markets, yes, we lose less, but we still lose! Value investing is an amazing investment model, but a horrible business model. Finally, there is the paradox of confidence. At the very moment that our clients are the least confident in us – because crazy prices are getting crazier, valuations spreads are getting wider, speculative mania is getting more manic, and career risk is getting more uncomfortable – we at GMO become the most confident in Value’s eventual reversal.

How do we make sense of this paradox? We look to a similar period when we trusted in mean reversion when everyone else was doubting it. A period when sticking to a process seemed prudent and disciplined, while others called it stubborn, antiquated, and inflexible. And a period when the worst business decision for GMO ended up being far and away the best and right thing to do for our clients. In other words, a period like 1999.

Download article here.

1To be clear, we think many of the FAANGS are unattractively expensive today. Apple, for example, trades at 35x earnings while only a few years ago it was closer to 11x.

2GMO’s own Partial Mean Reversion forecasts acknowledge that if interest rates remain lower for the foreseeable future, then equity multiples must, by definition, be higher. But, a few thoughts. First, this assumption is not without controversy because this has not been the case from an empirical perspective. Longitudinally, it has not been true within the U.S., as real rates were even lower in the late 1940s and early 1950s while P/E multiples were in the single digits. Cross-sectionally, we also know this is not true: rates in Europe and Asia are much lower than in the U.S., yet their P/E multiples are still measurably cheaper. Other components of this debate are presented in James Montier’s white paper, “Reasons (Not) To Be Cheerful,” August 2020.

3Cyclically-adjusted price-to-earnings ratios.

5See Ben Inker, “Shades of 2000,” GMO 3Q 2019 Quarterly Letter.

6In October 2020, Ted Aronson announced the closing of his old-line Value firm, AJO, based in Philadelphia. It was founded in 1984.

7From the summer of 2000 to the summer of 2010, the MSCI Emerging Markets index beat the S&P 500 by roughly 12% annually in local terms.

Disclaimer: The views expressed are the views of Peter Chiappinelli through the period ending November 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2020 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO