The post-pandemic world is charging into change. Trends that were in play prior to the onslaught of COVID-19 have been accelerated, and many of the companies that were already leading the charge are emerging supercharged.

Can valuations of these growth companies continue to defy gravity and deliver for investors? Growth experts Lawrence Kemp and Phil Ruvinsky reveal reasons for optimism.

How has growth been able to outperform amid both economic strength and the coronavirus crisis and recession?

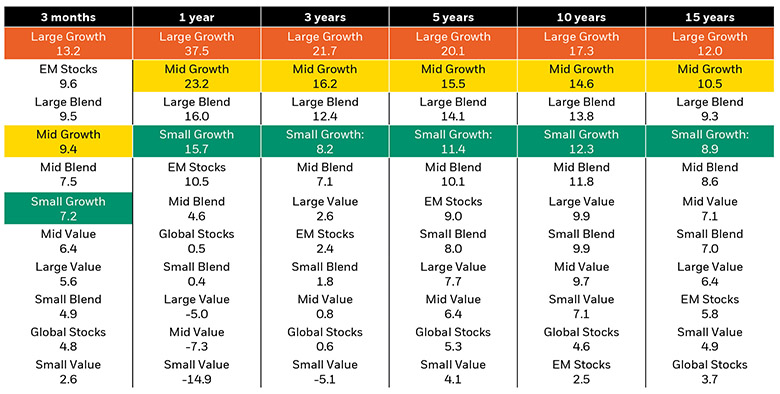

Growth has been a standout performer during three key market phases in recent years: the multi-year bull market, the pandemic-driven recession earlier this year and the subsequent snapback and market rally. (See the chart below.)

We believe this has to do with a broad migration in quality that has occurred slowly and quietly over the preceding decade. Growth companies have always been defined as those boasting higher earnings growth than their peers. But we have seen that a much broader cohort of these companies, primarily those offering unique solutions, are able to achieve both higher earnings growth and a stronger competitive moat. This is thanks in part to new technological innovation.

Growth has delivered across time

Performance (% return) of selected equity asset classes, Sept. 30, 2020

In addition, many growth companies today exhibit capital-lite business models, exemplary free-cash-flow generation, relatively lower leverage and cash-rich balance sheets. All of these ‘quality characteristics’ contributed to growth’s relative degree of protection during the downturn.

One final relevant variable: Many of these companies were viewed as beneficiaries of a remote working environment, fueled by the tailwind of a corporate digital transformation that has been in place for years. In this way, growth companies were both best prepared for the downturn and most likely to accrue the benefits in its aftermath.

Can growth’s ascendency continue beyond the pandemic?

We believe so. Investors are looking for a new type of portfolio balance in a low-rate, low-growth world. This could mean not only increased allocation to equities, but greater exposure to growth equities given their strong structural tailwinds.

The pandemic has been an accelerant for many of these firms, but we’re focused on the broader implementation of technology by more ordinary businesses. Some of the best companies in our portfolios have been everyday businesses that have put low-cost technology to work to gain market share against competitors. Child daycare companies, salvage auto, pest control, landscaping supplies — companies in these industries have been important drivers of return for us in recent years.

Are you concerned about lofty valuations?

Valuations have been a big part of the discussion around growth stocks in recent years. In today’s pandemic-oriented market, the questions have centered on: How can these companies be so highly valued when the economy is struggling? Isn’t there a disconnect? We believe that in parts of the market, there is. But it’s important to remember that the current valuation of a company comes from discounting future cash flows. In a low-rate world, businesses with a long duration and the ability to generate lots of free cash flow deserve to trade at a higher multiple given the low yields offered by other asset classes.

Best-in-class growth companies may experience bouts of volatility, but we see long-term, supportive trends firmly in place. And today the market is betting that this cohort of companies will drive sizably higher growth in years ahead. All of that said, we can be more comfortable paying a premium for a company when we can see quality. Quality today comes in the form of free-cash flow generation, sensible leverage and earnings growth backed with a strong competitive stance in the market.

What does all of this mean for active stock pickers like yourself?

The preceding decade, during which all stocks seemed to move up together, was a difficult one for active fund managers. Today, we see more dispersion, a greater separation between winners and losers in the market, and an environment with the likelihood for higher volatility - all of which have traditionally been positives for active managers.

The large-cap universe is teeming with high-quality companies, and the mid-cap space presents a slate of up-and-comers that have unique products and solutions we believe will enable them to take market share and grow. Innovation and disruption are here to stay, and these trends make it an incredibly exciting time to be an active manager.

Lawrence Kemp, CFA, Managing Director and portfolio manager, is head of BlackRock's US Growth team within the Fundamental Active Equity business of BlackRock.

Philip H. Ruvinsky, CFA, Managing Director, Lead Portfolio Manager of the Mid-Cap Growth Equity Strategy and research analyst.

© BlackRock

Read more commentaries by BlackRock