Executive Summary

Executive Summary

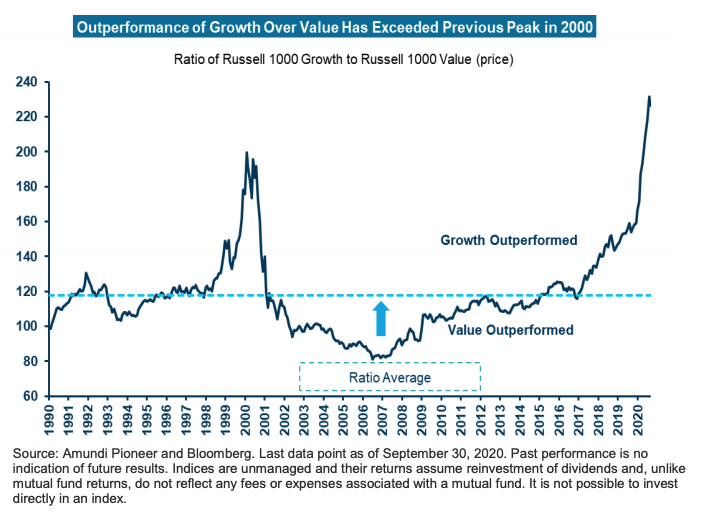

- The outperformance of growth stocks over value stocks has reached record levels, as has the valuation gap.

- The environment for growth stocks has been ideal: interest rates have plummeted, and US technology companies have become increasingly dominant in the US and abroad.

- However, we believe this ideal environment is unlikely to last. Inflation, which has been dormant for years, may rise as a result of stimulus measures. Historically, value has outperformed growth during inflationary periods.

- We expect that select quality value stocks that can manage through this difficult economic period should benefit as the US and global economy rebounds and inflation returns.

- Given the uncertainty regarding the timing of a reflation of the US economy and the potential for a corresponding increase in interest rates, we believe increasing exposure to both high-quality value stocks and stable growth stocks, while reducing exposure to hyper growth and deep value stocks, may be prudent.

Why Growth Has Outperformed Value

We see two primary reasons for the outperformance of growth stocks:

1. Declining inflation and interest rates – The consumer price index (CPI) declined from 3.5% in October of 2007 to 1.3% in August of 2020, negatively impacting companies that have commodity exposure, many of which are in the value universe.

The 10-year US Treasury rate, meanwhile, plummeted from 4.5% on October 1, 2007 to .68% as of September 30, 2020. This has been a negative for financial stocks, which dominate the value universe and rely on a healthy interest rate spread to generate profits. Conversely, falling interest rates have been a positive for growth stocks, as a lower discount rate has been applied to future expected cash flows, increasing the net present value of those cash flows.

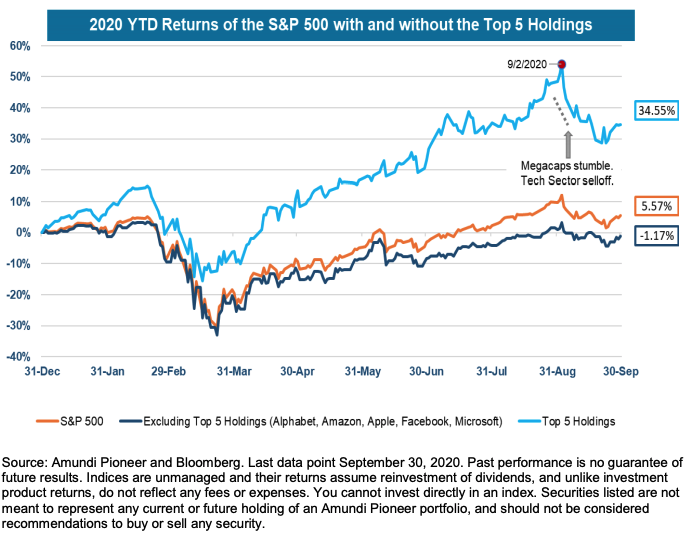

2. US Dominance in Technology-Related Industries with Strong Secular Growth – Alphabet, Amazon, Apple, Facebook and Microsoft as well as Netflix and Tesla, among other companies, have emerged as dominant in their industries, which have been growing due to the digital transformation of the global economy. The success of these companies propelled the S&P 500 Index to record highs, even amidst the pandemic.

We Believe it May Be Time to Shift Toward Value

The reasons why we believe now may be a good time to make this shift include:

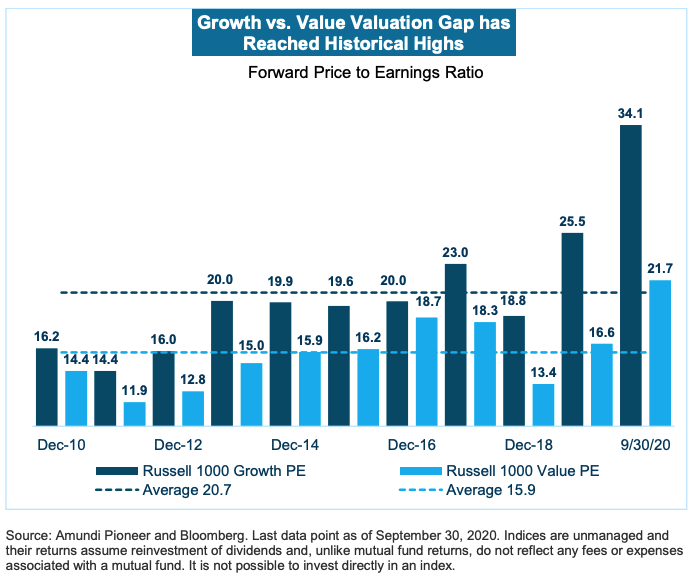

1. The valuation gap between value and growth stocks is wide – As of September 30, 2020, the Russell 1000 Growth Index was trading at approximately at 50% premium on price-to-earnings, which is the highest valuation gap in recent history.

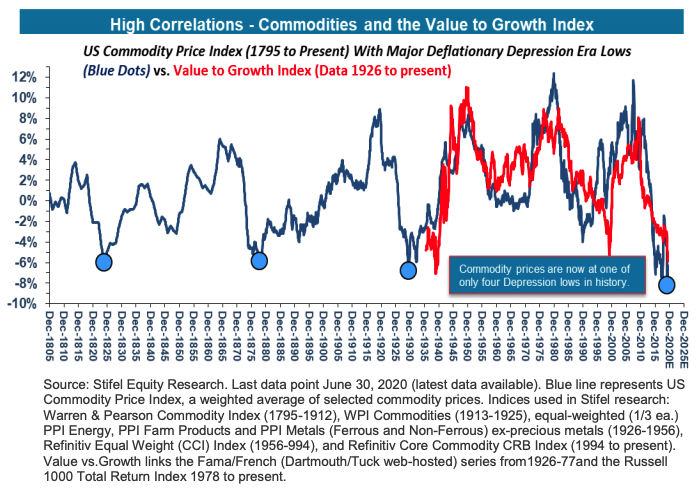

2. Possible Reflation in the US economy – Unprecedented levels of monetary and fiscal stimulus may result in a reflation of the US economy. As seen in the chart on the next page, commodity prices have been highly correlated to the value to growth index. This is because the value indices generally have much greater exposure to inflation-sensitive stocks than growth indices.

For example, the energy, financials, industrials and materials sector represented 41% of the Russell 1000 Value Index as of September 30, 2020 compared with 15% for the Russell 1000 Growth Index. In addition, commodity price trends have typically lasted for a decade or more. As of June 30, 2020 commodity prices were lower than they have been in over 200 years. While they could decline further, stimulus efforts and gradual improvements in the economy are likely to push them higher, which we believe is likely to result in value outperforming growth.

Increasing Value Exposure is Not Without Risk

In our view, the risks to increasing value exposure are threefold:

1. The first is that the US and global economies may be slow to recover from the pandemic, causing interest rates to remain low and investors to continue favoring growth stocks.

2. The second risk is that a number of companies in the value universe are structurally impaired. Some airlines, for example, will likely survive only with continued government assistance. Full-price department stores have lost share to online and discount retailers; this will likely continue even after the pandemic ends as consumers remain budget conscious.

3. Finally, a Biden victory could result in higher regulation in sectors such as energy and financials, which have larger weightings in value indices than in growth indices. Growth stocks could also be at risk under a Biden Administration due to a proposal to increase in taxes on foreign income from a minimum of 10.5% to 21%. This would disproportionally impact US technology companies, which derive 43% of their revenue from the US compared with 60% for the S&P 500. The technology sector has a higher weighing in growth indices than in value indices. In short, both value and growth stocks could be negatively impacted by a Biden victory. Offsetting this, at least in part, is the likelihood of additional fiscal stimulus under a Biden Administration, especially if there is a Democratic sweep. By comparison, a Trump reelection may result in cyclical stocks outperforming given a pro-business agenda, with large cap technology stocks a likely source of funds.

Given these risks, we believe it is important to take an active approach to increasing exposure to value.

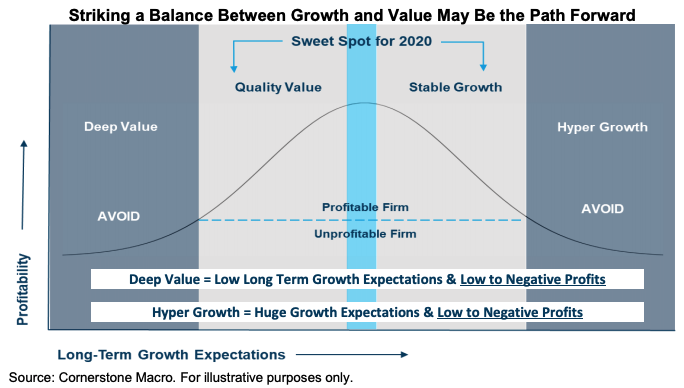

A Path Forward in US Equities

In the current market environment, we see four distinct categories of stocks:

1. Hyper growth companies that are wildly overvalued, approaching dot.com levels

2. Stable growth companies that have been highly profitable, but are also in some cases highly valued (and dependent on low interest rates/a low discount rate) to maintain those valuations

3. Quality value companies that we believe are likely to survive the economic downturn and emerge competitively stronger

4. Deep value companies that are struggling to survive the pandemic and have a questionable future (i.e. airlines, full-price department stores, restaurants), even If they do survive

We believe the most appealing opportunities in US equities are in stable growth and quality value stocks. Stable growth stocks can provide exposure to secular growth trends that are not dependent on economic growth. An example would be the shift to online retail. While a number of stable growth stocks may have high valuations, others may be more reasonably valued. Quality value stocks can offer cyclical exposure in companies that may be positioned to manage through the difficult economic period if the US and global economy take longer than expected to recover. Therefore, we believe shifting portfolio exposure in US equities away from hyper growth stocks into stable/defensive growth and quality value, while avoiding deep value, is prudent.

Given that the pandemic has increased the spotlight on labor practices and safety issues, we also believe the more successful investment strategies in this environment may be those that focus on sustainability, holistically – meaning not just from a competitive and financial perspective, but also with ESG (environmental, social and governance) considerations in mind. Doing so could enable these strategies to pursue companies that could not only survive the current economic environment, but emerge from the pandemic stronger than they were before it began.

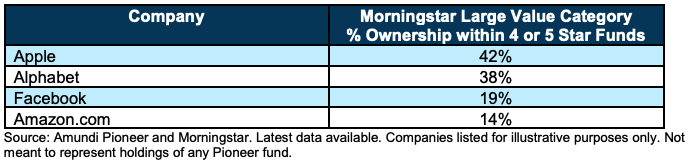

Be Wary of Value Strategies that Hold Growth Stocks

The table below offers a snapshot of the 4- and 5- star rated funds in the Morningstar Large Cap Value universe that held shares of the top 4 stocks in the Russell 1000 Growth Index as of August 31, 2020.

Value strategies that hold these stocks benefitted from their strong performance through the first three quarters of 2020, but they are vulnerable if and when these stocks begin to falter. We believe value strategies that have remained pure by avoiding these stocks offer better diversification and greater upside as value recovers, than strategies that have migrated towards growth.