Many broad domestic equity markets moved sharply higher last Monday after investors took into account stabilization in the expected outcome of the US presidential election as well as positive coronavirus vaccine news. This is shown through the SPDR S&P 500 ETF Trust SPY gaining as much as 3% intraday to complete a bullish triangle pattern at $360, which also marks a new all-time high for the core equity market representative, surpassing the September chart high of $355. The default point & figure chart of SPY reveals that this is the fourth time the fund has moved to a new chart high since August of 2018, with prior occurrences coming in June 2019, November 2019, and this past September. The further advancements that came Monday in broad domestic equities also led to a substantial increase in the Bullish Percent for NYSE ^BPNYSE, which shows an intraday reading of 65% at the time of this writing on Monday. This indicator reversed back up into a column of Xs after the market movement last Thursday from 46% to 52%, demonstrating an increase in participation of the roughly 2,000 names included in the NYSE. The drastic increase in participation Monday shows a confirmation of the risk-on appetite for domestic equity investors, with a specific increase in demand stemming from the laggard areas of small-cap and value-oriented names that make up a majority of the representatives in the NYSE.

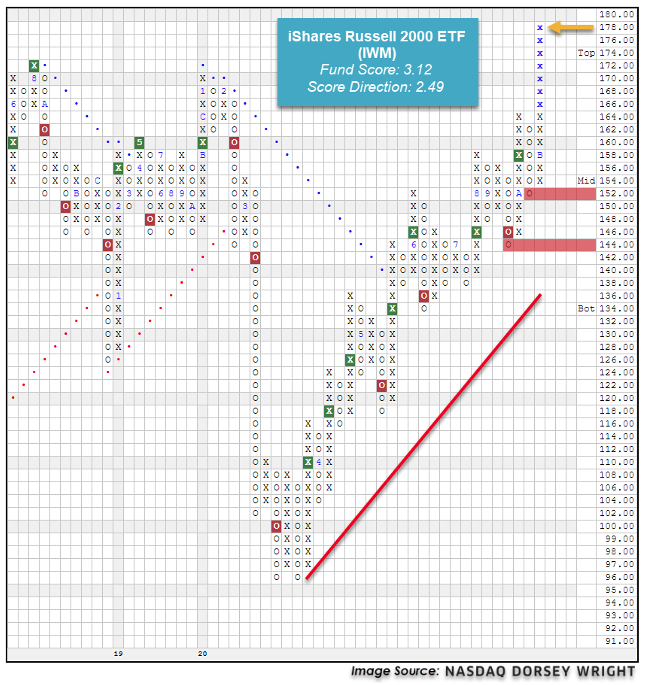

This increase in demand for small-cap names is displayed through Monday’s substantial rally in the iShares Russell 2000 ETF IWM, which gained almost 9% intraday to mark a new all-time high at $178 before backing off to levels near $170. Interestingly enough, this increase marks the first time the broad small-cap representative has reached a new all-time chart high since August of 2018, starkly different than the four all-time highs attained by SPY over the same timeframe.

The default chart of IWM rose substantially off its recent low of $96 in March to return to a positive trend in May and now sits on two consecutive buy signals with the advances Monday. The fund possesses a suitable 3.12 fund score through trading Friday, which is lower than the average all-US equity fund of 3.86. However, the 2.49 score direction is indicative of the continued improvement of IWM over the past few months.

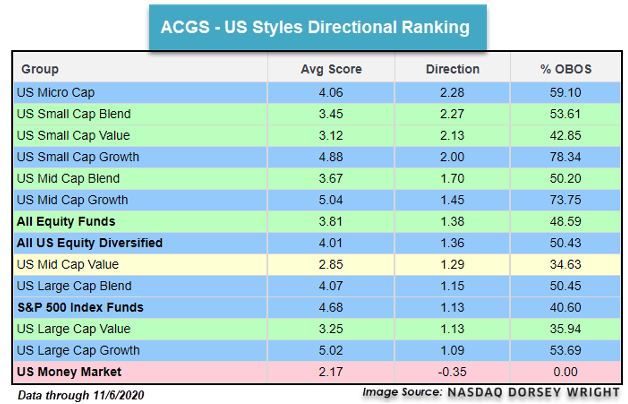

The recent improvement in small-caps has also been evident in the US Styles view of the Asset Class Group Scores (ACGS) page on the Nasdaq Dorsey Wright research platform. The average score ranking of the size & style groups still has large- and mid-cap growth in the top two positions, however, small-cap growth is close behind with an average score of 4.88 that ranks 7th out of all 135 groups on the ACGS system (through 11/6). Sorting the US styles by the average direction of each group reveals that each of the small-cap representatives has shown the most score improvement from their six-month score lows, with US micro-cap showing the highest directional reading at 2.28. Interestingly, small-cap blend and value show the next highest directional reading of 2.27 and 2.13, respectively, slightly better than the 2.00 direction of the small-cap growth group. These directional rankings provide further evidence that the improvement in small-cap names is not a new observation. Rather, Monday’s gains are just significantly more pronounced than other advances the space has seen recently. Based on Friday’s score evaluation, the growth-oriented groups continue to outpace their value counterparts across each size classification, which will also be important relationships to monitor as we move toward the end of the year.

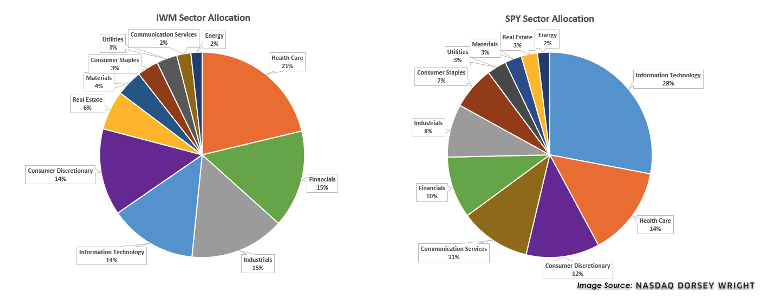

The breakdown of underlying holdings in IWM compared against that of SPY also reveal some notable differences from a sector perspective. The large-cap representative is unsurprisingly overweight technology at an allocation of about 28%, while the small-cap representative maintains half that allocation at only 14% exposure to the sector relative strength leader. In place of technology, we see IWM with a 7% higher weighting than SPY in both healthcare and industrials, accounting for 21% and 15% of the fund, respectively. IWM is also overweight financials at about 15% of its allocation, compared to just under 10% for SPY. Out of these three overweight sectors for IWM, healthcare is the only one that currently sits in the top end of the DALI domestic equity sector breakdown, with industrials and financials each in the bottom half of the rankings. Keep a close eye on these sector relationships for further developments if we continue to see outperformance from the broader small-cap space.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.