As we arrived at the beginning of November, much of the investment community had heightened concerns about the prospects for continued domestic equity growth during what was assumed to be a volatile market environment with the potential for a contested US presidential election. This has largely proven to not be the case, however, as the core domestic equity market, represented by the S&P 500 Index SPX, has posted a gain of 8.79% since the end of October. While the magnitude of these gains would have been difficult for anyone to predict, we do see that most US presidential election cycles generally produce positive returns for domestic equity indices in the two months after the election, regardless of which party wins. This is not the case every year, as some market environments remain immune to historical tendencies due to extraordinary events, such as those recently seen in 2000 and 2008. Nonetheless, the bias toward positive average equity returns following US presidential elections remains intact. Markets generally do not like uncertainty, and so it is not necessarily surprising that we typically see domestic equity improvement when most of the country understands the political direction of the US for the next four years.

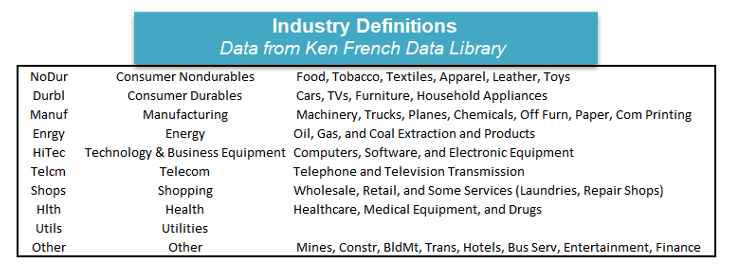

Although broad domestic equity indices have continued to march higher over the past few weeks, the assumed change of the political party in the white house brings about the question of how this may affect sector leadership within these indices. In order to examine this question further, we have looked at the historical performance of 10 broad domestic equity industry sectors following US presidential elections using data pulled from the Ken French Data Library. This is the same Ken French from the famous Farma-French Model. This data was used as it ran from October 1928 through October 2017, allowing us to take our testing back significantly further than what is offered by the current GICs sectors. A breakdown of what is included in each of the ten industries can be found below:

Using these sectors, we then took the average returns of each portfolio over a forward 2 month, 6 month, and 12 month timeframe, starting at the end of October of each election year. These average returns were then further separated by the political party that won each election, with 11 republican years since 1928 and 12 democratic years through 2016. The results of each industry’s performance in the three different timeframes can be found below, along with commentary. Note that these industry indices are market-cap weighted and use total return data.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

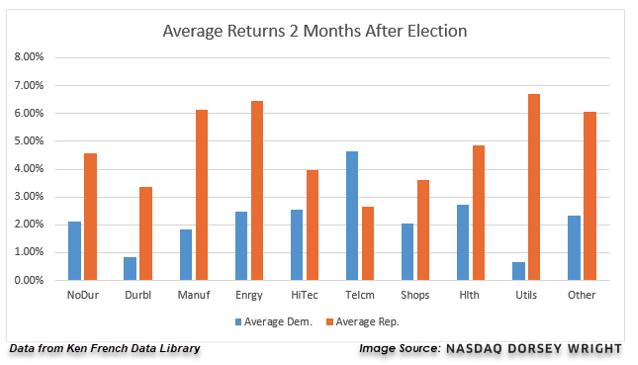

- The first observation from the forward two month return averages is that every sector posted positive average returns regardless of the political party that won the election.

- Telecom had the highest average return of any sector for years when a democratic candidate won, with a gain of over 4%. It was also the only sector where the average democratic year gain outpaced the average republican year gain.

- Healthcare, technology, and energy all sit behind telecom with average gains exceeding 2% in the two months after a victory for the democratic candidate.

- Utilities produced the worst average returns in the two-month timeframe after a democrat victory.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

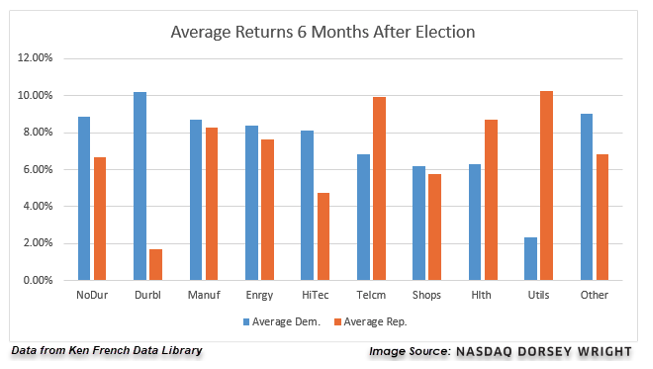

- Moving six months out from an election produces substantially higher returns in most sectors examined, with each sector again showing positive average returns regardless of the party in power.

- Consumer durables is the best performing sector, on average, in the six months after a democratic candidate wins the election, at an average gain of 10.21%.

- There are five other sectors that posted average six month gains exceeding 8% in years where democrats won: consumer non-durables, manufacturing, energy, technology, and the other classification (which includes financials).

- Utilities was again the worst performing sector for years of democrat victories, gaining just over 2% on average.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

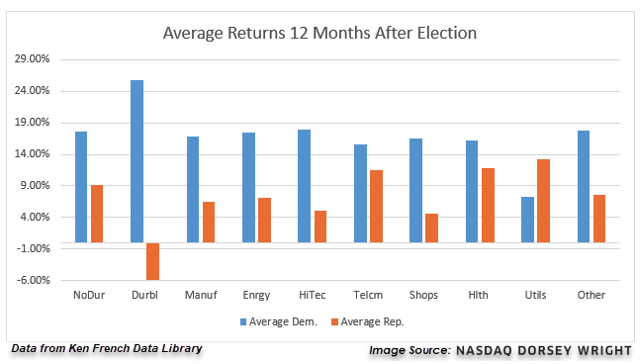

- The themes from the 6 months forward performance evaluation are furthered in the 12 month timeframe, as we see consumer durables continued to produce the highest average returns at a gain of over 25%. The average for durables in years of victories for democrats is actually the only sector-party breakdown to post a gain exceeding 20% in this 12-month window.

- Interestingly enough, the average for consumer durables in years of republican victories is the only industry to post negative returns throughout any of the three timeframes examined.

- Eight of the other sectors show positive average returns between 14-19% 12 months after a democratic victory, with utilities again bringing up the rear at an average gain of 7.28%.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.