At various points previously, we have discussed the debate regarding active vs. passive management. Proponents of passive management insist that active managers cannot consistently outperform a passive benchmark and therefore investors are better off to invest in lower cost index funds. Meanwhile, those in the active camp maintain that through their analysis and expertise active managers can produce persistent alpha. The question of active vs. passive is often framed with the premise that active or passive is always superior and focuses largely on the U.S. equity market. However, all markets are not the same and so we should examine the merits of each style on a market-by-market basis instead of taking a one-size-fits-all approach.

The key determinate of which strategy, active or passive, is superior is market efficiency. Market efficiency describes the degree to which asset prices quickly and rationally adjust to reflect new information. In a highly efficient market, any new information is quickly incorporated into prices and therefore it is not possible to consistently achieve above average risk-adjusted returns in this type of market. Therefore, due to their lower cost, passive investment strategies are favored over active management in a highly-efficient market. In less efficient markets, on the other hand, the opportunity exists for skilled active managers to outperform passive strategies, thereby adding value for clients.

As mentioned above, the active vs. passive debate often examines only large cap U.S. equities, which is a natural starting point for the discussion – the large cap U.S. equity market is composed of the most well-known companies in the world and represents a large portion of many retirement portfolios. However, if we stop there we ignore what should be an obvious and fundamental element of the discussion – the various markets around the globe are unlikely to all be equally efficient. The very fact that those U.S. large cap companies are the most visible and researched firms in the world suggests that the U.S. large cap equity market is likely to be more efficient than its less-well-known counterparts.

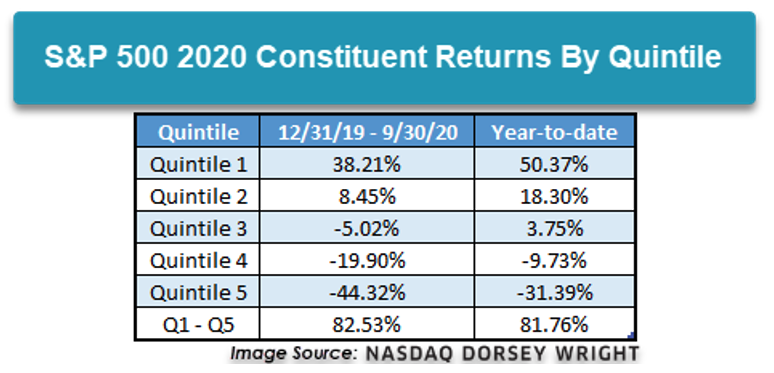

In addition to variation across markets, individual markets can also have different characteristics in distinct time periods. During the 10-year bull market from 2009-2019 active managers, especially in the U.S. large cap space, often struggled to match the performance of their benchmarks. One common refrain from the active camp during that time was that active managers were skilled at identifying quality and outperformed in down/volatile markets. 2020 has been one of the most volatile years in recent memory and there has been wide performance dispersion between the best performing and worst performing stocks. As the table below shows, there has been a performance spread north of 80% between the top and bottom quintiles of S&P 500 constituents; this dispersion has not narrowed significantly since the end of the third quarter even as laggard stocks rallied in November. This environment should offer opportunities for active management to add value via stock selection and sector allocation decisions.

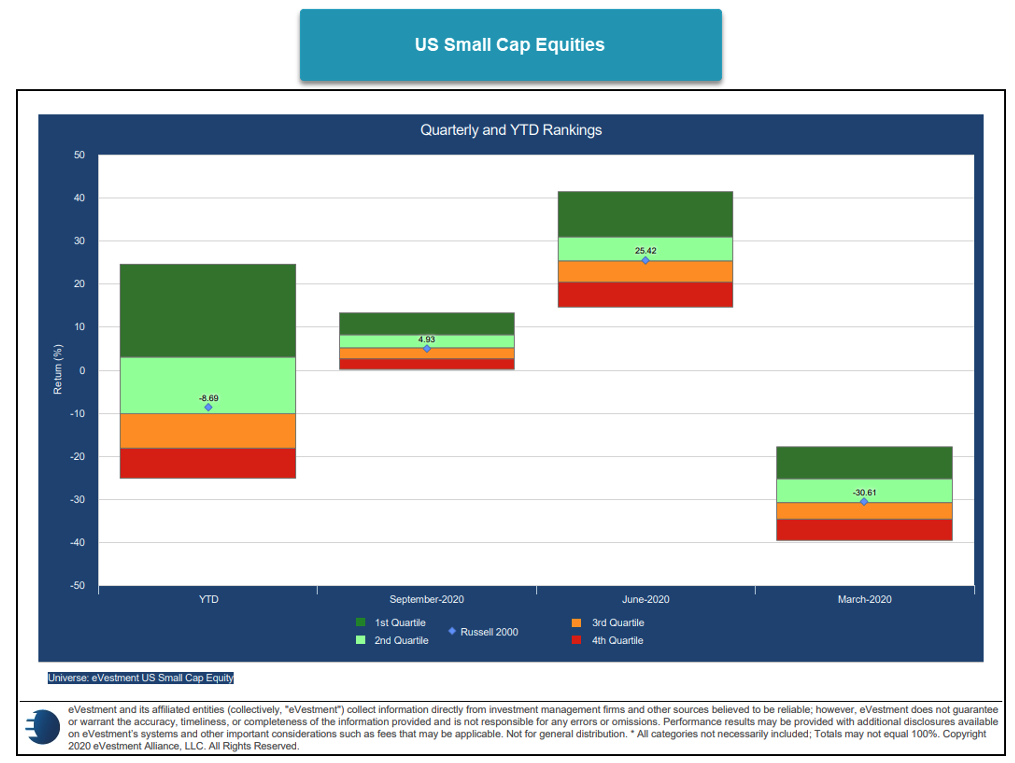

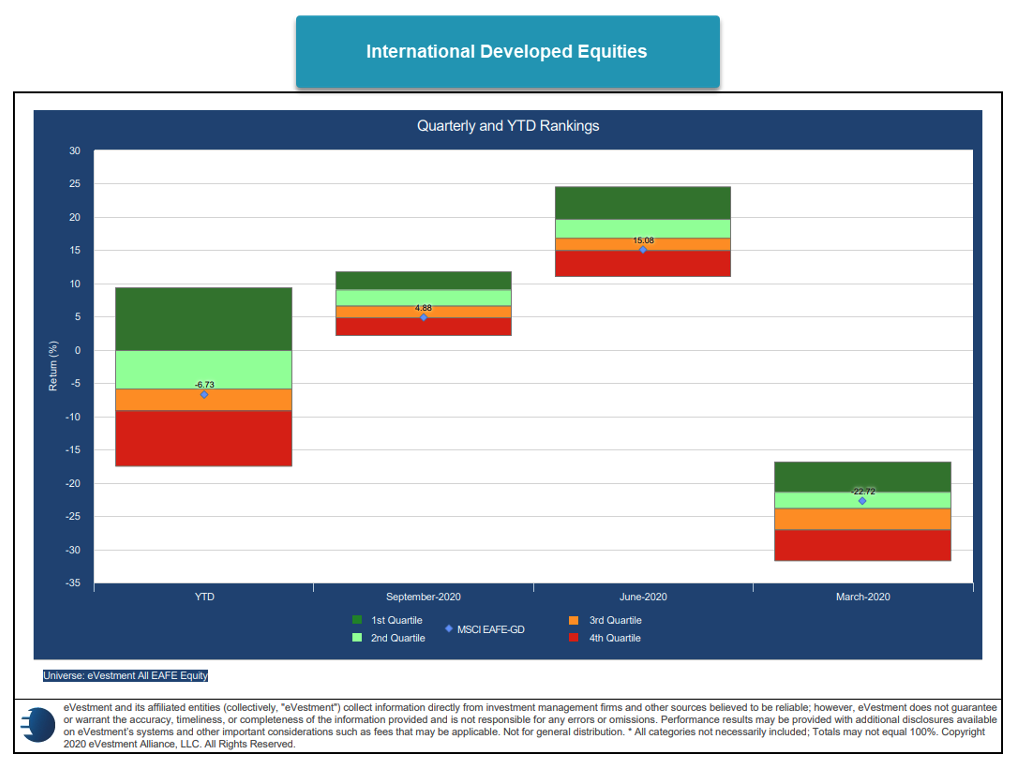

In order to see if active managers have been able to capitalize on this environment, today we’ll take a look at rankings of passive benchmarks across five markets: U.S. large cap, U.S. small cap, international developed, emerging markets, and domestic fixed income. The graphs break each universe into quartiles. If the passive fund is in the top two quartiles, that means it outperformed more than half of the managers in that market. Each image shows where the benchmark ranked in each of the first three quarters and on a year-to-date basis (through the end of the third quarter as some active managers only report results on a quarterly basis).

It does not appear that active managers in the US large cap space have been able to translate the bifurcated market and volatility of 2020 into consistent outperformance. The S&P 500 ranked in the top two quartiles in all three quarters and year-to-date. The index did not finish in the top quartile in any period, so it would not be surprising if some managers have been able to consistently beat the benchmark this year, but, on average they have lagged.

Small cap managers may have fared slightly better than their large cap counterparts as we can see that the Russell 2000 straddled the line between the second and third quartiles in each of the quarters. However, through the first three quarters cumulatively, the benchmark is above the 50% mark. On a relative basis, it appears that small cap managers may have actually done worse than usual, as over longer time periods the benchmark has often finished in the third quartile.

On average, international developed equity managers underperformed the EAFE index during the extreme volatility of Q1 ‘20. However, in the subsequent two quarters the index ranked in the bottom half and finished in the third quartile through the first three quarters of the year, meaning that the average developed international manager has beaten the benchmark in 2020. This is similar to what we have observed over longer time periods.

Active managers in emerging market equities have, on average, underperformed the MSCI Emerging Markets this year, if only slightly as the index sits just inside the second quartile through the first three quarters of the year. This is a departure from the longer-term trend, where we have often seen the index finish in the bottom half of the rankings.

The US Agg benchmark finished in the top quartile during the first quarter of the year as falling interest rates rewarded investors who held US Treasuries, while widening credit spreads were a headwind for holders of corporate bonds. Active managers regained significant ground in the second and third quarters, however, and as a result, the benchmark finished near the bottom of the third quartile. This is consistent with the longer-term trend which has seen fixed income managers consistently outperform the passive benchmark.

Overall, the market environment in 2020 does not appear to have been a catalyst for sustained outperformance by active managers as the longer-term (whether active or passive generally outperforms) seems to have been mostly sustained this year. When there were departures from the longer-term trend, more often than not, they seemed to break in the favor of passive management (the US Agg outperforming in Q1 and the EM index outperforming year-to-date, for example). This is not to say that there has been a structural shift in these markets that will tilt them in favor of passive management, but only that the increased volatility has not been the boon for active management that some proponents might have predicted.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.