The US Election and COVID-19 Vaccines: Implications for the Economy and Markets

- The likelihood of a divided US government removes a major potential headwind to the US economy, that is, higher taxes.

- With multiple Covid-19 vaccines showing promise, the US economy may surprise on the upside in 2021.

- We estimate that the ten-year yield may reach 1.00%-1.25% by the end of 2021, with foreign demand reining in potentially higher longer-term rates.

- We think equities will continue to be more attractive than fixed income because earnings yields through November exceeded investment-grade corporate yields, and the gap between dividend yields and the ten-year Treasury yield was the largest since the 1950s.

- While a divided government will limit the most aggressive policies of Democrats, including the Green New Deal, the power of Biden’s executive branch to increase regulation should bring meaningful pressure on companies to improve their ESG profiles. We expect continued momentum for ESG investing.

Divided government is good for markets

Joe Biden has been elected 46th president of the United States, and it is likely that he will preside over a divided Congress, with the Republicans maintaining their Senate majority. US voters, like the markets, appear to prefer a balance of power. While President Trump has contested the election results in numerous states, President-elect Biden is likely to be confirmed.

A divided governing combination will result in fewer and less extreme policy shifts than contemplated under a ‘Blue Wave’ pre-election scenario. Another round of fiscal stimulus should be passed shortly after Biden’s inauguration. We expect the fiscal package to total a relatively modest $1 trillion, with allocations earmarked for targeted Covid-19-related support and selected democratic platform initiatives. Biden is unlikely to be able to enact most of his proposed tax increases, and this removes a significant potential headwind to corporate earnings growth. Even more important to global economic growth and investment markets for 2021 are promising vaccine announcements from Pfizer, Moderna and AstraZeneca. These are potential watershed events for both the US and the global economy. The prospects of vaccines should have a positive impact on near-term investor sentiment, while effective vaccines are an essential element to return to economic normalcy in 2021.

Potential upside surprise for the US economy

While the rate of improvement in US growth may slow somewhat over the next few months, we believe that 2021 growth could deliver an upside surprise. A faster decline in unemployment buoyed by the manufacturing, auto and housing sectors should help mitigate the negative near-term impact of any restrictions put into place to limit rising Covid-19 infections. US unemployment has fallen from an April peak of 14.7% to 6.7% in November, indicating that a significant share of job losses earlier this year were temporary. To that point, 30%-40% of those currently unemployed are still deemed to be furloughed employees. Industries contributing to that sharp decline include: manufacturing, where the ISM Purchasing Managers Index reached a two–year high of 59.3 in October; the auto sector, where consumers have stepped up to push the annual domestic sales volume up to 15.6 million units1, and the housing market, where sales of existing and new homes have reached fourteen-year highs2

On that last point, it is notable that the housing sector accounts for approximately 15% of US GDP, while the hardest-hit sectors, including entertainment, recreation, accommodation, and food services, were roughly 4% percent of the pre-Covid-19 GDP. Promising vaccine announcements from Pfizer, Moderna and AstraZeneca represent a potential seminal moment for the US economy. These vaccines should have a positive impact on near-term sentiment and, more importantly, usher in a return to economic normalcy over the course of 2021. Assuming the broad availability of a vaccine by March, reasonable durability, and high takeup, which is highly correlated to efficacy -- which Pfizer estimates at 95%, Moderna at 94.5%, and AstraZeneca at up to 90% -- a successful vaccine should drive the economic reopening and recovery significantly beyond what has already been priced into markets. Pent-up consumer demand may contribute to outsized growth in beaten-down services sectors such as travel, entertainment, lodging and food services. Consumers have significant capacity to spend, considering that they spent only 29% of the Cares Act stimulus, repaid debt with 35%, and saved the remaining 36%. The latter has been an important contributor to the still high 14.3% US personal savings rate. We would expect continued positive momentum across the manufacturing, auto and housing sectors.

If the United States ends up with a divided government, US economic growth should benefit from the passage of additional fiscal stimulus, which we think could be approximately $1 trillion early into the Biden administration. While significantly lower than what was contemplated under a ‘Blue Wave’ election outcome, we expect that this package may combine Covid-19-related stimulus with some elements of Biden’s platform, including infrastructure spending.

Limited implementation of Biden’s platform

Under a ‘Blue-wave’ scenario, Biden’s platform contemplated up to $8 trillion in spending over ten years, funded by $4 trillion of tax increases. The reality of divided government means that, at most, Biden may be able to gain agreement on some infrastructure spending focused on surface transportation, well below $1 trillion. The Republicans are not likely to agree with Biden on most of his proposed tax increases, particularly on the corporate tax rise from 21% to 28%.

Where Biden will be able to have an impact is in increased regulations implemented through use of his executive order power.

Having designated climate change as one of his top priorities, we would not be surprised to see new regulations to limit oil drilling and methane emissions. The Biden administration can also be expected to rejoin the Paris Climate Agreement, mandate new fuel efficiency standards, expand the subsidy for electric vehicles, and provide a renewable energy credit. Biden may also increase regulation of financial institutions and enforcement. The cost of such increased regulation may be close to that reported under the Obama administration, of approximately $100 billion per year, or 0.5% of US GDP.

Finally, we expect the Federal Reserve to remain committed to easy monetary policy, particularly in light of the limited additional fiscal stimulus over the next few months. We believe that the Fed will extend all of their asset purchase programmes beyond the current December end date. Over the next few years, interest rates should maintain ‘lower for longer’, driven by the new average inflation targeting (AIT) policy. This will support economic activity, particularly interest-rate sensitive auto and housing markets.

The Treasury yield curve may steepen, primarily reflecting higher real yields, as the growth outlook improves. We estimate the ten-year yield may reach 1.00%-1.25% by end-2021. While market participants speculate that the Fed may invoke yield curve control should the ten-year yield breach 1.25%, we believe non-US investors, particularly Asian investors, will help rein in longer-term rates, given the demand for high-quality yield, and the fact that 30% of global government bonds trade at negative yields.

Collapsed yield differentials driven by the Fed’s rate cuts and commitment to low rates, combined with the increasing US twin deficits, may cause a weakening of the US dollar in the medium and longer term. Rising deficits are a certainty given Biden’s commitment to increased spending and, with a divided Congress, no significant reversal of Trump’s tax cuts. The dollar remains overvalued based on our proprietary fair value models.

Inflation should remain contained

We think inflation is likely to rise temporarily above 2% in the second quarter of 2021 due to base effects stemming from the sharp price declines during the Covid-19 lockdowns of March and April of 2020. However, inflation should rise only modestly in 2021 as a whole. Key components of the consumer price index, including shelter and healthcare costs, may moderate, continuing their near-term trends. Lower shelter costs reflect declining rents, as workers have been leaving high-cost cities during the Covid-19 crisis either to move back in with family members due a job loss, or to live in suburbs or rural areas and work remotely. Spiking healthcare costs, which benefited from government subsidies related to Covid-19 care, should fall back as the crisis abates in the wake of a vaccine. More broadly, inflation should be benign, as unemployment remains elevated and capacity utilisation stood at 72.8 as of October 2020. As measured by the ECI (Employment Cost Index), which we think is a better measure as it excludes any Covid-19-related distortions, wage inflation has been relatively contained and stood at 2.4% YoY in the third quarter, down from 2.8% in the first quarter of the year.

In the medium and longer term, inflation may rise, fueled by improving global growth, a depreciating dollar, and a dovish Fed, driven by its AIT policy.

MARKET OUTLOOK

Fixed income markets

While longer-maturity government bonds may sustain losses as the yield curve steepens, we believe corporate credit markets should continue to enjoy narrowing spreads and positive returns in 2021. Credit markets should benefit from significant tailwinds, including recovering global and domestic economic growth, accommodative monetary policy, and continued global demand for yield. Although the Fed’s US corporate bond purchase activity has been relatively limited (at around $13.6 billion in actual corporate bond and ETF purchases to date3 versus $750 billion in combined facility capacity), the Fed’s ‘presence’ has had a significant positive impact on investor confidence and spreads. Although both facilities are currently set to expire on 31 December 2020, we expect the US Treasury and Fed would quickly reopen down the road if necessary to help stabilise credit markets and economic growth.

Corporate earnings should benefit from higher growth and a stable tax outlook. Already in the third quarter, corporate earnings saw their largest upside surprise in a decade. Of the 92% of S&P 500 companies having reported third-quarter earnings, a record 84% of them beat EPS estimates4. We find both US investment-grade and high-yield markets modestly attractive, while emerging-market sovereign debt and currencies offer more attractive relative value. Within emerging markets, Asian securities and currencies may outperform, as China leads the world out of recession.

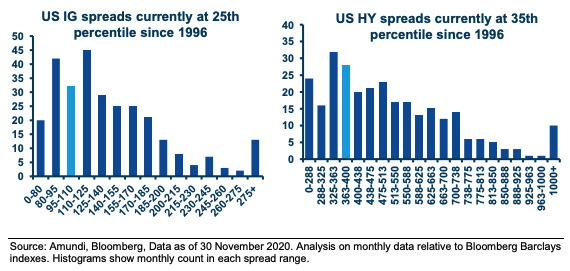

US investment-grade spreads have retraced to 101 bp as of 30 November 2020, well within the long-term average of 150 basis points, but still above near-term lows seen at the end of 2019. High-yield market spreads of 397 bp were approximately 100 bp inside of long-term averages, and 75 bp higher than the early-2020 level. In addition, we anticipate that defaults will decline through 2021. However, total yields in the high-yield market stood at record lows of approximately 5%.

Dollar IG and HY spreads

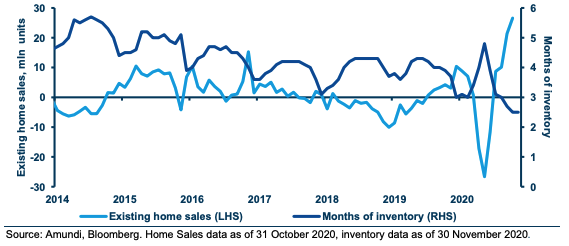

We believe US housing-related securitised markets are particularly attractive in light of the best housing market in 14 years. Home prices have risen over 6% YoY, fueled by strong demand, tight inventories, and record low rates. Demand has been driven by millennials who have reached peak household formation age, combined with the trend within the labour force to work remotely (accelerated by the Covid-19 crisis), leaving high-cost cities and states. Residential mortgage securities have also enjoyed a halving of forbearance rates since their May peak, as the unemployment rate has declined and consumers have regained their financial footing.

Home sales high, inventory low

Equity markets

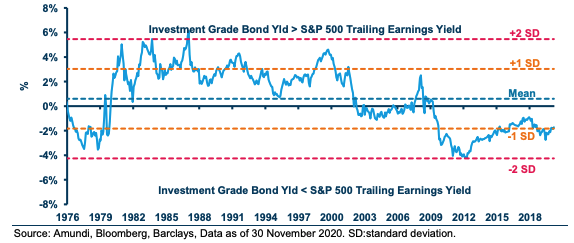

We believe equities will continue to be more attractive than fixed income because earnings yields exceeded investment-grade corporate yields as of 30 November 30 and the gap between dividend yields and the ten-year Treasury yield was the largest since the 1950s. We also believe that the 2021 economic recovery should drive a rotation from the mega-cap growth stocks towards more cyclical growth and cyclical value stocks.

Investment-grade credit yield (YTW) vs. S&P500 trailing earnings yield

Over the long term, we believe US equities could potentially outperform non-US developed markets for one simple reason: US equities are more profitable. In 2019, US equities, as measured by the Russell 1000, delivered a return on assets of 2.9%, compared to 1.3% for the MSCI EAFE Index. This higher profitability means that US companies have more capital to reinvest back into the business to grow, and/or return to shareholders in the form of dividends and share repurchases. However, in the near term, non-US stocks may benefit from the tailwinds of improving growth, led by China and the United States, by the diminishing intensity of the pandemic, and by a rotation from growth to cyclical stocks.

Cyclical and value stocks may outperform growth stocks in 2021

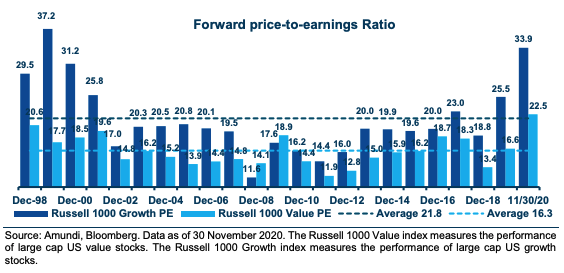

We believe that value stocks should outperform growth stocks in 2021 as beneficiaries of the economic recovery, higher infrastructure spending, and lower interest rate sensitivity. Value stocks traded at a price-earnings discount of 12 percentage points relative to growth stocks (22X vs. 34X) in the Russell 1000 Value and Growth Indices, respectively, as of 30 November 2020, based on Bloomberg data. This represents the largest valuation disparity since 2000.

As the economic recovery takes hold, we expect the S&P 500 index to see broader market participation from cyclical stocks, which are more highly represented in value indices. In addition, we expect that infrastructure spending under a Biden administration could disproportionately benefit cyclical stocks. Finally, growth stocks are more rate sensitive because they have a higher dependency on long-term future earnings than value stocks, which would be hurt more from the steepening yield curve and rising discount rates. Conversely, financials -- heavily represented in the value universe --would benefit from a steeper yield curve.

Growth vs. value valuation

We believe investors should consider shifting exposure within US equities away from hypergrowth stocks, which we believe are valued excessively, into reasonably priced stable growth (i.e., medical device stocks) and high-quality value stocks (i.e., industrial automation, parcel delivery).

ESG investments may find favour under a Biden administration

Biden has designated ‘Climate Change’ as one of his top four priorities and this may extend into the investment arena, with a greater focus on ESG mandates and company ESG profiles. Many of Biden’s priorities should only enhance ESG improvement among companies, particularly as it relates to environmental or labour policy. While a divided government will limit the most aggressive policies of Democrats, including the Green New Deal, the power of the executive branch to increase regulation should bring meaningful pressure on companies to improve their ESG profiles. That being said, the divided government, with its more moderated response to environmental policy, may make the most economic sense for US long-term revenue growth, operating margins and capital efficiency. We think this outcome may help explain the current increasing momentum for US ESG.

AMUNDI INVESTMENT INSIGHTS UNIT

The Amundi Investment Insights Unit (AIIU) aims to transform our CIO expertise, and Amundi’s overall investment knowledge, into actionable insights and tools tailored around investor needs. In a world where investors are exposed to information from multiple sources we aim to become the partner of choice for the provision of regular, clear, timely, engaging and relevant insights that can help our clients make informed investment decisions.

Discover Amundi Investment Insights at www.amundi.com

Definitions

- Basis points: One basis point is a unit of measure equal to one one-hundredth of one percentage point (0.01%).

- Credit spread: Differential between the yield on a credit bond and the Treasury yield. The option-adjusted spread is a measure of the spread adjusted to take into consideration possible embedded options.

- Cyclical vs. defensive sectors: Cyclical companies are companies whose profit and stock prices are highly correlated with economic fluctuations. Defensive stocks, on the contrary, are less correlated to economic cycles. MSCI GICS cyclicals sectors are: consumer discretionary, financial, real estate, industrials, information technology and materials, while defensive sectors are consumer staples, energy, healthcare, telecommunications services and utilities.

- Growth style aims at investing in the growth potential of a company. It is defined by five variables: 1. long-term forward EPS growth rate; 2. short-term forward EPS growth rate; 3. current internal growth rate; 4. long-term historical EPS growth trend; and 5. long-term historical sales per share growth trend. Sectors with a dominance of growth style: consumer staples, healthcare, IT

- Value style means purchasing stocks at relatively low prices, as indicated by low price-to- earnings, price-to-book, and price-to-sales ratios, as well as high dividend yields. Sectors with a dominance of the value style: energy, financials, telecom, utilities, real estate.

- Purchasing Managers' Indices (PMI): Purchasing Managers' Indices (PMI) are economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates an improvement, while a reading below 50 indicates a decline.

- Yield curve steepening: If the yield curve steepens, this means that the spread between long- and short-term interest rates widens. In other words, the yields on long-term bonds are rising faster than yields on short-term bonds, or short-term bond yields are falling as longterm bond yields are rising.

- Yield to worst (YTW): It is the lowest potential yield that can be received on a bond without the issuer actually defaulting

Important Information

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 30 November 2020. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of First Use: 9 December 2020.

Chief editors

Pascal BLANQUÉ

Chief Investment Officer

Vincent MORTIER

Deputy Chief Investment Office