“The Only Thing New in the World is the History You Don’t Know”

-Harry Truman

Dear Millennials “Welcome to the Jungle.”

“Welcome to The Jungle” Guns and Roses

Welcome to the jungle

We’ve got fun ‘n’ games

We got everything you want

Honey, we know the names

We are the people that can find

Whatever you may need

If you got the money, honey

We got your disease

Introduction

Bernie Madoff’s mother ran a “bucket shop” that was shut down by the SEC 30 years before her son ended up in handcuffs for perpetrating the greatest Ponzi scheme in American history. A bucket shop profits from clients’ trades without them knowing about it – it is basically an unethical broker. In my 2nd quarter letter, “Infatuation”, we discussed the unstoppable power of genes leaving current Millennials to finally jump into the speculative pool of stock trading, even though their parents struck out at this dangerous exercise 20 years ago.

For all Millennial readers, if you visited a casino in your lifetime only to see your money quickly disappear, you have not seen anything compared to trading versus professionals. So to all you Robinhood traders I say, “Welcome to the Jungle.” The market has fun and games for whatever you may need and “if you got the money honey” the street has “your disease.” The market is lining up your diseases -options trading, triple leveraged ETFs, coin- based currencies, tech stocks trading at 100x revenues and IPOs galore.

Playing the casinos is pikers next to trading the market. The 1999 bubble saw Nasdaq stocks fall 78% from their peak.

After years of writing that we have not seen the speculative phase of this bull market because retail trading never joined the frenzy, ka-boom a generational health crisis strangely coincided with an explosion in Joe Six Pack stock trading. There is now no question that we are starting to reflect behaviors of 1999. The good news is we are nowhere near the speculative valuations of 1999 bubble and a 78% correction is not in the near- term cards. However, in the current sea of liquidity provided by the central bank’s largesse, we could see an explosion post vaccination that would see us revisit 1999.

The entire 1999 bubble thesis comparison is currently moot due to the only chart that really matters – 10-year treasury rates being at 1%, considerably lower than the dividend on the S&P and 500% lower than 1999 interest rates. Even more urgent is the fact that in 1999 the Fed was raising interest rates, now in 2021 the Fed is planning to keep interest rates at zero for “the foreseeable future.”

Let us review some of the recent phenomena that grinds us slowly back toward the internet bubble days. Politics change, taxes change and weather changes, but human nature never changes.

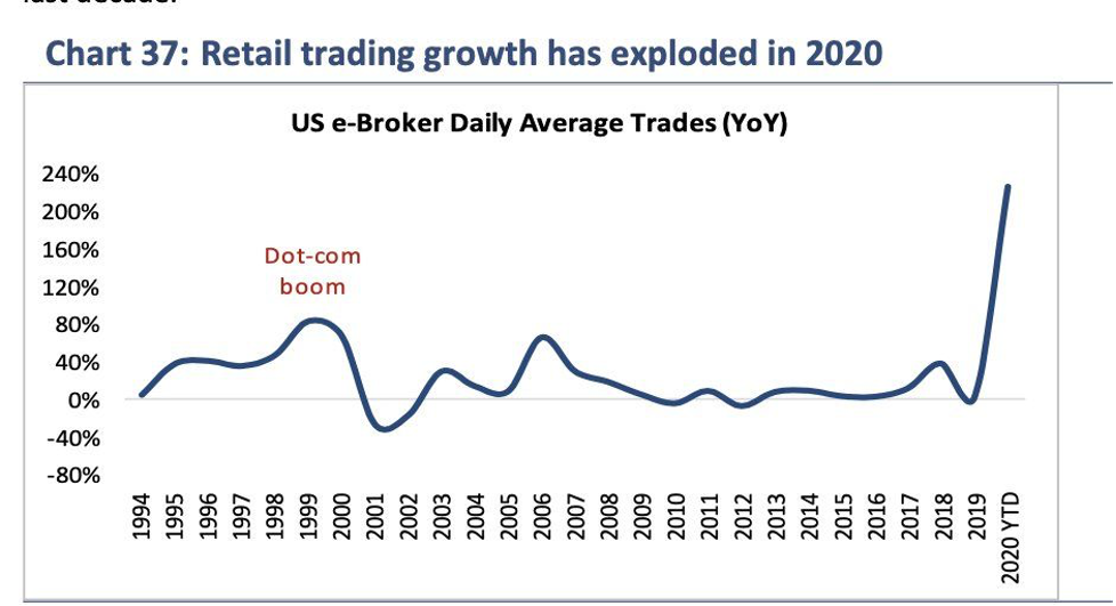

Retail Trading Explodes

In a year that investors experienced a faster stock market crash than 1929 or 1987, we also experienced the re-invigoration of animal spirits. During some periods in 2020 retail trading got up to 25% of the daily stock volume after staying flat at 10% in 2019.

This chart illustrates the longest hibernation of retail trading in history post internet bubble crash in 2000. See the flat line for two decades as baby boomers permanently swore off stock trading and swapped into index funds and shore houses. Then a massive steroid injection as the most educated generation ever (Millennials) slaps on their trading pants.

Callum Thomas Top-Down Charts

Discount Brokers Explode

In 1999 discount brokers exploded onto the scene to upend the thundering herd of old school brokers behind their phones. The number of online brokers grew from 12 in 1995 to 100 in 2000 with E-Trade at one point adding 5,000-10,000 accounts daily as the lure of $7 trades coupled with the internet bubble was too much for most humans to resist.

CNN. Money 1999 “Online trading firms such as E*Trade Group (EGRP), Ameritrade (AMTD) or Datek Online — full of energy and dressed in brilliant colors to grab attention — have been on a mad dash. CS First Boston recently estimated that online trading volumes ballooned at their fastest quarter-by-quarter rate to start 1999, at 47 percent in the first quarter, blowing past a previous record of 34 percent. Online trades now account for just under one in six trades in the stock market.”

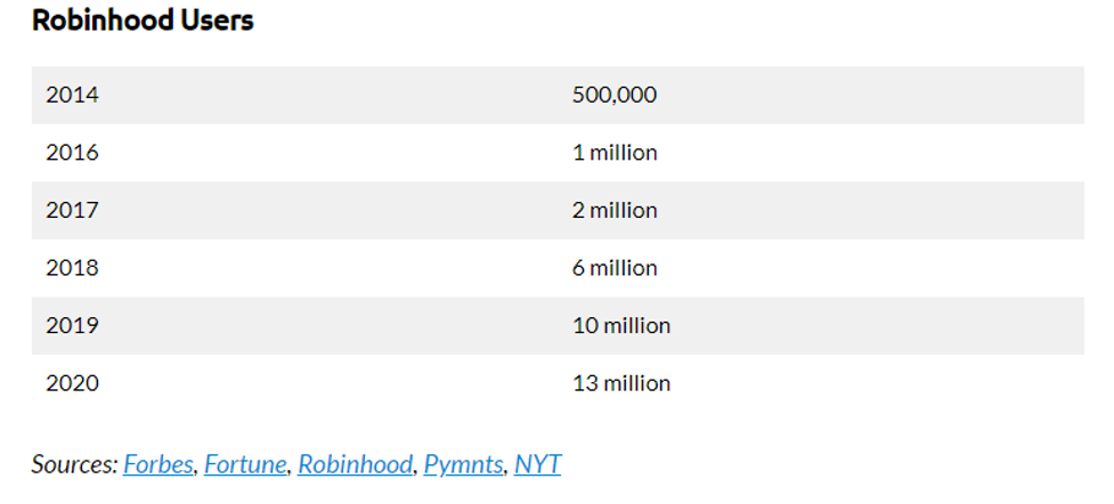

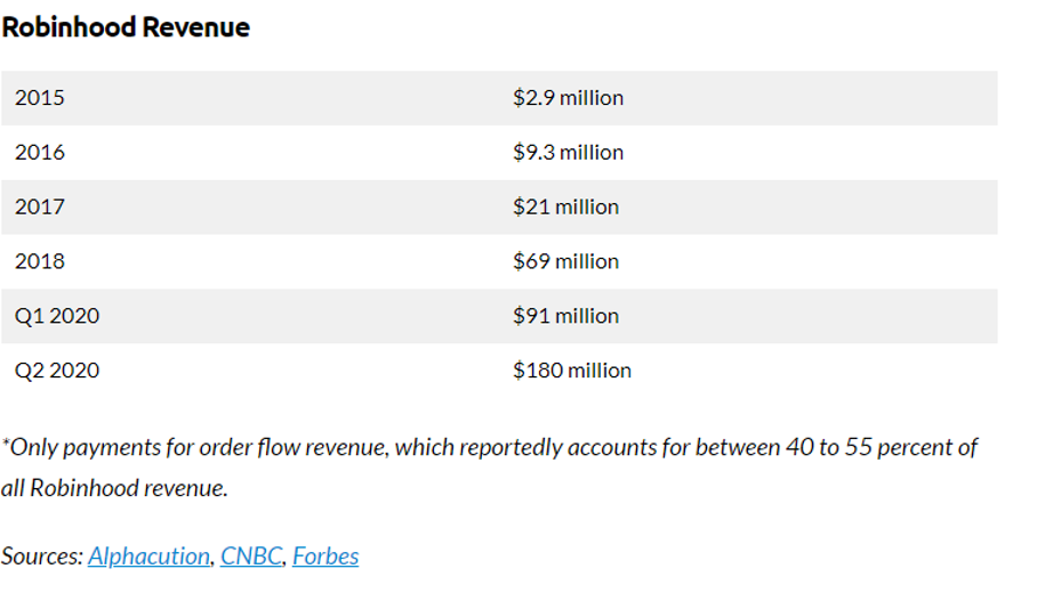

Fast forward to 2020 and Robinhood trading comes on the scene with zero commission trades and a slick app that fits the way Millennials' brains function. Robinhood has jumped from 500,000 users in 2014 to 13 million in 2020 with matching revenue growing from $2.9m to $180m. Robinhood is also a shining example of the technology conundrum, meaning how much of our technology is helping us and how much is hurting us.

Robinhood claims to be ‘Democratizing” the markets while making it fun and exciting to boot. Robinhood is the discount broker model of the 1999 bubble, on artificial intelligence steroids, and attached to investors I-phone hip 24/7.

As Marty Zweig describes in the WSJ, Robinhood is filled with Vegas like slick software and 24-hour pop-up alerts all encouraging users to trade more.

“Signing up was fun and easy. Three mystery cards emblazoned with question marks popped up. I scrubbed to reveal which free stock I had won, like in a scratch-off lottery game. Confetti showered my phone screen: I had gotten one free share of Sirius XM Holdings Inc., at $5.76.

The next morning, my phone lit up: “Your free share of SIRI is up 1.05% today. Check on your portfolio now.” Two hours later, Robinhood nudged me again: “Start Trading Today.” An email from Robinhood proclaimed “You’re Ready to Begin Trading!”

Robinhood Revenue and Usage Statistics (2020)

IPO Market in the Process of Exploding

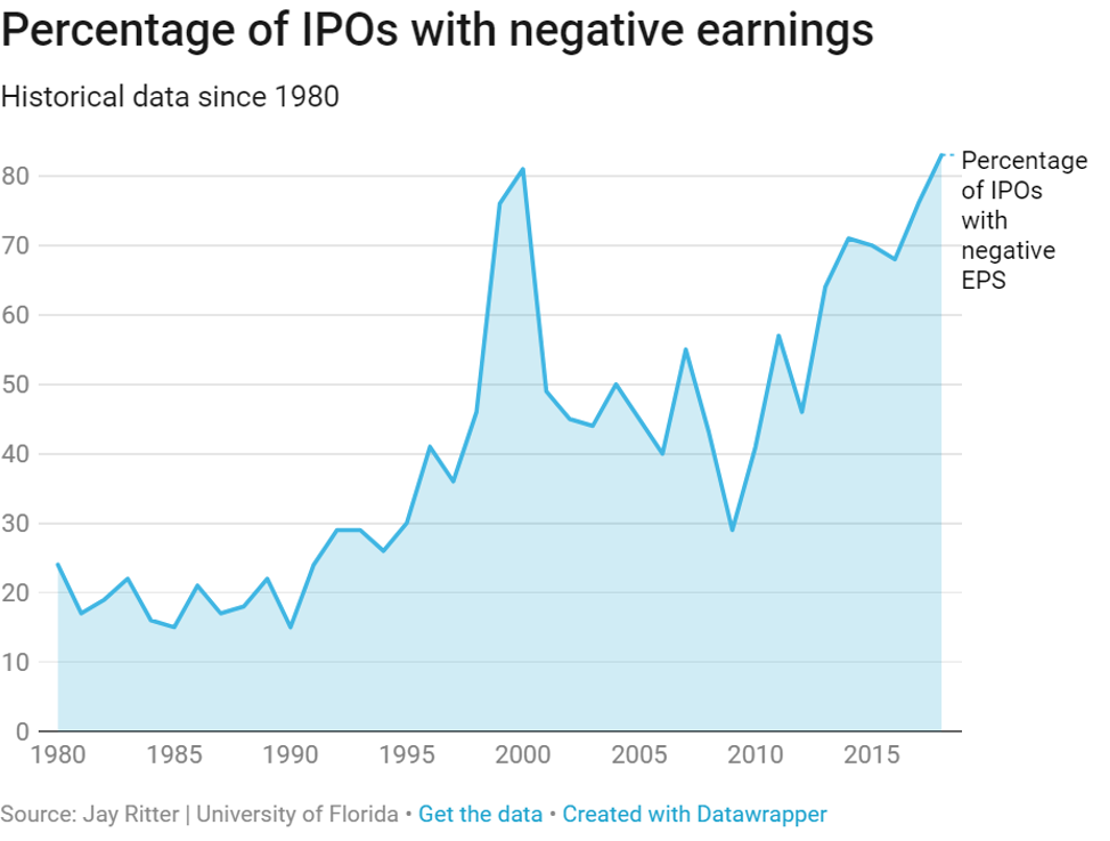

The IPO market is not yet at euphoric levels of the internet bubble where 547 companies went public in 1999, but we’ve already matched the number of IPOs with negative earnings and the total amount of IPO profits.

Negative Earnings IPOs Above 1999 Levels

Profits from IPO Market Above 1999 Levels

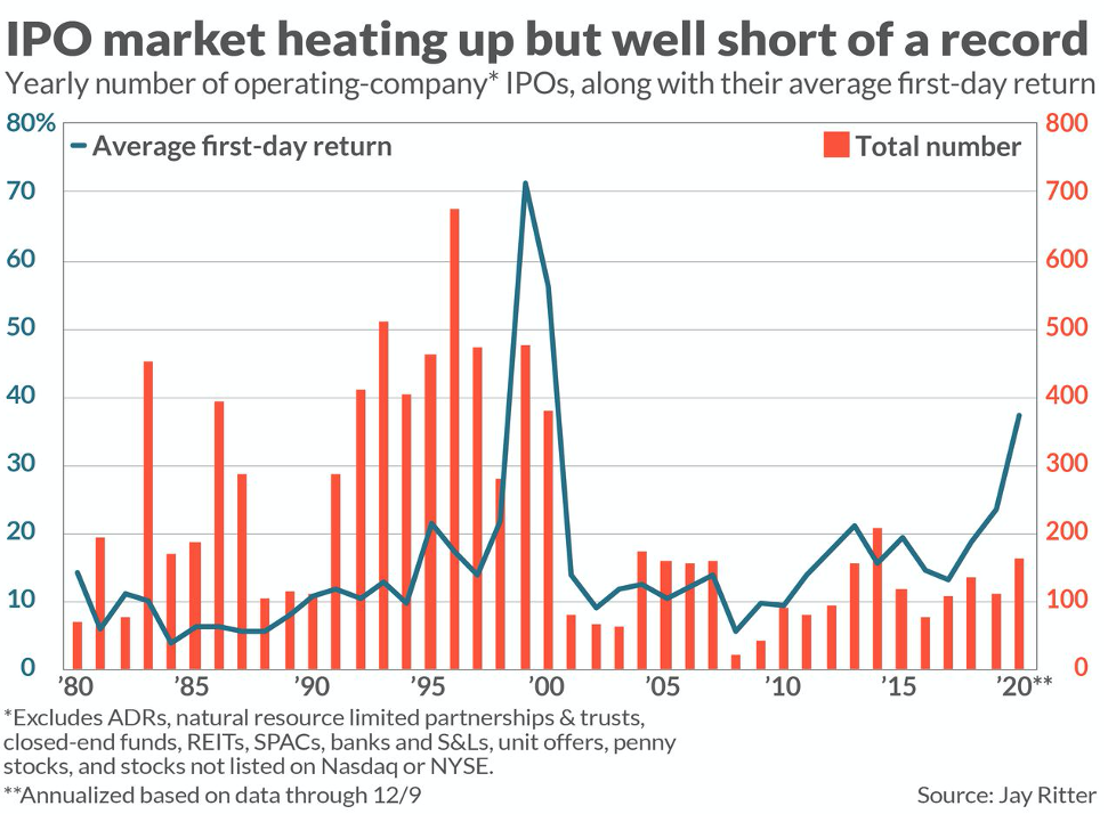

The total number of IPOs in 2020 is less than half the 1999 levels but the street has a 2021 pipeline that could make a run at the internet bubble highs in number of deals per year.

State of play: There are over 500 “unicorns,” or upstart companies that are valued at $1 billion or more by venture capitalists, according to CB Insights. More than half of those are based in the U.S., and around two dozen are valued at more than $5 billion. The newfound retail euphoria for stock trading will lead to investment bankers convincing Unicorn clients to “not miss the window” for monetizing your company into public markets.

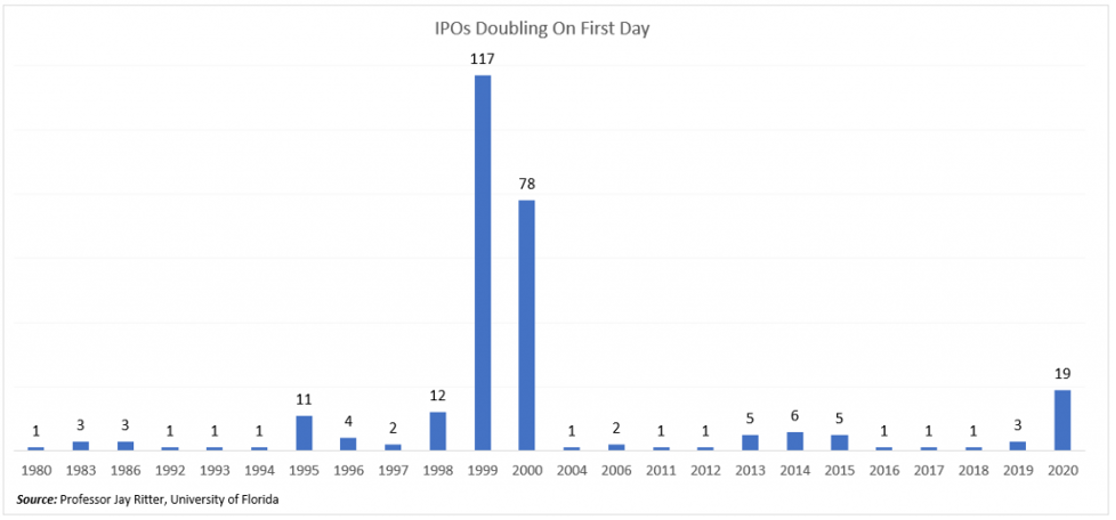

The most vivid example of why we are not yet at 1999 bubble levels is the next chart showing the insane amount of IPOs that were doubling on the first day. Although some IPO ETFs saw 100% gains in 2020, that pales in comparison to the 350% return for IPOs in 1999 before the internet bubble crash.

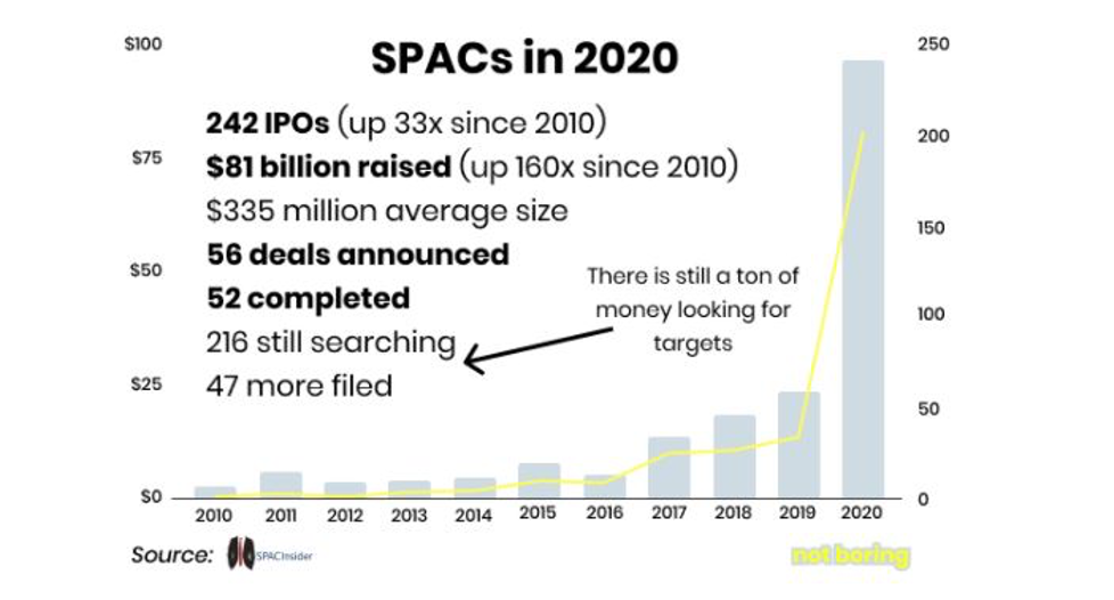

SPACs Explode

SPACS also known as blank check companies where money is raised before a company is chosen for purchase, are exploding. SPACS raise cash then have two years to purchase a company. SPAC IPO fundraising is now at a stunning 33x 2010 levels.

SPACS, once playing in the underbelly of Wall Street, are now sponsored by major investment banks Credit Suisse, Deutsche Bank, and Goldman Sachs. In the interest of keeping this letter short, I would encourage investors to read up on SPACS, but it’s safe to say this kind of growth is becoming speculative, especially when you see celebrity sponsors like Billy Beane, Shaq, and Paul Ryan.

These businesses are too strong, too dynamic, and have seen the future. There is no going back.

Technology Stocks See Record High Valuations with Dominant Outperformance

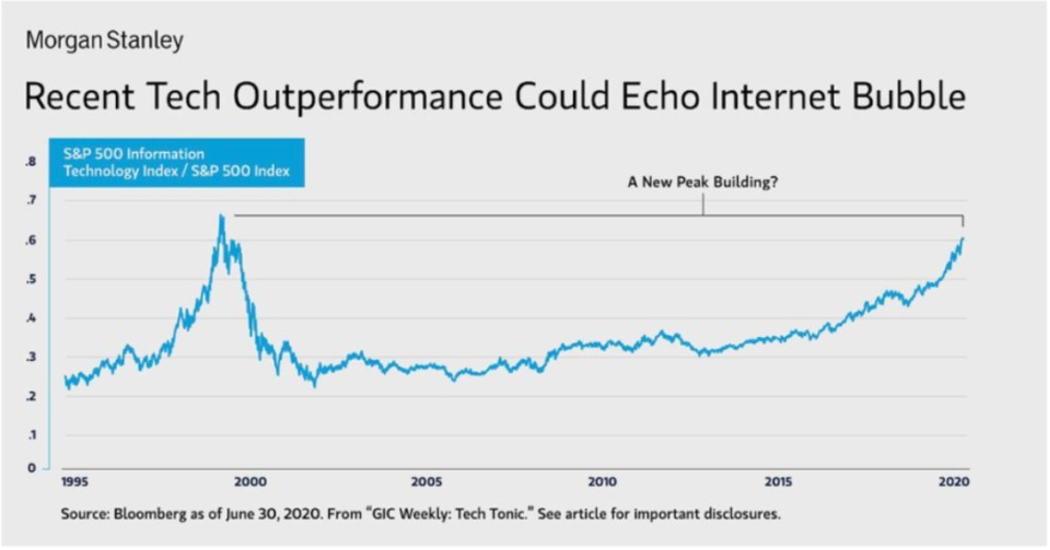

We have not witnessed fraudulent tech IPOs like 1999, but we have re-visited record outperformance of tech stocks versus other sectors returns to previous record levels.

Tech Outperformance Hitting 1999 Levels

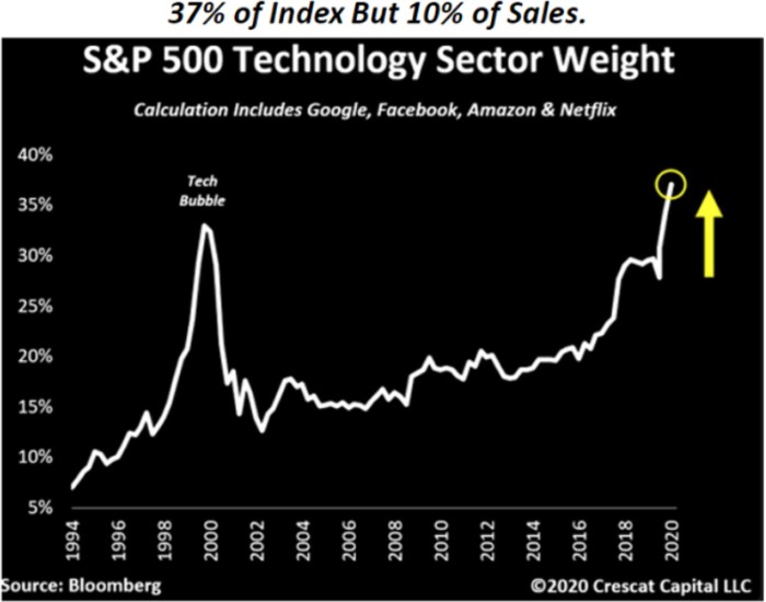

This level of outperformance has led to technology stocks exceeding 1999 record weighting in the S&P 500. The chart below highlights the tech sector weighting as 37% of S&P.

S&P Tech Weighting Passes 1999 Levels

Venture Capital Investing Soars to New Highs

Again, although the total number of deals is lower, the dollar amount raised is converging fast. The 1999 bubble was followed by close to a 10-year period of record venture capital fund underperformance, as it took that long for all of the no-revenue junk to run its course in the funds.

U.S. Venture Capital Funding Reaches Dot-Com Era Level

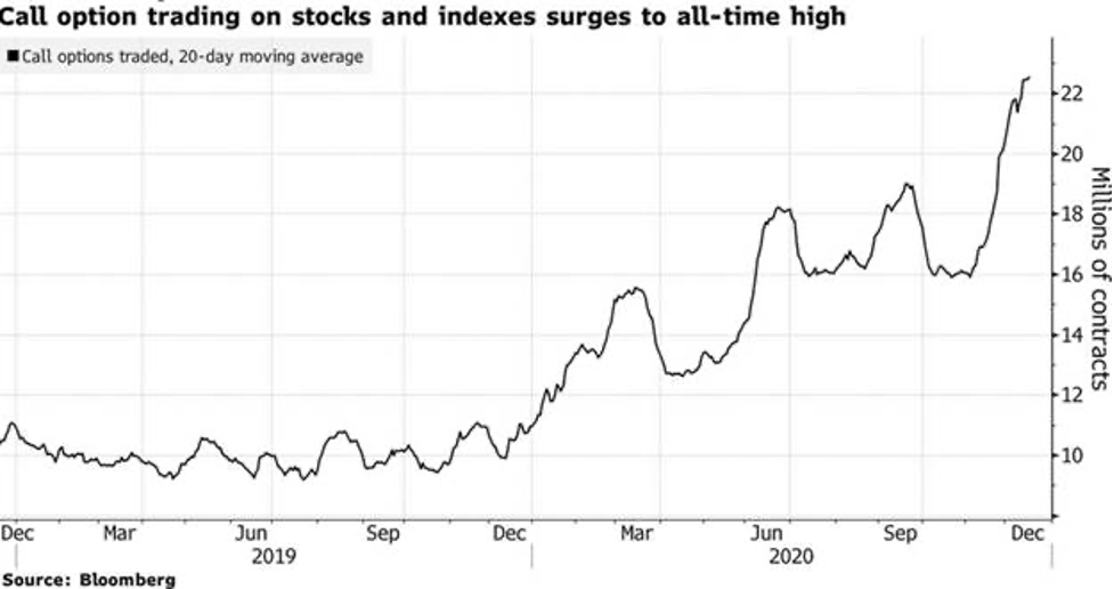

Surge in Call Option Trading on Stocks

This is the most perplexing one to me. No one and I mean no one that trades options make money, except the broker selling the options. Yet we have witnessed a frenzy of naked call option buying to leverage bets on already hot stocks like Tesla and Apple. Retail investors will not lose money playing the option game, they will get financially annihilated.

Barron’s “Option volume in single-stock equities averaged a record 18.4 million contracts a day in August (each contract gives the holder the right to buy or sell 100 shares of stock), up about 80% from the average monthly volume during 2019, according to Cboe Global Markets. But much of the action this summer has involved investor purchases of call options to effectively get leveraged bets on leading stocks. “There has been a huge ramp-up in speculative trading,” says Jason Goepfert, president of research firm Sundial Capital Research, who has called it a “retail option-trading frenzy.”

To put things in perspective, Softbank, the Japanese conglomerate ranked as the 36th largest company in the world, decided to try its hand at options this year and managed to rack up a $3B loss. Softbank thought venture capital was high risk business until they saw $3B go poof overnight in the ultimate “Welcome to the Jungle” game of options trading.

From Dave Lutz at Jones Trading.

Hot Managers Explode

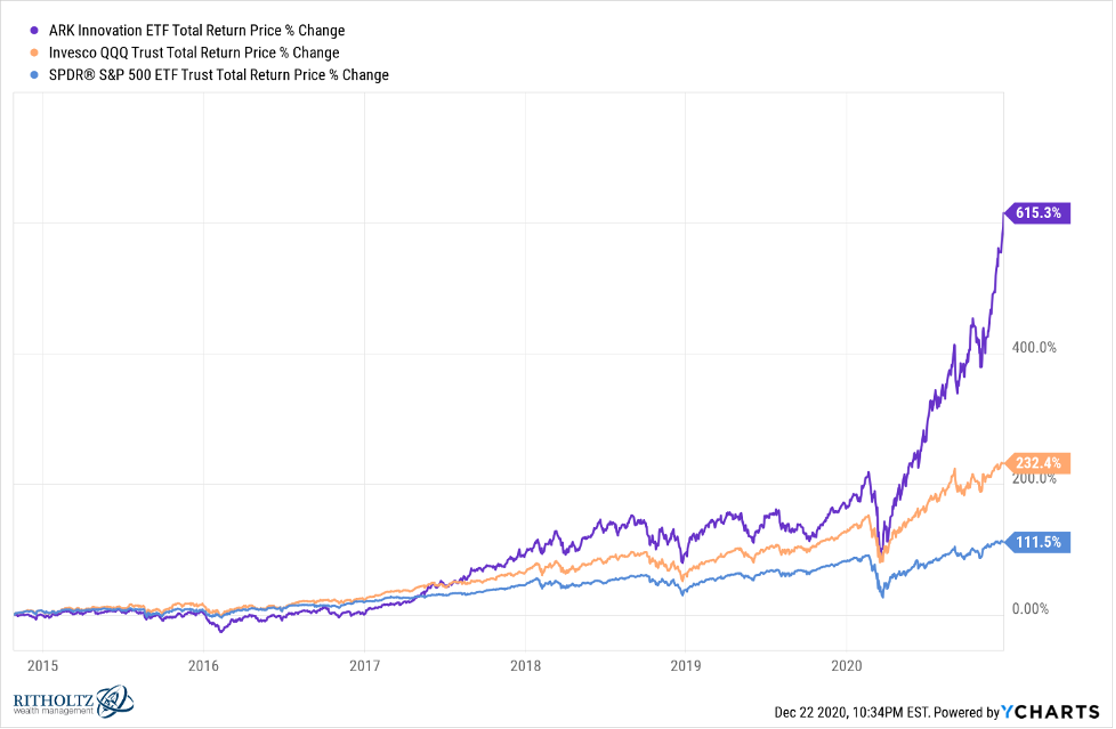

Cathie Wood, founder and CEO of ARK Innovation, is brilliant for creating her ETF offerings. But in 2020 they went parabolic – like 1999 technology stock mutual funds. In classic retail investor behavior of chasing the hot funds, ARK innovation ETF saw a 900% increase in new money flows during 2020.

Ben Carlson at A Wealth of Common Sense does a fabulous job of summarizing story.

Conclusion

As we close out 2020, we do have more similarities to 1999, but we are not yet in full bubble status. Keep in mind the Nasdaq did not re-capture above 5000 levels attained before the internet crash until Spring of 2015 and it took until 2017 to get to 6000. Also, the current interest rate environment favors more speculation and risk. Finally, we have record amounts of cash on the sideline with the majority of fund flows in 2020 going to fixed income which is earning investors zero and possibly facing principal risk.

My third quarter letter discussed the massive pre-election inflows into bonds which isa tell- tale sign that the stock market was unlikely to crash, no matter which party won the seat. We also discussed historic trends of flows reversing post-election out of the safety trade and back into equities. That scenario has played out exactly in the last two months.

3rd Quarter Letter-Betting on Zero

The market is not cheap with the S&P trading at 21x expected earnings, leaving us 24% above last 25 year average. But equal weighted S&P is trading at 17x earnings, only 10% above last 25 year average. In simple terms, the S&P is expensive due to overweight in tech names, but ex-tech valuations are not far from median.

Here was my quote in Joe Distefano’s March article for Philadelphia Inquirer on COVID-19 market crash.

Topley himself sees key differences between the fall 2008 and winter 2020 crashes. This is a health crisis, not a credit crisis. And traditionally, health crises lasted months not years,” he told me. And when markets fall sharply, they also tend “to rebound sharply.

The 2008 crisis ended a bubble real estate market with unsustainable asset prices. By contrast, Topley says, the U.S. economy, pre-virus, “was in relatively good shape, low unemployment — and slightly rising wages, though not as much as we should see.”

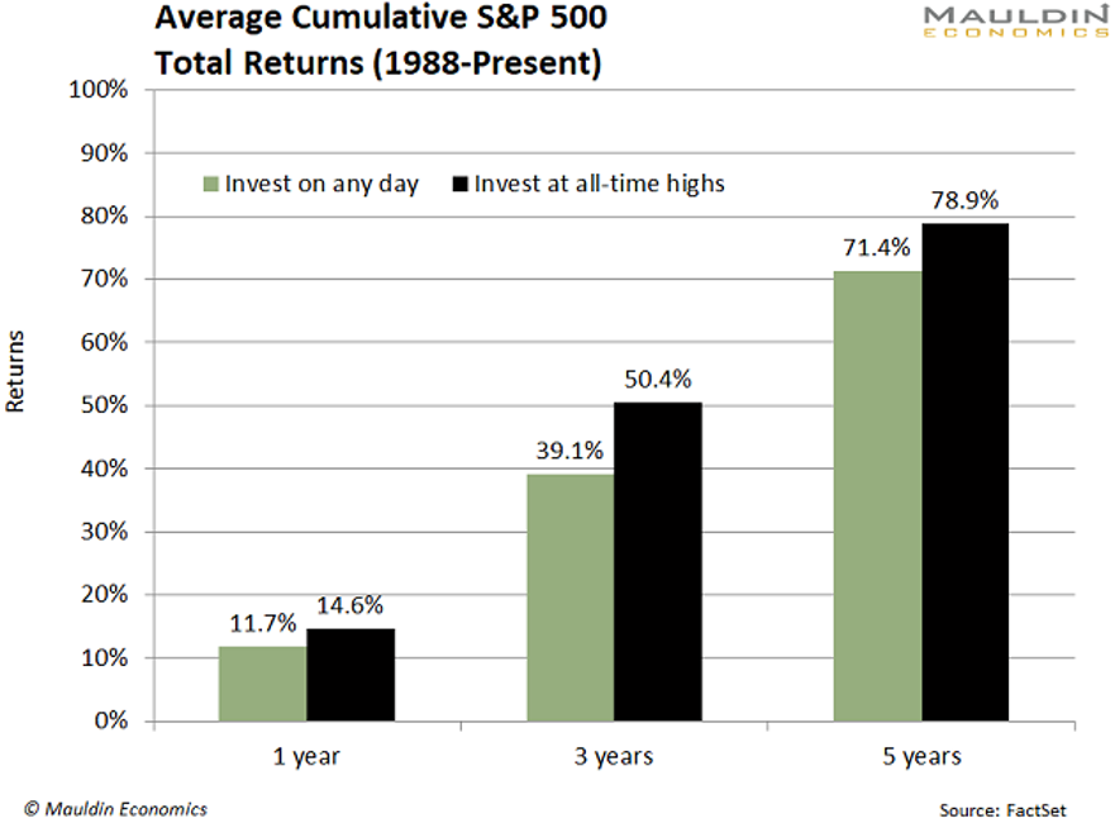

The market fell sharply and rebounded sharply, so the question is what happens next? Since 1988, the S&P 500 returns were significantly higher on one, three, and five-year time horizons when the index was at all-time highs like today.

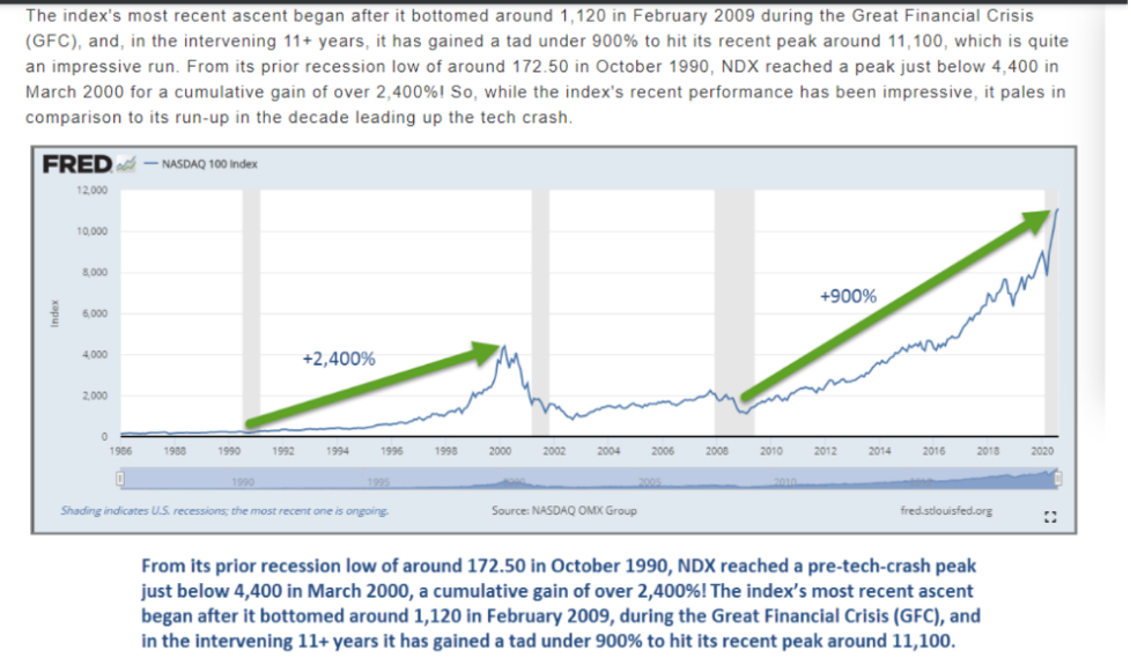

As mentioned in my 3rd quarter letter, from the 1990 recession low the Nasdaq rallied 2400% versus a 900% rally today. We have all the 1999 similarities starting to play out, but we are nowhere near the lofty internet bubble valuations especially, after factoring in interest rates.

In conclusion, some investors have elected to enter the jungle, but the fun and games may just be starting. Nothing is guaranteed in the markets, but a few things have overwhelmingly negative odds such as day trading stocks, retail investors buying call options, and retail investors playing the IPO market. At Lansing Street, we adhere to the saying that investing is a psychology game not an IQ game. Presently, we have investors experiencing recency bias around tech stocks only going up, but those that do not learn history are doomed to repeat it.

In the jungle

Welcome to the jungle

Watch it bring you to your

Knees, knees

I want to watch you bleed

Matt Topley

President & CEO

Lansing Street Advisors

Disclosure

Lansing Street Advisors is a registered investment adviser with the State of Pennsylvania.. To the extent that content includes references to securities, those references do not constitute an offer or solicitation to buy, sell or hold such security as information is provided for educational purposes only. Articles should not be considered investment advice and the information contain within should not be relied upon in assessing whether or not to invest in any securities or asset classes mentioned. Articles have been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Securities discussed may not be suitable for all investors. Please keep in mind that a company’s past financial performance, including the performance of its share price, does not guarantee future results. Material compiled by Lansing Street Advisors is based on publicly available data at the time of compilation. Lansing Street Advisors makes no warranties or representation of any kind relating to the accuracy, completeness or timeliness of the data and shall not have liability for any damages of any kind relating to the use such data. Material for market review represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Indices that may be included herein are unmanaged indices and one cannot directly invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information included herein is for illustrative purposes only

© Lansing Street Advisors

Read more commentaries by Lansing Street Advisors