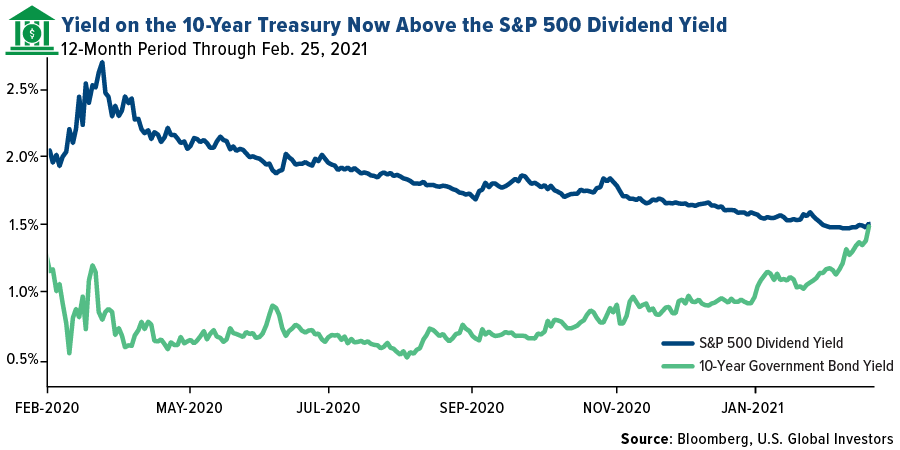

Government Bond Yields Have Surged, but Real Yields Are at Zero

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Government bond yields have been rising steadily for the past three months, but they went parabolic in February. The yield on the 10-year Treasury touched 1.6% yesterday, up from 0.9% just a couple of months ago. That’s more than a two standard deviation move, suggesting the bond selloff may be overdone. Remember, bond yields rise as prices fall.

Yields have jumped so much, in fact, that they’re giving stocks a serious run for their money. The 10-year yield is now higher than the S&P 500 dividend yield, which may have added to the selling pressure that cost stocks close to 2.5% yesterday.

It’s important to recognize the reasons why yields are rising. In an email to clients today, Evercore ISI analysts explained that the move is “associated with the higher inflation expectations” and that investors are pricing in “a positive economic skew.”

In other words, as expectations of a strong economic recovery mount—assisted by trillions in fiscal stimulus, loose monetary policy forever and hopes of herd immunity by summer—so do expectations for higher inflation.

This is a topic I covered in a Frank Talk this week. Despite what Federal Reserve Chair Jerome Powell says, prices for a lot of assets are far from “soft” and likely to continue rising as more and more liquidity is pumped into the economy.

There’s a quote by Stanley Druckenmiller I want to share with you here. On a recent episode of “Talks at GS,” the billionaire investor said that “the longer the Fed tries to keep rates suppressed… the more I win on my commodities.”

Indeed. Interest rates were slashed to near-zero last April, and since then commodities have increased about 45%, as measured by the Bloomberg Commodities Index. But they’re not done yet. I believe we’re just one big infrastructure spending package away from a full-blown commodities supercycle.

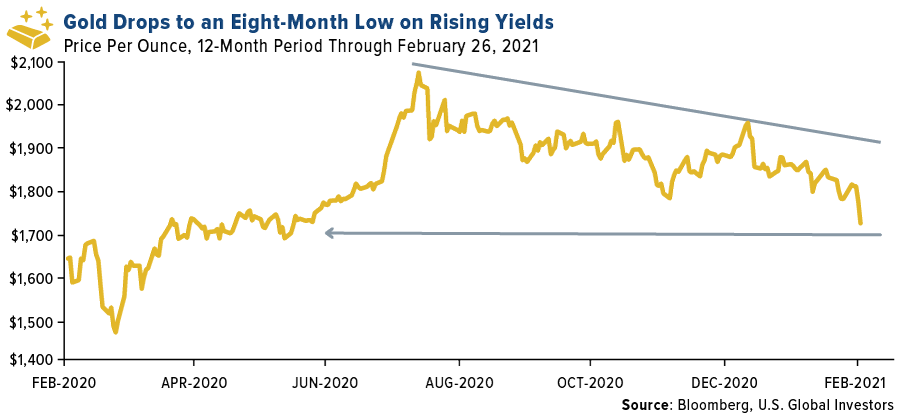

With Real Yields at or Below 0%, Is It Time to Buy the Dip in Gold?

Gold participated in the rally, hitting a new high in August, but since then it’s been stuck in a downtrend. The metal, which has the highest weighting in the commodities index at more than 13%, is being clobbered right now by rising yields. Today it fell further to an eight-month low.

When it comes to trading gold, I think what’s important for investors to pay attention to is not so much nominal yields but real yields. Right now the 10-year bond is trading with a yield of 1.4%, which is the exact same rate that consumer prices rose at in January year-over-year, according to the Bureau of Labor Statistics. So in reality, inflation is eating your lunch even with the yield increase.

I expect gold to catch a bid when consumer prices really start to turn up on additional stimulus. Until then, I see now as an attractive time to buy.

Want to hear more about gold investing? Register for our upcoming webcast (“Gold and Crypto: There’s Room in Your Portfolio for Both”) by clicking here.

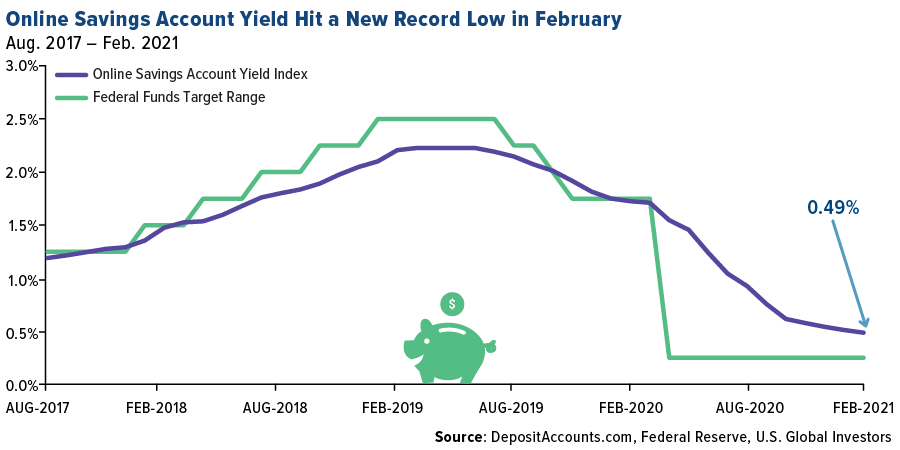

Record Low Savings Account Yield

Plus, you’re not gaining anything by leaving your money in the bank, and I mean that literally.

The average yield for a personal savings account fell to a new all-time low in February, according to an index by DepositAccounts. How low? Try 0.49%, which doesn’t come anywhere close to matching inflation, to say nothing of beating it.

Low interest rates tell only a part of the story of why this is happening. The other part is that Americans are squirreling away their money like never before, putting pressure on savings account yields. At the end of 2020, U.S. banks held a record $17.8 trillion in deposits, up significantly from $14.5 trillion a year earlier, as people were stuck at home with fresh $1,200 stimulus checks.

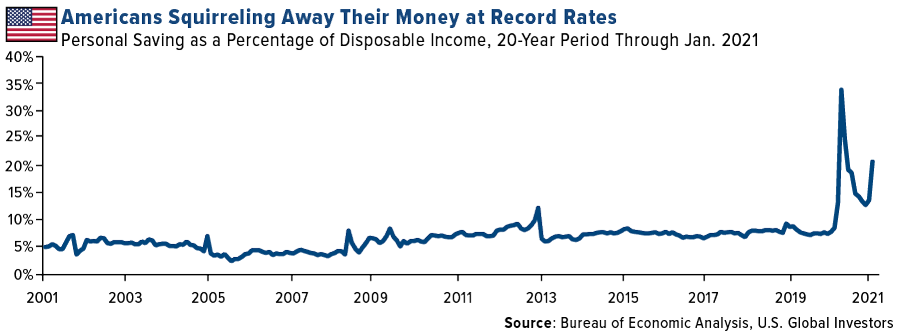

Here’s another way to look at it. The chart below shows you personal saving as a percentage of disposable income. You can see that the rate skyrocketed to 33% at the beginning of the pandemic, and though it’s tapered somewhat, it surged again in January thanks to the second round of stimulus.

Granted, not all of this money is sitting in a bank, but a lot of it is, and it’s earning nothing.

Trillions of Dollars Arriving Soon… From Thrifty Households

On the plus side, when everyone gets vaccinated and the pandemic ends, these massive savings will be unleashed on the economy as people get back to their pre-pandemic lives, book vacations, send their kids to college and more. (Colleges in the U.S. saw an unprecedented 13.1% plunge in freshman enrollment in the fall of 2020 compared to the same period a year earlier.)

Last I checked, $17.8 trillion (the amount held in banks) is a bigger sum than $1.9 trillion (the size of President Joe Biden’s relief bill, which Congress is expected to pass this evening). All of that pent-up capital is just waiting to be put into use, which is highly positive going forward.

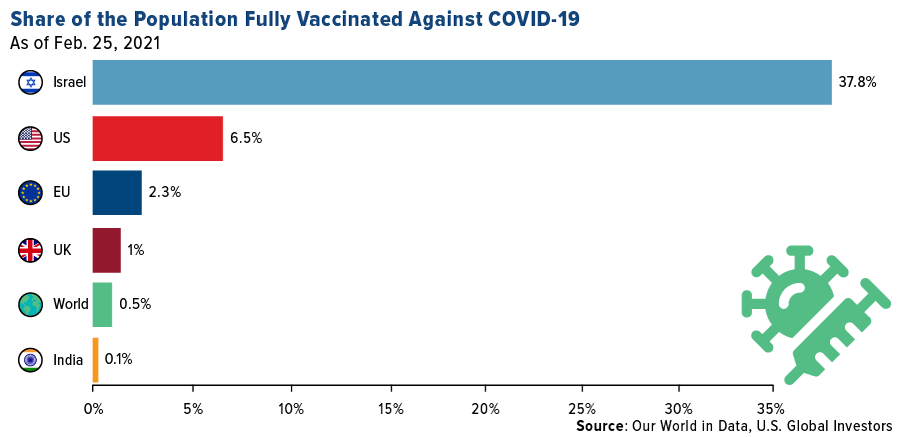

We’re well on our way to vaccinating everyone, but there’s still a long road ahead of us. Millions of doses have been administered (I got my second shot this week and feel great), and yet only 6.5% of the U.S. population has been fully vaccinated. Israel is the global leader with 37.8% of its population having gotten the vaccine.

A Knockout Quarter for Thunderbird Entertainment

|

On a final note, Thunderbird Entertainment reported this week, and it was a knockout quarter. For the quarter ended December 31, revenue came in at $28 million, a jaw-dropping 98% increase year-over-year. The company had 21 programs in various stages of production during the quarter, on networks and platforms as diverse as Netflix, Nickelodeon, Apple and Disney+.

Thunderbird, which trades on the TSX Venture (TBRD.V) and over the counter in the U.S. (THBRF), has been named to the 2021 TSX Venture 50, ranking as one of the top Canadian companies across all sectors.

Jennifer McCarron has done a fabulous job leading the company as CEO and president.

Sadly, I’ll be stepping down from the board of Thunderbird, but it’s for a good reason. The remarkable expansion in U.S. Global ETFs, as well as the rapid growth of HIVE Blockchain Technologies, has meant that I have less and less time to give Thunderbird the attention it deserves. But again, with Jennifer in the driver’s seat, I have no worries about the company’s future. Onward!

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-23 | Eurozone CPI Core YoY | 1.4% | 1.4% | 1.4% |

| Feb-23 | Conf. Board Consumer Confidence | 90.0 | 91.3 | 88.9 |

| Feb-24 | New Homes Sales | 856k | 923k | 885k |

| Feb-25 | Hong Kong Exports YoY | 30.5% | 44.0% | 11.7% |

| Feb-25 | Durable Goods Orders | 1.1% | 3.4% | 1.2% |

| Feb-25 | Initial Jobless Claims | 825k | 730k | 841k |

| Feb-25 | GDP Annualized QoQ | 4.2% | 4.1% | 4.0% |

| Feb-28 | Caixin China PMI Mfg | 51.4 | -- | 51.5 |

| Mar-1 | Germany CPI YoY | 1.2% | -- | 1.0% |

| Mar-1 | ISM Manufacturing | 58.6 | -- | 58.7 |

| Mar-2 | Eurozone CPI Core YoY | 1.1% | -- | 1.4% |

| Mar-3 | ADP Employment Change | 168k | -- | 174k |

| Mar-4 | Initial Jobless Claims | 798k | -- | 730k |

| Mar-4 | Durable Goods Orders | -- | -- | 3.4% |

| Mar-5 | Change in Nonfarm Payrolls | 145k | -- | 49k |

Gold Market

Strengths

- The best performing precious metal for the week was palladium, but still down 2.51%. Palladium was buoyed by the partially suspended operations at Russia’s Nornickel mine due to flooding. AngloGold Ashanti boosted its dividend more than fivefold to 48 cents, up from 9 cents in 2019 after profit climbed to $953 million in 2020. The move follows similar dividend increases from rivals Barrick Gold and Newmont.

- Gold Fields said regulators approved its plan to build a 40-megawatt solar plant at its South Deep mine in South Africa, reports Bloomberg. The new plant will supply 20% of the mine’s electricity needs and help limit operational losses from power outages.

- African Gold Acquisition Corp, a special purpose acquisition company (SPAC) targeting gold assets in Africa, raised more than $360 million ahead of its New York listing. Bloomberg reports the offer was set to raise $300 million and saw stock sold at $10 a share. Founder and chairman Rob Hersov says potential acquisitions will be in “well-trodden mining countries, so no surprises. And we will likely buy a mining company and possibly add others thereafter.”

Weaknesses

- The worst performing precious metal for the week was platinum, down 6.93%, perhaps on the production expansion plans announced by Anglo American Platinum. Gold had a second weekly drop as 10-year Treasury yields rose to the highest in a year on Tuesday. Spot gold fell 1.9% to $1,770 an ounce on Wednesday and was down as much as 4% for the month. “The broad-based rally on the commodities markets is continuing to bypass gold completely,” Commerzbank AG analyst Carsten Fritsch said in a note.

- Platinum continued its decline, falling from a six-year high reached earlier this month. Bloomberg reports the metal fell 3.7% on Tuesday to $1,228 an ounce along with other base metals as investors reassess the demand outlook.

- Goldman Sachs lowered its gold price forecast to $2,000 an ounce, down from $2,300, after a rocky start to the year. Analysts wrote in a note: “We think the strong rotation into risky assets on the back of repricing of global growth has been the main reason behind gold’s underperformance.”

Opportunities

- De Beers, the world’s largest diamond producer, raised prices by 4% at its second sale of this year, marking a third straight sale with higher prices. Strong holiday sales in the U.S. and positive signs from Chinese New Year have seen buyers rush to replenish their stocks of rough stones, reports Bloomberg. De Beers, an Anglo American Plc business, made massive discounts last year as the pandemic hit demand.

- Anglo American Platinum Ltd plans to boost production of platinum-group metals 20% to 3.6 million ounces by 2030 through ramping up South African operations. Chief Executive Officer Natascha Viljoen expects prices to remain robust in 2021, even as the platinum market will likely turn to a surplus. “If you consider the momentum in battery electric vehicles and fuel cells, we believe the future lies in a mixed drive train where platinum certainly plays a significant role.”

- Harmony Gold Mining, South Africa’s top producer, is considering digging further at the Mponeng mine, already the world’s deepest mine at 2.5 miles underground. CEO Peter Steenkamp says ore reserves below the current level are “massive” and the company is looking at ways to find the investment needed to keep extracting. Harmony purchased the legendary and aging Mponeng mine from AngloGold Ashanti last year.

Threats

- Citigroup says gold is losing luster to cryptocurrencies in a new report, which compares net outflows from gold-backed ETFs to the increase in outstanding shares for the Grayscale Bitcoin Trust. “While a few months does not imply a structural trend, it appears rotational flow impacts are favoring cryptocurrencies to the detriment of gold this year,” analyst Aakash Doshi writes. The bank cut its six-to-12-month price target for gold by $150 an ounce to $1,950.

- Fed Chairman Jerome Powell spoke on Tuesday and signaled the central bank will continue to support the economy and is nowhere close to unwinding its easy policy. “Gold is still in the danger zone since Powell did not deliver a response to the recent surge in yields,” said Edward Moya, a senior market analyst at Oanda Corp. “Treasury yields can probably go a lot higher before the fed will step in, and that could derail gold’s outlook in the short term.” Higher yields hurt gold’s appeal since it does not pay interest.

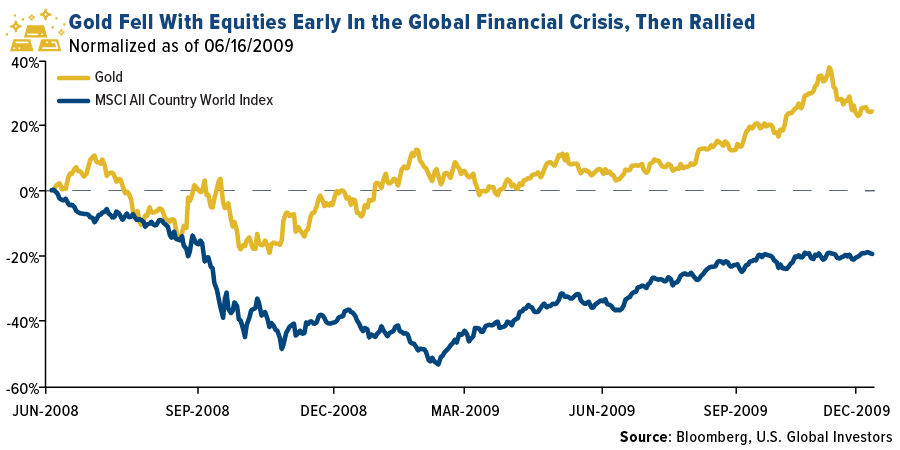

- Bloomberg’s Jake Lloyd-Smith says shrinking holdings in gold-backed ETFs are a bad omen for bullion prices as outflows have remained steady since peaking in September. “Bullion faces stiff headwinds this half, with Treasury yields pushing higher amid investor optimism about the pandemic’s endgame and the dollar off its lows.” The analyst thinks investors might be taking the opportunity to exit gold positions during a time of relative strength. Another Bloomberg analyst, Eddie van der Walt, says “it’s always worrying to see gold sell off along with risk assets.” He also points out that bullion is usually among the first to rebound in episodes of acute market volatility, as seen in the chart below from 2008.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.78%. The S&P 500 Stock Index fell 2.45%, while the Nasdaq Composite fell 4.92%. The Russell 2000 small capitalization index lost 2.90% this week.

- The Hang Seng Composite lost 7.37% this week; while Taiwan was down 2.37% and the KOSPI fell 3.05%.

- The 10-year Treasury bond yield rose 6 basis points to 1.405%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Fantom, rising 206.92%. Coinbase filed to go public via direct listing and finally investors got a glimpse of its financial results. Retail customers accounted for only 36% of trading volume during the fourth quarter of 2020, down from 80% in early 2018. This shows the shift of bulk volume coming from institutional customers. In the fourth quarter of 2019, Coinbase reported $5 billion in retail trading volume compared to $9 billion in institutional volume. These figures blew up to $32 billion in retail volume and $57 billion from institutional clients during fourth quarter of 2020, marking a 540% and 533% increase in each, respectively.

- Singapore is using blockchain technology to develop a global standard for verifying Covid-19 test results to speed up clearing local and foreign immigration checkpoints.

- Bitcoin has outperformed the MSCI global equity index this past year, as seen in the chart below, showcasing its strength as an investment vehicle during a time when inflation expectations are on the rise.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Horizen, down 35.59%. Bitcoin hit its lowest level since February 11 this week when the price dropped to $44,000. Bitcoin is down nearly 20% for the week and if the losses are held through Sunday, the resulting weekly drop would be the biggest since the second week of March 2020, when prices tumbled by 33%. With the meteoric rise in the cryptocurrency, the asset does seem overheated and was due for a correction.

- The Grayscale Bitcoin Trust (GBTC) plunged 22% this week, outpacing the 17% decline in Bitcoin, evaporating the trust’s massive premium it held and is now trading at 3.8% below the value of its underlying holdings. With Bitcoin declining, there is a supply and demand imbalance for the trust’s shares, resulting in the discounted value that it is trading at.

- A Serbian man has been charged with embezzling $7 million from U.S. investors through two fraudulent cryptocurrency platforms. He founded “Start Options” and “B2G”, which claimed to be a cryptocurrency mining and trading service and an “ecosystem” for exchange of B2G tokens, respectively. The money invested by users was laundered through a Philippines-based account and digital currency wallet.

Opportunities

- Analysts at JPMorgan are suggesting that a one percent portfolio allocation in Bitcoin will serve as a hedge against fluctuations in traditional asset classes. This endorsement comes on the back of major investments in Bitcoin by Tesla and MicroStrategy. The analysts do stress that crypto assets should be treated only as investment vehicles and not funding currencies like the USD.

- Canada’s CI Global Asset Management filed a preliminary prospectus for the world’s first Ethereum exchange-traded fund (ETF). The firm said its proposed “CI Galaxy Ethereum ETF” would be the first ETF to invest directly in ether, the native cryptocurrency of the Ethereum network. The ETF, under the proposed ticker ETHX, will invest in ether with its holdings priced using the Bloomberg Galaxy Ethereum Index.

- Wyoming has introduced a bill for the implementation of a system for company filings that uses blockchain technology. Under the act, the system would be used by companies for reports, data and other information required by law. The filing system will provide necessary security standards through authenticated digital identities. Wyoming has been working to market itself as a blockchain and crypto-friendly state in a bid to attract companies.

Threats

- The European Central Bank (ECB) is seeking the power to veto launches of any stablecoins in the eurozone. The ECB believes that it should have the final say ahead of any proposed stablecoin launches, such as the Facebook-backed diem. ECB stated that stablecoin issuers must meet rigorous liquidity requirements on cash reserves similar to money market funds.

- The Reserve Bank of India (RBI) stated “major concerns” about cryptocurrencies as the Indian government is contemplating an outright ban on the use of such assets, except for an official digital rupee. RBI’s governor acknowledged the benefits of using blockchain technology but remains worried about the risk “private” cryptocurrencies pose to financial stability.

- The House Financial Services Committee’s subcommittee on National Security, International Development and Monetary Policy held its hearing on domestic terror financing this week. While the focus was not on cryptocurrencies or decentralized tools, the hearing did feature issues of recent concern that such tools are being increasingly used by far-right extremists, especially after they were expelled from more centralized social media and financial technology platforms. The proposed bills to counter these activities are aimed at boosting the powers of the Financial Crimes Enforcement Network (FinCEN), allowing them to freeze the financial assets of any individuals arrested on rebellion or insurrection charges and provide classified information to employees of private financial institutions.

Domestic Economy and Equities

Strengths

- The jobs market appears to be returning to growth, with new applications for unemployment benefits falling to the lowest level since November amid other signs hiring is picking up. Initial weekly unemployment claims decreased by 111,000 to a seasonally adjusted 730,000 last week, the Labor Department said Thursday. It was also the biggest drop in new applications for regular state programs since last summer.

- The Conference Board Consumer Confidence Index went up to 91.3 in February from a revised 88.9 level in January. The monthly survey measures how people feel about current and future economic conditions. The Present Situation Index, which went up to 92.0 from January’s 85.5, measures how people feel about the economy right now. The Expectations Index declined a bit, dropping to 90.8, from last month’s 91.2. The index gauges how people feel about income, business, and labor market conditions in the short term.

- Royal Caribbean Cruises Ltd was the best performing S&P 500 stock for the week, increasing 18.26%. Cruise stocks have been making a broad rally this week, primarily on hopes of reopening as news around COVID-19 becomes more optimistic.

Weaknesses

- January marked the fifth straight month that the National Association of Realtors (NAR) has reported a decline in its Pending Home Sales Index (PHSI). The index, based on newly signed contracts for the purchase of existing homes, was down 2.8 percent from its December level.

- CDC Director Rochelle Walensky issued a sobering warning during a press briefing Friday, where she said the more contagious B.1.1.7 variant, first found in the U.K., now accounts for an estimated 10% of current U.S. cases, and that variants in California and New York also appear to spread more easily.

- Viatris Inc Inc was the worst performing S&P 500 stock for the week, decreasing 18.45%. The company release of financial guidance for its fiscal year 2021 disappointed investors as it expects to record revenue between $17.2 billion and $17.8 billion, well below the consensus analyst estimate of $18.46 billion.

Opportunities

- Morgan Stanley turned bullish on Carvana and nearly doubled its price target to a Street-high view of $420 from $225. “Carvana is uniquely positioned to serve an automotive and transportation [total addressable market] that goes far beyond the used car market.” This could potentially drive far higher growth than is now reflected in the valuation. The firm anticipates higher market share and margins in the company’s used car business.

- Restaurant-software provider Toast is preparing an IPO that could value it at around $20 billion. The Boston-based company could also consider a sale or a merger with a blank-check company, the WSJ said.

- Lime, a Silicon Valley scooter startup, is in early discussions about going public via a SPAC. The Uber-backed electric scooter startup is working with investment bank Evercore as it explores going public via a blank-check company, two sources told Insider.

Threats

- CFRA downgraded shares of Nikola to a "sell" on Thursday and lowered the price target to $12 per share after the electric-vehicle maker reported earnings. Senior analyst Garrett Nelson cited "supplier issues" and potential "legal risks" as the main reasons for the downgrade.

- Michael Burry expects the economy's reopening and more stimulus to fuel inflation. "The Big Short" investor warned governments might 'squash' bitcoin and gold to protect their currencies. Burry highlighted Germany's hyperflation in the 1920s as a cautionary tale for the U.S.

- HSBC's profits plunged 45% as low interest rates and bad loans took a toll. The bank earned $12.8 billion in Asia, but lost $4.2 billion in Europe.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was coffee, up 6.47% on severe supply shortages out of Brazil. Copper, up 5.65% the last 5 trading sessions, extended its rally and moved closer to the record high set a decade ago, trading at $9614.50 on the London Metal Exchange (LME). Investors are piling into metals with the expectation that rebounding economies will further tighten supplies. Meanwhile, aluminum is trading at a two-year high of $2,223 a ton.

- Commodities hit their highest levels in almost eight years on the bullish bet that government stimulus combined with near-zero interest rates will fuel demand, generate inflation and weaken the U.S. dollar as the economy rebounds from the pandemic. Bloomberg’s Commodity Spot Index, which tracks price movement of 23 raw materials, hit its highest level since March 2013. The index is up 60% since reaching a four-year low in March 2020.

- Oil rose to nearly $62 per barrel with predictions that the market’s rally could go further. Oil futures in New York gained 0.8% this Tuesday and are up 30% this year already. The market is heading towards what could be the tightest quarter since 2000. Socar Trading SA is predicting the global benchmark Brent will hit $80 a barrel this year as the glut of inventories built up during the pandemic is drained by the summer. Market expectations for oil are ultra-bullish due to the 200% rally after hitting an 18-year low during the pandemic. Option bets on oil prices rising above $100 have seen a rise, as open interest on the calls has gone from 500 to 3,950 in the past week.

Weaknesses

- The worst performing commodity for the week was natural gas, down 7.52% on weakness in demand after last weeks’ winter storm. Norilsk Nickel’s GDRs fell as much as 9.4% on Monday, most since June 2020, after a deadly accident on February 20. Investors are expecting that the accident may impact operations and undermine the company’s ESG reputation.

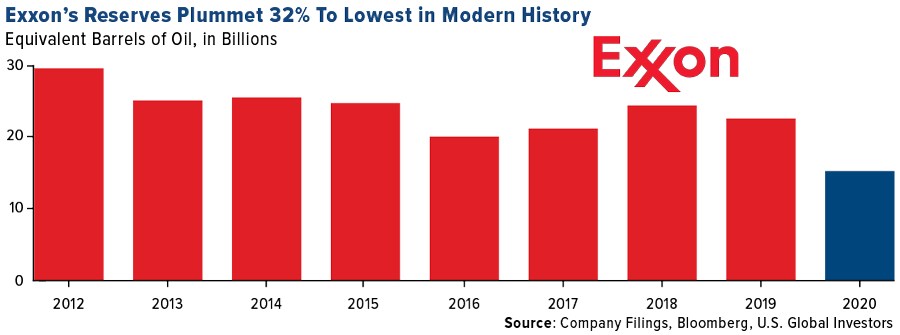

- Exxon Mobil’s worldwide oil and natural gas reserves declined by almost one-third to the lowest in the company’s modern history, following the pandemic-driven collapse in energy demand and prices. As of December 31, Exxon counted the equivalent of 15.2 billion barrels of reserves, down from 22.44 billion a year earlier. A majority of these downward revisions came from Exxon’s Canadian oil-sands developments and U.S. shale. This revision is a blow to Exxon’s future production potential and comes just weeks after the company posted its first annual loss in four decades.

- Petrobras shed $18.8 billion in market value following the news that Brazilian President Bolsonaro appointed a former army general as its new CEO, pending the board’s approval. A long list of analysts from different firms cut their ratings on the company’s shares citing risk of delays in the sale of its refineries, which will hinder its deleveraging plans. The sudden change in management might also reduce the company’s autonomy.

Opportunities

- Venture Global LNG Inc. could have the next major liquefied natural gas (LNG) export terminal in the U.S. when production begins in October. Venture Global’s momentum is coming at a time when U.S. developers are struggling to sign long-term offtake agreements as the Covid-19 pandemic has sputtered deal-making.

- Albemarle Corp., the world’s biggest lithium supplier, is planning on using almost all the proceeds from a $1.5 billion equity offering to expand its lithium capacity as the demand for batteries is expected to gather momentum throughout the decade. The company is planning on expanding operations in Chile and Australia and processing plants in China. As demand for green vehicles increases, Albemarle is positioning itself to meet those demands with an increase of 14% in its demand forecast by 2025.

- Anglo American Platinum Ltd. is targeting a 20% increase in production by 2030 as it mechanizes mines in South Africa. This development comes as investors debate the long-term supply and demand of the metals and the boost to platinum consumption from new hydrogen technologies against a shift to electric vehicles. For the short-term, platinum is up 19% this year as tougher pollution regulations require vehicle makers to use more platinum in catalytic convertors. The expansion is likely to cost around $1.5 billion.

Threats

- Texans will likely be paying for the state’s energy crisis that left millions without heat and electricity during last week’s winter storm for years to come. The cost of electricity sold from Monday till Friday of last week was $50.6 billion, compared to $4.2 billion a week prior to the storm. There are already reports of customers getting exposed to the wholesale prices and wracking up power bills as high as $8,000. CPS Energy, which is owned and run by the city of San Antonio, said that it is looking into ways to spread costs for last week over the next 10 years.

- After Texas’ energy crisis, there are concerns surrounding President Biden’s climate change plans and how the U.S. power grid might have to be reimagined to reach the goal of deriving all electricity from carbon-free sources by 2035. According to a Princeton University assistant professor, U.S. would have to expand its transmission grid by as much as 60% for wind and solar to make up half of U.S. electricity capacity by 2030. Grid improvements in the U.S. to accommodate a cleaner and carbon neutral future could cost as much as $90 billion by 2030 and the full price tag by 2050 could reach $690 billion, according to a 2019 study commissioned by WIRES.

- China’s oil stockpiles have risen to around 100 days worth of net imports, making it increasingly challenging to find extra storage tanks and facilities to hold supplies. The storage build-up is due to Beijing buying crude oil for its reserves last year when prices crashed due to the pandemic. There could be a downward pressure on the price of crude as Russia wants to increase production while Saudi Arabia is content with its current production. China, being the world’s largest importer, might have to slow down its oil imports due to reserves reaching storage capacity and leave crude’s rally in jeopardy.

Airline Sector

Strengths

- The best performing airline stock for the week was TUI AG, up 19.6%. S&P affirmed EasyJet’s BBB-/Negative credit rating despite the impact of the pandemic and the impact of the corresponding lockdown on the company’s operations. This has resulted in lower passenger demand and passenger confidence. The company is planning its first Eurobond ($1.5 billion) sale since 2019.

- IAG boosted the liquidity of British Airways (a key unit of the company) by $3.4 billion. It is also looking for other liquidity by drawing down an export development term loan and deferring pension contributions by $630 million.

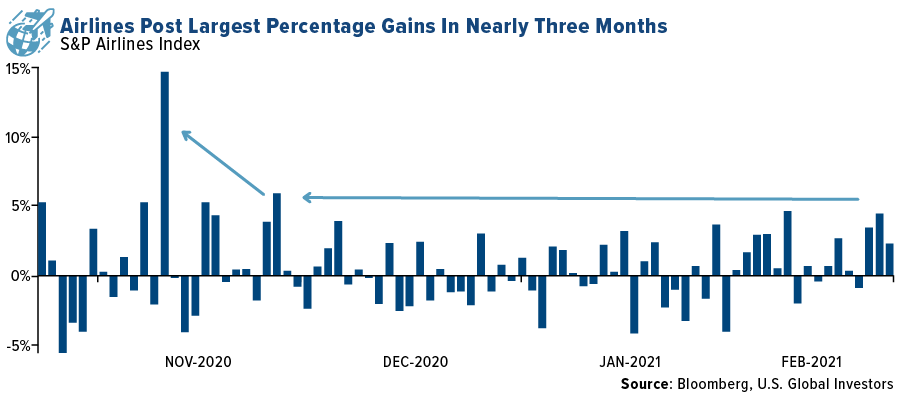

- Airline stocks are starting to rally. The S&P Airlines Index had its largest move in three months, and the index hit its highest level since early March. Vaccine hopes and analyst upgrades have also contributed to the rise.

Weaknesses

- The worst performing airline stock for the week was GOL, down 5.3%. Boeing recommended that airlines stop operation of its 777 model that uses the Pratt & Whitney engine. This is the aircraft model that was involved in the engine incident that forced a United Airlines aircraft that left Denver International back to the airport. Japanese regulators also forced the grounding of this aircraft within the country.

- Qantas pushed back the date for restarting international travel from June 2021 to October 2021. The company has reduced headcount by 8,500 and has grounded its fleet of A380s for three years. The company reported a loss of $1.0 billion Australian dollars in its most recently reported first half.

- Boris Johnson’s government issued a statement requiring that foreign travel for leisure holidays be banned until May 17. A review will be completed by the government by Easter, and a decision to extend this deadline will be made at that time. The economic impact is estimated at 10.5 billion pounds. Lockdown rules will be eased over the next four months.

Opportunities

- British Airways has offered to work with the U.K. government to restart travel in the country. One in10 jobs depends on travel and tourism, and this contributed 200 billion pounds to the economy.

- Airlines are expected to receive an additional $14 billion when the $1.6-1.9 trillion COVID relief bill is finally passed. The aid is expected to reduce the furloughing of employees, since capacity is still at 60% of year-ago levels.

- United Airlines was authorized by its Board to offer up to 37 million shares at market prices. The funds will help the company to weather the reduced travel (passengers at 40% of year-ago levels) that has occurred because of the COVID-19 pandemic.

Threats

- South Africa is worried about the potential failing of its national airline. A failure would have repercussions for the entire economy. The airline was grounded in March of last year, and $713MM has been earmarked by the government to get the airline flying again.

- Banks continue to see more risk in airline debt relative to the S&P. American Airlines, JetBlue and Korean Air Lines were rated the riskiest. Singapore Airlines was the most credit worthy.

- The financial impact of the United 777 plane engine incident may spill over into the debt markets. This plane has been difficult to offer as collateral, and the most recent incident may destroy its collateral value. In the past, investors wanted interest rates as high as 11% if the collateral was a 777.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was the Czech Republic, gaining 30 basis points. The best performing country in Asia this week was Indonesia, gaining 16 basis points.

- The Romanian leu was the best performing currency in emerging Europe this week, gaining 10 basis point.The Pakistani rupee was the best performing currency in Asia this week, gaining 84 basis points.

- The consumer confidence indicator in the euro-area was confirmed at -14.8 in February 2021, up from -15.5 in the previous month, due to an improvement in households’ assessments of their future financial conditions, their intentions to make major purchases, and especially, their expectations about the general economic situation.

Weaknesses

- The worst performing country in emerging Europe for the week was Turkey, losing 6.4%. The worst performing country in Asia this week was Hong Kong, losing 5.4%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 6.8%. The South Korean won was the worst performing currency in Asia, losing 2.6%.

- Mainland Chinese investors pulled their money out of the Hong Kong stock market for the first time in more than two months. The net selling amounted to HK$20 billion on Wednesday through the Stock Connect’s southbound links, according to Hong Kong stock exchange data.

Opportunities

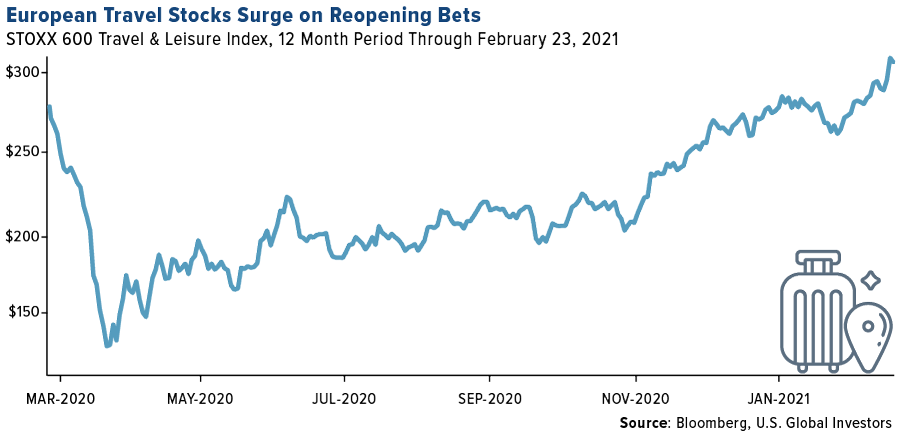

- European travel stocks moved higher on optimism about easing lockdown restrictions in the United Kingdom. All schools are planned to reopen March 8, followed by stores and outdoor hospitality from mid-April. A full restart of the economy is planned for June 21. Other countries are planning to remove some restrictive measures as well, as distribution of the COVID vaccine is picking up. Thailand, whose economy heavily depends on tourism, may remove its two-week quarantine requirement for vaccinated foreign visitors.

- Taiwan boosted its outlook for growth and exports. The exports will likely rise 9.58% this year versus 4.59% previously, while gross domestic product may hit 4.64% versus 3.83% previously, according to the statistics bureau. The increased demand for semiconductors was a key reason for the upgraded 2021 forecasts.

- Financial institutions in Russia may be granted easier access to funding if they improve their environmental, social and governance standards, Bloomberg reported. Russia has been slowly improving ESG standards and so far, most of the progress in developing sustainable finance has been driven by the nation’s biggest companies. The ESG rankings system is a step further to show that Russia is serious about joining the international shift toward green and more socially responsible investments.

Threats

- Taiwan is experiencing the worst drought in decades which may negatively affect the country’s semiconductor production. The global chip shortage may further increase as Taiwan’s government is preparing to further tighten water use in cities that are home to important manufacturers.

- Honk Kong announced tax increases on shares trading. It will become effective August 1 and it should bring extra HKD12 billion a year in revenue for the government. On Wednesday, Hong Kong equites recorded their first outflow since December 18 as mainland investors were net sellers. However, the inflows from the mainland will most likely return as equities trading in Hong Kong are less expensive than those listed in the mainland. Moreover, Hong Kong Stock Exchange is attracting a slew of new hot IPOs.

- The Czech Republic is preparing to impose stricter lockdown measures to prevent the collapse of its medical system. The country of 10.7 million reported 968 COVID-19 cases per 100,000 people over the two-week period ending February 18, seven times higher than that of neighboring Germany, according to the European Centre of Disease Prevention and Control. Prime Minister Andrej Babis blamed the Christmas reopening for the current spike in infections.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All