As the chorus of inflation concerns grows louder by the day, it’s important to take a step back and remember that inflation is not inherently bad. Inflation, nominal GDP, and corporate sales are all highly correlated. When prices rise gradually, it’s an indication of positive economic momentum. This important detail is often lost in the echo chamber of headlines that like to paint all inflation scenarios as nefarious.

Since the publication of our annual outlook, we have maintained the view that inflation is more of a “cyclical” phenomenon rather than a “structural” risk. Structurally “bad” inflation is defined by rapidly increasing input costs that cannot be passed on to consumers, a dynamic that helps feed a vicious feedback loop of higher unemployment and declining nominal GDP. In the U.S., this type of “stagflation” was last experienced in the 1970s, the decade most often cited in today’s media frenzy about potential inflation doomsday scenarios looming on the horizon. In the 1970s, geopolitical events caused a sudden and unexpected disruption to the supply of oil, which sent prices sharply higher in a short period of time. In an economy that was already facing high unemployment, corporations could not pass these higher prices to consumers, and inflation contributed to the overall economic malaise.

Compare the stagflation of the 1970s with today’s environment. Broadly speaking, inflation pressure has been muted. Of course, investors’ concerns about inflation are not backward looking. With the Biden administration’s $1.9 trillion stimulus package and ongoing vaccinations creating a bridge to a fully reopened economy, investors are viewing inflation through the lens of what’s to come. In most market commentary regarding inflation fears, the logic goes something like this. Consumers, flush with inflated bank accounts from stimulus checks will unleash a purchasing frenzy that will lead to higher prices, i.e. inflation. But remember, even if this plays out, it’s not inherently bad. In this scenario, consumer demand would create higher inflation, which should lead to higher corporate sales growth and be a net benefit for the economy.

Others have pointed to the recent rise in some input costs as an omen for “stagflation” ahead. However, here again, consumer demand has been more than enough to offset rising input costs. Homebuilders are a great example of an industry that is prospering despite strong input cost inflation. Lumber prices have surged, yet homebuilder margins are expanding because of strong home sale pricing power and robust consumer demand.

The example of homebuilders reinforces the important “K-shaped” dynamic of the economic recovery. It has been our view since last year that the pandemic led to a “two-speed” recovery that created winners and losers with broad strokes across the economy. As this relates to inflation, there will certainly be companies that are unable to pass through higher input costs to consumers. However, these companies will be contained to certain pockets of the economy and broadly speaking there will be more “winners” than “losers” from a corporate perspective.

As we signaled in our 2021 outlook, spreads across sectors are approaching levels that are uncomfortably tight. In this type of narrow spread environment, what you avoid is just as important as what you invest in. The same is true for the risks you seek to hedge. Given our current view of inflation, we believe TIPS are overvalued and that higher inflation is appropriately priced in to the TIPS market. While inflation is a risk we will continue to monitor, we have avoided TIPS thus far based on our outlook. In the current market backdrop, many investors are choosing to hedge against rising inflation. In our view, this hedge is premature and may ultimately prove to be futile.

Bond Market Outlook

Global Rates: policy rates stay low, further curve steepness limited in near term

Global Currencies: U.S. dollar trends weaker against DM, EM currencies

Investment Grade: spreads were flat in January, as tighter levels curbed some enthusiasm, but the macro, technical and fundamental story remained intact

High Yield: following a strong close to 2020, the market began the new year choppy and in search of direction, even as another monthly new issuance volume was set

Securitized: massive monetary and fiscal support, both current and expected, as well as vaccine rollout optimism, position the consumer and housing markets well heading into the new year

Emerging Markets: the recovery supported by strong manufacturing and exports continued, though its sustainability will depend on a rebound of employment, domestic consumption and investments

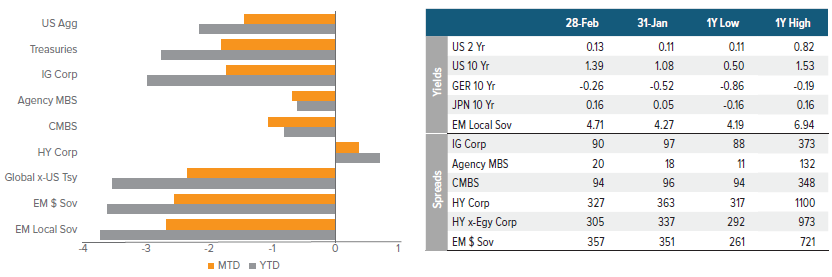

Rates, Spreads and Yields

Sector Outlooks

Global Rates and Currencies

After the sharp move higher during the last week of February, we expect Treasury yields to remain range bound in the near term. The yield curve will continue to gradually steepen through year end, likely with bouts of intermittent volatility amid strong growth expectations and inflation concerns. Markets seem to be wrestling with the idea of peak central bank intervention receding, at least in terms of tangible action, and are now trying to determine which among the vaccine roll out, U.S. fiscal stimulus, or better economic and corporate data, will be the next main catalyst driving sentiment and activity. While the Bank of Japan is reviewing the Japanese Government Bond 10-year band and is thinking of beginning to taper in April, the European Central Bank said it may not need to fully employ its Pandemic Emergency Purchase Program (PEPP) and China has let SHIBOR rise above the three-year sovereign bond rate. Also, trade data has been improving and bodes well for global growth. However, if strong data does not materialize by March, markets may once again force Central Banks into dovishness.

In Europe, the main surprise has been on inflation: The January flash HICP country prints have so far surprised to the upside; prior to the country releases, consensus expectations were for euro-area January HICP of 0.54%, year-over-year. Given the country prints, it seems reasonable to expect 0.75%, year-overyear. Also, vaccine rollout has been very disappointing and puts downside risk to the growth.

Investment Grade (IG) Corporates

IG spreads were flat in January as tighter levels curbed some enthusiasm, but the macro, technical and fundamental story remained intact. The move higher in interest rates to start the year led to a slight risk off sentiment, but as rates settled at the new higher level, yield-based buyers stepped in to support spreads. Despite the negative total return for IG during the month, inflows continued, led mostly by BBgBarc U.S. Aggregate Bond Index-based funds. Supply was in line with expectations at $123 billion, but lower 30-year new issuance helped support some modest credit curve flattening. We continue to expect spreads to move sideways to start the year and see overall levels as less attractive at this point.

High Yield Corporates

Following a strong close to 2020, the market began the new year choppy and in search of direction. Triple-C rated issues had a strong January, benefiting from carryover from the fourth quarter’s risk-on appetite. Higher rated issues showed signs of sluggishness as the month bore on, mostly due to interest rate sensitivity and downward price pressure from a particularly heavy new issuance calendar. Indeed, January notched yet another monthly new issuance volume record. Elsewhere, credit ratings have mostly stabilized and defaults are still trickling through, but we do not think a new wave currently on the horizon.

Securitized Assets

Following a strong closing to 2020, Agency MBS continued to outperform comparable Treasuries in January, driven by a strong technical environment in the higher coupons. Lower coupons were overwhelmed with heavy originations, despite heavy Fed buying, while the higher coupons were well bid by money managers and banks in response to the rate sell off. For 2021, net supply is projected to be between $400-500 billion, due to an increase in home sales and cash-out activity driven by the low rate environment, which will likely offset the headwinds of high unemployment and economic uncertainty. The Fed will remain the largest source of demand for the foreseeable future, and with an uncertain economy and a "blue-heavy" political environment, the chance of a near-term taper event is low.

We maintain our positive tactical outlook for mortgage credit, as low mortgage rates, a robust housing market, and overall solid consumer credit worthiness foster sponsorship. Layering in monetary policy and the most recent fiscal stimulus package, mortgage credit is well supported fundamentally even if progress in trimming unemployment continues to be slow.

Building from a strong December, CMBS is poised to continue its spread recovery. A busy, but manageable new-issuance calendar and reflationary impulses from monetary and fiscal policy - as well optimism from the vaccine roll-out - are extremely supportive of CRE fundamentals. Ultimately, markets are likely translate these factors into broader and deeper demand for CMBS risk. Near term, off the back of the year-end surge in COVID cases, which led to more shutdowns in broader areas, risks scarring from a fundamental standpoint, so caution from a security selection point of view remains warranted.

Non-benchmark ABS is likely to continue to perform well, as the consumer oriented sub-sectors will further attract sponsorship due to strong fundamentals, solid technicals and relative value. We maintain our assessment as positive and increase our conviction. The fiscally improved profile of the US consumer coupled with ABS structural dynamics were already believed to provide the sector with solid footing to withstand this sustained period of elevated, albeit improving, unemployment. Indeed, Recently enacted stimulus is acting as a fortifying bridge to the end of the pandemic.

Emerging Market (EM) Debt

The EM economic recovery has been supported by strong manufacturing output, new orders, exports (excluding China) and global trades volumes, even while services were stalling and global supply delays and delivery times rose in January. Uncertainties related to COVID are likely to prevail, and related precarity will remain a drag for consumption; COVID eradication and vaccine rollout schemes are likely to take more time and not fully reach the broader EM universe until 2H21. China’s marked slowdown contrasts with the rest of EM Asia, where factory growth kept accelerating. Growth in Africa and Central and Eastern Europe maintained momentum, while LatAm appears to be stalling. EM headline inflation was driven slightly higher by volatile food prices and an oil rally. Core inflation remains subdued overall as domestic demand is projected to lag well into 2021, which should allow central banks to remain supportive, despite the market pricing in some rate hikes. We expect QE to continue into 2021 and for Fiscal activity and strategy to remain under scrutiny as governments will weigh potential renewed support versus needed fiscal consolidation.

IM1545790

Past performance does not guarantee future results. This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management's current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

©2021 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169 • All rights reserved.

Read more commentaries by Voya Investment Management