"It's a slightly old-fashioned and perhaps also a somewhat bourgeois way of looking at it. I believe that we in Denmark can invest us out of the crisis we are in at present." Mette Frederiksen, Danish Prime Minister

You know society is in trouble when the Prime Minister of your country stands up and says something along the lines of “of course we can afford to take on more debt – you are old-fashioned if you think otherwise”. That is roughly what the Prime Minister of Denmark, Mette Frederiksen, said a few weeks ago, and that is the conclusion a classically trained economist like me came to when she uttered those words, but could she actually be on to something? Or is it just another case of a political leader in the Western world saying what many are thinking, i.e. that, if Japan can get away with all that government debt, why can’t we?

The issues at heart

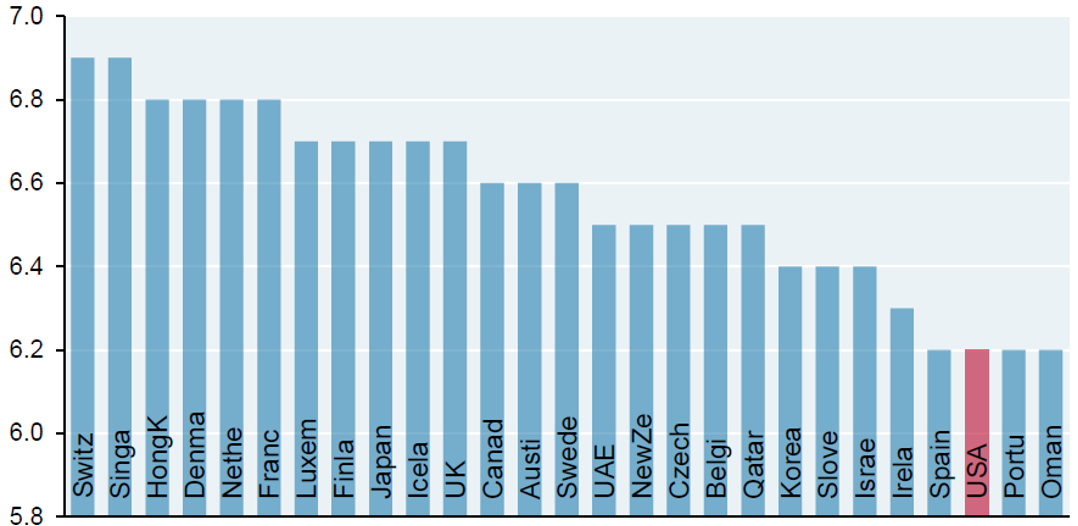

As we all know, the global infrastructure is far from perfect, although it is clearly more dilapidated in some countries than in others. A simple example is electricity grid reliability, which is one of the most important productivity agents in the modern world. Without a reliable electricity grid, there are many things we can’t do these days, such as working from home during a pandemic. I have referred to the poor US electricity grid before, and why it is to blame for many of the big US wildfires over the past few years but, as you can see in Exhibit 1, the USA is far from the only OECD country suffering from a sub-optimal electricity grid.

Exhibit 1: Electric grid reliability by OECD country (7=best) Source: JP Morgan Asset Management

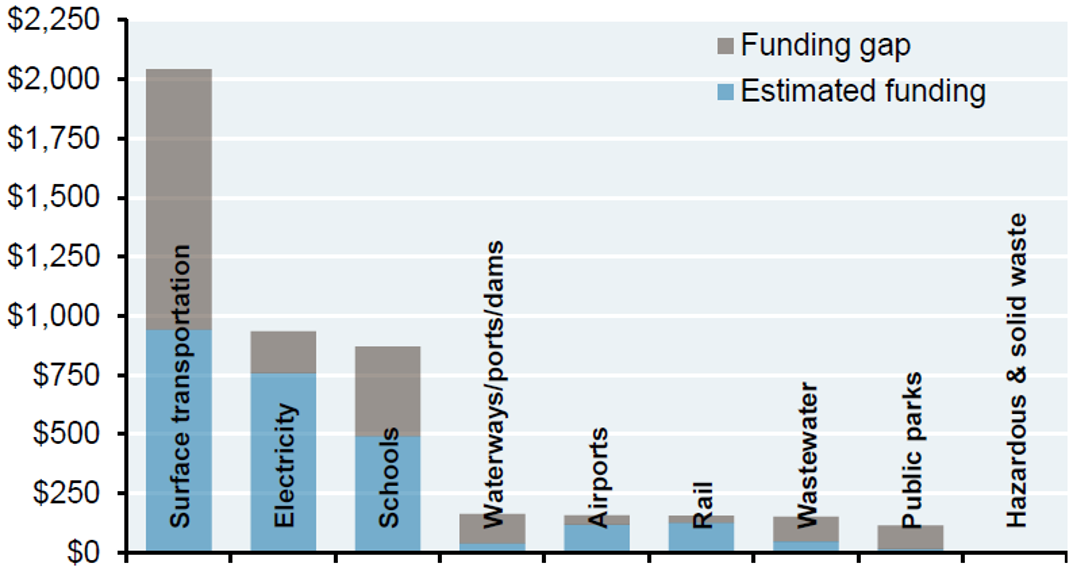

Investments in the electricity grid account for only a modest share of overall infrastructure spending, though. In the USA, it is about 20%, as you can see in Exhibit 2 below. By far the biggest item over there is the spending that goes towards the transportation infrastructure. As you can see, between roads, railroads and airports, transportation accounts for over half of total infrastructure spending in the USA. Unfortunately, I don’t have data from any other countries so wouldn’t know if those numbers are meaningfully different elsewhere.

Exhibit 2: US public infrastructure needs, 2016-2025 Source: JP Morgan Asset Management

You may have noted, as I immediately did, that spending on the digital infrastructure is not even included in Exhibit 2 and, as we have all learned over the past 12 months, having a robust digital infrastructure is critical these days. There may be one or two readers who will disagree with what I am about to say, and I should point out that I am biased, as I live in a town (only 30 miles from Trafalgar Square) where the digital infrastructure is rather poor. I feel quite strongly, though, that the pandemic should be a lesson to the political elite everywhere that the digital infrastructure is not yet good enough, although it is much better in some countries than in others with the UK firmly in the ”other” category.

The desperate need for upgrades

This could end up being a very long letter unless I limit myself. The list of things to modernise and improve in society is so worryingly long that a thorough review of the topic could turn this letter into a 50-page monster, and I shall save you from that. Let me instead give you a few examples – from the US and the UK respectively. The US first.

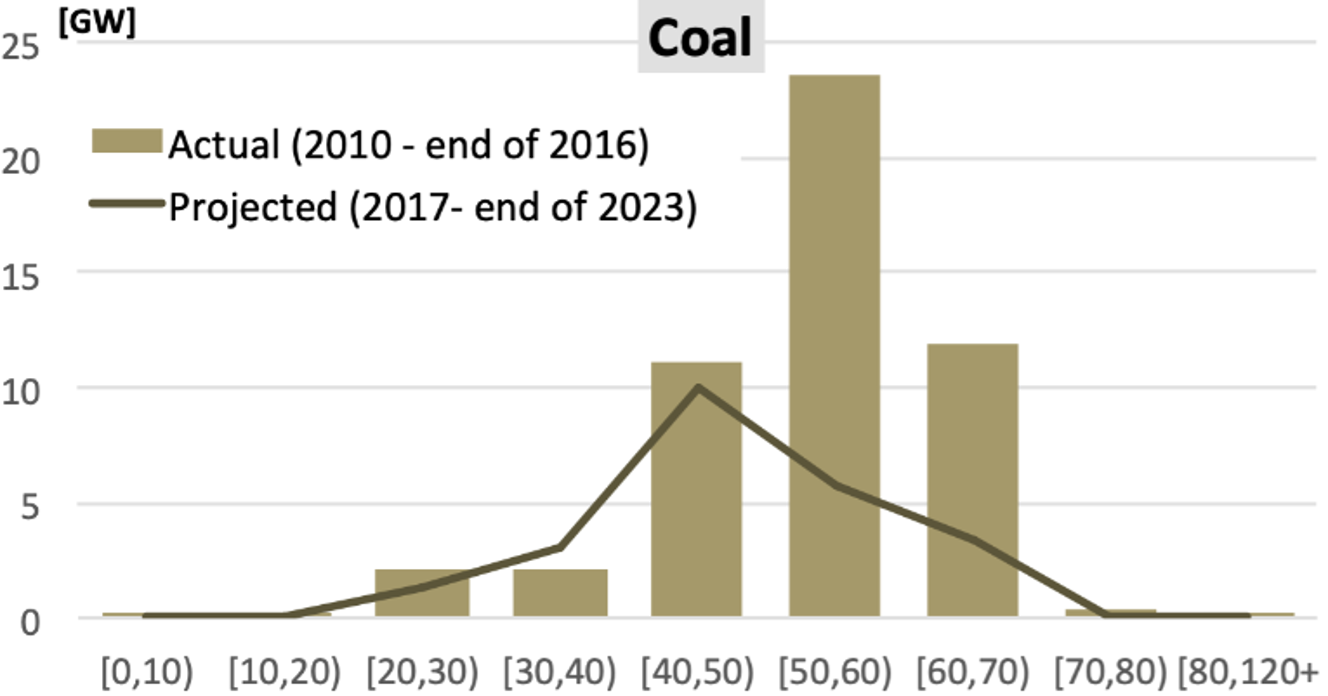

In 2019, no less than 62.6% of all US electricity generation was based on fossil fuels. That number was made up as follows – 23.4% from coal, 38.4% from natural gas and the rest (0.8%) from other fossil fuels, mostly oil (source: EIA). In the context of the ageing infrastructure, the number to focus on is the nearly one-quarter of total US electricity generation that comes from coal-fired power plants.

Exhibit 3: Age profile of US coal-fired power plants Source: Clean Technica.com

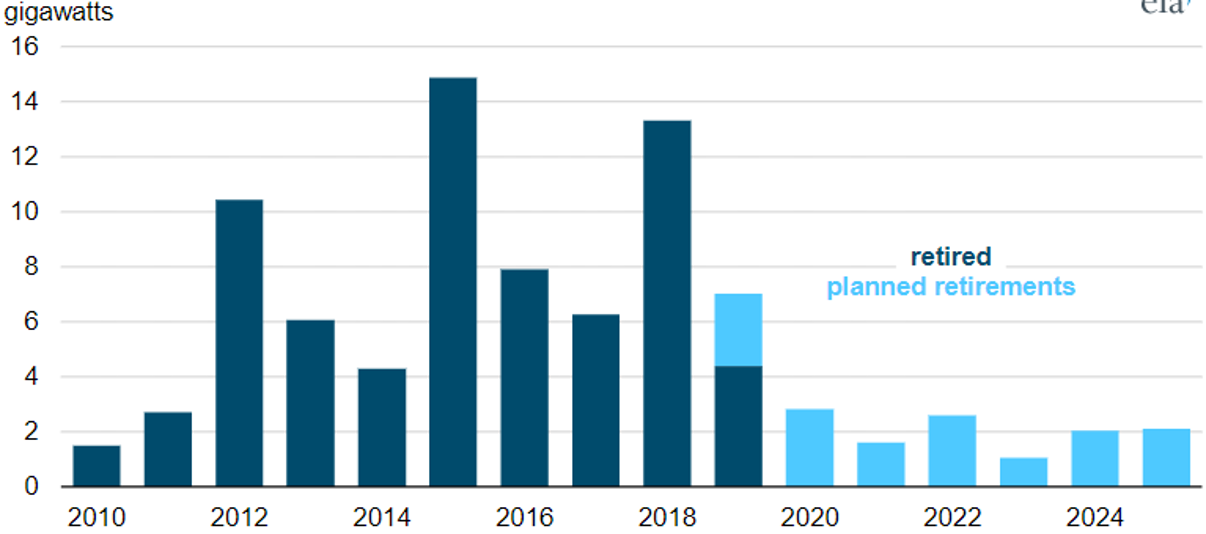

The problem facing US power plant owners is that the average coal-fired power plant is over 40 years old with a significant number of plants being over 50 years old (Exhibit 3) and increasingly uncompetitive when compared to power plants fuelled by natural gas or renewables. In 2018 alone, plant owners retired more than 13 GW of coal-fuelled generation capacity, which is the second-highest number of annual coal-fuelled power plant retirements ever (Exhibit 4).

Exhibit 4: Decommissioning plans for US coal-fired power plants Source: EIA

Not a single new coal-fuelled power plant has been built in the USA since 2011. That fact, combined with the tendency to run coal plants into the ground over there, means that, in 2050, the average coal-fuelled power plant will be over 70 years old. Assuming the cost of generating electricity from renewables will continue to fall, 30 years from now, virtually all coal plants will be uncompetitive. Many already are.

Although plain logic would suggest that, in an environment of declining profitability, coal plant owners will most likely accelerate the decommissioning programme, weak cash flows may prevent them from doing so. The retirement plans indicated in Exhibit 4 are therefore quite uncertain. As the cost of generating electricity from renewables continues to fall, that uncertainty can only get bigger.

The only silver lining, I suppose, is the fact that tomorrow’s nuclear technology (SMR) is both safe enough and nifty enough to fit into almost all decommissioned coal-fuelled power plant sites. You can therefore expect nuclear to move into the suburbs in the years to come, as they take over existing brownfield sites.

The list of other US infrastructure projects in need of improvement is not exactly short. Did you know, for example, that the USA has a fewer miles of high-speed rail lines than countries like Uzbekistan and Luxembourg? That no less than 40% of all bridges in the USA are more than 50 years old? That shoreline counties in the US account for two-thirds of all jobs and $3.4Tn in wages, and that a 2-metre rise in sea levels will put at least $1Tn of property and other structures at risk? The list of infrastructure challenges is uncomfortably long, but let’s switch our attention to the UK.

From an infrastructure point-of-view, the challenge facing Britain is that much of the existing infrastructure dates back to Victorian times, and there is little appetite in Britain to compromise with Victorian values. Take for example the rail network which faces zero competition from the rest of Europe in terms of offering poor services, particularly around London, where millions of people (used to) commute into town every morning.

As many of those commuter lines use an outdated infrastructure built in Victorian times – for example old Victorian bridges – and that you will probably go to jail for the rest of your life for treason if you suggest modernising those bridges, the UK is now the only country in Europe of a reasonable size without double-decker trains (they can’t get under the bridges). The net result? An embarrassingly poor rail network in a country of otherwise high living standards. With the onslaught of COVID-19, commuters have refused to stand on the toes of each other, leading many Brits to work from home for the past year. This again has resulted in a painful 9.9% loss of UK GDP in 2020 – far higher than most other countries. (In all fairness, I should point out that another reason so many Brits have chosen to work from home over the last 12 months is the high proportion of service sector jobs in the UK when compared to other European countries.)

On a more positive note, Thames Water (which runs London’s water system) is in the process of upgrading the old, Victorian, sewage system. Until about 1850, London’s growing volume of sewage was led straight into the River Thames. At the time, the river transported hundreds of tons of raw sewage every day and, as a result, was virtually dead. Then, in 1858, Westminster decided to build a sewage system which (sort of) works to this day. A new waste-water system is now under construction at the cost of £4.2Bn. From 2023, it is expected to carry raw sewage from 34 of London’s largest sewage overflows along a 25 km long tunnel to a new facility at Lee Tunnel.

Quite sadly, though, this is one of only a handful of successful, large-scale infrastructure projects in a country that desperately needs to put the Victorian times behind it once and for all. That will come at a massive cost, though, at a time where the country is limping heavily from a combination of COVID-19 aches and Brexit blues.

Why do we invest so little when so much is needed?

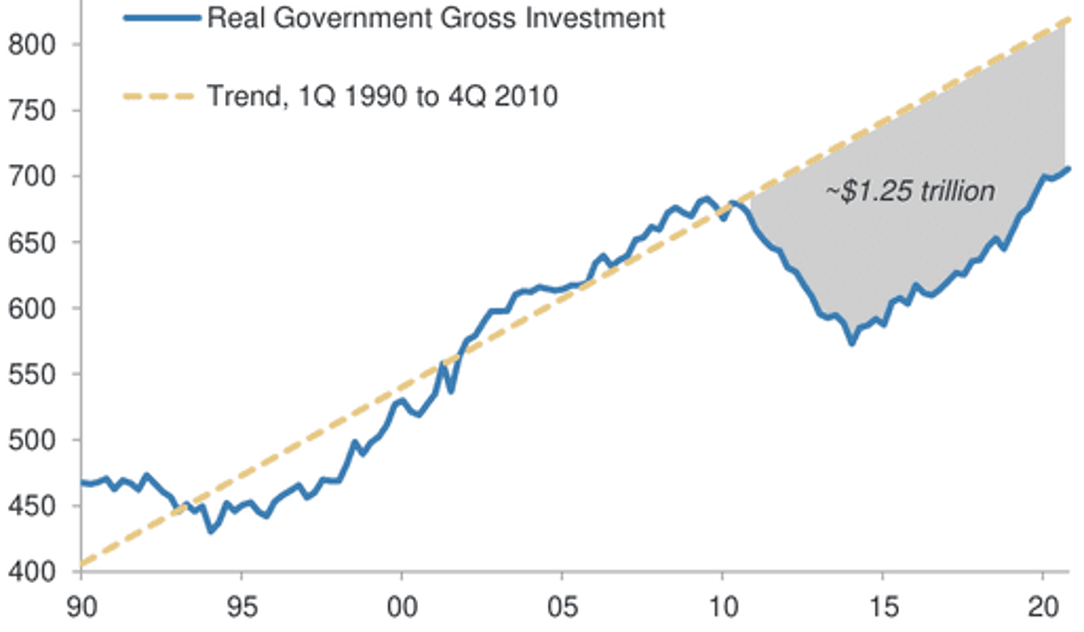

It should be clear by now that an ageing infrastructure in both the US and the UK (and elsewhere, I might add) shall require massive investments. That said, precisely the opposite is happening. Less and less capital is spent on investments, both in the public and the private sectors. In Exhibit 5 below, you can see how the US government has dramatically underinvested since the Global Financial Crisis (GFC) in 2008.

Exhibit 5: Real US government gross investments ($Bn in 2009$) Sources: Morgan Stanley Research

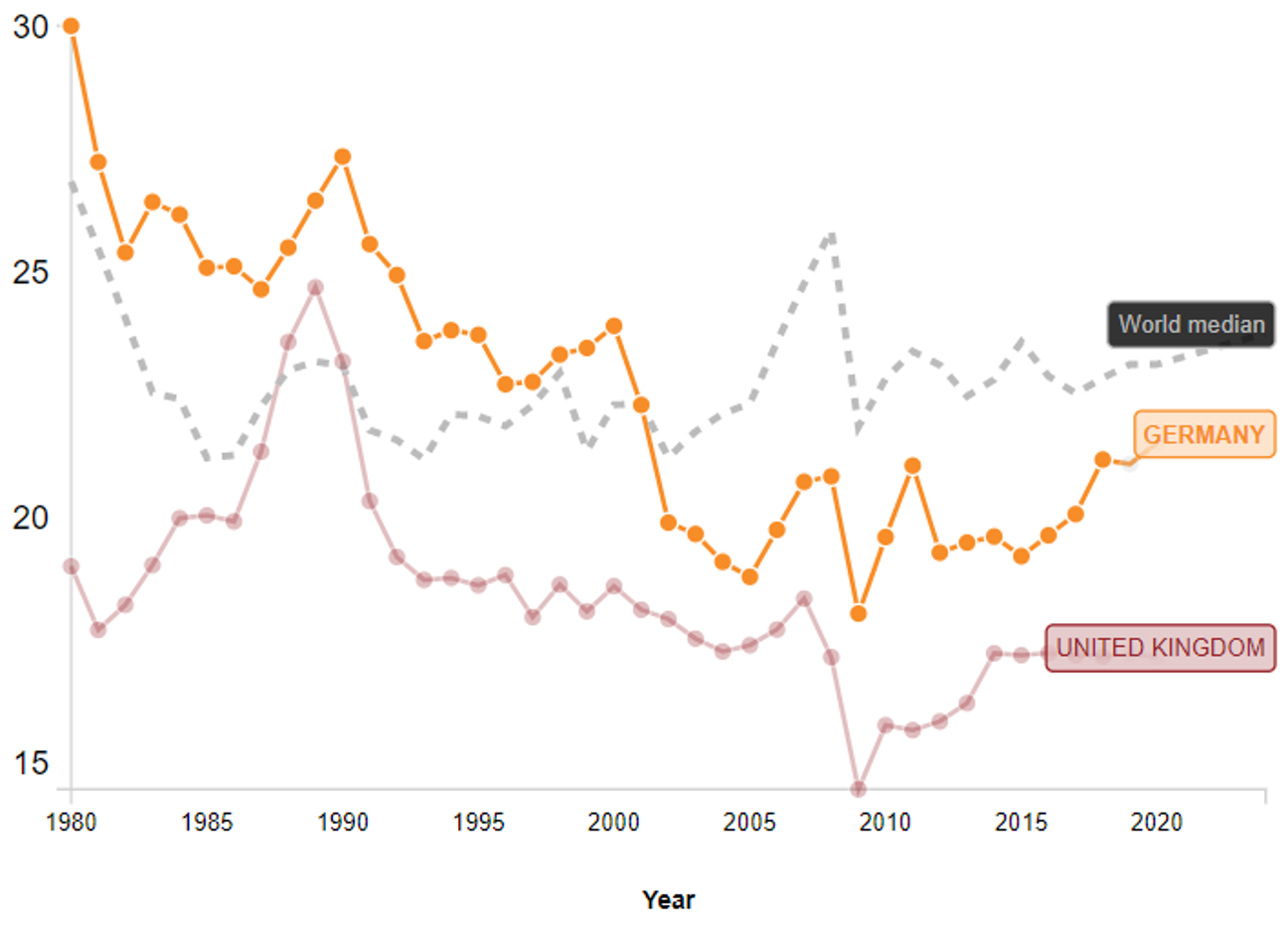

Likewise in Europe. As you can see in Exhibit 6 below, investments in both Germany and the UK (and elsewhere I might add) are trending down. Although the data in Exhibit 6 includes both private and public investments, i.e. it can be difficult to establish if it is one or the other causing total investments to soften, I can tell you that both public and private investments in Europe are down from yesteryear’s levels.

Exhibit 6: Total investments, % of GDP Sources: WorldBank.org

This raises the question – why? If it is so obvious that most countries need to update an outdated infrastructure, and that we could do with some job creation, why is it not happening? There are at least a couple of reasons for that. If you go back to Exhibit 5 for a moment, it is no coincidence that US government investments dropped like a stone post-2008. The GFC was a very expensive crisis to deal with. A fortune had to be spent to get the economy back on its feet again. Obviously, when you are forced to do that, you have to cut back on your spending elsewhere.

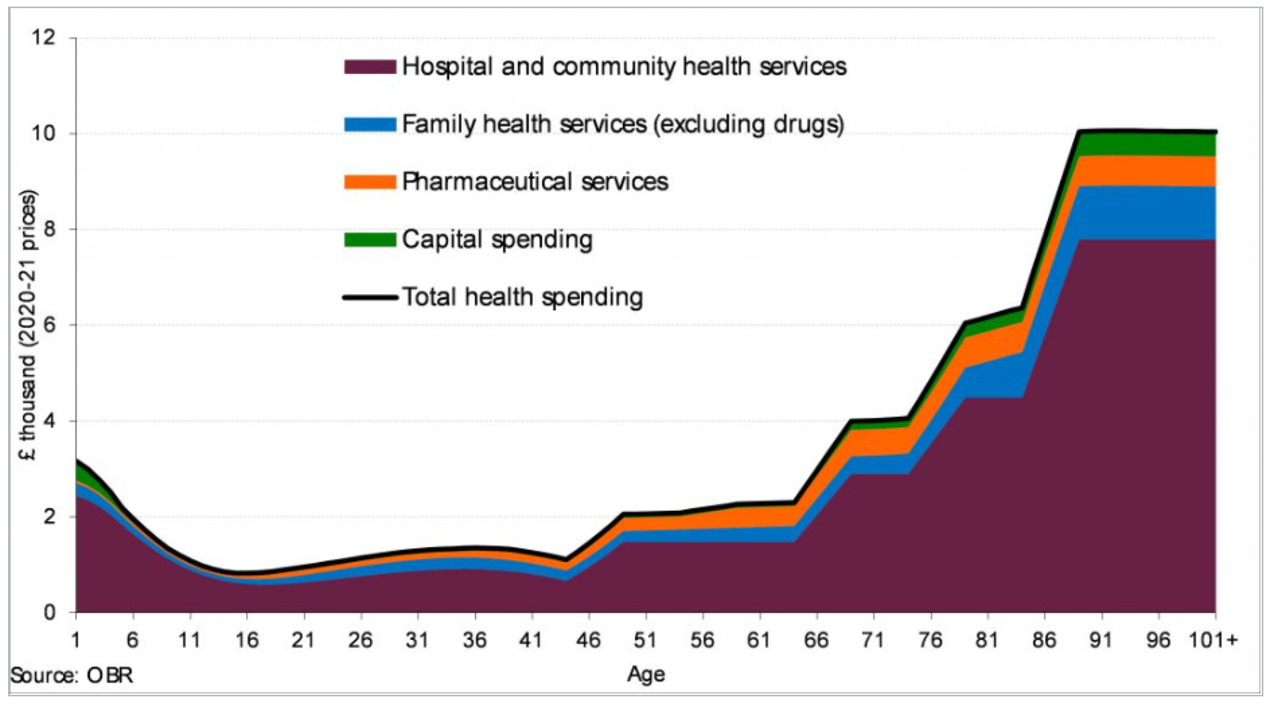

Secondly, ageing of society is confiscating more and more of public budgets. As you can see in Exhibit 7 below, a British man in his mid-80s is 6-7 more expensive to the NHS than someone in his mid-30s. With the number of British people aged 80 or older projected to almost double by 2030, the pressure on public budgets will continue to grow, and spending on the elderly will likely overwhelm other spending plans. Likewise in the US, and I should point out that the demographic profile in those two countries is far more benign than it is in most other OECD countries.

Exhibit 7: UK health spending per person in 2018 Sources: Gov.UK

The cost of rising interest rates

In the following, I will zoom in on the cost of borrowing in the UK. Having said that, if I had enough time, I am sure I could dig out a similar amount of ‘dirt’ on most other OECD countries, which would lead me to conclusions very similar to what is about to follow.

UK central government debt stood at £1,891.1Bn as at the end of December 2019 (85.4% of GDP), i.e. just before COVID-19 began to have an effect on public spending. A year later, as at the 31st December 2020, UK central government debt had risen to £2,131.7Bn or 99.4% of GDP (source: ons.gov.uk). The financial year in the UK doesn’t follow the calendar year, so be careful when comparing numbers, but the Chancellor of the Exchequer, Rishi Sunak, said recently that he expects UK government borrowings in fiscal 2020-21 (through March) to reach £350Bn, i.e. UK government debt will continue to rise.

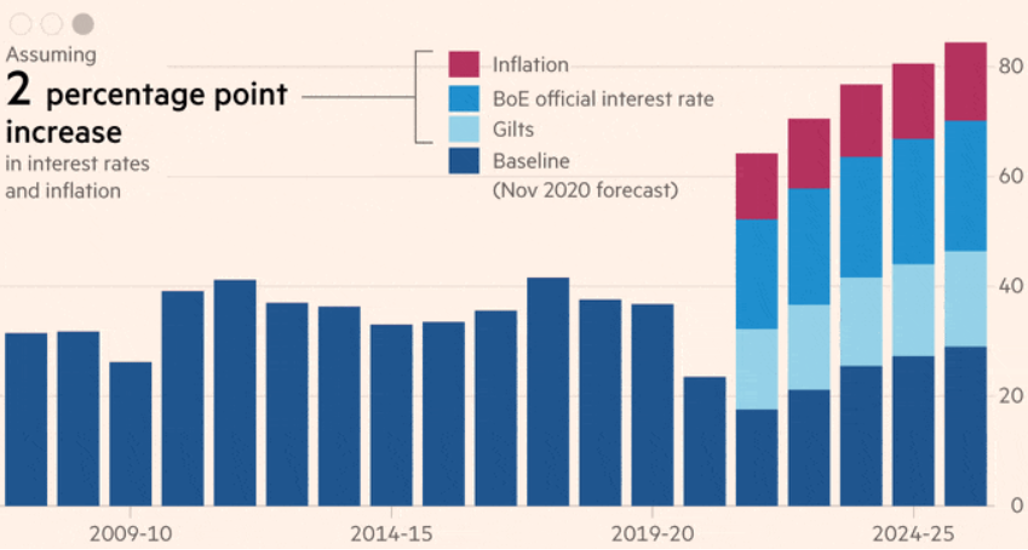

Should interest rates and inflation both rise by 2%, the net impact on borrowing costs to the UK government will be over £50Bn annually according to calculations conducted by the Financial Times (Exhibit 8) – and 2% is not as outlandish as it sounds, given the big rise in overall debt levels and the massive fiscal spending programme announced by Boris Johnson’s government more recently.

Due to QE and the fact that the Bank of England (BoE) has doubled its planned QE programme in 2021 to £895Bn, UK public finances are increasingly sensitive to interest rates – allow me to explain. As BoE buys gilts through its QE programme, interest on those bonds is recycled within the public sector and is no longer paid out. However, BoE still pays its official interest rate on the electronic money it creates to purchase the gilts – 0.1% at present – to the banks which hold these reserves. A rise in interest rates will therefore add to public spending, even if all the gilts are acquired by BoE.

Exhibit 8: UK central government debt interest (£Bn) Source: Financial Times

The bottom line is that the UK government is far more exposed to rising interest rates and rising inflation than generally perceived – the latter because a quarter of all the gilts that BoE plans to acquire in 2021 are linked to inflation. Tax rates are about to rise. Corporate tax rates, for example, will be increased from 19% to 25%, and the combination of higher corporate tax rates and higher income tax rates will leave Britain with its highest tax burden (35% of GDP) since the late 1960s (source: Financial Times). Therefore, you cannot assume that the money for the investment programme that is so desperately needed will necessarily be made available. It all depends on how interest rates and inflation behave in the months and years to come.

The link to the debt supercycle

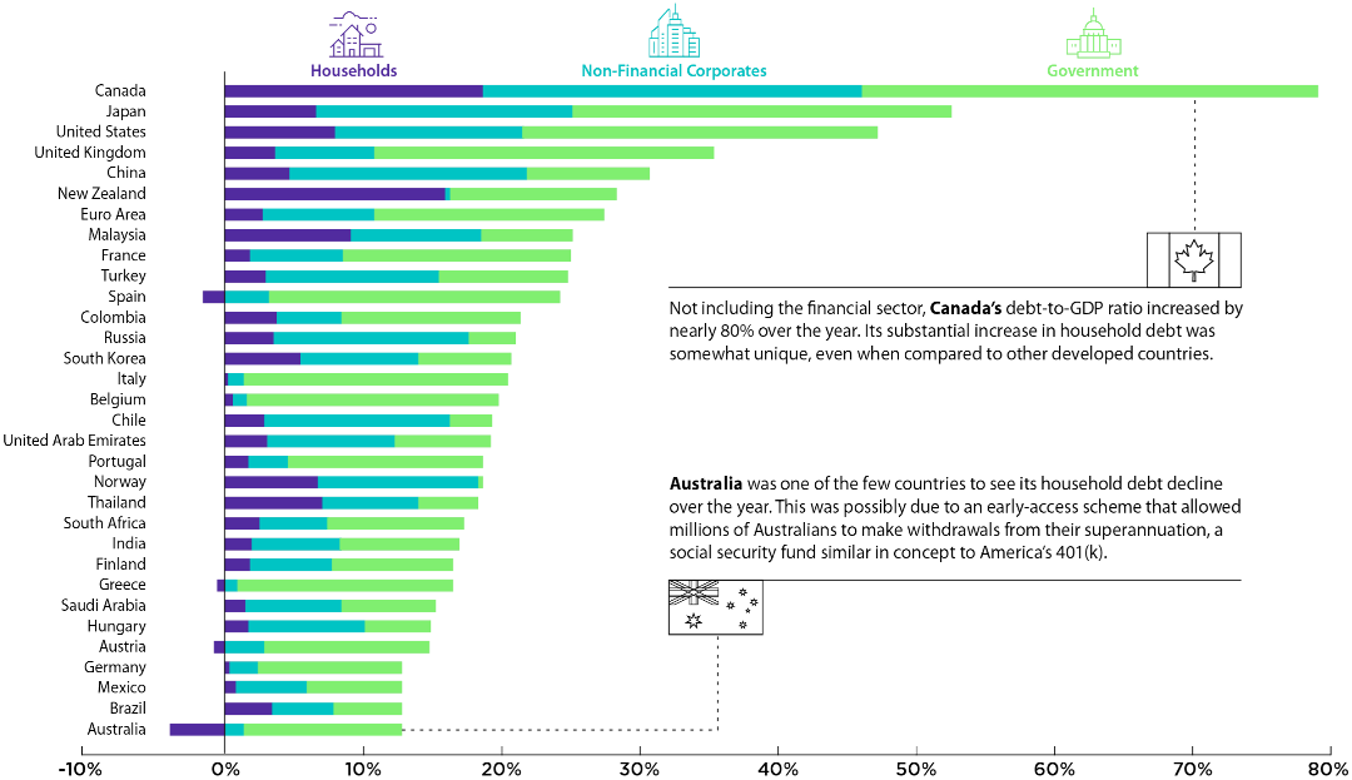

Going back to Mette Frederiksen’s opening statement, “I believe that we […] can invest us out of the crisis … ”, when saying that, she is assuming that we can afford to do so. Take a look at Exhibit 9 below. In most countries, the increase in debt-to-GDP in 2020 has been astonishing, and the numbers below don’t even include the final quarter of the year. As you can see, at the top of the tree, Canada has increased its overall debt-to GDP (ex. financial institutions) by no less than 80%, but Canada is far from the only country going through a massive increase in debt-to-GDP as a result of the pandemic.

Denmark is not included in Exhibit 9, but I know from other sources that Denmark’s government debt is estimated to have risen from about 33% of GDP in 2019 to 45% of GDP in 2020 (I do not yet have any numbers for the other sectors in Denmark). Mette Frederiksen’s statement is therefore not as outrageous as I first thought, but only because Denmark is near the bottom of the global debt tree, at least as far as government debt is concerned.

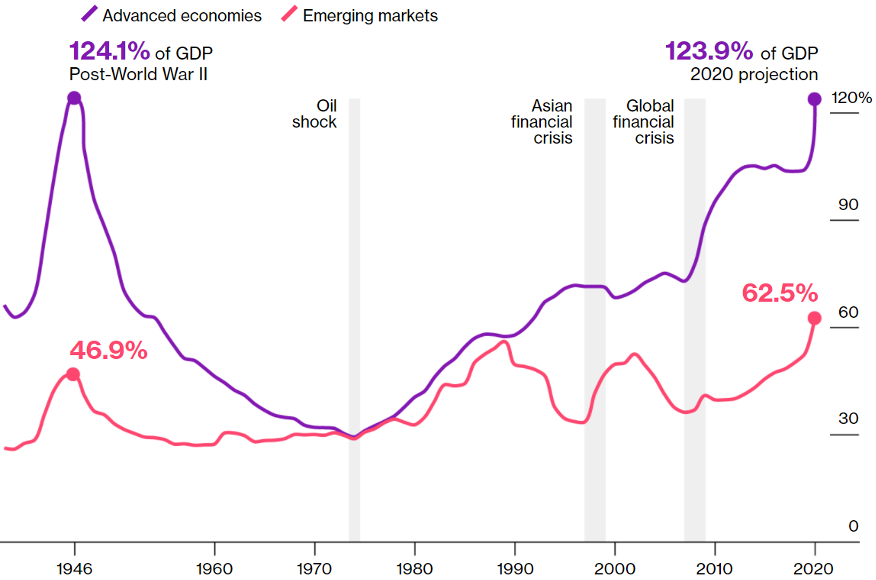

Most other countries are not as fortunate. According to Bloomberg (see here), the pandemic has added $19.5Tn of debt to a global economy already drowning in it. As a result, government debt-to-GDP globally is now in line with levels at the peak of the previous debt supercycle (Exhibit 10). As long-term readers of the Absolute Return Letter will be aware, for years, I have argued that we are approaching the end of the current debt supercycle which, by the way, is getting rather long in the tooth – almost 76 years old now versus c. 60 for the average debt supercycle.

Exhibit 10: Global government debt as % of global GDP Sources: Bloomberg

Where are we in the current debt supercycle?

The last debt supercycle in the West ended with World War II, and a new supercycle was born in the second half of the 1940s – one which is still alive and kicking. That said, as events have unfolded over the past 12 months, the end of the current debt supercycle has moved much closer and, at the present speed, we are approaching the day of reckoning at an uncomfortable pace.

Debt supercycles are not always global in nature. A gigantic build-up of debt in the 1850s and 1860s to finance the expansion of the US railroad system led to widespread asset speculation. It all culminated in 1873 when many US banks went bankrupt – an event that is now known as the railroad crisis. In Japan, a wave of real estate speculation in the 1980s culminated in 1989 when the Japanese debt supercycle collapsed. Now, some 30 years later, the Japanese are still paying the price.

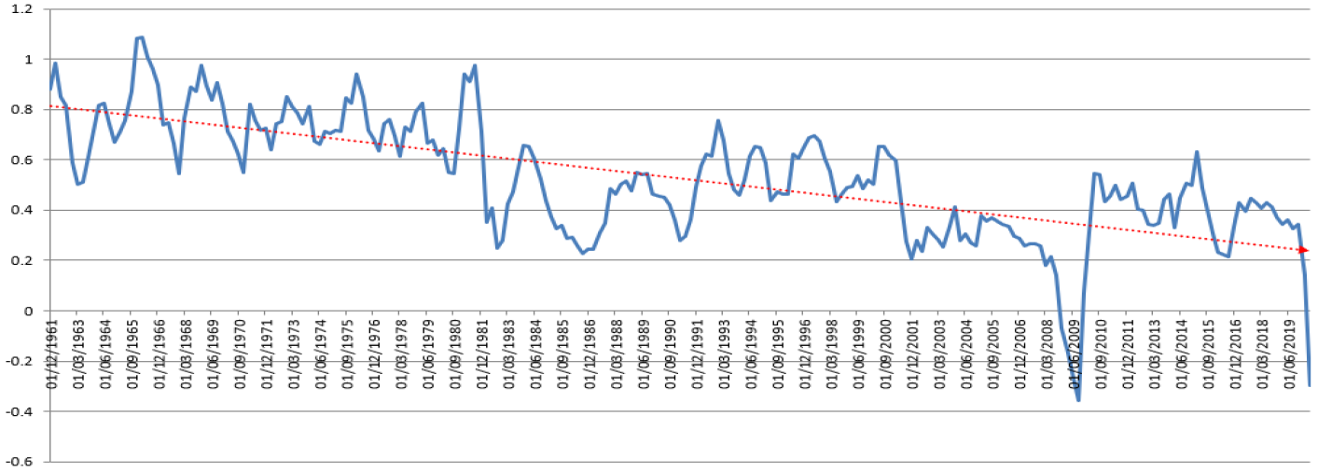

Exhibit 11: US nominal GDP growth per dollar of debt growth Note: 12-month averages Sources: MacroStrategy Partnership LLP

Precisely what will cause the current debt supercycle to end, I have no idea – no two supercycle collapses are identical. All I know is that all previous debt supercycles have ended when GDP has only grown about one-quarter of a dollar for every dollar of added debt. As you can see in Exhibit 11, in the US, we are effectively there now. I haven’t produced a chart to prove my point but, according to BIS, the ratio of ΔGDP/ΔDebt in China is below 0.25 now whereas, in the Eurozone, it is still comfortably above that level at about 0.35.

Final few words

Big fiscal spending programmes in many countries in 2021 will add significantly to already massive amounts of government debt. For now, we are getting away with it because the cost of servicing debt is so low, but that could change very quickly. In only one month, 10-year US government bond yields have risen 30 bps and, over the last year, no less than 113 bps – a rise very much driven by President Biden’s ambitious spending plans for this year and next.

The challenge Biden and his government is up against is that the US output gap is much smaller than it is here in Europe, i.e. to spend $1.9Tn of public money to fire up the US economy, as Biden plans to, could quite possibly turn into a case of serious over-stimulation, which will most likely have a negative impact on inflation and thus on interest rates.

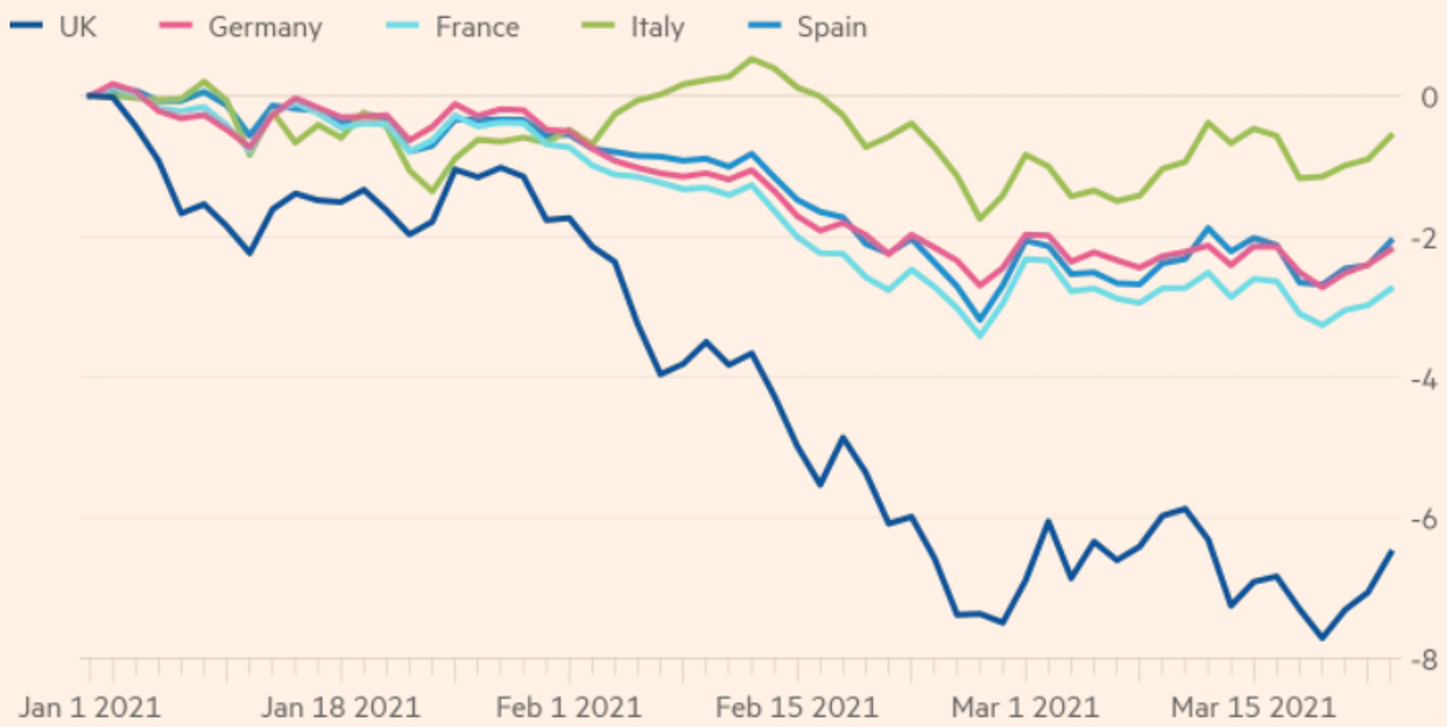

In Europe, the only major country which has declared its hand so far is the UK. Boris Johnson and his government are as eager as the Americans to inject some stimulus into the domestic economy, and UK gilts have reacted in kind with the yield up 39 bps over the last 12 months. The fact that the British can hardly afford to spend that much is being conveniently ignored by all but bond investors. Year-to-date, gilts are easily the worst-performing government bonds among the big five in Europe. As you can see in Exhibit 12, YTD losses on gilts are 2-3 times worse than those holders of government bonds in other major European countries have suffered.

Exhibit 12: Total returns on European government bonds in 1Q21 Sources: Financial Times

Now, a well-thought out stimulus programme would ensure that much of the capital that is being earmarked for stimulating a limping economy would be allocated to infrastructure spending, as that would lead to higher GDP growth, and with higher GDP growth follows elevated tax revenues. However, a combination of rising populism and adverse demographics make that unlikely to happen, and that is the real headache.