In 1974, U.S. President Gerald Ford took office “amidst one of the worst economic crises in U.S. history,” which was characterized by double digit inflation. Shortly thereafter, the new administration and Congress established the National Commission on Inflation, and the President declared inflation to be “public enemy number one.” He urged Americans to voluntarily increase personal savings and discipline their spending habits, with a goal of harnessing untethered price increases. “People who supported the mandatory and voluntary measures were encouraged to wear “WIN” (Whip Inflation Now) buttons, perhaps in hope of evoking in peacetime the kind of solidarity and voluntarism symbolized by the V-campaign during World War II.” Ultimately, the campaign to “whip inflation now” was an abject policy failure and years of economic and financial market volatility followed (Source: Wikipedia, as of March 31, 2021).

Policy Largess At a Time of Economic Tailwinds

Today, the Federal Reserve (Fed) is flirting with a mirror-image of that policy, by steadfastly adhering to its new average inflation targeting (AIT) ideology, which aims to thwart powerful secular disinflationary influences that have kept inflation stubbornly low for the last decade. Specifically, the Fed has promised to stay extraordinarily accommodative until economy-wide levels of inflation exceed their long run inflation targets for an extended period of time. And that policy would seemingly be pursued without regard to some very real left-tail risks around financial stability and possible unintended consequences. Thus, investors face a growing amount of uncertainty as a result.

Visibility is being clouded significantly further by surging fiscal stimulus amidst the rapid reemergence of the U.S. economy from the 2020 pandemic shock. Indeed, the combination of extreme central bank accommodation, combined with profound and historic deficit-financed fiscal policy is creating the most powerful economic policy cocktail in the history of peacetime America. This is occurring at a moment when the U.S. economy appears to already be functioning very near its potential. The federal government is pumping trillions of dollars of broad money liquidity into an economy that’s already flush with cash. The 2021 federal deficit Is now forecast to equal 15% of GDP, matching 2020’s record shattering deficit, and with the help of the central bank’s monetization of these deficits, U.S. broad money will continue to grow at an outsized clip. We estimate that by the end of this year, nearly a third of all broad money in circulation in the United States will have been created over a 20-month interval from the onset of the pandemic.

This policy largess comes at a time where the U.S. economy already enjoys the tailwinds of robust consumption, booming manufacturing and a red-hot housing market. It also comes at a time when household balance sheets are surprisingly strong, thanks to broadly distributed federal stimulus initiatives (for example, household debt service levels are near the lowest point they have ever been). And while some lagging services segments have been slow to rebound, it is highly likely that a recovery is close at hand with vaccine rollouts accelerating in earnest, catalyzing mobility, engagement and general economic reopening. This recovery will be further supported over coming quarters by the incremental spending associated with President Biden’s Build Back Better plan, and its bold endeavor to upgrade U.S. infrastructure and make broad-based societal investments.

Will Policy Threaten Fed Credibility?

With economic growth forecasts accelerating, and with inflation set to rise markedly for a handful of cyclical influences, policymakers risk looking increasingly out of touch with reality, which threatens their credibility and feeds volatility-inducing uncertainty. In fact, the Fed’s own GDP forecast of 6.5% real GDP growth this year is now running ahead of the 5.7% consensus estimate (Bloomberg, as of March 26, 2021), itself having been revised up from 3.9% at the start of the year. These are the largest numbers we’ve seen in at least 35 years, and at the current pace, they could rise to become the largest since World War II by the end of the year.

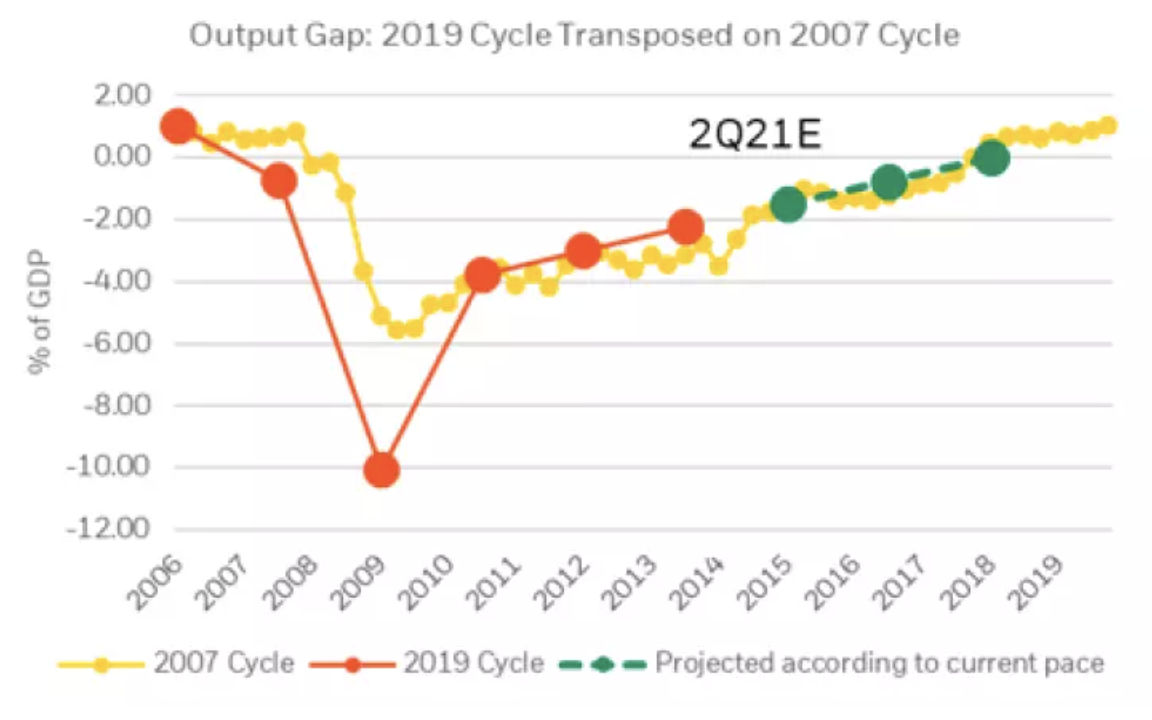

If it is hard to comprehend how we could have gone from the worst growth since World War II to the best in the space of a year; that is because we just ended the slowest post-war economic cycle in 2019 and began the fastest (the Covid cycle). The 2007 to 2019 cycle that troughed during the Global Financial Crisis (GFC) was a 55-quarter-long cycle, measured in relation to peaks and troughs in the output gap, taking 13 quarters to trough, and 34 quarters to recover. In the Covid cycle, a trough was formed in two quarters, and we are closing the output gap at a pace six times as fast as in the GFC, from a trough almost twice as deep (see first graph). That means that the four quarters since March 2020 are the equivalent of six years in the GFC recovery, placing us in theory at the equivalent of sometime in 2015.

The recovery has been nothing short of remarkable, and it is with that backdrop in mind that we question the efficacy of the AIT framework and worry that its core tenets are based in desired outcomes that would likely do more harm than good for society; outcomes that will quickly be sniffed out by markets. We are convinced that there are large swaths of the economy where disinflation, or price stability, are highly desirable for consumers, and particularly for households that deploy a disproportionately large share of their income on consumption. It is difficult for us to fathom how ongoing price increases in used cars, apparel, food etc., for example, are beneficial to the average consumer. Why should policy endeavor to offset the virtuous technology-driven disinflation of the last decade for these necessities?

There are undoubtedly parts of the economy where some inflation makes sense. Housing is an area where price increases over time can be linked with increases in consumer confidence and provide a tailwind to consumption through wealth effects. Similarly, stable prices for certain commodities (like energy) can incentivize investments and capital expenditures that can build a sustainable economic growth paradigm.

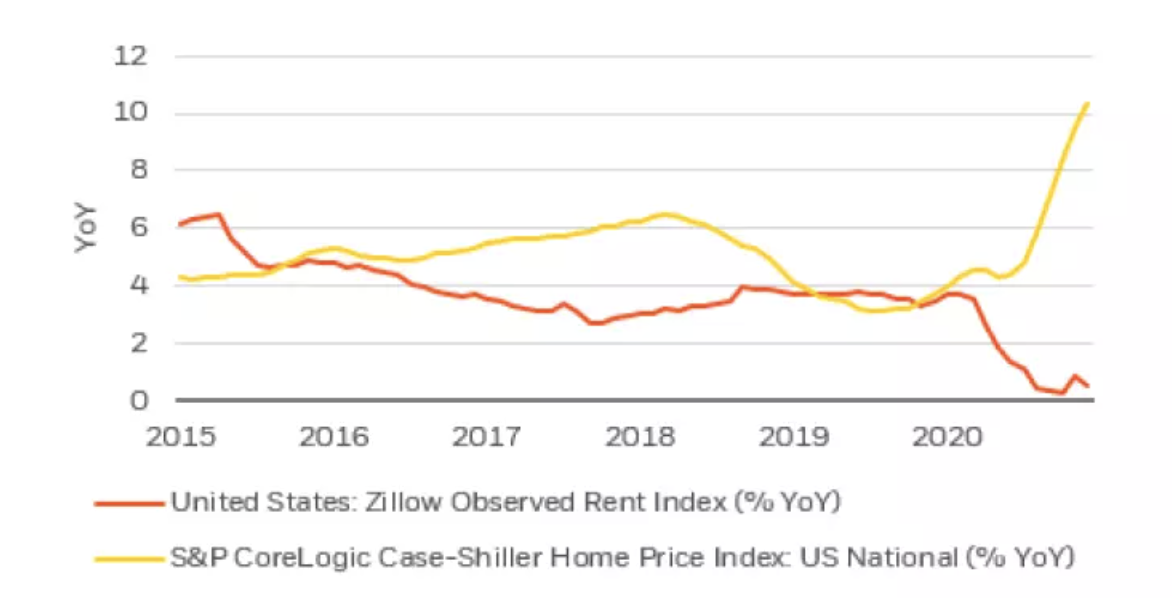

Yet the Consumer Price Index (CPI) faces limitations in capturing these nuances in inflation: for example, the shelter component only considers urban rental units, ignoring prices in the market for non-urban owner-occupied units. The Covid crisis has been unique in the sense that it has changed consumer preferences sharply away from the former and toward the latter, as evidenced by the collapse in Zillow’s Rent Index, and the surge in Case-Shiller’s house price index since January 2020 (see second graph). It is not the Federal Reserve’s mandate to shape consumer preference, yet their mandate is to implicitly prop up urban rental units and ignore price fluctuations in the owner-occupied market, simply because the former is where we tend to measure housing cost inflation.

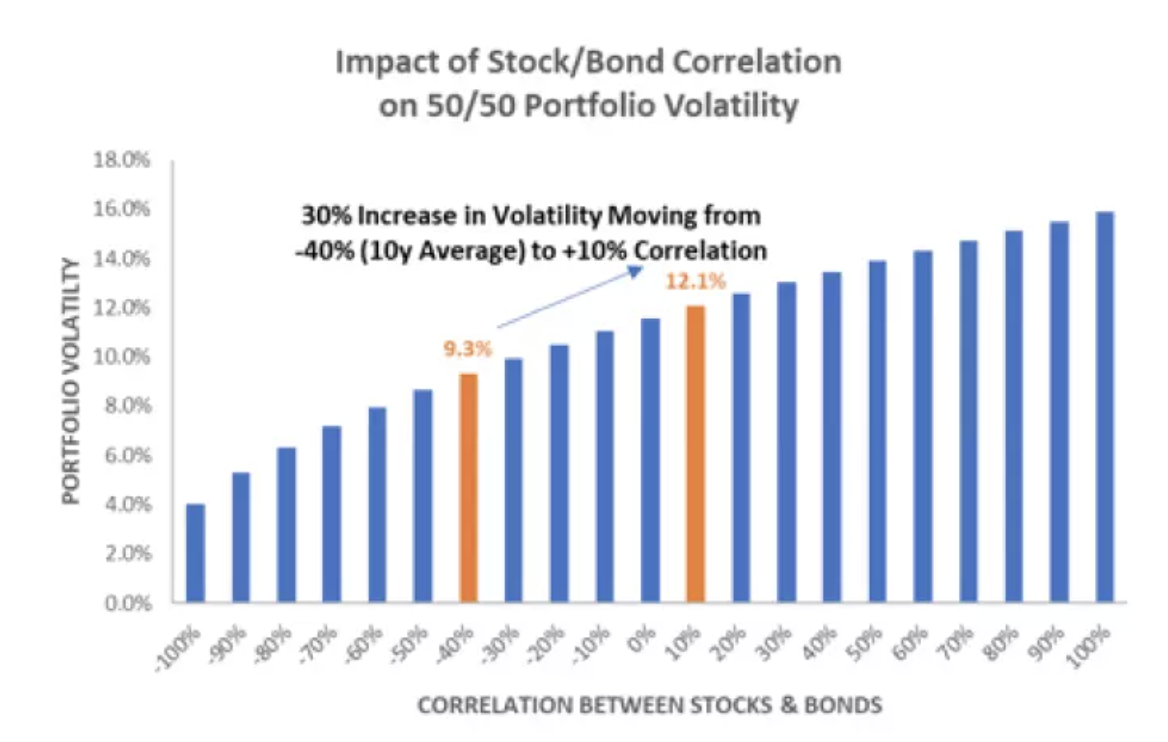

Markets may become increasingly nervous about the dissonance related to robust and accelerating fundamentals combined with excessive and ongoing emergency monetary and fiscal policy accommodation, and the impact this combination ends up having on asset prices (not least, houses). Nominal U.S. Treasury yields have surged over recent weeks with realized volatility for these “risk-free” assets spiking. The “smooth functioning” of U.S. financial markets that is thought to be an unspoken third mandate of the Federal Reserve has diminished markedly over that same timeframe. In our view, this may be leading to diminished trading liquidity and a breakdown in many traditionally reliable cross-asset correlations (for instance, the long-term correlation between stocks and bonds has flipped, as displayed in graph three).

Can Economic History Provide Guidance?

Leafing through the history books, there was similar uncertainty around growth, inflation and the path of policy in 2015. The Chinese currency was devalued in August of that year, and oil prices collapsed 30% into the end of the year. Risk assets did not do well that year, and in fact, the Bloomberg High Yield Index had its worst calendar year total return since 2008. The Fed also ended up hiking rates in 2015 for the first time in that cycle, creating uncertainty as to the effectiveness of the risk-free rate as a portfolio hedge. The fact is that higher yields in the risk free spectrum take away a commonly used fixed income portfolio hedge, and act as a headwind for price returns in assets down the capital stack – especially if starting valuations are at the lows in spread or yield, as they were then, and as they are now.

The risk-free U.S. Treasury rate is the foundation for pricing almost every asset in the world. As we continue moving into a higher real rate regime (detailed in our commentary Finding Some Real Perspective), the market may have to grapple with higher portfolio volatility, not just in the risk free market, but also in risk markets as well (see graph four). So, while strong growth still makes equities attractive relative to most fixed income assets, with yields moving higher (and with higher levels of volatility), even the equity-opportunity is less compelling until we enter a new regime where “duration adds value” again. When risk-free yields offer a margin of safety approaching equilibrium, that will help. But today there is a lot of debate about what two-to-five year “equilibrium” nominal growth might be.

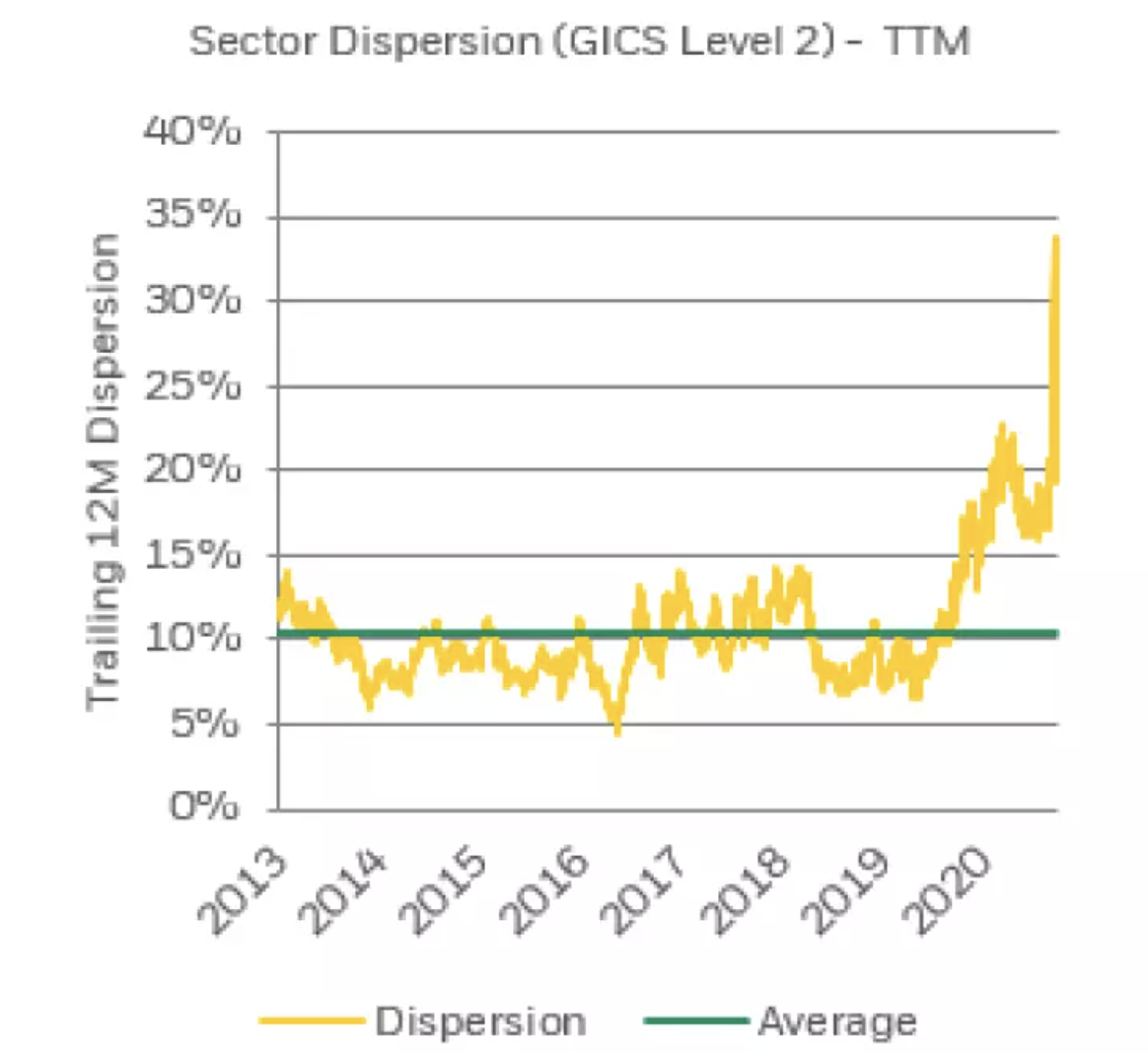

Similarly, we made a strong case for high yield when it offered three times the yield of investment-grade assets, but today one cannot even earn twice as much (as measured by the yields on the Bloomberg Barclays High Yield and Investment Grade indices, at 4.31% and 2.29%, respectively, as of March 30, 2021). As we referenced with the 2015 analog, there is not much risk premium left to harvest in credit spreads. Hence, portfolio construction needs to reflect a potentially more difficult operating environment for many financial assets over the coming weeks, just as year-to-date performance has been tough for fixed income, and divergent, at best, in equities and commodities. We think the best opportunities through mid-year (and they are indeed plentiful) will be intra-market, as sector and security-level dispersion remains at record highs (see graph five).

Human beings love to see patterns and symmetry, even in places where in actuality they may not exist. Looking to past precedent is a timeworn exercise for those studying economies and markets, in part because it often can be helpful in understanding the path one is currently on, but it can also be dangerous at those times when environmental conditions are truly unprecedented and therefore aren’t as subject to study through analogy. We are somewhat less bullish on financial assets than we have been over the prior year, or so, given the policy uncertainty, and despite the very large fiscal policy infused into an already “hot” economy, with the Fed simultaneously pouring more fuel on the fire. But to be clear, we still think there are opportunities to generate real return – it is simply a very different portfolio construct than we have recently been accustomed to. These times do appear to be unprecedented, warranting a commensurate degree of skepticism and caution from investors.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 2, 2021 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, LLC, member Finra

©2021 BlackRock, Inc. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States or elsewhere. All other marks are the property of their respective owners.

USRRMH0421U/S-1586781-1/10

© BlackRock

Read more commentaries by BlackRock