Elon Is Wrong About Bitcoin. Crypto Miners Are Key to Renewables' Success

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

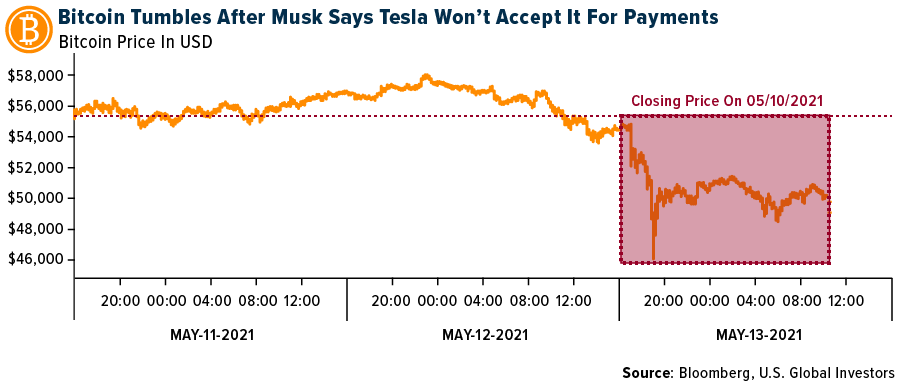

And just like that, Elon Musk has turned on Bitcoin.

In a tweet on Wednesday, the self-proclaimed “Technoking of Tesla” said his company—which announced in February that it bought $1.5 billion in Bitcoin—would be suspending vehicle purchases using the cryptocurrency. Musk cited crypto miners’ “increasing” use of fossil fuels, particularly coal, “which has the worst emissions of any fuel.”

The price of Bitcoin responded by dipping below $50,000, ending the day down more than 12%, its worst trading session since January.

I don’t question Elon Musk’s good intentions, but I respectfully disagree with the underlying insinuation that crypto miners in particular are a threat to the climate. It’s just not true, for reasons I explain below.

Don’t get me wrong: The computer processing power needed to mine Bitcoin, Ether and other digital tokens is not insignificant. The University of Cambridge’s Bitcoin Electricity Consumption Index (CBEI) estimates that the global Bitcoin network, running at full capacity, uses about 147.8 terawatt hours (TWh) on an annualized basis, or almost as much as Sweden consumes every year.

That’s a big number, but it doesn’t take into account the percentage of Bitcoin mining that uses renewable energy. In a December 2019 report, CoinShares believed it to be 73%. Last month, ARK Invest’s Yassine Elmandjra said it was closer to 76%.

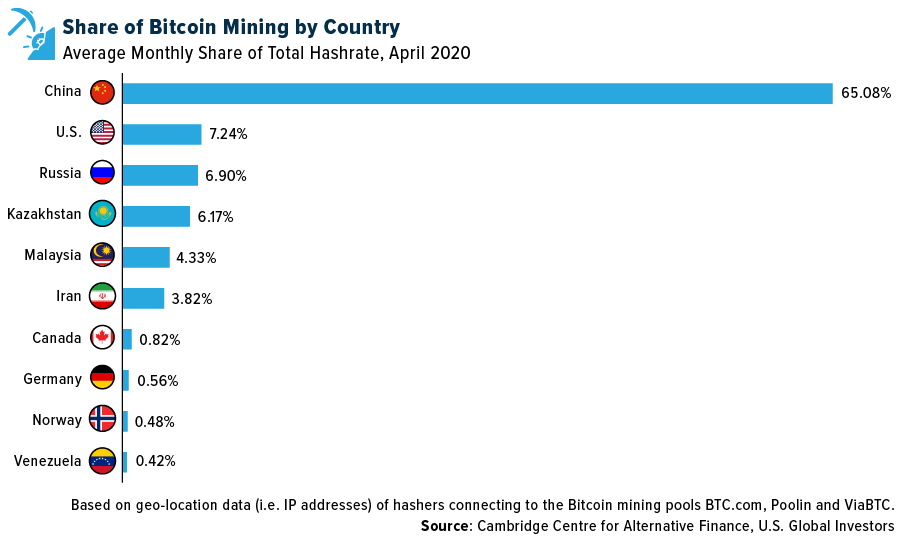

I wish Musk had included these figures in his very one-sided comment. He also failed to point out that a vast majority of the world’s Bitcoin mining is done in China. North American Bitcoin enthusiasts shouldn’t be penalized for how cryptos are generated in other countries.

|

Because Bitcoin is on the blockchain, you can see where each unique token originated. If Musk is truly serious about promoting green energy, he could easily change the policy to say that only Bitcoin that was mined using renewables can be used to purchase a Tesla.

Similarly, maybe he should only sell his electric vehicles (EVs) in states where renewables represent the greatest share of electricity generation (Vermont, Maine, Idaho, Washington) and restrict sales in states that still heavily rely on coal (West Virginia, Wyoming, Missouri, Kentucky).

Musk’s influence on capital markets and asset prices rivals that of even Warren Buffett. He’s worth tens of billions of dollars more than Buffett, in fact, and he commands a Twitter audience of 55 million. As the saying goes, with great power comes great responsibility.

Square: Crypto Is Key to a Clean Energy Future

I expect the crypto mining network to convert entirely to renewable energy much more rapidly than other industries precisely because it uses so much energy. Solar and onshore wind are now cheaper than coal and even gas, so it only makes sense from a cost perspective.

Take HIVE Blockchain Technologies. We use nothing but cheap renewable energy in Sweden, Iceland and elsewhere to mine Bitcoin and Ethereum. This is one of the reasons why HIVE is among the most profitable crypto miners right now.

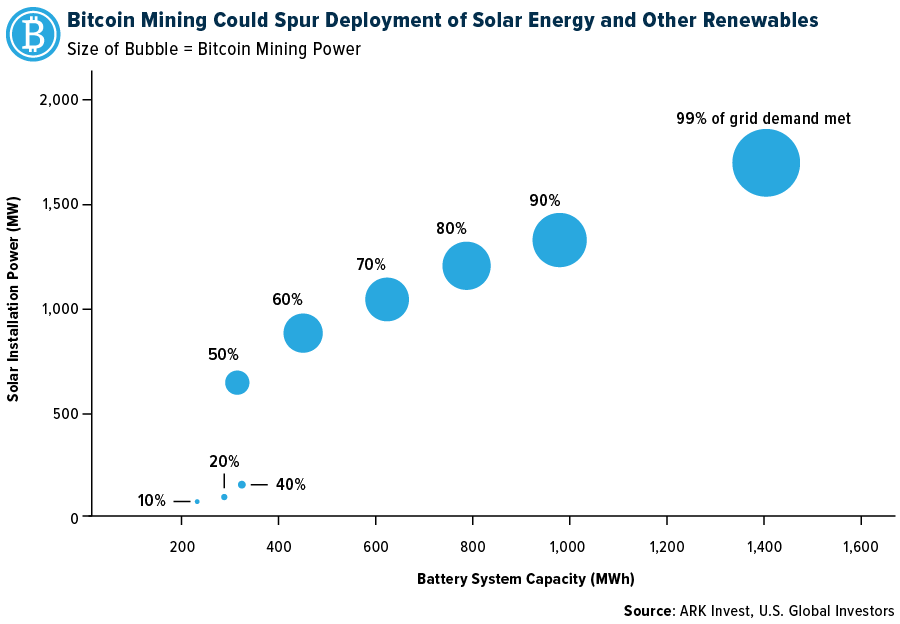

Crypto mining may even help accelerate the deployment of renewable energy, which should please Musk. That’s according to a special report published last month by Square and ARK Invest. The digital payments company says that, because crypto miners are “unique” energy buyers, they’re an ideal complement to wind and solar as well as better storage technology. Returns on investment could be improved, for one thing, which would incentivize the deployment of new renewable and storage projects.

The chart below illustrates the impact that Bitcoin mining could have on solar in particular. The size of each blue bubble is proportionate to the size of the Bitcoin network in the U.S. As the size of the network increases, the greater amount of solar power (y-axis) and battery storage (x-axis) is available to the energy grid. “Increasing Bitcoin mining capacity could allow the energy provider to ‘overbuild’ solar without wasting energy,” the report says.

I believe this model could be a win-win for not just crypto miners, which would get access to cheap energy, but also states that have aggressive decarbonization goals. Everyone’s needs would be met.

Mike Colyer, CEO of New York-based crypto services firm Foundry, agrees. Locating renewable energy projects near crypto mining operations “allows for a faster payback on those solar projects or wind projects,” he told Markets Insider in March. More renewables “can be built faster in regions where before it was not attractive because they would produce too much energy for the grid in that area.”

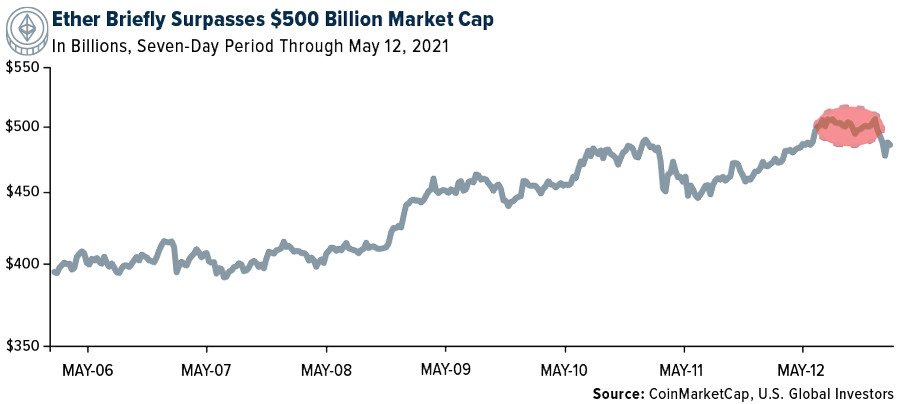

Total Crypto Ecosystem at $2 Trillion Market Cap, Ether at $500 Billion

Despite Musk’s flip-flop, demand for cryptos continues to boom, with trading on major crypto exchanges reaching an incredible $1.7 trillion in April. Early that month, the size of all cryptocurrencies surpassed $2 trillion for the first time, more than double where it was at the beginning of the year.

Early Wednesday, the market cap for Ether, the number two digital coin, briefly surpassed $500 billion as its price touched a new all-time high of over $4,300 before declining on Musk’s tweet. To put that in perspective, $500 billion is greater than the market cap for JPMorgan and Visa.

Ether Demand Is Reflective of Growing Awareness of DeFi’s Potential

Ether, of course, powers the Ethereum network, which is the basis for decentralized finance (DeFi). With Ethereum, anyone with an internet connection can have access to financial services—from banking to investing to borrowing and lending—that in the past have been opaque, tightly-controlled and inequitable. When there are no overhead costs associated with running a traditional bank or insurance firm, prices can come way, way down. And since everything is built on smart contracts, human error can be eliminated.

The growing demand for Ether tells me investors are becoming more and more aware of DeFi’s potential in making financial services cheaper, faster, more reliable and more equitable. It’s also a big reason why we made the decision to mine Ether at HIVE on top of Bitcoin. Bitcoin is clearly digital gold, which I believe will remain hugely in demand, but Ether is the fuel that powers the whole system.

In Recognition of Roy Terracina

On a final note, I’d like to brag on my friend if I may. Roy Terracina, serial entrepreneur and longtime vice chairman of U.S. Global, was awarded an honorary Doctorate of Humane Letters last weekend from Our Lady of the Lake University (OLLU) here in San Antonio in recognition of his many years on the school’s Board of Trustees.

When Roy joined the Board in 2006, he applied his remarkable business acumen to help make OLLU more competitive at a time when many private schools were struggling financially.

When Roy joined the Board in 2006, he applied his remarkable business acumen to help make OLLU more competitive at a time when many private schools were struggling financially.

A first-generation college student, Roy set about making sure OLLU was attracting nontraditional and historically underserved students and helping them succeed, not just academically but also holistically. He was instrumental in bringing online education to the university as well as intercollegiate athletics.

One story in particular stands out as indicative of Roy’s generosity and selflessness. He got the sense one day that members of the basketball team weren’t fully satisfied, and when he asked them what could be improved, the players said they didn’t have matching shoes like the other teams.

“Go out and buy the shoes, then send me the bill,” he told them.

To my friend—tireless entrepreneur and mentor, talented boxer, beloved husband and father, and now doctoral degree recipient—congratulations! I couldn’t be prouder.

Gold Market

This week spot gold closed at $1,843.43, up $12.19 per ounce, or 0.67%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.07%. However, the S&P/TSX Venture Index came in off 2.47%. The U.S. Trade-Weighted Dollar rose 0.10%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-11 | ZEW Survey Expectations | 72.0 | 84.4 | 70.7 |

| May-11 | ZEW Survey Current Situation | -41.6 | -40.1 | -48.8 |

| May-12 | Germany CPI YoY | 2.0% | 2.0% | 2.0% |

| May-12 | CPI YoY | 3.6% | 4.2% | 2.6% |

| May-13 | Initial Jobless Claims | 490k | 473k | 507k |

| May-13 | PPI Final Demand YoY | 5.8% | 6.2% | 4.2% |

| May-16 | China Retail Sales YoY | 25.0% | -- | 34.2% |

| May-18 | Housing Starts | 1703k | -- | 1739k |

| May-19 | Eurozone CPI Core YoY | 0.8% | -- | 0.8% |

| May-20 | Initial Jobless Claims | 460k | -- | 473k |

Strengths

- The best performing precious metal for the week was gold, up 0.67%. Gold is near its highest level in three months. Bond market expectations for the pace of inflation over the next five years surged on Monday to the highest since 2006. The recent consumer price index (CPI) data, which was much higher than expected, only bolstered this argument. Weaker-than-expected jobs data supports the case for dovish monetary policy. The U.S. dollar fell on the news, which also supported the gold price. April retail sales were reported on Friday and came in weaker than expectations, bolstering gold as yields and the dollar sank.

- Palladium continues to do well and should be undersupplied by about 1 million ounces per year, which is 9.5% of 2021 demand, according to UBS. 2021 supply has been reduced by 545,000 ounces due to some recent mine disruptions in Russia. UBS continues to see the metal going to $3,100 per ounce in the next few months. Additionally, comments by Sibaneye Stillwater CEO Neal Froneman indicates that mining companies have become more restrained on new project spending compared to 10 years ago, which may keep the market tight.

- Endeavor Mining reported a strong first quarter of $0.50 per share, above the $0.42 per share consensus. Production was 347,000 ounces of gold, compared to the 310,000-ounce consensus. Torex Gold also beat earnings forecasts by reporting earnings per share of $0.66 in the first quarter, above the $0.46 consensus. Cash costs were 10% below consensus, at $580 per ounce.

Weaknesses

- The worst performing precious metal for the week was platinum, down 2.11% on light news, falling with financial markets in general. Harmony Gold reported a weak fiscal third quarter, with volumes down 12% quarter-to-quarter. The weak volumes are related to COVID-related production issues. Cash costs rose 11% quarter-to-quarter due to lower volumes. The company’s Hidden Valley mine also had lower grades being mined. The next quarter will include significant plant maintenance.

- For the second consecutive year, purchases of gold on Akshaya Tritiya, considered to bring luck and prosperity, have been shuttered with the current COVID-19 wave running nearly out of control. The chairman of the All-Indian Gem and Jewelry Domestic Council noted that about 80% of the country is on lockdown, and while some sales will take place online, they will again be impacted as in the prior year.

- Fortuna Silver missed on first-quarter results and finished the week off by close to 3% with its peers off less than 0.5%. Fortuna’s share price weakness also pulled Roxgold’s share price lower on its all-stock bid to acquire Roxgold. While the C$40 million break fee is high, it reduces the value accretion to the new buyer to a gain of 31% versus 37%.

Opportunities

- Coeur Mining has announced its intent to acquire 17.8% of the outstanding shares of Victoria Gold at a price of C$13.20 per share. Additionally, Orion will receive about 5% of the shares of Coeur Mining and achieve a liquidity even. Orion also agreed to vote in favor of Coeur Mining acquiring more than 50% of the shares of Victoria if that ever occurred. It’s significant that we have seen another transaction in the junior mining space where a more senior peer is finding value in production more accretive than exploration currently.

- Investment Bank Liberum wrote recently that the diamond market looks to be in better condition after a rocky few years. Major producers have reduced inventories significantly without lowering pricing, thus implying demand has been robust. There are a limited number of diamond producers to invest in. Diamond exploration is much riskier while the macro lift in diamond markets could most directly be played through the producers.

- Montage Gold reported initial results on its drilling program at the Kone Gold Project, which were the best to date. There was high gold quality grade, which could lead to higher production (about 200,000 ounces per year) during the first five to seven years of the mine life. The preliminary economic assessment is expected in two weeks.

Threats

- Barrons highlighted that the gasoline lines we saw this week have to remind you of the 70s inflationary period. But Barrons points out that during the decade of the 1970s, investors had money market funds with high yields to try to keep up with inflation. With such a historic descent in interest rates, there are few ways to protect your wealth through cash substitutes. Barrons notes that TIPs and gold could play a role in investors’ portfolios today.

- The Western Electricity Coordinating Council (WECC), which monitors electric grids in the western U.S. and Canada, estimates that without imports, Nevada, Utah and Colorado could be short power during hundreds of hours this year, or equivalent to 34 days. New Mexico and Arizona fare a little better with being short only 17 days, under worst-case scenarios this year. The WECC’s Jordon White said: “It’s no longer necessarily a California problem or a Phenix problem. Everyone is chasing the same number off megawatts.” Miners included!

- AngloGold Ashanti and Barrick Gold continue to trade with little premium for management with the Democratic Republic of the Congo still not repatriating their profits back to the companies this year. Plus, the state-owned Congolese mining company SOKIMO has lodged a claim against Kibali Goldmines for $1.114 billion for unpaid dividends and other funds.

Index Summary

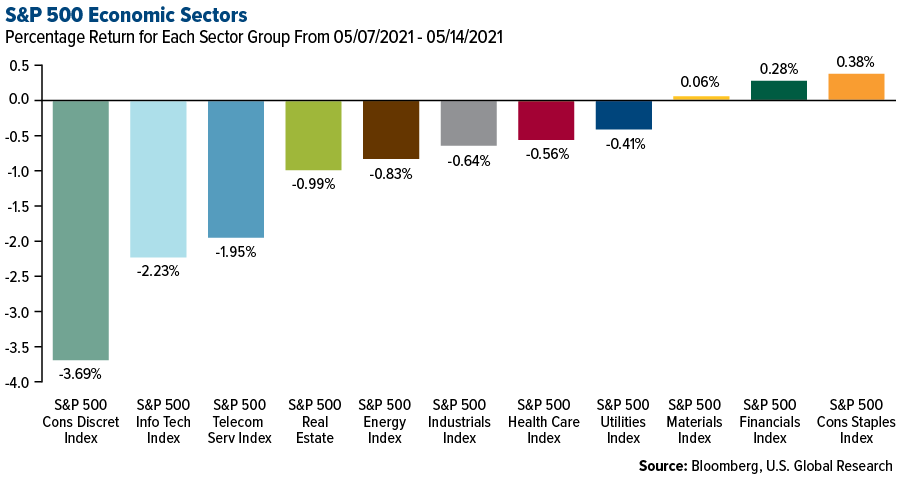

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.14%. The S&P 500 Stock Index fell 1.39%, while the Nasdaq Composite fell 2.34%. The Russell 2000 small capitalization index lost 2.07% this week.

- The Hang Seng Composite lost 2.45% this week; while Taiwan was down 8.43% and the KOSPI fell 1.37%.

- The 10-year Treasury bond yield rose 5 basis points to 1.631%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Australian Safe Shepherd, rising 2870.95%.

- South Korea-based technology giant Samsung announced that it is connecting its smartphone cryptocurrency wallet to Ledger storage devices. Launched in 2019, the Samsung Blockchain Wallet supports Bitcoin, Ether, ERC-20 tokens, Tron, and Tron’s ERC-20 analog, and allows third parties to create decentralized apps. Samsung’s VP and Head of Blockchain said that the company is planning on expanding its wallet’s support to more cold storage wallets and added that monthly active users of its blockchain ecosystem have doubled in the past seven months.

- Ethereum’s market capitalization surpassed the $500 billion mark this week, as the blockchain’s native token Ether set a new-record high, trading at $4,362.35 per token. This week saw Ethereum surpassing market capitalizations of financial behemoths JPMorgan Chase & Co. and Visa Inc. Ethereum’s record setting rally is backed by fundamentals, as the number of active Ether addresses also rose to a record high of 7.94 million, topping the previous peak of 7.14 million reached in January 2018.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Crypto Village Accelerator, down 99.18%.

- Colonial Pipeline, which was the victim of a ransomware attack this week, has reportedly paid $5 million in an “untraceable cryptocurrency” as ransom to its alleged Eastern European hackers. Contrary to earlier reports, the private company did pay the hackers, who the FBI has identified as having links to the DarkSide group, to restore its functionality. “Untraceable cryptocurrency” suggests that the payment was made using privacy coins like Monero or Zcash, but people familiar with the matter noted that the ransomware group demanded payment in Bitcoin.

- Bitcoin is set for another weekly decline as the world’s biggest cryptocurrency based on market capitalization fell below $50,000 per coin for the first time in almost three weeks. The sell-off is being attributed to Elon Musk tweeting that Tesla will no longer allow customers to pay for its vehicles using Bitcoin, citing issues regarding the environmental impact of mining the cryptocurrency. Although Bitcoin has since jumped above the $50,000 mark, the volatility and influence from one tweet does showcase that the crypto markets could benefit from investor protection and additional regulations.

Opportunities

- Toronto-based Ninepoint Partners LP is planning on dedicating a portion of its crypto ETF’s 0.70% management fee to offset the fund’s carbon footprint. The Canadian investment firm announced that it is partnering with CarbonX, an environmental software fintech-firm, to purchase carbon credits and support forest conservation projects. Additionally, the Crypto Carbon Ratings Institute, which tracks energy consumption and environmental impact of cryptocurrencies, will work in tandem with CarbonX to provide carbon footprint analysis to Ninepoint Partners.

- San Francisco-based Bitwise Investments launched a new ETF that provides its investors exposure to companies in the cryptocurrency sector. Trading under the ticker “BITQ”, the Bitwise Crypto Industry Innovators ETF aims to track Bitwise’s Crypto Industry Innovators 30 Index, which is made up of companies that have either 75% of their income derived from cryptocurrencies or 75% of their net assets in cryptocurrencies. Furthermore, firms with at least $100 million of liquid crypto assets on their balance sheet are also included in the ETF.

- Spain’s stock exchange BME is testing its blockchain infrastructure for small and medium-sized enterprises (SMEs) financing under the guidance of a regulatory sandbox created by Spain’s Ministry of Economic Affairs and Digital Transformation. The tests will allow BME to examine the suitability of the Ethereum-based system in raising capital for limited liability companies outside the traditional bank financing route. BME reported that its blockchain platform seeks to facilitate SME financing digital assets that represent funding avenues like convertible notes and participatory loans, adding that the platform will also include a digital wallet for SMEs to store both their financial investment instruments and electronic money.

Threats

- Bank of Korea (BOK) reported that it is seeking to maintain a stricter oversight on cryptocurrency trading activity via real-name bank accounts. BOK officials added that they are wary of unlawful crypto transactions causing risks to internal monetary control policies, and that the country’s Financial Services Commission (FSC) and the Financial Intelligence Unit are closely monitoring the crypto markets, with the FSC asking its employees to declare all their cryptocurrency holdings. BOK has given crypto service providers, including exchanges, custodians, wallet platforms and asset managers, until September to be in full compliance with the new reporting requirements. The nation also introduced a 20% capital gains tax on cryptocurrency trading profits above $2,200 beginning in January 2022.

- The Reserve Bank of India (RBI) is informally encouraging country’s lenders to cut ties with cryptocurrency exchanges. A senior executive at an Indian bank told Reuters that regulators are unofficially questioning banks as to why they deal in such speculative assets, adding that RBI is not comfortable with this type of trading activity that allows for money to flow overseas, citing money laundering risks. This comes a few months after India’s proposed ban on all private cryptocurrencies, discussions on which are currently ongoing.

- The U.S. Securities and Exchange Commission (SEC) issued an investor warning regarding risks of mutual funds that have exposure to Bitcoin futures, emphasizing the volatility of both Bitcoin and Bitcoin futures markets as well as lack of regulation and potential fraud or manipulation in the underlying Bitcoin market. Furthermore, the SEC said that it is closely monitoring Bitcoin futures-exposed mutual funds’ compliance with the Investment Company Act of 1940 and federal securities laws, and it will also assess the impact of mutual funds investing in Bitcoin futures on investor protection, capital formation, and the fairness and efficiency of markets. This comes on the back of the SEC delaying its decision on approving the VanEck Bitcoin ETF until June.

Domestic Economy and Equities

Strengths

- The number of Americans seeking unemployment benefits fell to 473,000. Last week’s unemployment claims marked the lowest level since March of last year when the pandemic spread quickly across the economy. Fewer employers are cutting jobs as consumers are spending more and businesses are reopening.

- New COVID-19 guidance was released this week from the CDC, saying fully vaccinated individuals no longer need to wear a mask or remain socially distanced from others in most settings, whether outdoors or indoors. U.S. COVID statistics have continued to trend in a positive manner (lower), with the seven-day new case rate now the lowest since September and the death rate hitting its lowest since July.

- NortonLifeLock Inc., an oilfield products and services company, was the best performing S&P 500 stock for the week, increasing 20%. Shares of the company rose after it reported fourth-quarter profit and revenue that beat expectations. Bank of America raised its recommendation of NortonLifeLock to a “buy.”

Weaknesses

- Inflation accelerated faster than most Bloomberg economists expected. Prices increased by 4.2% in April year-over-year, versus 2.6% in March and projected inflation of 3.6%. Used car and truck prices increased by 10% in April. The jump marked the largest one-month increase since data collection began in 1953. Other prices are rising as well, as the U.S. reopens and demand rebounds.

- Retail sales in April, a measure of spending at restaurants, stores and online, was unchanged, according to the Commerce Department. Bloomberg analysts were expecting an increase of 1%. March retail sales were revised up to 10.7% from a 9.7% increase.

- Hanesbrands Inc., was the worst performing S&P 500 stock for the week, decreasing 14.2%. Shares of the company declined 11% on Tuesday after the company announced an earning miss, recording the worst one-day drop in six months.

Opportunities

- No deal was announced this week from the infrastructure meeting at the White House, but the efforts are still there to have a set plan soon. President Biden is calling for a roughly $2 trillion infrastructure plan, in addition to another massive spending proposal on families and education.

- Problems with labor shortages in the United States should improve. Iowa and Tennessee joined a list of at least nine other states that are eliminating the extra $300 per week benefits ahead of the program’s expiration in September. Others argue that it is not the extra pay that is keeping workers outside of the workforce but the fear of the coronavirus and inadequate childcare.

- Cornerstone Macro says that the U.S. economy is booming. The massive stimulus package and easing of restrictions will further improve economic activity. The job market is strong and growth in blue collar jobs (manufacturing and construction) is leading the way, along with technology, health care, and innovative retailers.

Threats

- The BBH Global Currency Strategy team believes that risk to U.S. yields lie to the upside. With the 10-year trading around 1.6%, they don’t see much room to go lower, barring some sort of double recession due to the pandemic.

- If U.S. investors continue to worry about raising inflation, equites may fall. The fear of inflation is causing investors to speculate if the Federal Reserve may have to shift its policy sooner than expected, by either reducing bond purchases or even raising rates at some point.

- Last week, the Colonial Pipeline, one of the primary fuel pipelines on the East Coast, shut down 5,500 miles of its infrastructure because of a ransomware attack. The attack, which is being investigated, is causing fuel shortages in several states and an increase in gas prices. The Colonial Pipeline restarted operations of a major oil pipeline, but a return to normal operations will take days. Ransomware attacks are a growing problem for businesses of all sizes and scopes.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was palm oil, up 1.78%. Palm oil futures hit a record high as crop prices continue to rally because of weather damage and booming demand from recovering economies, especially China.

- Copper on the London Metal Exchange reached all-time highs of $10,747.50 a ton this week as investors worried about missing out on further gains and industrial buyers, who had been waiting for lower prices, had to bite the bullet. The metal also hit a record high on the Shanghai Futures Exchange as the most-traded June copper contract reached $12,094.62 a ton. Copper’s neck-breaking rally is being attributed to investors betting on increased demand for the metal as economies recover from Covid-19 and increase in investments in the green energy sector. Meanwhile, aluminum and zinc hit the highest in about three years.

- U.S. liquified natural gas (LNG) exports jump-started in May as more shipments are headed towards Asian buyers who are seeking to refill their inventories ahead of the summer. Through May 11, average daily shipments by exporters are up 6.6% from the previous month. Currently, at least 43 tankers are in transit to Asia, with China receiving 11 cargos, followed by Japan and South Korea getting seven and six cargos, respectively. On May 12, the five-day moving average of net flows to LNG terminals was measured at 10.6 billion cubic feet per day, which was 1.6% higher than year-to-date average.

Weaknesses

- The worst performing commodity for the week was lumber, down 16.79%. Lumber futures fell for the fifth straight day in the longest losing streak for the commodity in 2021. Traders believe that big box retailers like Home Depot and Lowe’s have plenty of inventory now and are expecting them to reduce future buying, freeing up wood for the commercial market.

- The worldwide shortage of semiconductors, which are critical in producing new cars and trucks, has sent the cost of previously owned vehicles to record highs. The U.S. Bureau of Labor Statistics reported that the cost of used vehicles went up by 10% in April, the fastest climb ever in the data that goes back to 1953. This increase accounted for more than a third of the 0.8% increase in the consumer price index, which was four times the level economists estimated. Manheim, U.S.’s largest vehicle auction house, stated that wholesale prices of vehicles was up 54% in April from a year earlier.

- Oil’s recent rally saw weakness as risk of Covid-19 outbreaks persists in Asian countries even as U.S. demand picks up. Japan announced extended curbs and restrictions, China saw its first infections in about a month, and key oil imported India continued to report more than 350,000 cases a day. IHS Markit also attributed the latest slip in oil prices to rising cases in India, parts of Southeast Asia and Latin America. The firm added that the market expects demand to materialize later this year and maintains support in the mid $60 to $70 range.

Opportunities

- Texas is set to install around 10 gigawatts (GW) of utility-scale solar power through the end of 2022. The U.S. Department of Energy reported that these installations would account for one-third of the total U.S. solar capacity. This report comes a few months after a record-breaking cold snap that dismantled about half of Texas’s generating capacity. Texas is already the biggest wind energy state, and these solar installations set set to make it No. 2 after California. Around 30% of the state’s new solar farms will be installed in West Texas, which has abundant sunshine, land and existing transmission lines that carry power from the region’s wind farms.

- Mergers and acquisitions (M&As) are increasing in the U.S. shale drilling industry as a sustained rise in oil prices has brightened the outlook for energy demand. Year-to-date, the volume of U.S. shale deals has doubled to more than $10 billion compared to the same period in 2020, with the deal surge being kicked off by Pioneer Natural Resources Co. purchasing DoublePoint Energy LLC for $6.4 billion. This week alone saw two deals valued at $1.82 billion, with Bonanza Creek Energy Inc. merging with Extraction Oil & Gas Inc. to form Civitas Resources Inc., and Laredo Petroleum Inc. announcing its plan to buy Sabalo Energy LLC.

- Aluminum, which closed at decade-highs earlier this month in London and Shanghai, may have more room to run as it draws strength from China’s carbon policies and the broader boom in commodities demand as economies recover from the Covid-19 pandemic. The lightweight metal has been one of the biggest winners of the current commodities rally, and its surge is being compounded by supply curbs put in place to decarbonize China, which is the world’s biggest aluminum producer. An analyst with the Shanghai Metals Market noted that Chinese demand for the metal in the first quarter was driven by property, auto and home electronics sectors, and that aluminum inventories in China will drop during the second quarter as the market balance remains tight.

Threats

- The Western Electricity Coordinating Council (WECC), which oversees electricity grids throughout the western U.S. and Canada, warned that western U.S. states could face blackouts as nearly a dozen states enter the summer months without ample electricity. These blackouts could be attributed to the following: climate change making it harder to forecast demand for electricity and shifting to clean energy straining power supplies. With the clean energy transition well on its way, states closing coal and gas-fired plants are not replacing them fast enough, reducing electricity capacity while demand is on the rise, and the existing power infrastructure is vulnerable to wildfires, drought and heat waves. The WECC reported that none of the states in its coverage area generate enough electricity to meet its own needs during periods of high demand, and this has led to utility providers signing contracts for more emergency power supplies and are trying to ensure that they do not rely on the same suppliers as everyone else.

- A drought gripping Brazil and China buying U.S. supplies has sent corn prices to their highest levels in eight years. This global supply squeeze is boosting the cost of feeding chickens, pigs and cows and has stoked concerns about food inflation on a global scale. China’s record-breaking imports of corn comes on the back of its hog herds recovering faster than expected from a deadly swine fever, and an increase in demand led by professional farms replacing backyard operations, which tended to feed their pigs table scraps instead of corn and soy meals. Additionally, the U.S. is expected to decrease its outlook for Brazilian corn stockpiles from 109 million metric tons to 103 million, citing planting delays and an ongoing drought.

- India’s fight against rising Covid-19 infections and deaths is threatening operations at its biggest ports, which could trigger shipping delays that might reverberate through global supply chains. Karaikal Port in south India, which is the country’s biggest non-state port and handles commodities like coal, sugar and petroleum, invoked force majeure until May 24. IHS Markit associate director Pranay Shukla reported that India has 21.9 million tons of cargo coming to its ports this month, but with labor shortages at some ports, shipping vessels could see discharge delays, and this would create supply chain bottlenecks.

Airline Sector

Strengths

- The best performing airline stock for the week was Aegean Airlines, up 8.3%. Sun Country reported surprisingly strong first-quarter earnings of ($0.09) per share, which was better than the consensus of ($0.28) per share. Revenues were 9% above consensus. The company also indicated that it will be adding three new planes to its fleet this year.

- Mesa Air reported surprisingly strong earnings of $0.23, which was above the consensus of $0.18 for the quarter. The company’s partnerships with United Airlines and American Airlines are back to flying 90% and 100% of the block hours compared to pre-pandemic levels. The company is also employing a successful strategy in which it is expanding from being solely a regional carrier to also handling freight and cargo business.

- Moody’s, in a recent airline report, upgraded the industry to positive from negative. The group believes that conditions will materially improve over the next 12-18 months due to higher vaccinations, less travel restrictions and increased demand overall. However, Moody’s does continue to expect that the industry will report operating losses in 2021.

Weaknesses

- The worst performing airline stock for the week was Norwegian Air Shuttle, down 39.1%. Estimates continue to be lowered by 7% for Air France/KLM due to a much slower ramp up of capacity than expected. Capacity will only be 55-60% of 2019 levels during the peak summer season.

- Airlines are carrying extra fuel on board due to the cyberattack that happened to one of the nation’s largest fuel pipelines. United has been carrying extra fuel on board flights that touch a major East or Southern arrival or departure point. Southwest is also actively managing its fuel needs throughout the system while American has been adding a “fuel stop” to a few of its flights.

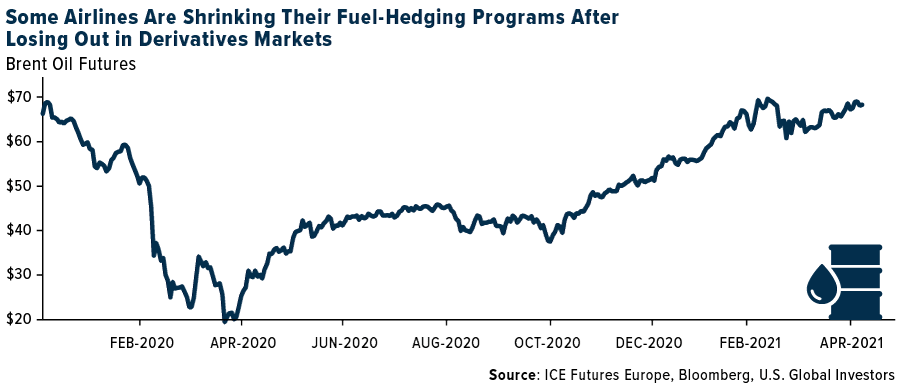

- Airlines are shrinking their fuel hedging programs after losing billions last year due to oil prices falling and oil needs dropping significantly. The carriers were stuck with unprofitable contracts that they had to honor. British Air will shrink its hedging to 60% of requirements. Previously the company was 90% hedged when oil prices collapsed last year, which created losses. Lufthansa is cutting its fuel hedges by 20%.

Opportunities

- Airlines continue to witness improved results, with Allegiant indicating that its demand momentum and booking curves are almost normalized. The company noted that the summer schedule will have higher traffic than 2019.

- UBS had some positive comments on the business jet market, saying they believe that the surge in global wealth will drive demand for this type of travel. Most of the buyers of business jets are first-time buyers, which is good for the market over the longer term. Corporate demand receded due to the pandemic, but demand is starting to return slowly. UBS also expects to have margins better than pre-COVID levels even without a full corporate recovery.

- Delta indicated that the demand acceleration that airlines are experiencing is continuing, specifically indicating that the fare environment can improve toward the end of the second quarter.

Threats

- Airline bookings began to slow at the start of May, primarily seen in both domestic and international bookings. Leisure demand has flattened out, with tickets sold being down 5% from 2019 levels.

- Traffic growth assumptions may be high for Japanese airlines. The slow rate of vaccinations in the country has been hampering acceleration. Airline traffic has been at 35-40% of normal levels in Japan.

- There has been a sharp rise in reported unruly passengers over the issue of masks being required while in an aircraft. There have been 1,300 incidents over the past three months, as opposed to 1,300 incidents over the past 10 years. Violations have been found in 260 of the 1,300 cases in the past three months. Fines for such violations can be up to $30,000.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 3%.The best performing country in Asia this week was China, gaining 2%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 0.70%. The Vietnamese dong was the best performing currency in Asia this week, gaining 0.10%.

- The European Commission revised its growth forecast to 4.3% in 2021 and 4.4% in 2022, up from 3.8%. The eurozone now expects all member states to see economies return to pre-COVID levels by the end of 2022. Europe was slow in rolling out vaccinations initially but is now improving the process.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 1.2%. The worst performing country in Asia this week was Taiwan, losing 8%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 2.3%. The South Korean won was the worst performing currency in Asia, losing 1.25%.

- Taiwan is experiencing worsening COVID-19 outbreaks on an island where almost no one is vaccinated. Equites trading on the Taiwan Stock Exchange declined sharply this week not only due to an increased number of reported COVID-19 cases, but due to a global sell-off in technology stocks and worries that Taiwan’s surging leverage is making equity markets riskier.

Opportunities

- Poland is planning to create eastern Europe’s largest energy group by merging PKN Orlen with PGNiG Sa and Lotus. Bloomberg reported that the enlarged company, with expected annual sales rising to 200 billion zloty ($53 billion), could boost Poland’s green transition as the country may have trouble reaching the European Union’s zero-emission target by 2050. The transaction could take a year to complete.

- The United States agreed to remove Chinese smartphone maker Xiaomi from the U.S. blacklist. Former President of the United States Donald Trump initiated the process to set a list of Chinese companies with links to the country’s military, prohibiting U.S. investors from owning those names and forcing delisting from U.S. exchanges. If more names are removed from the U.S. blacklist it could suggest warmer U.S./China relations and a potential bounce in stocks.

- Russia is working on a mechanism that will allow the government to retire costly ruble bonds sold to raise emergency funds during the coronavirus pandemic. Russia doubled its borrowing last year to help shield the economy from the pandemic as oil prices collapsed and the U.S. weighted sanctions on the ruble bond sales. Now, the Russian ministry is considering possible funding sources for the buyback to reduce the volume of floating-rate debt.

Threats

- Inflation is spiking not only in the United States but in central emerging Europe as well. It may be too early to worry about high inflation because higher CPI readings could be due to the base effect, but central banks will be observing it closely and may switch to tightening policies if needed. Prices in Poland increased by 4.3% year-over-year, Hungary 5.1%, Czech Republic 3.1%, Russia 5.5%, and Turkey 17%. Russia hiked its main rate twice already this year and more rate increases are planned for later this year. Other banks may follow.

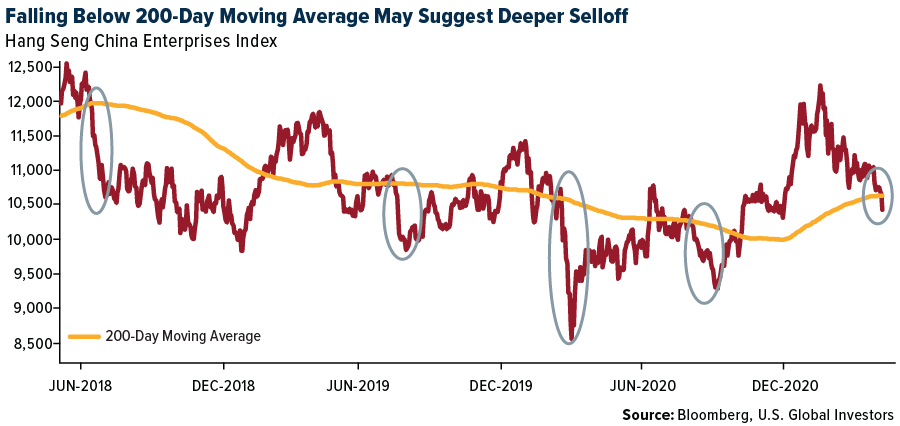

- Chinese internet giants continued to weaken this week on speculation that the Chinese government may increase regulatory pressure on the fintech sector beyond Jack Ma’s Ant Group. Alibaba, another internet giant, reported a 5.5-billion-yuan ($852 million) net loss, its first since 2012, after the company was fined a $2.8 billion fee for monopolistic behavior. The Chinese gauge closed below its 200-day moving average for the first time in six-months, and history shows that more weakness may follow.

- With a month delay, China released its 2020 consensus showing that the country is getting older and more urbanized. China’s population stands at 1.41 billion now versus 1.34 billion a decade ago, which is only an increase of 72 million people. More people are living in the city now (64% up from 50% in 2010). Older citizens (60 and higher) account for almost 20% of the total population and the younger group (age 15 to 59) fell by 7%.

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All