Strategic rivalry between the U.S. and China is creating a bipolar world. We believe investors need exposure to both spheres of growth to help meet their long-term goals.

Overview

01. An “undiscovered” market

China’s economy and capital markets have rapidly grown to become the second-largest in the world, yet foreign investors own only a minuscule share of Chinese stocks and bonds.1 We believe this is a missed opportunity for helping meet investors’ long-term goals.

02. Potential diversification

Investors will need deliberate diversification across countries, sectors and companies, in our view. How to gain exposure to the Chinese sphere of growth? It’s not just about Chinese assets; it’s about investing in companies, sectors and countries that are leveraged to Chinese growth.

03. A matter of balance

Both China and the U.S. are seeking self- sufficiency in the critical industries of the future. We believe investors need to balance the investment case for gaining exposure to both within their objectives and constraints, as well as with possible investment restrictions on each side.

China has emerged from the pandemic with renewed confidence – just as it did after the global financial crisis. Growth has bounced back to trend and foreign direct investment inflows are surging.2 A stable economic backdrop has made authorities more comfortable emphasizing structural reforms over short-term growth targets, in our view.

This signals greater emphasis on reducing risks in the financial sector, reliance on imported technological know- how and pursuing self-sufficiency in energy.

We believe the narrative on the health of China’s financial system has shifted markedly. Its economic and market outperformance through yet another global shock has brought sharply into focus the resilience Chinese assets can help bring to portfolios.

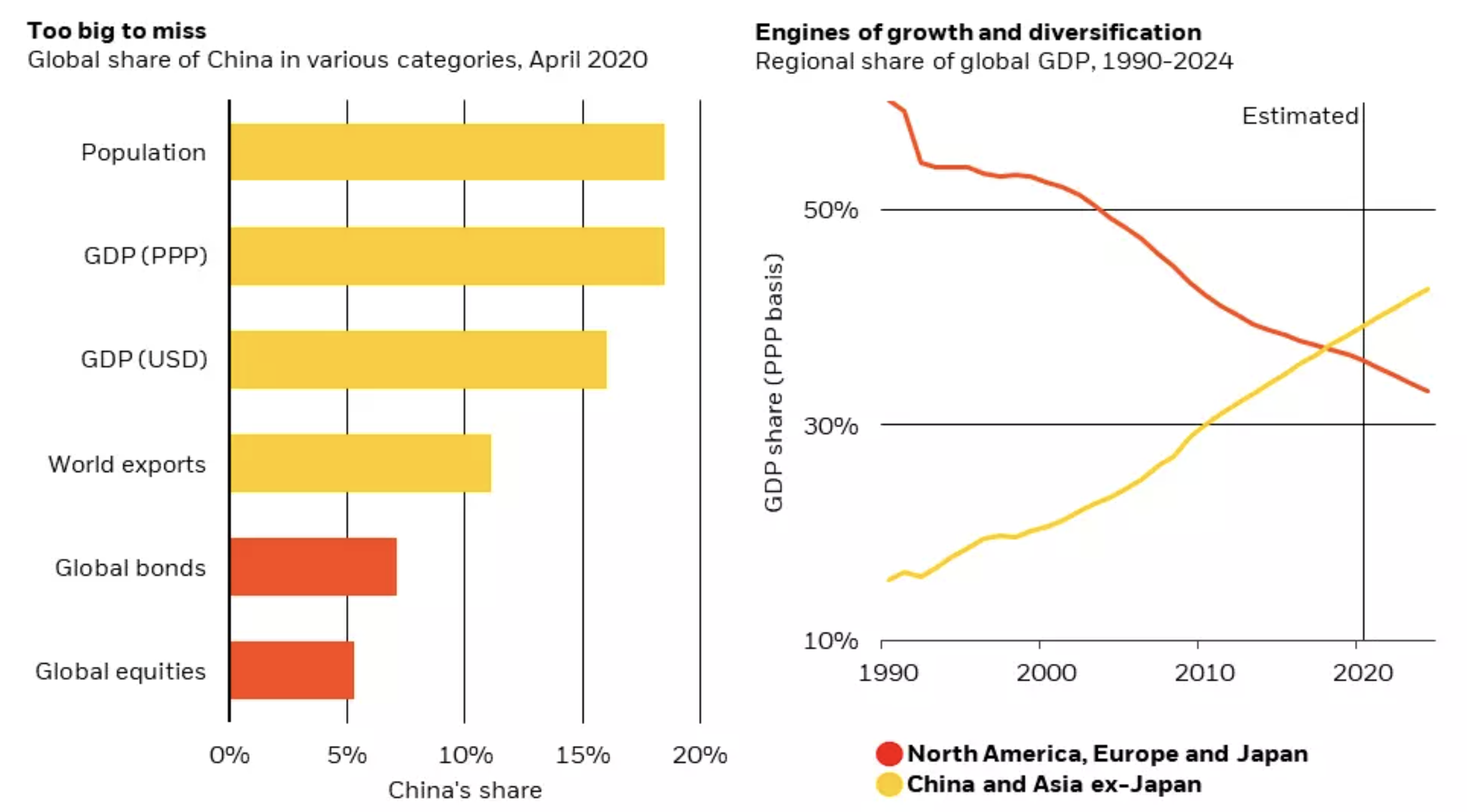

China’s presence on the global stage is becoming ever more prominent. We believe its representation in benchmark indexes is far below its economic and technological importance, as shown in the first chart. Trade volumes and direct investment inflows - both at record highs – show little sign of U.S.-China trade tensions impeding the country’s rise.

This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise - or even estimate - of future performance. Indexes are unmanaged and do not account for fees. It is not possible to invest directly in an index Sources: BlackRock Investment Institute and IMF, with data from Datastream Refinitiv, June 2020. Notes: The left chart show shows China’s representation across major macro and market metrics. We use the Bloomberg Barclays Global Aggregate Index and MSCI ACWI equity index as proxies for global bonds and equities respectively. The right chart shows each region’s combined share of global GDP on a purchasing power parity basis.

A nuanced picture

The path forward for U.S.-China relations may be more predictable under U.S. President Joe Biden’s administration compared with recent years. The U.S. and China have committed to working together to tackle climate change, suggesting some re-engagement on key global issues. Yet we believe the strategic rivalry between the two powers – across multiple dimensions – is likely to persist.

Economically, China has an ambition to double GDP by 2035 – surpassing the U.S. and firmly shifting the center of gravity for global growth to Asia in coming years. See the chart above on the right. China’s wide-ranging plans touch many flash points in the U.S.-China relationship, with the Covid pandemic amplifying each country’s focus on economic resilience. Secure supply chains and self- sufficiency in critical technologies and industries are a strategic priority and could drive a rewiring of global trade. Intensifying competition on key technologies, such as 5G and semiconductors, is one example.

What does “quality” entail? In the context of China’s growth outlook, we believe it covers at least three areas highlighted by President Xi Jinping in January 2017 at the World Economic Forum: the environment, economic wellbeing and stability of the financial system. In other words, China wants to become a more productive economy with each unit of incremental GDP generating proportionately less pollution, inequality and financial risk (debt).

We believe China will prioritize reforms that emphasize these goals as policymakers view them as mission-critical in achieving a more prosperous and powerful country.

Debt in perspective

Both the West and China are undergoing a policy revolution – one of our key themes since the Covid-19 shock struck. But crucially, these revolutions are very different. Western economies are blending large fiscal and monetary stimulus, with the hope that the scale of such policy support can help achieve societal aims beyond a narrow inflation goal.

In China, we believe the revolution is a sincere effort to move away from an overriding focus on the quantity of growth towards a greater focus on the quality of growth. Western governments have put in place a fiscal impulse many multiples of what was seen during the GFC even as the overall estimated economic loss from the Covid shock is expected to be a fraction. We believe China’s overall debt levels should be viewed in this context.

Politics versus markets

This publication is about China-related assets. We acknowledge it is often hard to separate politics from markets and believe this is partly why the Chinese risk premium – the compensation investors demand for holding Chinese assets – is elevated. Engagement enables investors to share expectations for companies in which they invest. In BlackRock’s case, our Investment Stewardship team engages with companies, including Chinese ones, to champion governance and sustainability goals outlined in our global engagement priorities.

Concerns around social and governance issues are likely to persist. Yet we believe it is important to distinguish between the state of play today versus the direction of travel and to engage with companies on sustainability goals.

Sustainability in focus

Sustainability will be a powerful driver of global returns in the medium term, in our view, and ever more central to all investment decisions. There are many aspects to sustainability – and the weight placed on each differs across investors. As a result, the overall assessment of China is investor specific. We consider both the current status as well as the direction of travel when it comes to assessing China’s sustainability credentials. We see improvement on several fronts – notably its environmental commitments – but recognize there is further to go, and commitments need to be realized.

Our asset return assumptions (CMAs) incorporate the impact of climate change on long-term asset returns. Popular wisdom has it that investing in China and being climate-friendly are at odds. We disagree. China’s commitment to a net- zero economy by 2060 was an important step – not just for its own economy, but for global progress toward climate goals. We believe China’s economy stands to benefit the most among major nations from a “green” transition to a more sustainable world, in our analysis, than a scenario of no climate action.

In our CMAs we focus on the E in ESG. Why?

- There is wide recognition of the importance of climate change for economic and social outcomes.

- There is consensus on the measurement of an entity’s contribution to climate change via carbon emissions.

These factors suggest climate change will be a driver of returns at the broad market level. See our paper Climate change: Turning investment risk into opportunity of February 2021 for more.

Our overweight to Chinese assets versus benchmark indexes does not change after taking into account the impact on climate change on expected returns. The composition of Chinese equity indexes is better aligned with the transition to a low-carbon economy, in our view. For instance, China’s industrial sector has around a 30% share of China GDP. Yet industrials only make up 5% of the MSCI China index, which has a higher concentration in the ‘greener’ sectors, such as consumer discretionary (34%) and consumer services (20%), according to a March 31, 2021 MSCI fact sheet.

We believe the need to gain exposure to the Chinese pole of growth in portfolios has only gotten stronger since we first wrote about our overweight stance in November 2019. The acceleration of structural trends and China’s resilience in the aftermath of the Covid shock has helped further crystalize our views on Chinese assets.

China’s fast-changing economy, relatively limited historical data and lower transparency than developed market peers prompt us to assume higher uncertainty around our median return assumptions. The risks to holding Chinese assets – such as the escalating tensions with the West – cannot be overlooked. Yet we expect investors to be compensated for these risks and uncertainty over a strategic horizon.

© BlackRock

Read more commentaries by BlackRock