Ethereum Miners Saw Record Revenues in May

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsI’ll keep it brief this week because I’m currently in Miami at the Bitcoin 2021 Conference with a world-class team of people representing HIVE Blockchain Technologies.

Tomorrow I will participate in a panel on running a publicly traded crypto-mining company. I look forward to sharing the stage with Kevin O’Leary, “Mr. Wonderful”; Jason Les, CEO of Riot Blockchain; and Fred Thiel, CEO of Marathon Digital.

Did you know that just two years ago in San Francisco, the Bitcoin conference attracted around 2,000 people? This year, an estimated 12,000 people are in attendance, a sign that Bitcoin and cryptos in general, have decidedly broken into the mainstream.

I’m sure I’ll have much to share with you next week, so stay tuned.

For the time being, sentiment has been very high among the conference’s attendees and speakers despite the recent negative headlines, including Bitcoin mining’s fossil fuel usage (more on that in a second) and crypto’s role in ransomware attacks.

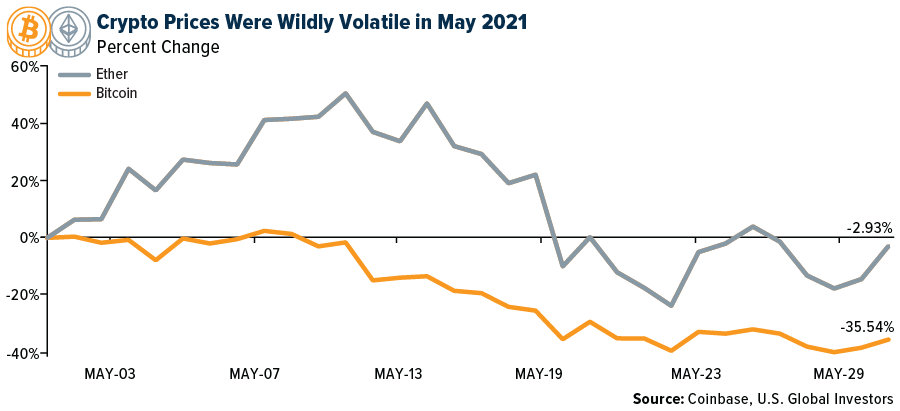

And then there’s last month’s price volatility. Bitcoin tumbled more than 35% in May, its worst month since November 2018, while Ether fell a moderate 2.9%. As a result, total market cap for all digital currencies lost more than $730 billion, decreasing from $2.2 trillion to $1.5 trillion.

This didn’t stop some crypto miners from raking in record revenues, though. According to data provided by The Block, mining revenue on the Ethereum blockchain topped $2.35 billion in May—a new all-time high—compared to $1.45 billion for Bitcoin. Transaction fees alone contributed over $1 billion.

HIVE a First Mover in Renewable Energy and ESG Strategy

The reason for the May crypto rout was two-fold. China announced it would begin banning financial institutions from providing services related to digital assets. And then Elon Musk tweeted that Tesla would stop accepting Bitcoin as a form of payment due to what he believes is an “increasing” amount of energy generated by fossil fuels for Bitcoin mining and transactions.

As I made clear soon after he made the announcement, I believe Musk is mistaken. Bitcoin mining is very much a part of the solution to curbing greenhouse gas emissions. It’s already been estimated that 76% of the global Bitcoin network uses green renewable energy. Another study finds that Bitcoin emits less than 5% of the emissions generated by the traditional financial sector. If Musk were so concerned about emissions, he would reconsider selling his electric vehicles in states that have the highest dependency on fossil fuels.

That said, I was honored to participate on behalf of HIVE Blockchain on the recent call with Musk, my fellow North American crypto miner executives and MicroStrategy co-founder Michael Saylor, who organized the call. From the very start, HIVE has mined both Bitcoin and Ether using only 100% renewable energy. It’s also the first publicly traded miner to have an ESG (environmental, social and corporate governance) strategy.

Air Passenger Traffic Up 100% from the Beginning of the Year

Traveling to Miami marked only the third time I’ve flown commercial in about a year and a half, a huge departure from my globetrotting before the pandemic. Like my other two experiences, the flight was pleasant and comfortable, and I felt at ease that airports were taking every precaution to ensure travelers’ safety.

I should add, though, that there were comparatively many more people catching flights this time around.

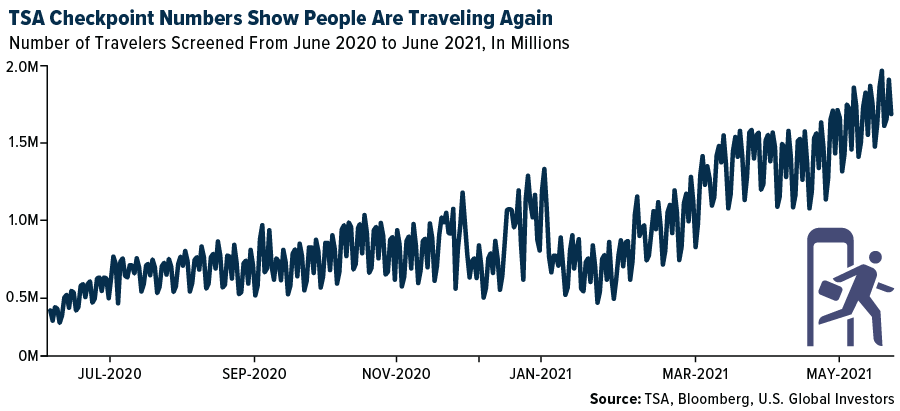

On the day I left for Miami, a total of 1.6 million passengers were screened at U.S. airports, according to Transportation Security Administration (TSA) data. That’s up nearly 100% from the passenger count at the start of 2021, and up 420% from 12 months ago.

This improvement is due in large part to the growing number of Americans who have been vaccinated against COVID-19. As of June 1, over half of all U.S. adults were either fully or partially vaccinated, putting the U.S. well ahead of other developed and emerging countries.

This week, in fact, new coronavirus cases hit their lowest point in the U.S. since the pandemic began in March 2020. Axios reports that cases are now so low, and the virus so well contained, that it will stop providing weekly updates on new infections for the first time in 56 weeks.

This is hugely constructive for the domestic travel industry in general and airlines in particular, and I’m optimistic that a full recovery will come much faster than initially anticipated.

Europe Is the Next Leg in the Travel Recovery Story

I expect the next major recovery story to be Europe, which is still lagging behind the U.S. in terms of vaccination rates but accelerating. This week, Eurocontrol, a trade organization that supports European aviation, released updated air travel forecasts for the remainder of 2021, and the scenarios are encouraging.

In May, air traffic in Europe was only 39% of what it was in the same month in 2019. That doesn’t sound great, but if vaccine rollout continues at a rapid clip this year, traffic by December 2021 could be close to 80% of the baseline 2019 numbers, according to Scenario 1. (By comparison, traffic in the U.S. is currently at 67%.) Scenario 2 predicts 70% capacity by December if vaccinations are stretched out to the first quarter of 2022. Call me overly optimistic, but I don’t see Scenario 3 happening, which envisions “persistent restrictions,” “patchy vaccine uptakes” and “renewed outbreaks.”

90 New Airlines to Launch this Year

You may say I have an optimism bias, but business leaders in commercial aviation seem to agree with me. More than 90 new airlines are set to launch in 2021, in North America, South America, Europe, Asia and Africa. Here in the U.S., two have already taken their inaugural flights: Avelo Airlines on April 28, from Burbank to Santa Rosa, California; and Breeze Airways on May 27, from Tampa, Florida, to Charleston, South Carolina. Breeze is the fifth airline founded by serial entrepreneur David Neeleman, who also founded Morris Air (purchased by Southwest in 1993), WestJet, JetBlue and Azul Brazilian Airlines.

We’ve also seen two U.S.-based airlines go public this year: Sun Country on March 17, Frontier on April 1.

This tells me there’s massive pent-up demand by consumers and investors alike that airlines are scrambling to capitalize on. I believe it’s not only a great time to fly but also to invest.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.66%. The S&P 500 Stock Index rose 0.61%, while the Nasdaq Composite climbed 0.48%. The Russell 2000 small capitalization index gained 0.77% this week.

- The Hang Seng Composite lost 0.24% this week; while Taiwan was up 1.64% and the KOSPI rose 1.61%.

- The 10-year Treasury bond yield fell 3 basis points to 1.558%.

Airline Sector

Strengths

- The best performing airline stock for the week was Avianca, up 13.3%. TSA checkpoint numbers hit record highs since the pandemic started, showing people are more comfortable traveling again. Last Monday, the number of people screened was down by only 10% versus 2019 levels, and by last Thursday 1.85 million people passed through TSA checkpoint. The encouraging numbers come despite limited long-haul international and corporate travel. TSA data continues to trend positively in North America which should bode well going into the summer travel season. In addition, Stifel’s proprietary airline demand model suggests that retail demand is 80-85% recovered compared to pre-pandemic levels.

- The coronavirus had a major impact on passenger aircraft worldwide being parked, but now the stored fleet of global airlines continues to decline, currently at 7,448 aircraft parked, or 28.1% of the global fleet (versus 29.4% in mid-May). All regions have seen declines in storage rates since mid-May, with Europe particularly better (down 3.7%).

- United Airlines has yields on tickets issued (since early May) consistent with those in 2019, with domestic leisure yields exceeding these levels. The airline noted that while business travel remains depressed, improved demand and higher ticket yields could nudge them into a third quarter profit, reports TheStreet. United cites tight supply (aircraft are not being brought back fast enough) and demand as the main reason.

Weaknesses

- The worst performing airline stock for the week was Copa Airlines, down 7.9%. Wizz Air will report fiscal year 2021 (FY21) results soon, which unfortunately are expected to be poor. The company has guided for a FY21 reported net loss of 570-590 million euros. Reported capacity is down 74% for the airline as well, compared to 2019 levels. On a positive note, bookings are increasing and are now at 70% of 2019 levels, which is a sign of hope looking forward.

- Corporate and international bookings continue to be weak compared to leisure and domestic bookings. In fact, tickets booked through corporate channels are down 58.1% versus 2019 levels and international travel is down 34.8% versus 2019 levels. The re-opening of borders continues to be a slow process and we likely will not witness meaningful transatlantic travel until the second half of the summer.

- U.S. to Atlantic and U.S. to Pacific travel remains depressed. U.S. to Atlantic capacity is down 67% in the second quarter of 2021 versus 2019 levels, and U.S. to Pacific capacity is down 77% in the second quarter of 2021 versus 2019 levels. U.S. to China capacity is down 96% in the second quarter of 2021 versus 2019 levels.

Opportunities

- U.S. airlines continue to ramp up capacity in anticipation of strong air travel recovery. In the third quarter, domestic capacity should be down 2% versus 2019, an improvement from down 20% in the second quarter of 2021. Many U.S. carriers are anticipating a strong holiday season this year with current fourth-quarter capacity tracking down 1%.

- Management at Allegiant, which is 100% exposed to leisure and domestic travel, is very bullish on its prospects. The company stated that yields in April and May were greater than in 2019. Along with strong bookings, management believes Allegiant will be earnings per share (EPS) positive in the second half of this year. They also indicated they are on track to earn $2.00 of EPS.

- Pension reform has a significant impact on airlines. Under the Pension Protection Act of 2006, airlines were able to use a grandfathered 8.85% discount rate to determine actual cash liabilities. Recently passed legislation now sets a 5% floor on the discount rate, which has a significant impact on a company’s pension liability. Delta Air Lines will no longer need to make $500 million to $1 billion annual contributions to its plans. The plan should be close to fully funded after this year’s planned contributions.

Threats

- The closure on non-essential travel and 14-day quarantine requirements between Canada and the U.S. was extended last week to at least June 21, with Canada's Prime Minister suggesting the border would remain closed until 75% of its population is vaccinated. Canada's vaccine rollout has been slower than that of the U.S., with only 5.5% of its population currently fully vaccinated.

- Delta Air Lines recently shared data on the spread of COVID-19, particularly when it comes to catching it while on a flight. According to the airline’s statistics, there is a 1/10,000 chance of sitting on a plane next to someone that is infected/infectious and somewhere between a 1/1,000,000 and 1/5,000,000 chance of contracting it while aboard a plane. Ultimately, Delta believes we could see the mask mandate lifted sometime in the summer or in late fall, at least domestically. Electrostatic spraying is no longer performed after every flight and has moved to an end-of-day procedure following studies that concluded the process was not required intra-day.

- More news from Delta; the airline expects Asia to be the slowest market to reopen and expects the corporate rebound to outpace that of leisure. The major carrier indicated that cultural and business norms, unique to Asia, are particularly ill-suited to Zoom-type substitutes (tough to exchange business cards and determine “who is the most senior executive in the room”). Furthermore, in several business settings, an interpreter is required.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 4.4%. The best performing country in Asia this week was Indonesia, gaining 3.7%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 0.52%. The Indonesian rupiah was the best performing currency in Asia this week, gaining 0.32%.

- Global Manufacturing PMI is improving, rising to 56 in May from 55.9 in April. PMIs in the Eurozone strengthened as well, pointing to continued economic recovery. The Eurozone’s Service PMI was reported at 55.2, Manufacturing PMI improved to 63.1 and Composite PMI rose to 57.1.

Weaknesses

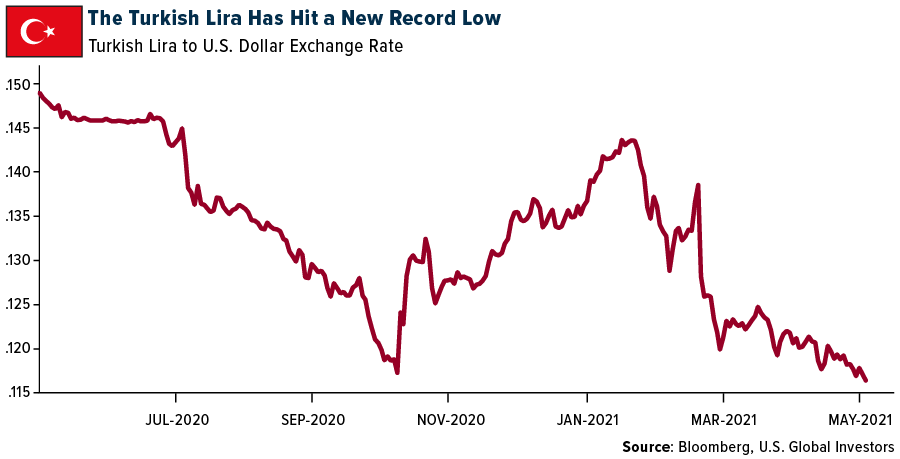

- The worst relative performing country in emerging Europe for the week was Turkey, gaining 0.76%. The worst performing country in Asia this week was Malaysia, losing 1%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 1.3%. The Indian rupee was the worst performing currency in Asia, losing 0.61%.

- The Caixin China Manufacturing PMI was reported slightly higher, at 52 in May versus 51.9 in April. However, the Caixin China Service PMI weakened to 55.1 in May from 56.3 the previous month, causing the composite PMI to decline to 53.8 in May from 54.7 in April.

Opportunities

- Barron’s says it’s time for investors to buy European stocks over Unites States equites. Analysts forecast STOXX 600 companies to have good earnings, posting possible gains of 12% in 2022. Moreover, European equities are less expensive than their U.S. counterparts. Barron’s also pointed out that European stocks are paying higher dividends. In fact, the STOXX 600 is yielding 5.4%, much more than the S&P 500 at 1.5%. In emerging Europe, Russia and Romania offer even higher rates than the STOXX 600.

- The Presidents of Belarus and Russia met last weekend near Sochi. Vladimir Putin once again showed his support for the President of Belarus, Lukashenko. Russia offered a second loan installment to Belarus in the amount of $1.5 billion despite recent global criticism for Belarus diverting a Ryanair plane to Minks and arresting a journalist aboard who is critical of the country’s leader.

- On Monday, China changed its two-child policy limit per family. The country will now allow three children going forward per family. The government may also announce special monetary payments to encourage parents to have more children. China scrapped the one-child policy in 2016, which resulted in more births.

Threats

- The Turkish lira is the world’s worst performing currency year-to-data and it may continue to weaken further. Turkey’s president once again called for lower interest rates, putting pressure on the central bank governor to ease policy despite high inflation. Erdogan believes that cutting rates will lower producers’ costs and will eventually result in slower increases in consumer prices.

- Russia has warned that its economy is overheating, with annual inflation currently at 5.9%, said Anton Siluanov, the country’s finance minister. The next central bank meeting is scheduled for June 11 and speculations are mounting that Russia may hike again, this time by 50 basis points. The Russian economy shrank nearly 3% in 2020 due to the pandemic, causing the worst contraction in 11 years. The central bank noted that the economy continues to recover and gross domestic product should reach its pre-pandemic level in mid-2021.

- The U.S. has amended its Chinese blacklist. The list will contain 59 companies with ties to China’s military or surveillance industry. Many of the companies in President Biden’s order were already on Trump’s administration list, including the nation’s largest telecommunications companies: China Mobil Communications Group Co., China Unicom Ltd. and China Telecommunications Corp. The list has room to be extended, too. The new ban will become effective August 2 and investors will have one year to divest. Our mutual fund that invests in the China region does not hold any of the 59 companies.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was iron ore, up 11.33%. Iron ore futures rallied this week as China mulled production restrictions at a time when it is pushing forward with its green ambitions and is trying to crack down on surging commodity prices.

- U.S. shale oil producers have been able to reduce their costs by 17% in the last two years, with the median cost declining from $30.80 per barrel in the first quarter of 2019 to $25.60 in the first quarter of 2021. The biggest contributor to this decline was the drop in depreciation, depletion and amortization expenses (DD&A), with shale operators’ DD&A falling by $2.60 per barrel in the last two years. This decline, which is responsible for 50% of the total drop in unit costs, can be attributed to the industry’s increasing efficiencies in capital deployment, with companies drilling and completing wells faster and at lower costs.

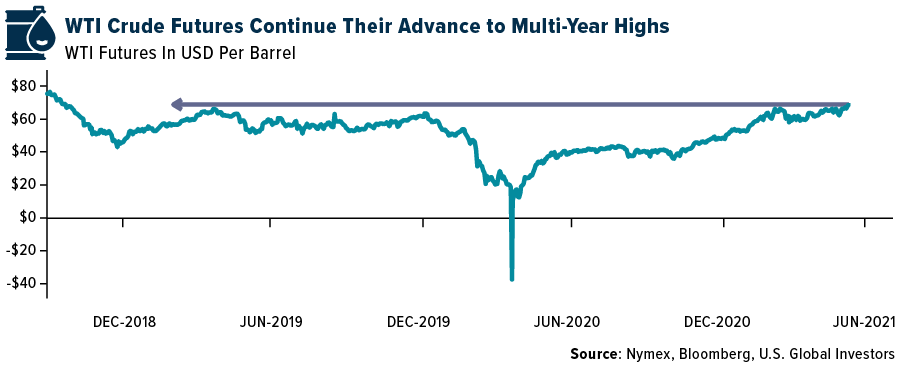

- West Texas Intermediate (WTI) crude futures rallied to the highest in over 2.5 years after forecasts from the Organization of Petroleum Exporting Countries and its allies (OPEC+) suggested that the global market may see tight supplies, with efforts to revive of a nuclear deal with Iran still underway. WTI rose to $69.76 per barrel on Friday, while Brent crude crossing above $72 per barrel. An OPEC+ committee reported that oil stockpiles across are rapidly depleting, and demand has started to pick up in the U.S. and Europe, although the COVID-19 pandemic is still raging in countries like India and Brazil. Chairman of Facts Global Energy (FGE) consultants said in an interview that if Iranian oil does not enter the market, prices could hit $75-$80 per barrel by the third quarter of 2021.

Weaknesses

- The worst performing commodity for the week was tin, down 3.65%. Tin rallied to the highest levels in a decade right before the rally cooled down as investors and traders took profits, leading to an increase in inventories at the London Metals Exchange.

- The largest meat producer in the world, JBS SA, fell victim to a cyberattack which forced the company to shutdown some of its largest slaughterhouses. The Sao Paulo-based JBS halted processing at five of its biggest beef plants in the U.S., leading to a 20% drop in total U.S. production. Moreover, the Brazilian company had to halt operations at its slaughterhouses in Australia and Canada as well. The ransomware attack, which took place on May 30, forced JBS to suspend its North American and Australian computer systems, and in the last year, over 40 food processing companies have reported some sort of ransomware attack. JBS accounts for 23% of U.S. beef production capacity and roughly a fifth of the nation’s pork capacity.

- Engine No. 1, the activist investor that won two seats on Exxon Mobil’s board, is expected to win a third seat, with private equity investor Alexander Karsner being elected to Exxon’s 12-member board. This victory for Engine No. 1 after a months-long proxy fight could be a massive blow CEO Darren Woods’ ambition for Exxon. Woods told shareholders in May that voting for Engine No. 1’s nominees would derail the oil giant’s progress and jeopardize their dividends. Investors have been dissatisfied with Exxon due to the company’s financial performance and its refusal to commit to targets to zero out emissions.

Opportunities

- MMC Norilsk Nickel (Nornickel), the Russia-based miner, which is the world’s largest producer of refined nickel, announced its plans to offer carbon-neutral nickel this year amidst an increase in the metal’s demand. The company’s senior vice president, Sergey Dubovitsky, said that the carbon-neutral nickel project will allow them to test the market and understand the depth of demand for such a product, and added that the carbon neutrality will be achieved by investments in measures such as replacing power station equipment and increasing efficiency of their electricity consumption. He also mentioned that the company will provide verification from independent international auditors regarding the nickel’s carbon-neutral credentials. Regarding output of the project, Dubovitsky said that Nornickel may produce 10,000 tons of “green” nickel in 2021 and cut its CO2 emissions by 70,000 tons.

- OX2 AB, the Sweden-based wind energy farm developer, is set to raise $400 million in an initial public offering to fund its expansion into wind parks at sea and solar power. The company’s CEO said that OX2, which is one of the biggest builders of onshore wind parks in Europe, will debut on the Nasdaq First North Premier Growth Market in the next few months, and has set the target to install projects with a combined capacity of 2 gigawatts starting in 2024. The plans include their first offshore wind park in the Baltic Sea and solar facilities in Italy, Poland, and France. The CEO added that the company will look into entering U.S., Australia and southeast Asia to capitalize on opportunities in the longer term. Currently, OX2 generates 17 gigawatts of electricity annually from its green energy portfolio.

- Kayrros SAS, a private French company that tracks emissions from the oil and gas industry, has seen growing demand as governments and fossil fuel producers increase their efforts to fight climate change and commit to zero emissions goals. The company’s President, Antoine Rostand, said that Kayrros is planning on raising funds to accelerate its growth into countries like Germany and Japan and that an initial public offering may follow in the next three to five years. Founded in 2016, the company has already raised $48 million and has invested in monitoring technologies that use satellites to measure emissions of the most harmful greenhouse gases and now possesses the ability to detail emissions by company and region. Rostand added that Kayrros’s technology can also help governments of European nations to track CO2 content of imported products as the region mulls levying a carbon border tax.

Threats

- The United Nations (UN) Food and Agriculture Organization (FAO) reported that its gauge of world food costs has climbed for a 12th straight month in May, recording its longest stretch in a decade. As a result, there are growing concerns regarding acceleration in broader inflation, which could complicate central banks’ efforts to provide stimulus to economies struggling to recover from the COVID-19 pandemic. To exacerbate the issues, droughts in key Brazilian agriculture hubs are crippling crops from corn to coffee, while vegetable oil production has tempered down in Southeast Asia. These issues have boosted costs for livestock producers and risk straining global grain stockpiles which have been depleted by soaring demand from China. The UN index for staple commodities has reached its highest levels since September 2011, with May’s gain of 4.8% being the biggest in more than 10 years.

- The world’s largest petrostates are rejecting the International Energy Agency’s (IEA) road map to reach net-zero carbon emissions by 2050, which called for no new investments in new fields. The Russian Deputy Prime Minister and energy ministers of Qatar and Saudi Arabia voiced their concerns regarding the accelerated shift to green energy, stating that if investments are halted, oil and gas prices would skyrocket and cause significant disruptions in the markets. They also added that they plan on expanding their oil and gas facilities. These comments showcase the massive disconnect between the world’s current fossil fuel-heavy energy system and the changes needed to prevent damaging climate change.

- Reports from the U.S. Drought Monitor suggests that nearly three-fourths of the western U.S. is under a severe drought warning, likes of which have never been recorded in the 20-year history of the U.S. Drought Monitor. A meteorologist with the U.S. Department of Agriculture said that the mountains across the west have not received enough precipitation, depriving reservoirs of much needed snowmelt and rain. Further, the dry conditions elevate the threat of wildfires and farmers are struggling to irrigate their crops. According to the U.S. National Centers for Environmental Information, the drought in 2020 cost the nation $4.5 billion and this year the costs could be higher. Elizabeth Klein, a senior counselor for the Department of Interior, mentioned at a Congressional hearing that California is experiencing its third-driest year on record and the driest year since 1977.

Domestic Economy and Equities

Strengths

- Markit PMIs continue to improve. Final Manufacturing PMI for May was reported at 62.1 versus the prior reading of 61.5. The Markit Service PMI increased to 70.4 from 70.1. Composite PMI stands now at 68.7, pointing to a strong economic recovery supported by massive fiscal and monetary stimulus.

- The U.S. unemployment rate fell to 5.8% in May from 6.1% in April. It is the lowest jobless rate since March 2020, when it stood at 4.4%. Leisure and hospitality companies led the gains, with 292,000 new jobs. The education sector added 140,000 jobs as schools returned to in-person learning. Employers in health care and social assistance added 46,000 jobs, while manufacturing, wholesale trade, transportation and warehouses gained about 20,000 jobs each.

- Devon Energy, an oil and gas exploration and production company, was the best performing S&P 500 stock for the week, increasing 20%. Shares gained following brokers’ recommendations to buy along with revising up the stock’s price target.

Weaknesses

- Nonfarm payrolls increased in May but missed expectations. U.S. employers added 559,000 jobs last month, the Labor Department reported Friday, up from a revised 278,000 jobs in April. May’s number came in below the expected 675,000 jobs to be added.

- On Thursday, the White House warned corporate executives and business leaders to step up security measures to protect against ransomware attacks. There has been a significant hike in the frequency and size of cyber-attacks, including the recent instance that disrupted operations at the biggest U.S. fuel pipeline.

- Darden Restaurants Inc. was the worst performing S&P 500 stock for the week, losing 6.34%. Restaurants may benefit from further economic reopening but this week shares of Darden recorded net outflows on no specific negative news. The company announced that will release first-quarter results on June 24.

Opportunities

- Nominal gross domestic product (GDP) in the first quarter increased at an 11% quarter-over-quarter annual rate. Ed Hyman from Evercore ISI estimates that nominal GDP in the second quarter will reach 15.3%. Over that past two quarters, nominal GDP growth has averaged +13.1%, the highest level since the first quarter of 1981, when bond yields where 13% and Fed funds were at 15%, Hyman explained.

- Bankruptcy filings in May declined after a two-month spike in March and April. New filings for May dropped to 34,734 across all chapters. This represents a 15% drop from the April 2021 new filings count of 40,913. Non-commercial consumer filings across all chapters totaled 32,958, down 15% from 38,830 in April.

- President Biden offered to create a new tax floor of 15% rather than raising the corporate tax rate to 28% in his latest $1 trillion infrastructure proposal to Republicans. The White House says it wants a deal by June 7 to keep open the possibility of Biden signing a bill this summer.

Threats

- The Finance Minister of Russia announced that the country will eliminate the dollar from its National Wellbeing Fund, shifting to euros, yuan and gold, instead. The wealth fund currently holds 35% of its liquid assets in dollars, worth about $41.5 billion, with the same amount in euros and the rest spread across yuan, gold, yen and pound. After the change, the fund’s assets will be held 40% in euros, 30% in yuan, 20% in gold and 5% each in yen and pound.

- Mortgage rates continue to stay at record-low territory. Favorable rates, increasing employment and an improving economy will keep pushing home prices higher, making it harder for buyers for find affordable properties. In April 2021, the median home listing price reached an all-time high of $375,000, up 17.2% compared to last year.

- The Federal Reserve may start pushing forward with the idea of removing some stimulus measures and beginning to hike rates in the summer. Bond yields could increase as the Fed starts to taper.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Curve DAO Token, rising 40.47%.

- Kraken Cryptocurrency Exchange launched its mobile application in the U.S. this week, after launching in Europe earlier this year. The San Francisco-based company announced that it will allow U.S. customers to trade more than 50 tokens on its platform but will not be available to customers in Washington state or New York, citing the costs of maintaining regulatory compliance. Kraken also announced that it is planning to go public in 2022, following Coinbase’s suit, and is in talks to raise a new funding round which is expected to give way to a valuation of $20 billion.

- The rally of CME Ether futures has outpaced that of CME Bitcoin futures since mid-April. Ether futures began trading on February 8, 2021, and have risen 46% since that time, while Bitcoin futures have dropped around 20% during the same period. The chart below compares the return one could potentially generate by investing $100 into either Ether or Bitcoin futures, with the former picking up pace over the last 1.5 months.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was BakeryToken, down 18.78%.

- Hamas, the Palestinian militant group that is considered a terrorist organization by a majority of the western world, has seen a sudden increase in Bitcoin donations since the start of conflicts with Israel in early May. An unidentified Hamas official told the Wall Street Journal that donations in Bitcoin have increased in proportion to the overall donations, while withholding the actual amount that the organization has received in Bitcoin. An Israeli blockchain analytics firm, Whitestream, identified the association between Hamas and Bitcoin in February 2019.

- The non-fungible token (NFT) market has seen a more rapid decline than the wider cryptocurrency markets, with sales of NFTs dipping 90% since the peak in early May. During the last week, just $19 million worth of NFTs were sold, down from over $170 million during the seven-day window on either side of the cryptocurrency market top, which occurred on May 12. Protos, a cryptocurrency company that provides asset management services and analytics, reported that the number of NFT wallets showing any activity has dropped 70% since early May, adding that the NFT bubble has already burst.

Opportunities

- ETC Group, which is a specialist provider of digital asset-backed securities, announced this week that it is going to launch the first Bitcoin exchange-traded product (ETP) in the U.K., on the Aquis Exchange Multilateral Trading Facility (MTF) in London. Starting on June 7, trading of the ETP will take place in four different currencies: British pound, euro, U.S. dollar, and Swiss franc. Additionally, the ETC Group also listed two exchange-traded commodities that are physically backed by Bitcoin and Ethereum, the BTCetc and ETHetc, on the Euronext stock exchanges in Paris and Amsterdam.

- Anchorage Digital, the FDIC-insured crypto custody bank, is set to expand its lending services by partnering with Massachusetts-based BankProv to extend Ethereum-backed loans to its clients. Currently, Anchorage provides Bitcoin-backed loans through capital providers like Silvergate Bank. Anchorage’s co-founder, Diogo Mónica, talking about the new offering mentioned that the bank’s clients are struggling to find liquidity on their Ethereum assets as no one extends them credit on such assets.

- FTX Trading, the cryptocurrency derivatives exchange, announced the launch of its two new perpetual futures products based on MV Index Solutions GmbH (MVIS) indices, which is a subsidiary of VanEck Global. Market data provider CryptoCompare and MVIS said that the MVIS CryptoCompare Digital Assets 10 Index and the MVIS CryptoCompare Digital Assets 25 Index, which will trade under the tickers “MVDA10” and “MVDA25” respectively, are market capitalization-weighted indices of 10 and 25 of the most liquid digital assets. Both the products will be calculated in U.S. dollars as a price index and rebalanced monthly.

Threats

- The governor of the Reserve Bank of India (RBI) said that the central bank is still critical of cryptocurrencies after it withdrew a 2018 circular which stated that banks in the country cannot deal with individuals or businesses that deal with cryptocurrencies. India’s Supreme Court said in a ruling in March 2020 that the ban on cryptocurrencies should be reversed, and commercial banks continued citing the 2018 circular as the reason for refusing to service crypto businesses. The RBI has been a critic of cryptocurrencies due to their potential of causing financial instability and for facilitating money laundering, and the governor has voiced those concerns to lawmakers in the Indian government.

- Decentralized Finance (DeFi) protocol Belt Finance on the Binance Smart Chain (BSC) was the latest victim of an exploit that resulted in a loss of $6 million. This hack comes a week after the decentralized exchange BurgerSwap was attacked, resulting in the loss of $7.2 million. Developers of other protocols on the BSC analyzed the attack and described it as one of the more complex hacks as the hacker exploited Belt’s yield generation strategy. Since launching in September 2020, seven different protocols have been attacked on the BSC. There are growing concerns regarding the safety of BSC as the total digital assets locked on various DeFi protocols on the BSC has reached $44.25 billion and could cause significant financial harm if the exploits keep occurring.

- U.K.’s Financial Conduct Authority (FCA) reported that as many as 50 firms in the country that deal with cryptocurrencies could be forced to shut down operations as they are failing to meet FCA’s anti-money laundering (AML) rules. FCA postponed its deadline for crypto businesses to register under the U.K. regulator’s Temporary Registrations Regime (TRR) from July 9, 2021, to March 31, 2022. Currently, only five crypto-related firms have been added to the FCA’s formal register and 90 firms have their application pending.

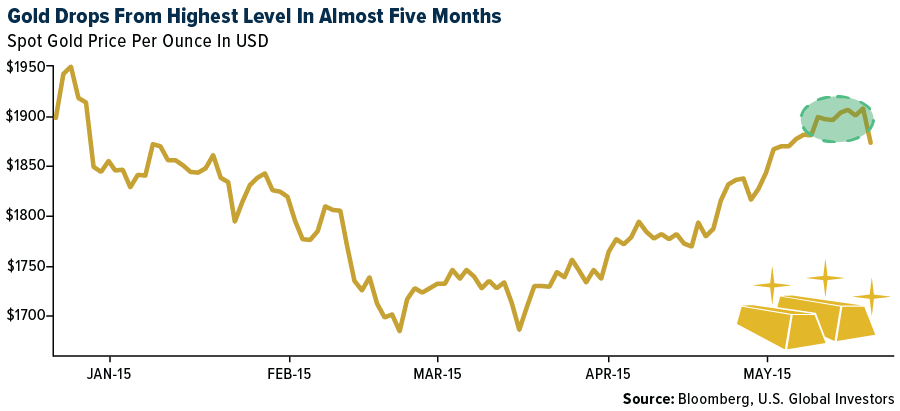

Gold Market

This week spot gold closed the week at $1,891.59, down $12.18 per ounce, or 0.64%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.91%. The S&P/TSX Venture Index came in up 1.21%. The U.S. Trade-Weighted Dollar rose 0.11%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-31 | Germany CPI YoY | 2.3% | 2.5% | 2.0% |

| May-31 | Caixin China PMI Mfg | 52.0 | 52.0 | 51.9 |

| Jun-1 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.7% |

| Jun-1 | ISM Manufacturing | 61.0 | 61.2 | 60.7 |

| Jun-3 | Initial Jobless Claims | 387k | 385k | 405k |

| Jun-4 | Change in Nonfarm Payrolls | 675k | 559k | 278k |

| Jun-4 | Durable Goods Orders | -1.3% | -1.3% | -1.3% |

| Jun-8 | Germany ZEW Survey Expectations | 86.0 | -- | 84.4 |

| Jun-8 | Germany ZEW Current Situation | -27.5 | -- | -40.1 |

| Jun-10 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Jun-10 | CPI YoY | 4.7% | -- | 4.2% |

| Jun-10 | Initial Jobless Claims | 375k | -- | 385k |

Strengths

- The best performing precious metal for the week was palladium, up 0.73% on expectations of strong automobile production, perhaps tempered by the chip shortage. Palladium supply, however, has been restrained by flooding at one mine in Russia. Sibanye Stillwater may buy back about 9.6 billion rand ($700 million) of its shares. The company will repurchase as many as 147.7 million shares, or 5% of its total, which will be implemented between June 2 and April 6 of 2022.

- Dundee Precious Metals announced a plan of arrangement to acquire INV Metals at a 63% premium to the five-day average price. The all-share transaction values INV at C$132 million given the 0.091 share exchange ratio. The deal will also allow for a much lower cost of capital (internally generated or raised in the market) to fund the Loma Larga project.

- Russian miner Nord Gold Plc announced plans to hold an initial public offering (IPO) in London. The company, known as Nordgold, expects to have a free float of at least 25%, and plans a secondary listing in Moscow. Nordgold said an IPO would widen its options for raising capital and help the company to retain key managers.

Weaknesses

- The worst performing precious metal for the week was platinum, down 1.28% despite speculators boosting their net-lot positions in the past week. Gold slipped from the highest level in almost five months as strong economic data from the U.S. diminished demand for haven assets. Data released showed a gauge of U.S. manufacturing quickened in May, propelled by stronger growth in orders. That boosted yields on 10-year Treasuries, which weighed on demand for non-interest-bearing bullion. However, U.S. payrolls were weaker than expected on Friday, letting gold close out the week on a positive note. The Perth Mint says gold coin and minted bar sales totaled 91,146 ounces last month, according to figures on its website. Sales compare with 101,379 ounces in April, according to previously released data.

- On May 31, Centerra announced that it has commenced a filing under Chapter 11 of the U.S. Bankruptcy Code for its subsidiaries Kumtor Gold Company (KGC) and Kumtor Operating Company (KOC). This is intended to provide a worldwide automatic stay of all claims against KGC and KOC, and presumably to prevent the Kyrgyz Government from stripping KGC of its assets and disposing of the Kumtor mine. According to Centerra, the government intends to use environmental and tax claims to place KGC into insolvency proceeding and then potentially strip KGC of its assets.

- Nevada lawmakers voted to reform how the state taxes the mining industry, passing a measure that will effectively double the amount of taxes imposed on silver and gold mines. The bill will preserve the state's Net Proceeds on Minerals tax structure, which requires mining businesses be taxed at less than 5% of what are called net proceeds — profit minus deductions for certain costs. It will add an excise tax of 0.75% on mines that report gross revenue of $20 million to $150 million and 1.1% on mines that report any higher gross revenue. It has been signed by the Governor.

Opportunities

- Precious metal mining companies that are developing and exploring new projects have the best return potential among peers, according to a report by RBC. The group sees value among mid-cap precious metal miners as stocks lagged their large-cap peers. The spread in valuation for intermediates has widened to a 40% discount, 10% higher versus the historical average despite better growth, yields and leverage to metal prices.

- Newcore Gold released more drilling results from the Boin deposit that add grade accretive ounces to the Boin resource. Drilling hit 0.90 grams per ton silver. This hole was from the south end of the Boin pit shell. The current Boin pit grades are 0.84 grams per ton, so this is immediately accretive to grade. Boin is the second largest deposit and accounts for 44% of the total resource ounces.

- Russia announced it will eliminate the dollar from its oil fund to reduce its vulnerability to Western Sanctions. The news comes just weeks before Putin and President Biden are scheduled to meet at an upcoming summit. Finance Minister Anton Siluanov noted that the dollar holdings will now be shifted to euros, yuan and gold.

Threats

- Newmont’s CEO admitted that it is hard to find talent in the mining and metals industry right now. Competition with remote work along with an increased role of technology is presenting challenges across the board.

- The global chip shortage has had “quite a significant” impact on platinum and palladium demand in the automobile industry, according to Suki Cooper, a precious metals analyst at Standard Chartered Bank. “We were expecting a strong recovery across auto production to lift demand for both platinum and palladium, but because of the chip shortages, recent estimates look like they’ll reduce auto production by about 2 to 3 million units in the second half of the year.”

- Many ETFs continue to sell their gold holdings, cutting 196,113 troy ounces of gold in the last trading session, bringing this year's net sales to 6.05 million ounces. Total gold held by ETFs has fallen 5.6% this year to 101 million ounces.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All