3Q 2021 OUTLOOK

Membership required

Membership is now required to use this feature. To learn more:

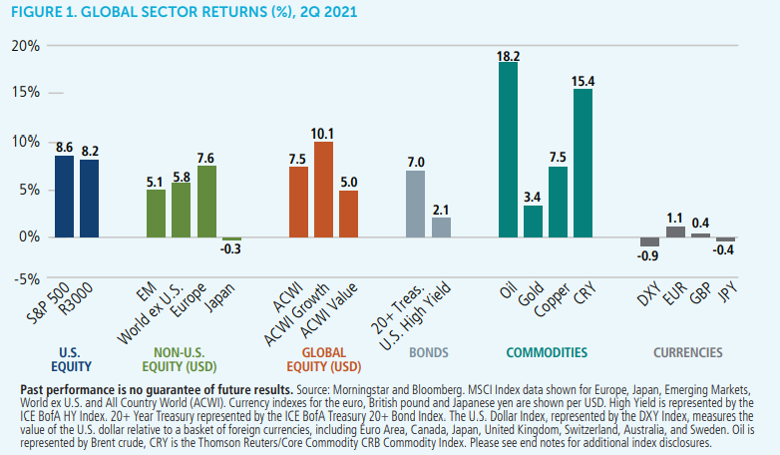

View Membership BenefitsDuring the second quarter, global equity markets extended their strong performance. The MSCI ACWI returned 7.5%, bringing its year-to-date return to 12.7%. Under the surface, markets remained highly rotational from regional, sector, and factor perspectives.

In our April outlook, we noted the first quarter outperformance of U.S. equities was driven initially by strength in large-cap growth names, but the market shifted its focus toward Covid vaccination rates as the quarter concluded. Against this backdrop, cyclicals and Covid-reopening beneficiaries led the markets higher. Heading into the second quarter, our view was that the acceleration of vaccination rates throughout Europe would likely support a shift in leadership to European cyclicals and Covid-reopening beneficiaries. This indeed was the case in April and May, as European equities returned 9.5% and outpaced the MSCI ACWI’s gain of 6.0%. Unfortunately, many countries have delayed reopening because of the threat of the Covid Delta variant and the reduced efficacy of the nonmRNA vaccines that have been more prevalent overseas. For example, China intends to keep its pandemic border restrictions in place for at least another year to mitigate the risk of disrupting the 2022 Winter Olympics and the Chinese Communist Party Congress. Japan has banned spectators at the Toyoko Olympics. Meanwhile, the U.S. has benefited from its early lead in vaccinations, with economic reopening proceeding at a brisk pace, although Delta variant cases are now rising in the U.S. as well.

In addition to ongoing concerns about Covid, market participants have become less certain about the firmness of monetary policy support, specifically the Federal Reserve’s commitment to its new policy framework. As expected, inflation data has accelerated sharply, and there is much debate as to whether this is a temporary spike due to low base effects or whether we are in the early stages of a more durable shift upward. The Fed has been clear that it views the current inflation readings as “transitory” and that monetary policy will remain highly accommodative through 2022. But following the FOMC’s June meeting, investors found reasons to question the central bank’s resolve as rate projections and commentary by various FOMC members signaled earlier-than-expected rate hikes.

As Delta-driven Covid cases rose and the Fed’s timeline became less certain, investors downgraded their expectations for global growth, and the U.S. Treasury yield curve flattened late in the quarter. Against this backdrop of weaker growth expectations, the U.S. dollar strengthened, commodity prices (excluding oil) fell; U.S. equities outperformed; and market leadership rotated toward secular growth and away from cyclical growth, disrupted industries, and reopening beneficiaries.

Holding Pattern: Synchronized Global Recovery Delayed, Not Dismissed

We believe the market is overstating the risk that the Fed tightens too early. The “dot plots” that unnerved the markets are based on notoriously terrible forecasts. Chairman Powell has said as much on many occasions, including at the Fed’s June press conference. Also, FOMC members are likely to change over the next year. Given the current fiscal backdrop, it seems unlikely that openings will be filled by policy “hawks.”

We do not believe inflation will rise to a level that forces the Fed to abandon its new framework. As we have discussed in past outlooks, the likelihood of a durable acceleration in inflation has increased as a result of monetary policy and fiscal policy responses to the Covid shock, as well as the trend toward deglobalizing supply chains. However, disinflationary forces (e.g. technology, debt levels, demographics) remain formidable. (For more on this, see our post, “Perspectives on Growth and Inflation Expectations for a Post-Covid World.”) Also, unprecedented near-term supply chain disruptions are contributing to higher inflation readings. Although it is difficult to predict when these will be alleviated, we believe the supply side will address many of these issues over the next several quarters. In summary, we continue to believe monetary policy will remain highly accommodative for the next several quarters and likely longer.

We have grown more concerned that new Covid variants, particularly the Delta variant, could become a headwind delaying the synchronization of a global recovery. Even so, we believe that synchronization is a question of when, not if. Although the human impact of Covid remains immeasurable, markets have been resilient, recovering to new highs as conditions improve. India and Brazil both experienced severe waves of infections, hospitalizations and sadly, deaths in the first half of the year because of the Delta variant. Even so, both countries avoided the largescale shutdowns that occurred across much of the world in 2020. We are also encouraged by recent reports from the United Kingdom, which is facing widespread Delta variant infections but not the commensurate rise in hospitalizations and fatalities that could be expected. And while the second wave that struck Europe during the spring was likely not the Delta variant, the European economy was resilient. Businesses were better prepared to manage through the disruption, and government restrictions were less severe.

We continue to believe clearer skies are on the horizon. Reflecting this, our portfolios are positioned with a balance of cyclical growth/Covid-reopening exposure and secular growers. (For additional perspective on our positioning, see our post “What Factor Analysis Tells Us About Where the Global Markets Are Headed.”) We are vigilant to the threat of further Covid-related disruption but are hopeful that many countries are better prepared to respond to future shocks.

UNITED STATES

U.S. equities marched higher in the second quarter, with a more stable pace of gains compared to the volatility of the first quarter. The S&P 500 Index returned 8.6%, slightly ahead of the broader global equity index. The U.S. dollar spent most of the quarter in retreat, albeit with some strength in late June when markets discounted the possibility of earlier-than-expected policy tightening following the FOMC meeting. The combination of a strengthening dollar and economic data more closely aligned with expectations resulted in another market rotation. After leading in the beginning of the quarter, cyclicals and commodities saw their leadership fade in a rotation back to secular growth (Figure 2 on the previous page).

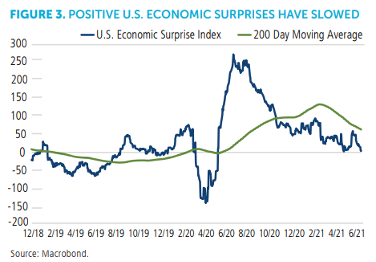

With regard to U.S. economic data, significant vaccination progress has been the linchpin in a broad reopening and the ramp-up of activity across the country. Manufacturing data continues to be robust, and inventory levels remain low, which portends sustained strength. That said, economic surprises have decelerated markedly since the second half of 2020 (Figure 3), and the rate of vaccinations is no longer accelerating. Although job growth has been very strong and 70% of the jobs lost in the first half of 2020 have been recaptured, recovering the next 30% of those jobs will be more difficult given productivity gains and permanent disruption caused by Covid shutdowns. (That is, many jobs aren’t coming back because they are in industries that have been disrupted. Either technology has allowed companies to adapt, or consumer/other activity has simply changed.)

In addition to the evolving monetary policy expectations noted earlier, there have also been shifting expectations on the fiscal policy front. During the first quarter, the prevailing narrative was that the massive fiscal stimulus packages proposed by the Biden administration would pass Congress. This narrative boosted anticipation that a reflationary boom would play out over the next couple of years, but with longer-term headwinds due to higher taxes and less capital-friendly policies. In recent weeks, the likelihood of such policies has fallen, and future stimulus packages will likely be smaller than those originally proposed by the administration. Although this dampens expectations for reflationary growth, it improves the medium-to-longer term outlook, and markets reacted accordingly.

Overall, our positioning in the U.S. market remains largely unchanged from the beginning of the year. We continue to favor a balance of cyclical and secular growth exposure in the portfolios. Defensive positioning is less attractive at this time.

EUROPE

During the second quarter, European markets and the euro rebounded, both in absolute terms and relative to global markets. The MSCI Europe ex-U.K. Index returned 8.2% and the MSCI U.K. Index gained 5.8%, versus 7.5% for the MSCI ACWI (all returns in USD terms). The euro gained 1.1% for the quarter; this rebound primarily reflects vaccine rollout progress in Continental Europe— progress that has tracked well against earlier U.S. and U.K. trends. We continue to envision similar vaccination ramp-ups can take place elsewhere around the world. In the United Kingdom, the Delta variant has caused a delay in full reopening and dampened relative performance, but at this point, we do not anticipate structural issues for either the U.K. or European economies given the vaccination progress already made.

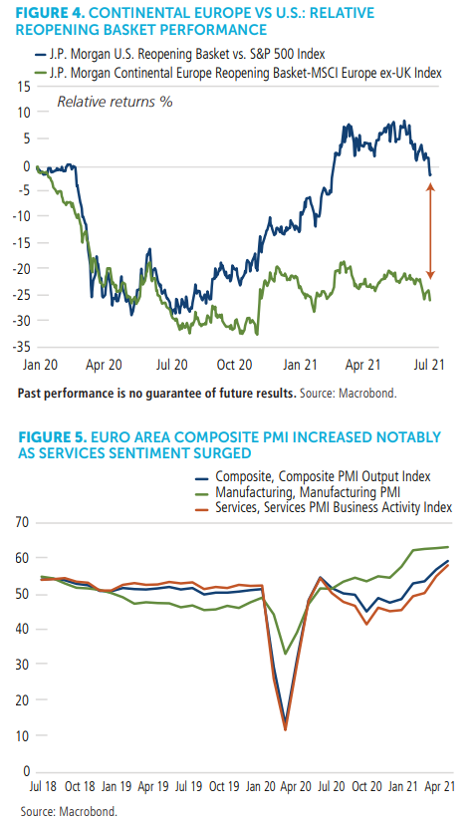

During the quarter, European companies aligned with Covid reopening trends began catching up to U.S. Covid recovery names. Even with these gains, we believe there is still significantly more catch-up potential for the European Covid recovery cohort (see Figure 4 on the next page). For example, vaccination progress should support the summer holiday travel season, which will benefit Southern Europe in particular.

Overall economic developments in Europe provide a complementary boost to the improving Covid backdrop. Supported by strengthening global product demand, European manufacturing PMI data remains healthy. Inventories still need to be rebuilt, which can further bolster manufacturing activity. Meanwhile, resurging activity in the eurozone’s contact-intensive travel and leisure industry and the brickand-mortar retail sector are helping to drive a strong recovery in services PMI (Figure 5 on the next page), with data in catch-up mode versus the United States. Given that services represent more than 70% of total contribution to GDP in Europe, this additional upside should have a significant impact. Moreover, this improving economic picture has contributed to a steady stream of positive EPS revisions from European companies.

On the fiscal support front, the €750 billion EU Recovery Fund was fully ratified by all participating countries in May. During the quarter, a clearer picture emerged about the timing and planned destination for disbursements for the fund as well as its ancillary economic benefits. Set to begin in the second half of this year and peaking in 2022 and 2023, disbursements will be split between grants (no payback required) and loans. Historically, stimulus of this type has not provided long-term tailwinds, but the fund should buoy select areas of the economy over the near term, and we will seek out opportunities to position around those themes. The fund has two main objectives: first, to support investment toward climate and improving green components of the economy, and second, digitalization of the economy.

To receive funds, countries must agree to conditions that make the eurozone a more attractive investment environment. For example, countries are incentivized to spend disbursements on capital investments, demonstrate progress on projects and comply with economic reform agendas. Countries in the periphery of Europe—namely Spain and Italy—will see the biggest benefits from these funds from both absolute and GDP-contribution standpoints. The larger targets for disbursements include high-speed rail, private and public sector digitalization, renewables, green transportation, building energy efficiencies, water resource protection, public education services, modernization of national health systems, and overall strengthening of private R&D.

The quarter also brought agreement by the G7 on a global minimum corporate tax. More specifically, the agreement requires multinationals within those countries to pay tax in the G7 countries in which they do business or incur a global minimum corporate tax rate of 15%. At this point, the plan remains light on technical details and represents more of an easy first, politically driven step. Wider G20 compliance would represent a larger impact, but that is not expected over the near term.

On the whole, our outlook for Europe remains constructive given a number of factors, including households’ willingness and ability to spend, further Covid reopening, fiscal support, and underlying economic strength and stability. Additionally, the structure of the market positions Europe to benefit from an environment of increasing interest rates and reflation. These dynamics provide tailwinds to a healthy number of European companies. Our portfolios also hold meaningful exposures to strong global franchises located throughout Europe that remain aligned with secular themes, such as luxury, biotech innovation, and global payments.

JAPAN

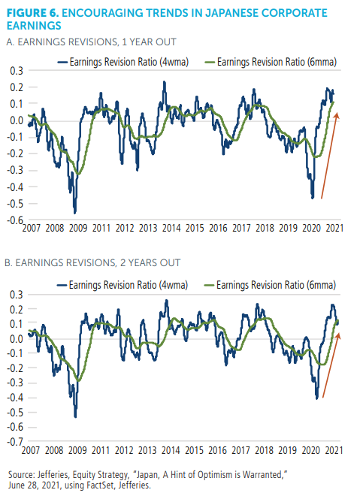

The Japanese equity market continued to underperform other major developed and emerging markets during the second quarter, returning -0.3%. Unlike during the first quarter, currency headwinds were not to blame for the underperformance. Instead, the delay in a more synchronized global recovery was the primary factor driving underperformance in the second quarter. The Japanese equity market is heavily weighted toward high-quality industrial, technology, and manufacturing companies that export goods globally—in other words, companies that would be positioned to benefit from improvements in global growth and increased capital investments. Many of these sectors underperformed due to concerns about China’s slowing credit growth and the timeline for European reopening, but corporate fundamentals remain compelling. During the most recent round of earnings announcements, we were encouraged by the number of companies beating earnings expectations and providing positive revised guidance on future earnings (Figure 6).

While agreement on a global minimum corporate tax garnered headlines during the G7’s meeting, another less publicized development may have significant positive implications for Japan. The G7 announced the launch of the Build Back Better World plan, which is the developed world’s answer to China’s Belt and Road Initiative. The plan emphasizes higherquality, cleaner, and more sustainable infrastructure investments. Combined with the vast array of country-specific green infrastructure programs and a global supply chain reorientation, the Build Back Better World plan has the potential to drive higher levels of capital investment in coming years. Many Japanese companies are likely to be key beneficiaries of these investments.

However, we remain selective in our exposure to Japan, emphasizing companies that are globally competitive and benefiting from improvements in global growth and the capital investment cycle. From a liquidity standpoint, we have been surprised at the degree to which the Bank of Japan (BoJ) has reduced its QE program, specifically via the more opportunistic use of the ETF/equity-buying program. While the BoJ has not indicated that it is removing monetary support, this is a development that we will continue to monitor closely.

EMERGING MARKETS

Emerging market equity performance weakened at the end of the first quarter as the dollar strengthened and U.S. Treasury yields rose. However, during the second quarter, emerging market equities recovered from March lows as the MSCI Emerging Markets Index finished the second quarter up 5.1%. Through the first half of 2021, emerging market equities gained 7.4% overall, but still trailed global equity markets.

While the dollar weakened during the first two months of the second quarter, it reacted with a sharp move higher in June after the market interpreted the June FOMC meeting as hawkish. Since then, however, emerging market equities have been fairly resilient relative to global equities, including U.S. equities. Following the June 16 Fed meeting through the end of the second quarter, emerging market equities gained 0.52%. This resilience of emerging market equities as the dollar strengthened during the final weeks of the quarter supports our view that emerging markets are on better footing to withstand U.S. rate increases than they were in 2013. (For more on this increased resilience of emerging markets, see our posts, “Taper Tantrum Redux? History Often Rhymes, but It Rarely Repeats” and “For Today’s Emerging Markets, A Less Accommodative Fed Would Be More Bark Than Bite.”)

Within emerging markets, the divergence in growth and performance can be tremendous from country to country—and this is certainly the case today, as economic recovery unfolds in varying ways. Especially in rapidly evolving environments such as these, we believe our active management and selective approach to allocating capital will provide us with key advantages.

Currently, this selective approach has led us to increase our emphasis on companies that are best positioned to benefit from a recovery in global growth. Central banks in emerging economies, such as Russia, Brazil, the Czech Republic, Hungary, and South Africa, have already begun rate hikes or plan to do so soon. Other countries, such as Chile, are expected to announce plans to tighten soon as well. While the market has discounted earlier rate hikes by the Federal Reserve, many emerging economies will raise rates even sooner and to a larger degree. This will likely prove to be a headwind for dollar strength as investors seek higher yields outside the U.S.

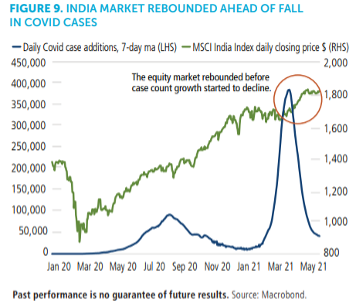

India. From a country perspective, India is well represented across our portfolios. A resurgence in Covid cases during the second quarter led to soaring hospitalizations, new lockdowns, and a sharp pullback in Indian economic activity. The Indian equity market retreated as well, reaching a low in mid-April. The MSCI India Index started the second quarter down 4.6% before bottoming on April 20 to finish with a second quarter gain of 7.0% (USD). The low during the quarter in the Indian equity market occurred about one month before Covid cases peaked (Figure 9). Since May, we have seen economic activity in India snap back rapidly, recovering more sharply than it did during the first Covid wave in 2020. Vaccine availability is climbing, with vaccinations expected to hit five million per day at the end of June versus 2.9 million per day in early June.

We continue to like India’s long-term growth potential and used the pullback in the equity market to add exposure. The country’s economic prospects are bolstered by its strategic partnerships with U.S. and European companies that view India as an attractive choice for reallocating key supply chains and adding capacity in new end markets. In addition, the Indian government’s pro-growth and stimulus measures support a postCovid recovery. From a sector perspective, we have identified opportunities in the financials, real estate, industrials and consumer sectors that can benefit from a Covid recovery. India also provides opportunities to invest in technology, manufacturing, and health care companies that can benefit from a developed market recovery.

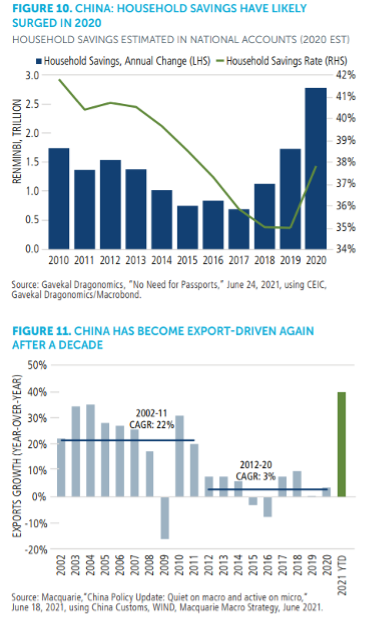

China. China is in a unique position globally, having embarked on an entirely different monetary cycle. Unlike most other major economies, China did not seek to combat the economic impacts of Covid through easy monetary conditions and significant fiscal support. As we have discussed in past commentary, China’s “first-in, first-out” experience of Covid meant that it was the first economy to recover, and strict lockdowns and management of Covid during the reopening phase have resulted in an economy requiring little stimulus or support. In addition, Chinese households built up large savings during 2020 as a precaution against further shutdowns (Figure 10). (For more on the Chinese consumer and the impact of Covid, see our post: “China’s Consumer Recovery: Lessons from the Tortoise and the Hare?”) We believe this higher level of savings will support consumer spending and contribute to the stability of the yuan.

When other countries halted production in 2020 due to more severe experiences of Covid, demand for Chinese exports strengthened (Figure 11) and offset weakness in consumption and the services sector. As production ramps up globally, export demand has slowed, but consumption and service demand has provided an offset as China’s economy more fully reopens and vaccination rates improve.

Because China does not need to remove aggressive monetary stimulus, it now has the capacity to ease at the margin through a recently announced cut to the reserve requirement ratio for banks. Instead, China has pushed forward with its deleveraging goals. After peaking last year well below the 2009 high, the China Credit Impulse Index turned negative during the second quarter for the first time in the current cycle. While this may have contributed to a less exciting first half of 2021 for Chinese equities and a nearly flat MSCI China Index, we’ve seen a stable-to-appreciating Chinese yuan. Against this backdrop, we believe Chinese equities are in a stronger position to weather near-term Fed tapering concerns. We expect that correlations between Chinese equities and global equities will fall during the next cycle, as Beijing will be in a position to resist reacting to changes in Fed policy.

Many new policies are being discussed and implemented within China across multiple industries, especially on the regulatory front. Given the nature of China’s one-party political system, these decisions may happen quickly and can have a significant impact on a variety of industries, providing either tailwinds or headwinds. (See our post, “The ‘Visible Hand’: How Beijing’s Policy Shapes Investment Opportunity in China.”) In recent years, the Chinese Communist Party (CCP) has enacted anti-monopoly regulations in the technology sector (including e-commerce) to limit the influence and potentially negative consumer impact of some of China’s largest companies. More recently, the Chinese government has focused on surging global commodity prices. Amid mounting concerns about inflation and its economic impact, China announced the release of state reserves of copper, aluminum, and zinc. The government also raised margin requirements for futures trading and introduced penalties for excessive speculation in an effort to cool down the commodity market and avoid negative inflation impacts.

COMMODITIES

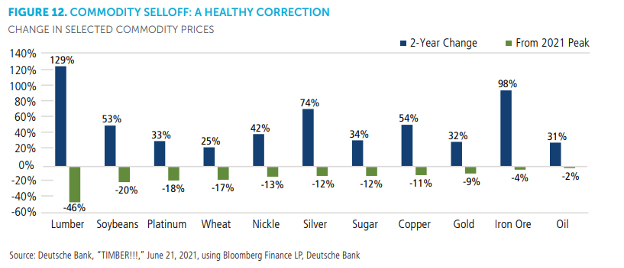

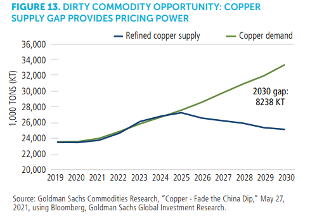

Commodities and commodity producers performed well through the first half of 2021 as demand came back online, but supplies remained constrained in many situations. However, the commodity complex corrected during the final few weeks of the quarter, with new China supply and the aforementioned shift in Federal Reserve policy expectations being the two most likely reasons for the selloff. To us, the recent decline looks more like a healthy correction; commodity prices are still well ahead of pre-Covid levels two years ago (Figure 12). In many instances, fundamentals support higher prices, as the commodity complex has made minimal investment in new supply over the past decade, while demand is increasing because of green infrastructure spending and traditional infrastructure investments. New green technology requires significant inputs of “dirty” commodities, such as copper and iron ore. (For more, see our post, “Copper: Cyclical Winner in a Shift to a Greener World”). The combination of significant capital flows toward these green initiatives and away from dirty commodities provides a backdrop for a multi-year period during which commodity producers can outperform.

In terms of bottom-up characteristics, our commodity exposure includes companies that have demonstrated capital discipline over recent quarters by using strong free cash flows to pay down debt and, in some instances, to repurchase equity and support dividends. We don’t believe commodity businesses have shed their boom-bust tendencies, but we do believe we are still in the early innings of this shift in leadership. Absent a dramatic change in demand or supply dynamics, we do not anticipate materially adjusting our conviction around the sector.

While these views support our overweight to commodity producers across our global, international, and emerging market portfolios, the strength of the commodity complex has additional implications for emerging markets. South Africa, Russia, and many Latin American and some ASEAN countries have significant exposure to the commodity complex, with banking and consumer sectors also geared to commodity recovery. Year-to-date, the currencies of these countries are among the strongest globally, and we have selectively added to financials and consumer exposure in countries positioned to benefit from this recovery. Additionally, the potential for China to reduce steel exports would be a positive for our positions in global steel players. We continue to monitor China’s policy response as it balances the longerterm goal of reduced carbon emissions with the shorterterm goal of curbing inflation.

CONCLUSION

We believe the case remains strong for strategic allocations to global and international strategies, including emerging markets, as economic recoveries among countries synchronize at the same time deglobalization continues. As we have discussed, the second quarter brought new concerns for changes in monetary policy and the threat of a Delta variant on global growth outlooks, contributing to a highly rotational market. While we monitor these risks, we are encouraged by the resilience of markets such as Brazil and India, which were hit hard by the Delta variant and have historically been susceptible to changes in U.S. monetary policy. These markets provide a template for how global markets can respond to these changing conditions. With a global synchronized recovery delayed not dismissed, we maintain a positive bias across the portfolios and a balance of cyclical and secular exposure as we navigate these volatile markets.

For additional commentary from Calamos Global Equity team and information about our global and international capabilities, please visit our global resource center at calamos.com/gloabalmarkets.

GLOBAL EQUITY TEAM CONTRIBUTORS

Nick Niziolek, CFA, Co-CIO, Head of Global Strategies, Senior Co-Portfolio Manager

As a Co-Chief Investment Officer, Nick Niziolek is responsible for oversight of investment team resources, investment processes, performance, and risk. As Head of International and Global Strategies, he manages investment team members and has portfolio management responsibilities for international, global, and emerging market strategies. He is also a member of the Calamos Investment Committee, which is charged with providing a top-down framework, maintaining oversight of risk and performance metrics, and evaluating investment process. Nick joined the firm in 2005 and has 19 years of industry experience, including tenures at ABN AMRO and Bank One. He received a B.S. in Finance and an M.B.A. from DePaul University.

Dennis Cogan, CFA, Senior Vice President, Senior Co-Portfolio Manager

Dennis Cogan is responsible for portfolio management and investment research for the firm’s global, international, and emerging market equity strategies. He joined Calamos in 2005 and has 20 years of industry experience. Previously, Dennis worked for Accenture in Strategic Planning and Analysis. He received a B.S. in Finance from Northern Illinois University.

Paul Ryndak, CFA, Senior Vice President, Head of International Research

Paul Ryndak is responsible for developing, enhancing, and maintaining our research processes and resources, working in partnership with senior members of our investment organization. He has oversight over the fundamental research efforts of our global equity research team and research associates. Paul has been with the firm for 17 years and has more than 20 years of industry experience. His previous experience includes roles at Fitch Ratings and GE Capital. Paul received a B.S. in Finance from Eastern Illinois University, and an M.S. in Finance from DePaul University.

Kyle Ruge, CFA, Associate Vice President, Senior Strategy Analyst

Kyle Ruge is a member of the international and global investment team and is responsible for fundamental research as well as for assisting in the portfolio management of the firm’s global, international, and emerging market equity strategies. He joined the firm in 2006 and has 16 years of industry experience. Kyle began his career with Broadview Advisors and McCarthy, Grittinger and Weil Financial Group. Kyle graduated magna cum laude from Marquette University with a B.S. in Finance.

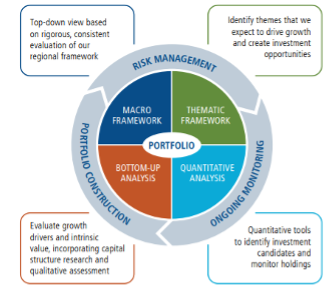

Calamos Global and International Strategies: A Robust Global Investment Process

TOP-DOWN THEMATIC VIEWS

» Expressed via active bets to key secular growth themes

TOP-DOWN CYCLICAL VIEWS

» Expressed via active bets to countries, currencies, sectors, etc.

BOTTOM-UP QUANTITATIVE TOOLS

» Calamos Timeliness Tools

» 3rd Party Quantitative Tools

» MSCI BARRA Factor Analysis

» MSCI ESG Ratings

BOTTOM-UP FUNDAMENTAL RESEARCH

» Analyze business model and growth drivers, competitive landscape, near-term catalysts, key risks and ESG considerations, business valuation, and capital structure opportunities

Themes Provide a Tailwind for Sustainable Growth

WE IDENTIFY AND PURSUE THEMES WE EXPECT TO DRIVE GROWTH AND CREATE INVESTMENT OPPORTUNITIES

Secular Themes: Long-term trends that drive growth for years/decades to come in a particular sector or industry. We believe that these themes provide a tailwind for select companies.

» Mobility and connectivity (information, entertainment, commerce anywhere/anytime; IoT)

» Mass digitization driving data explosion (cloud computing, data privacy/security, regulatory considerations)

» Artificial intelligence and automation (productivity gains, autonomous machines/vehicles)

» Global demographic shifts (shifts in consumption preferences, lifestyles, healthcare)

» Growing global middle class (S-curves for product and service consumption as incomes rise)

» Advances in nanotech, biotech, and genetics (improving standards of care, increasing lifespans)

» Globalization disrupted (rising nationalism and trade/geopolitical tensions)

Cyclical Themes: Themes tied to the general business cycle. These themes are shorter in duration but can provide shorter-term opportunities.

» Global central bank monetary policies

» Regional government fiscal policies /election cycles /reform initiatives

» Transitioning global commodity cycles

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including luctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to the potential for greater economic and political instability.

Indexes are unmanaged, do not include fees or expenses and are not available for direct investment. The S&P 500 Index measures the performance of large-cap U.S. equities. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI World ex U.S. Index measures developed market equities, excluding the U.S. The MSCI ACWI Index is a measure of the global stock market performance, including developed and emerging markets. The MSCI ACWI Growth Index and MSCI ACWI Value Index measure global growth and value equities, respectively. The MSCI US Index is designed to measure the performance of the large and mid cap segments of the U.S. market. The MSCI EAFE Index measures the performance of large and mid cap stocks in 21 developed markets, excluding the U.S. and Canada. The ICE BofA U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The ICE BofA Treasury 20+ Bond Index is market value weighted and designed to measure the performance of the U.S. dollar denominated, fixed rate 20+ Year U.S. Treasury market. The Russell 1000 Growth Index measures the performance of U.S. large cap growth stocks. The Russell 1000 Value Index measures the performance of U.S. large cap value stocks. The Russell 3000 Index measures the performance of 3,000 publicly held US companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market. The Russell 3000 Growth Index is representative of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 3000 Value Index is representative of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. The MSCI United Kingdom Index is designed to measure the performance of the large and mid cap segments of the UK market. The MSCI India Index is designed to measure the performance of the large and mid cap segments of the Indian market. With 101 constituents, the index covers approximately 85% of the Indian equity universe. The MSCI Europe ex U.K. Index captures large and mid cap representation across 14 Developed Markets (DM) countries in Europe. With 348 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across European Developed Markets excluding the United Kingdom. The MSCI China Index is constructed based on the integrated China equity universe included in the MSCI Emerging Markets Index, providing a standardized definition of the China equity opportunity set. The index aims to represent the performance of large- and mid-cap segments with H shares, B shares, red chips, P chips and foreign listings (e.g., ADRs) of Chinese stocks. Purchasing Managers’ Indexes (PMI) measure the prevailing direction of economic trends in the manufacturing and service sectors. The China Credit Pulse Index measures the growth in new financing as a share of gross domestic product

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits