“History never repeats itself, but it rhymes!” —Mark Twain

Dear fellow investors,

The group, OMC, made a very catchy song and video back in the 1990s called “How Bizarre.” It does a pretty good job of explaining today’s stock market.

Brother Pele's in the back, sweet Zina's in the front Cruisin' down the freeway in the hot, hot sun Suddenly red-blue lights flash us from behind Loud voice booming, "Please step out onto the line" Pele preaches words of comfort, Zina just hides her eyes Policeman taps his shades, "Is that a Chevy '69?" How bizarre How bizarre, how bizarre

Let us share some of the “bizarre red-blue lights flashing” in the S&P 500 Index:

- Bank of America Merrill Lynch mathematical model predicts -.8% annual 10-year returns

- Grantham, Mayo, Van Otterloo & Co. mathematical model predicts -6% real seven-year annualized large cap stock losses

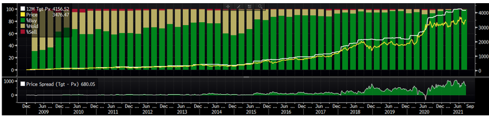

- S&P 500 Index price-to-sales ratio:

- S&P 500 weighting in 5x price-to-sales stocks:

- Amazon has 55 analysts and 55 buy recommendations:

Ooh, baby (Ooh, baby) It's making me crazy (It's making me crazy) Everytime I look around Everytime I look around (Everytime I look around) Everytime I look around It's in my face

“Every time I look around” this financial euphoria episode is “making me crazy,” because of how long it has lasted, how much the math tied to its carnage makes sense and because the anecdotal evidence has been visible for some time. We are channeling our inner Alan Greenspan, who called the tech bubble “Irrational Exuberance” in late 1996, only to look foolish for nearly four more years. As Art Cashin said recently on CNBC, the Y2K technology spending explosion elongated the tech bubble for another two years. Is the COVID-19 pandemic any different in elongating this euphoria episode?

However, back then you needed to be like Zina and “hide her eyes.” Everyone who has hid their eyes, plugged their nose and over-paid for glam tech and high price-to-sales stocks have been rewarded. The similarities or rhymes with 1999-2000 are “in my face.”

The thing that protected the singer from getting a ticket was his super-hot red 1969 Chevy convertible. Today, reality is being pushed back by the historically low interest rates. Warren Buffett explained in his May annual meeting that low interest rates have eliminated the gravitational pull on price-to-earnings and price-to-sales ratios. The low rates make expensive stocks look like the red ‘69 Chevy convertible.

Inflation is rearing its ugly head and it looks like a 1970s redo as the chart above shows. Ironically, this is not far from when OMC made “How Bizarre.” Overpricing Treasuries relative to inflation was a curse in the 1970s. What will stop it from being a curse this time?

Ring master steps out and says "the elephants left town" People jump and jive, but the clowns have stuck around TV news and camera, there's choppers in the sky Marines, police, reporters ask where, for and why

You see, the clowns who damaged investors in 1999 have “stuck around.” George Gilder had a huge newsletter following in the late 1990s and investors seemed to hang on every recommendation. Motley Fool (whose Coxcomb trademark is a clown hat) blasted away on radio and in their writing. Unmentioned tech stock research analysts substituted genuine research with investment banking customer recommendations.

Gilder has been replaced in 2021 by Ark disruption selections. Motley Fool has been reborn and “marines, police (SEC), reporters ask, where, for and why!” These current “bizarre” sets of experts are bound and determined to do to millennials what the prior group did to boomers. They bludgeoned boomers in the 2000-2003 bear market with the AOL chat room darlings. The millennials have Reddit and Robinhood to thank this time for the chat rooms and future carnage.

Jumped into the Chevy and headed for big lights Wanna know the rest? Hey, buy the rights

The nice thing about this episode of financial euphoria is that you can buy the rights to own common stocks which are outside this bizarre rhyme of the year 2000. Nobody wants oil stocks because of a big move toward ESG investing (which is also pumping up tech stock valuations). Oil prices have gone up and investors are still afraid to buy in. We view Continental Resources (CLR) like the ’69 Chevy. Folks don’t have the guts to bet on a rise in recurrent inflation and higher interest rates.

Lastly, everyone forgets how much value stomped growth from 2000-2003 when these “bizarre” circumstances existed, and the “red-blue lights” were flashing.

“Every time I (we) look around,” we see buyers of expensive stocks and, as always, fear stock market failure.

Warm regards,

William Smead

The information contained in this missive represents Smead Capital Management's opinions and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2021 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.