BlackRock portfolio manager Russ Koesterich, CFA discusses why earnings trumped rates as the catalyst for September’s poor equity performance.

September lived up to its reputation as a bad month for stocks. Global equity markets declined more than 4%, making September the worst month since the start of the pandemic. Beyond seasonal weakness, many attributed equity losses to higher interest rates. While rates clearly played a part, market patterns suggest that there was more going on than just a negative reaction to higher rates. Instead, investor behavior continues to be driven by an increasing focus on earnings and cash flow. Absent a significant change in either the growth and/or rate outlook, this is likely to continue.

1.50% 10 year ≠ end of the bull market

As I’ve discussed in previous blogs, the historical link between rates and equities is complicated, particularly when rates are low. It is also important to note that rates have been rangebound. Unlike last fall, when long-term rates began a melt-up that resulted in a near tripling of yields, today rates and rate vol are relatively contained. Rate volatility, as measured by the MOVE Index, remains well below the July and February peak. Moreover, the co-movement between rates and stocks in September suggests rates were not the dominant theme; there was effectively a zero correlation between daily changes in U.S. rates and U.S. equities last month.

What Do Investors Want?

While the September sell-off was not all about rates, higher yields did influence investor preferences, albeit in somewhat counterintuitive ways. Looking again at daily moves, defensive (low vol) stocks tended to outperform on days when bonds were selling off. This is somewhat at odds with historical patterns. Typically, low volatility names are the most sensitive to higher rates. Instead, investors seemed to focus on the low-beta aspect of these names rather than their rate sensitivity. Further complicating the picture: Not all cyclicals outperformed last month. Although energy had a stellar month, materials and industrials struggled along with the broader market.

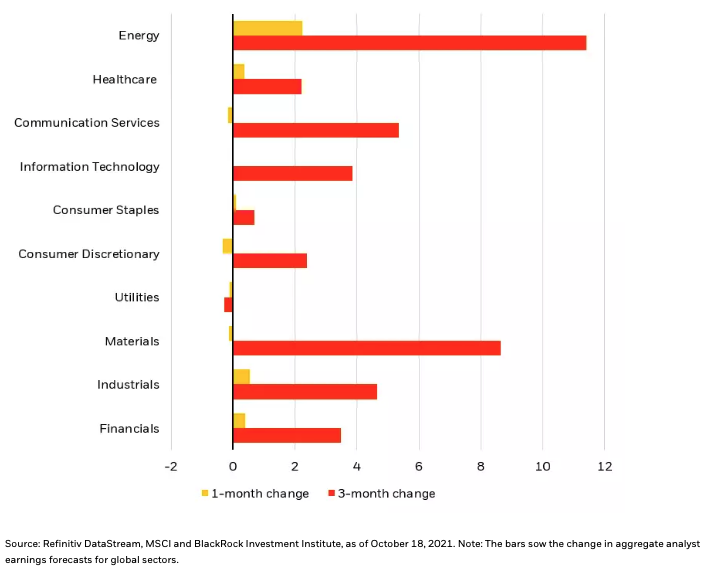

Arguably the missing part of the puzzle is earnings. With valuations drifting lower, earnings have become the driver of performance. This was evident in September. For example, while you could attribute energy’s stellar gains to resilience to higher rates, the simpler explanation is rising oil prices producing spectacular earnings growth (see Chart 1). At the opposite end of the spectrum, the underperformance of utilities arguably had as much to do with a lack of earnings growth rather than the sector’s historical relationship to interest rates.

Global sector earnings momentum

Going forward, I would expect a few key dynamics: modestly higher rates but no melt-up, sticky inflation in the near term and a Federal Reserve (finally) beginning the process of removing accommodation. None of this is a death knell for equity markets. But in the absence of ever easier financial conditions, earnings rather than multiples will continue to drive markets. This suggests less of a focus on rates and more on earnings, cash flow and sustainable margins in an era of rising cost pressure.

Russ Koesterich, CFA, is a portfolio manager for BlackRock’s Global Allocation Fund and lead portfolio manager on the GA Selects model portfolio strategies.

© BlackRock

Read more commentaries by BlackRock