Have small capitalization equity managers fared poorly this year, or not? It all depends on what benchmark you use.

I realized this after reading an article1 highlighting the struggles of U.S. small cap equity managers for the year ending June 30, 2021. The article stated that 78% of small cap core/blend managers failed to beat the passive benchmark, the S&P SmallCap 600® Index (S&P 600). That seemed strange: I had recalled that most small cap managers had done relatively well during that period, or at least I thought I recalled it.

That’s when I did a little digging. It’s not that the article was incorrect or that my prior understanding of small cap manager results was wrong. Instead, the different views came from the small cap benchmarks used for the comparison. For the year ending June 30, 2021, the S&P 600 returned 67.4%. For that same period, the Russell 2000® Index (Russell 2000) returned 62.0%. Doing the math, that’s a 5.4% spread for two indexes purportedly measuring the same U.S. small cap market segment. One can see how a 65% small cap return for the period could look good through one lens, but not so good through the other, depending on which index is being used for the comparison.

So, which index provides the correct answer? Did active small cap managers do well or poorly relative to the passive proxy? I’ll give the classic consulting/economist answer: it depends.

What’s your small cap definition?

The definition of small cap stocks typically starts with the benchmark. The article referenced the S&P 600 as the passive benchmark. It is one of the two more widely recognized small cap indexes. The second is the Russell 2000. The Russell 2000 represents U.S. stocks ranked 1,001 - 3,000 in terms of market capitalization. The S&P 600 represents 600 small cap stocks that meet S&P’s inclusion criteria, for which you will need to go to their website for a full description of methodology.

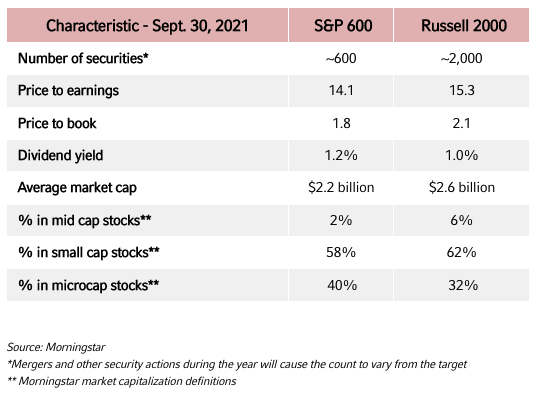

After you get past the stock count differences, the two indexes possess modestly different size and valuation profiles. The table below, populated with data provided by Morningstar, highlights some of these differences:

Reviewing price and yield-related measures, the S&P 600 appears to possess a modest value bias compared to the Russell 2000. The S&P 600 appears to be smaller in capitalization based upon both average market cap and the capitalization distribution of stocks. Depending on your view, these differences may be substantial or inconsequential, a big deal or a so what?

As of late, it has been more of a big deal due to the performance disparity between these two indexes. Fast forwarding to Sept. 30, 2021, the return gap grew even larger. For the year ending Sept. 30, the Russell 2000 returned 47.7%, another strong 12-month stretch. However, for that same 12-month window, the S&P 600 returned 57.6%, essentially 10% more. This gap introduces several follow-on questions, but the first to my mind is, does the S&P 600 always thrash the Russell 2000?

The simple answer to this is no. While the Russell 2000 trailed the S&P 600 by 9.9% for the 12 months ending Sept. 30, 2021, and by 7.5% for the year to date, the Russell 2000 topped the S&P 600 by 8.6% in 2020. In fact, going back to calendar year 2016, the two indexes have alternated leadership year by year, with the smallest gap between the two being 1.5% in 2017. The leads to the next question: are these two indexes measuring the same U.S. small cap market?

There certainly appears to be measurable differences from year to year. However, for investors with longer evaluation horizons, the two indexes tend to better align. For the five years ending Sept. 30, 2021, the S&P 600 tops the Russell 2000 by 10 basis points (bps) per year, 13.6% versus 13.5%. For the five years ending Sept. 30, 2020, the Russell 2000 led the S&P 600 by 0.8% bps per year. Leadership does reverse from period to period, reflective of the higher volatility inherent in the small cap universe, but over most longer horizons, the spread between the two tends to be far less dramatic than the calendar year results or the recent annualized returns.

Does this help identify which index you should use for your small cap evaluation? There isn’t one correct answer, but the decision should be driven by investor preferences for defining the small cap opportunity set and time horizon. The Russell 2000 is a broad small cap exposure that includes 2,000 small cap stocks in the U.S. market, versus the S&P 600, which is a subset of those small cap stocks that has a modest smallish and value bent. The differences appear to be much more important for calendar years and shorter horizons, since the differences level out as the time horizon expands. So, for investors who can get their arms around those two factors, a satisfactory answer should be available.

How does this impact investors evaluating and selecting small cap portfolios?

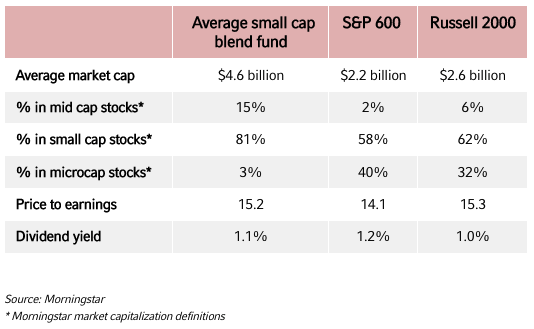

To evaluate current managers and select new ones, investors must understand the small cap portfolio’s positioning and the targeted benchmark. Let’s revisit the average small cap manager experience over the year ending Sept. 30 to demonstrate this point. Active small cap managers tend to have portfolio biases that persevere over time. On average, these managers own portfolios that modestly lean into mid cap stocks and have a slight valuation bias relative to the broad Russell 2000. The reasons for this are many, but to simplify: active small cap managers hold onto winners as they grow into the mid cap space, and active small cap managers have processes in place to identify and avoid expensive stocks. Morningstar data for Sept. 30, 2021 supports this:

These biases help explain the differences seen in the last year at the average manager level. Small cap value did much better than small cap growth for the 12 months (value beat growth by 33% according to Russell small cap indexes, and by 18% according to S&P small cap indexes). Thus, the average manager with a portfolio that leans a bit more value than the Russell 2000, but not as much to value as the S&P 600, produced returns that finished between the two indexes for the year. The managers looked smart versus the Russell 2000 and not so smart versus the S&P 600. (Market cap impacted relative results as well, but the gap between mid cap and small cap stocks was much narrower than the gap between growth and value).

So, what must investors do to select, manage and evaluate small cap portfolios?

- First, define your preference for identifying the small cap opportunity set. Select between the two primary small cap indexes, one comprised of 2,000 stocks defined by market capitalization, and one that is 600 stocks that can introduce style or cap orientation.

- Identify the benchmark the manager is targeting. This should be in the prospectus or accompanying guidelines. Annual evaluations can be quite difficult without this information.

- Recognize that small cap stocks tend to deliver higher volatility than larger cap stocks. Knowing this, the time horizon for evaluating small cap portfolios probably needs to be longer than the evaluation period for larger cap portfolios.

- Utilize multiple bogeys for assessing your small cap performance. Both small cap indexes can be beneficial to the evaluation process. Couple the benchmark evaluation with a corresponding review of the average manager results. By knowing the portfolio positioning driving these average results, the understanding of your own results will be more complete.

Advisors and investors with more sophisticated tools at their disposal can do deeper dives, but these steps will be a good start.

The bottom line

It would be great if we could simply rely on one index to define benchmark for our small cap portfolios. Unfortunately, given the higher level of volatility of small cap stocks, even small differences between benchmarks/portfolios can deliver significant differences in returns. Therefore, we need to understand the composition of the indexes defining the market—and how that composition relates to the portfolio(s) being evaluated—in order to make sound small cap investment decisions.

1 IGNITES: Small-Cap Funds Were Burned by Drift to Big Firms, Sept. 24, 2021

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

Russell Investments Financial Services, LLC, member FINRA, part of Russell Investments.

S&P SmallCap 600® Index: Seeks to measure the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

Russell 2000 ® Index: Measures the performance of the small-cap segment of the U.S. equity universe. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

RIFIS-24334