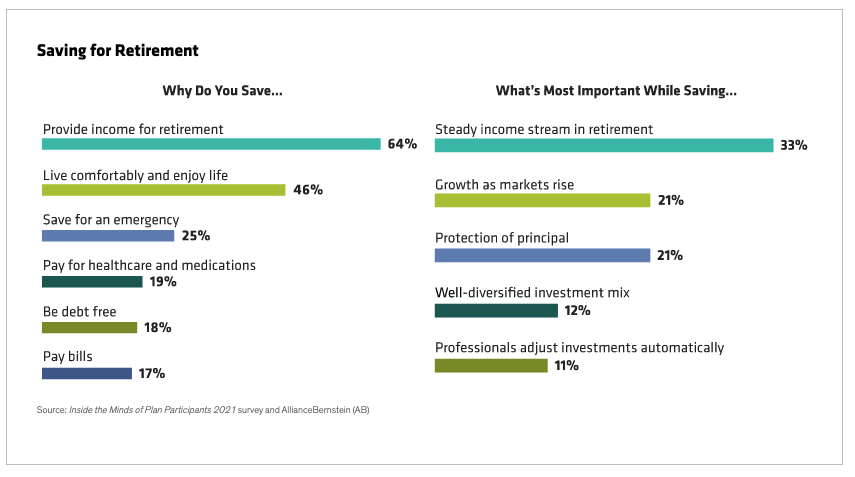

After decades of saving for a comfortable retirement, plan participants eventually face the question of how to create an income stream from those savings. Most aren’t sure how to do that, even though income is the main reason they’re saving in the first place, according to our latest Inside the Minds of Plan Participants survey (Display).

Lack of Confidence—and Time—Blur the Income Picture

What’s driving the disconnect between income priorities and realizing that income? A confidence shortfall, for one thing. Nearly half of plan participants (46%) said they don’t want to manage their investment mix, and roughly the same percentage is uncomfortable allocating plan options based on income goals. Low investment confidence may be connected to shrinking enthusiasm about outcomes: 44% of participants admitted they’re not confident their investments will generate enough income for life.

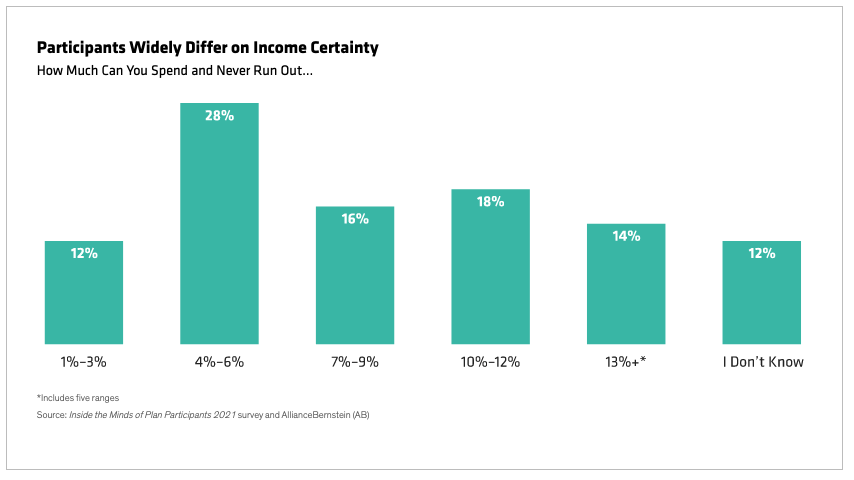

That uncertainty distorts participants’ perceptions of income sustainability. Our survey asked participants what percentage of a hypothetical $500,000 retirement nest egg they could spend annually without running out of money, and the answers were all over the map (Display).

The most common answer, 4% to 6%, may have made sense a generation ago when interest rates were much higher, but is much less realistic today. Many participants had even higher income expectations, and only 12% chose a more realistic 1% to 3% spending rate.

Participants Increasingly Want Control of Their Assets

Income uncertainty among participants is high on plan sponsors’ list of concerns. Default investment options, auto-enrollment and auto-escalation are all designed to help participants build income for retirement while requiring little hands-on involvement.

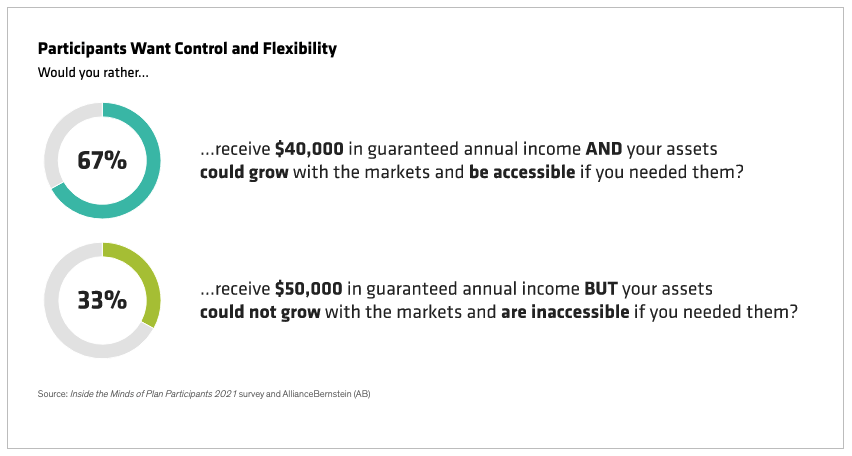

However, these enhancements don’t offer what our survey shows participants want most once retirement comes: control of their assets and flexibility. One way to give participants the control and certainty they desire is through guaranteed income solutions.

Solutions that either guarantee a specific amount of income in retirement or a specific withdrawal rate utilizing an insurance feature, such as an annuity, can offer these benefits and seem closely aligned with the direction most participants prefer. Given a choice, 67% of participants would rather have access to their assets after retirement and growth potential, even if it means receiving $10,000 less in guaranteed annual income (Display).

Not All Income Guarantees Are Created Equal

We think participants’ desire for tighter control of their retirement assets is a leap forward in ensuring a higher quality of post-work life. But control requires flexibility, opportunity and access—and not all income solutions offer them. For example, handing over a lump sum to a fixed annuity in exchange for predictable, guaranteed income provides steady income for life. However, if the income never rises, inflation could erode purchasing power.

So, not all guaranteed income solutions translate into a comfortable retirement, which may explain why only about one in 10 pre-retirees plans to buy an out-of-plan annuity; another 43% don’t have a particular solution in mind, so there’s work to be done on retirement income solutions. On that front, it was encouraging to see that nearly 20% of participants hope to leave their money in plan, where income solutions tend to offer more flexibility, access and growth potential along with their guarantees.

Evolving Income Needs Are Realistic and Achievable

Participants know what they want in retirement—reliable income. They’re also looking for help to decipher a topic that feels like abstract art into something tangible and understandable. And they want the ability to stay invested in the market for long-term growth potential and access their assets hassle-free.

These expectations are reasonable and obtainable, in our view, and income solutions must not only check the boxes but also be within reach and well explained. With baby boomers retiring in record numbers, income planning is a path for many plan sponsors to add a lot of fiduciary value right now. There's no shortage of income solutions to consider, but few can hit all these targets and turn savings into income that supports a comfortable retirement…for life.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein