Navigating Shifting Crosscurrents: 4Q 2021 Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits3Q 2021 Global Equity Market Review

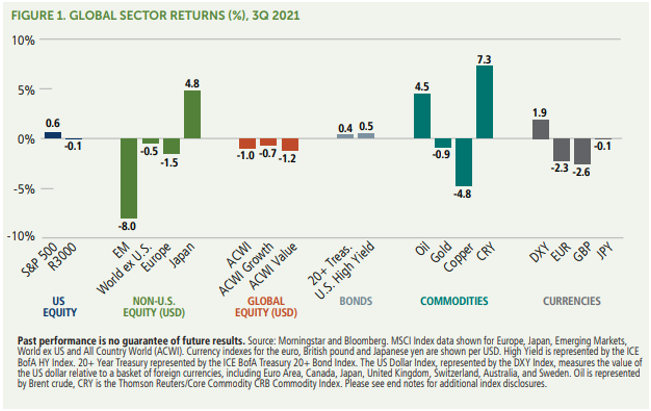

Internal rotations—regional, sector, and factor based—persisted through the third quarter. Global equity markets fell 1.0% during the quarter, which brought the MSCI ACWI Index’s year-to-date return to 11.5%. Developed equity markets started the quarter on an upbeat note. By early September, the MSCI World Index was up more than 5% for quarter. However, after a September sell-off, the index finished the quarter with a gain of just 0.1%. In contrast, emerging market equities never found their footing, and finished the quarter with a return of -8.0% (Figure 1). The dispersion of returns was wide, with the Indian equity market continuing its strong year-to-date run and returning 12.7% for the quarter. Conversely, the Chinese equity market returned -18.1% primarily because of the continued tightening of regulatory and monetary policy.

When the quarter began, markets were particularly concerned with the Covid-19 Delta variant and the Federal Reserve’s commitment to extending its highly accommodative stance under its new policy framework. At that time, we thought the market’s apprehension about the Fed was overstated. The Delta variant and the risk of ongoing economic disruptions were more troubling, although we were comforted by indications that severe cases in Europe were not soaring as they once had.

As the third quarter progressed, it became clearer that the Covid threat was receding. Global case counts dropped and news surrounding a new treatment from Merck increased optimism. Covid recovery names and cyclicals began to outperform. Unfortunately, visibility and confidence in the Fed’s monetary policy deteriorated, particularly in late September. Inflation readings accelerated, but we expected as much and believed the supply-side response would bring inflation back down as the global economy reopened. In September, two developments cast doubt on this view. First, a trading controversy caused two Federal Reserve Board presidents to step down, which increased the uncertainty surrounding future leadership and policy. Second, Chair Powell expressed less confidence that inflation was “transitory” and communicated an earlier-than-expected start and end to quantitative easing. This reset surprised the markets—bond yields rose, the yield curve steepened, and growth stocks in particular were pressured.

Navigating Shifting Crosscurrents

The world appears to be past the peak negative economic impact from Covid-19, absent a variant that can elude the benefits of vaccinations and natural immunities. The receding pandemic should continue to provide a tailwind for the reopening exposure, local consumption opportunities, and select reflationary beneficiaries we’ve been adding across our portfolios.

However, as economies begin to normalize, expectations for the future path of monetary and fiscal policies are shifting. As markets adapt to a post-Covid economy, we expect increased volatility, more rotational markets, and leadership changes. The risk of a policy error has also increased at the margin, with future Federal Reserve leadership and policy more uncertain today than a month ago.

The sustainability of this recovery depends a great deal upon the resolution of global supply-chain issues and the supply-side shocks in many commodities. China has been a clear disappointment to investors in 2021 and has weighed on the broad emerging market universe. Much of China’s pain has been self-inflicted via its own tighter monetary and regulatory policies. This leaves the door open to a swift course correction from the Chinese government, especially if the negative impacts of these policies on broader economic growth become more pronounced.

As we head into the fourth quarter, our portfolio positioning remains similar to where it was midyear. We have maintained a barbell approach, pairing cyclicals and Covid-reopening exposure with secular growers. Within our cyclical exposure, we are focused on industries with pricing power and those that are benefiting from global supply shortages.

In our strategies that seek lower-volatility global equity participation (i.e., those that invest in equities and convertible securities), we remain focused on providing investors with positive skew. We seek to mitigate exposure to a larger equity correction, while maintaining sufficient upside to continue participating in the global recovery.

Across all the Calamos global and international portfolios, we believe our focus on high-quality businesses that are consistently growing intrinsic value through time will serve our clients well through these rotational periods. Following this approach, we continue to find a wide range of opportunities supported by strong fundamentals, accelerated disruption and emerging leadership themes as the recovery cycle gains traction.

UNITED STATES

As a challenging September erased gains earned earlier in the summer, the US equity market as measured by the S&P 500 Index was flat for the quarter and marginally outperformed the MSCI ACWI Index. At the end of the quarter, the yield of the 10-year Treasury was also broadly in line with where it started, which again obscured an eventful September—in this case, a spike in yields.

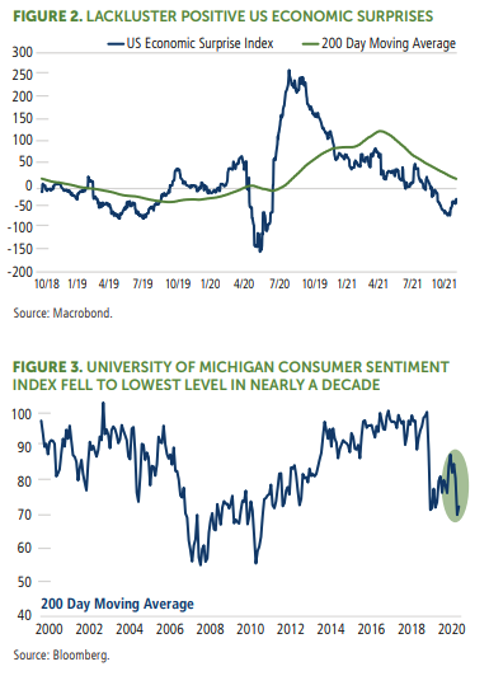

As measured by the Citi Economic Surprise Index, economic data remained lackluster during the third quarter and resulted in downgrades in most growth forecasts (Figure 2). Reflecting concerns over the high inflation readings of recent quarters, the University of Michigan Consumer Sentiment Index fell sharply in August to its lowest level in nearly a decade (Figure 3).

Global supply chain disruptions continued to increase order backlogs and extend lead times in manufacturing (Figure 4), with impacts that rippled across the economy. For some time, corporate commentary has flagged the supply-chain issues as a potential headwind, but earnings estimates have been stable to this point. We anticipate elevated volatility over the next several weeks as companies release third-quarter results and provide updated guidance and as markets discount any fundamental impact of supply chain issues.

On the monetary policy front, we expect the current highly accommodative path to continue for an extended period, but markets are likely to quickly discount a variety of headlines and crosscurrents over the next several quarters. The Federal Reserve was again front and center after communicating a more hawkish policy stance following the Federal Open Market Committee meeting at the end of September. The takeaways from the meeting and Chair Powell’s press conference were that tapering is likely to start and finish sooner than expected, and overall, the committee was more concerned about inflation than recent communications articulated.

Concerns about policy continuity over the next several quarters have been exacerbated by the trading scandal that has engulfed the Federal Reserve. In addition to four Fed positions that were already set to expire over the coming quarters, two more Fed officials stepped down early amid the controversy, and members of Congress are calling for further investigation. Given these developments, it’s reasonable for markets to be concerned about policy continuity and potential surprises, particularly in an environment where elevated inflation was already challenging that view.

And in regard to inflation, we have been of the view that most of the supply-side inflationary pressures are temporary. Although supply-side inflation pressures have been frustratingly slow to abate, we maintain our view that they will be temporary, although not uniformly so. Positive developments regarding Covid-19 give us confidence that the synchronized global recovery we’ve anticipated can develop and supply chains can normalize.

Even within our global recovery scenario, energy commodities may face more stubborn supply-side disruption. Years of low energy prices, shareholder demands for capex discipline, and environmental policies designed to support the transition to renewable power sources have led to underinvestment in energy infrastructure. In turn, this underinvestment has curtailed the supply-side’s ability to respond to the global recovery in demand. The result is surging oil, natural gas, and coal prices worldwide, with some countries rationing supplies. (See our recent post, “As Global Economy Reopens, Green Policy Creates Pricing Power for Traditional Energy.”) Much of the supply side should be able to bounce back quickly once the global recovery is on course, but to the extent that environmental policies prohibit new supply from coming online to meet increasing demand for energy, we can expect more persistent disruptions and inflationary pressures.

On the fiscal policy front, the likelihood of a large stimulus package decreased further amid weakening political support. As we’ve observed in the past, neither transfer payments nor higher taxes—cornerstones of the package—are likely to strengthen the economy over the long term. And although less demand-side stimulus might result in lower growth expectations in the shorter term, the economy isn’t in a good position to handle increased demand right now anyway, given the aforementioned supply-side challenges.

From a top-down perspective, our positioning in the US markets reflects our expectation for moderating-but-still-strong growth, framed by a balance of reflationary and disinflationary forces. For several quarters, our portfolios have been balanced across secular and cyclical growth opportunities. We believe this balanced approach continues to make sense. However, given the greater near-term uncertainty around monetary policy and inflationary and growth dynamics, we would not be surprised to see increased volatility and internal rotations in the quarters ahead, driven by growing market concerns that growth will slow more severely.

EUROPE

In local currency terms, the MSCI Europe Index returned 0.8% and slightly outperformed global markets. But a weaker euro (down -2.3% during the quarter) resulted in the index returning -1.5% in US dollar terms, which lagged global markets slightly. The euro weakness occurred primarily during the end of the quarter and was directly related to a stronger US dollar amid a perceived tightening stance in US monetary policy.

At the same time, Europe’s economic picture became less clear due to a variety of crosscurrents. The commencement of EU recovery fund distributions and German elections results reduced negative tail risks and contrasted with developments of more concern, such as manufacturing supply shortages; rising energy import prices; and the potential for incremental economic slowdown in China, a major export market for Europe. That said, we continue to have an optimistic medium-term view on Europe. The current market rebound since the Covid-bottom is tracking similarly to past market rallies, and Europe’s equity market remains more reasonably valued on the whole versus other developed market equities.

These recent macroeconomic crosscurrents have resulted in some churn in the European market, as they have in the global markets more broadly, but we believe there are specific areas of Europe’s equity market that continue to provide good near-term opportunities. Europe’s vaccination rollout has improved dramatically, with vaccination rates that now surpass those in the US, and there’s been a downturn in Covid-19 Delta-variant cases across Europe. On the back of these encouraging developments, economic activity across Europe is moving back to pre-Covid levels (Figure 5). Additionally, there is a considerable amount of catchup in the tourism sector (Figure 6), which is a large revenue driver for the Southern European region. We believe this leaves additional runway for further Covid reopening benefits for the region. As Covid case counts improve and travel restrictions ease, we expect the travel and tourism sector to gain strength.

Relative to the performance of the broader European equity market, the returns of Covid-reopening stocks also have begun to rebound. Here too, we see considerable catchup potential for these stocks to recoup performance relative to the overall European markets, without needing to return to pre-Covid levels (Figure 7). We believe our exposure to this contingent of names can benefit further and perform well as Covid-recovery trends build.

We also continue to find opportunities in Europe that align with secular trends. In particular, this includes smaller-cap names that we believe can benefit from the investment into technological capabilities, infrastructure and education in Europe. (For more, see our post, “The Big Opportunity in European Ecommerce.”) We maintain exposure to areas we’ve discussed in past outlooks, such as payments, but we also are expanding more broadly into ecommerce and IT software.

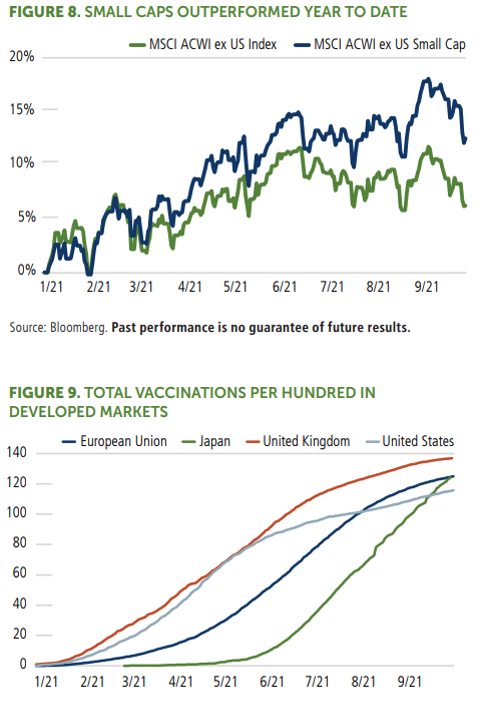

Leveraging technological development to deliver value to customers and investors, smaller-cap names in these areas are generating strong returns on capital for investors. The more fragmented nature of this space—and the absence of incumbent behemoths—also help smaller players. In both the European and global ex-US markets, these dynamics have contributed to the year-to-date outperformance of small caps (Figure 8). Across our portfolios, we have been increasing exposure to this contingent in Europe and believe it can be a promising source of additional future opportunities.

JAPAN

After a lackluster first half of the year, during which the MSCI Japan Index was up only 1.4%, Japanese equities delivered a strong third quarter return of 4.8%. Most of this positive performance came following the announcement at the beginning of September that Prime Minister Suga would step down. Because the Japanese economy is export-oriented, it is more vulnerable to slowing global growth than many other developed markets. For most of this year, the Japanese market has fought against a range of headwinds. As we discussed in our 2Q outlook, concerns mounted over a slower global recovery, Covid spikes, and ongoing Covid shutdowns globally. There were also fears of slowing credit growth in China, which continues to be a risk to global markets.

Additionally, consumer spending in Japan has been negatively influenced for much of this year by shutdowns as Covid cases were higher than in 2020.

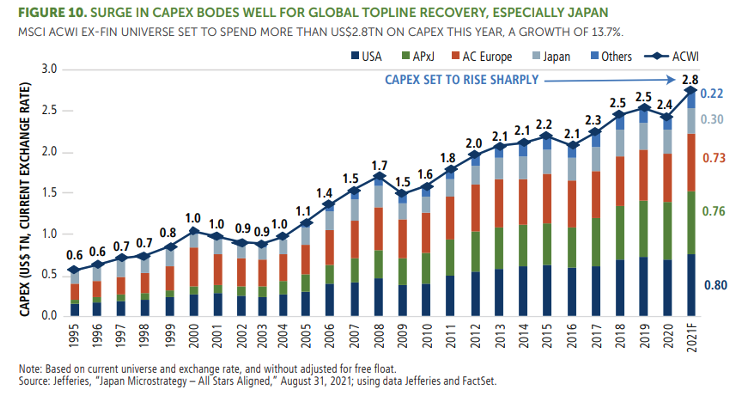

These headwinds have lessened considerably. Japan’s vaccination rollout efforts were very slow earlier in the year and contributed to the falling popularity of Prime Minister Suga. However, over this past quarter, vaccination rates in Japan have accelerated, surpassing the United States and catching up to Europe (see Figure 9). As Covid cases have fallen, Japan has started easing the Covid restrictions that have been in place the past six months, which should give a boost to the services sector. Continued easing of travel restrictions through the remainder of the year is also anticipated. Moreover, we expect that a ramp-up in global capital expenditures (Figure 10) will give many Japanese companies a lift, given the economy’s export-oriented nature.

At the beginning of September, Prime Minister Suga’s decision to step down catalyzed the Japanese equity markets. His resignation removed political uncertainty because his falling popularity had led to increasing concerns that the Liberal Democratic Party (LDP) could lose its majority to the Communist Party and lead to political turmoil. In elections that took place at the end of the third quarter, Fumio Kishida won the LDP’s nomination and was inaugurated as prime minister in early October. Kishida is pledging a large fiscal stimulus package (potentially around $275 billion) before year end and is a proponent of reopening the country quickly to stimulate the economy. Consumer confidence in Japan has improved since earlier in the year, and as the economy reopens, we anticipate improvements in consumer spending.

In our recent commentaries, we noted there were compelling opportunities to invest selectively in Japan despite the macro headwinds, given that many Japanese companies offer attractive fundamental characteristics, such as increasing margins (Figure 11). We maintain this selective approach to Japan and emphasize companies that are globally competitive and can benefit from improvements in global growth and the capital investment cycle.

EMERGING MARKETS

As measured by the MSCI Emerging Markets Index, emerging market equities were down 8.0% during the third quarter, bringing their year-to-date return to -1.2%. Although the rebound we’ve seen in the US dollar and interest rates may be viewed as a potential headwind for the asset class, the real pain in emerging markets has been primarily self-inflicted by China. Tighter regulatory and monetary conditions have been largely responsible for the correction in Chinese equity markets (-16.6% year to date and 18.1% for the third quarter). Outside China, emerging markets are up 9.2%, as measured by the MSCI Emerging Markets ex-China Index. Given China’s heavy weighting across emerging market benchmarks and its contribution to Asian economic growth, emerging market equities have been broadly weaker this year.

Although we are disappointed with the year-todate performance of emerging market equities, we are optimistic about a rebound. Because much of the pain has been self-inflicted, the solution can be self-administered. We are anticipating indications that China is moving to a more accommodative fiscal and monetary stance to support economic growth. Also, we note the recent increase of regulations is not unprecedented. There have been other periods when regulation has surged, but these have tended to wane over time once the government is confident that the country is aligned with key priorities. We’re watching regulatory announcements for signals that this latest round of new regulation is abating, as we’ve seen in previous cycles.

We believe it is highly likely the Chinese Communist Party (CCP) shifts its tone heading into the December politburo meetings. Recent statements prioritizing near-term growth and stability over longer-term policy goals seem to indicate an inflection, although we await further actions to validate these statements. We are watching the Chinese currency market and spreads of Chinese sovereign bonds and investment-grade bonds for further downside risk. Both of these markets have been very stable through this period, and year to date, the Chinese renminbi has actually appreciated versus the US dollar.

Although the Chinese government’s recently enacted policies have created headwinds for certain industries, there are still opportunities for companies that are aligned with the country’s strategic priorities. As we have discussed in our series on the “Visible Hand” of the CCP, these beneficiaries include companies involved with artificial intelligence, cloud technology and hardware, as well as companies tied to evolving consumer trends. We have used recent volatility opportunistically to build exposure in names that we believed were oversold (see our post, “Volatility Creates Opportunity in China’s Equity Market”). We are identifying a breadth of opportunity elsewhere in the emerging markets, including India. The Indian equity market had a strong third quarter, as measured by the MSCI India Index’s return of 13.2%, which was significantly better than the returns of most emerging and developed equity markets. Through the year to date, the Indian equity market is up 26.8%. Although India’s health-care system and economy suffered severely because of the Covid-19 Delta variant, we are seeing broad strength in India’s economy as it reopens, and there is optimism that increased vaccination rates and natural immunities will result in greater resilience to future waves. As we discussed in our post, “India’s Stealth Bull Market,” we have invested in companies positioned to benefit from more robust consumer activity, an upward turn in the housing sector, and broad global secular growth themes.

We believe several ASEAN markets hit hard by the Delta variant may experience recovery trajectories similar to India’s, with the potential to improve sentiment for the broad emerging market asset class. In particular, Indonesia, Thailand, and the Philippines have announced plans to remove Covid-related restrictions, and we anticipate other countries will follow. We saw a broad improvement in manufacturing Purchase Managers’ Indexes across these countries in September. As we saw in India, we anticipate consumers coming back online, and consumption and services rebounding quickly as these economies reopen. Cross-border travel may be slower to recover, in line with what we’ve seen in Europe to date, but economies that depend on international travel for a larger percentage of growth, such as Thailand, have already announced plans to fully reopen by year end.

Ultimately, although the emerging market equities have experienced a setback as 2021 has progressed, we are mindful of prior cycles and how quickly conditions can change—especially when much of the damage has been selfinflicted. We are optimistic about opportunities throughout emerging markets outside China, with India as a very recent example of how rapidly these economies can rebound once restrictions are lifted. We are also optimistic that recent policy headwinds within China could turn quickly to tailwinds, although the timing of this inflection is less certain.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All