After years of anxiously watching for inflation, it’s here. Unfortunately, what many expected to be a short, COVID-19-induced visit has turned into an extended stay, thanks to robust demand and a snarled supply chain. The question now is does the supply chain pose a threat to our economic outlook?

Government data broadcasts the heartbeat of the US economy, but it can lag real-time economic conditions by weeks or even months. That makes it less than ideal for predicting real-time disruptions. To quickly and accurately chart inflation’s unpredictable path, we developed a dashboard that provides a 360°-view by including traditional indicators, high-frequency data, big data and views from our global research team.

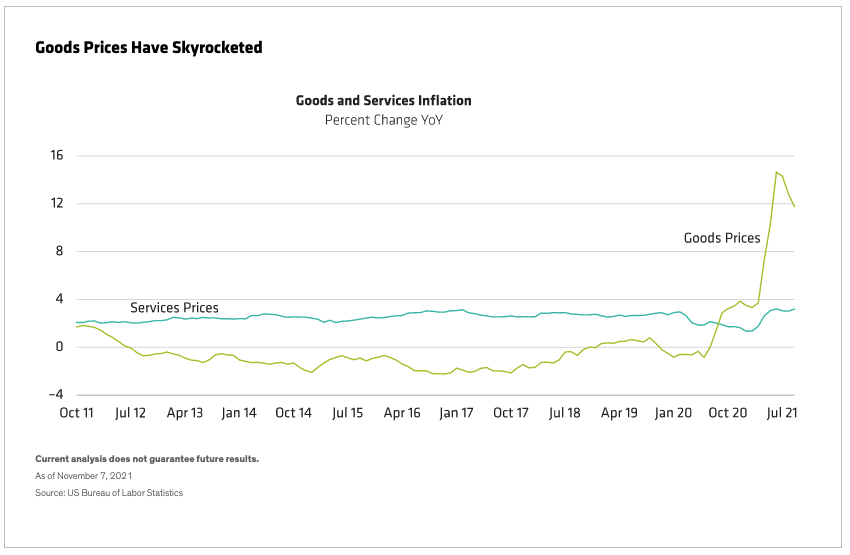

Supply Chain to Blame for Skyrocketing Goods Prices

For 10 years, the goods and services components of inflation have run separate courses (Display). While the services component of inflation held steady around 2.5% over the last decade, goods prices were disinflationary. Then, in mid-2020, goods inflation skyrocketed into double digits due to a combination of pent-up demand and supply-chain disruptions. A surge of this magnitude is unprecedented in modern economic history and is pulling headline and core inflation up significantly.

What’s the key to driving down inflation? Fixing the supply chain. Some blame labor shortages as workers appear less interested in their previous jobs after the pandemic shutdowns. Yet, monthly employment reports average 500,000 jobs added, sometimes with upward revisions to prior months. And at the current pace, the economy is on track to be back at pre-COVID-19 employment levels by mid-2022.

So, while supply-chain difficulties include labor shortages, that’s not the whole story. The best measure of supply-chain disruptions using monthly data is the Institute for Supply Management’s Backlog of Orders. This gauge peaked in June but remains well above normal due to widespread reports of challenges sourcing parts and materials, rising commodity prices, and transportation struggles, on top of difficulty attracting and retaining employees.

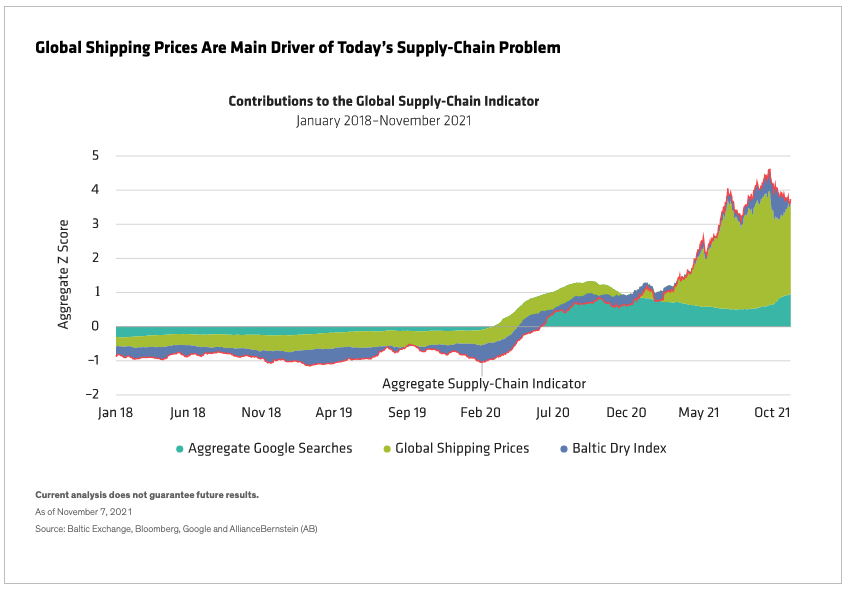

Untangling the Supply Chain

Eventually, traditional monthly economic data will tell us that supply-chain troubles are easing. But before then, we believe that alternative data sources can give us a real-time measure to help detect the untangling of the supply chain.

We’ve created an Aggregate Supply Chain Indicator that uses daily data to measure supply-chain health. The gauge combines global shipping container prices, the cost of transporting dry materials, and aggregate Google searches for terms such as bottleneck and food shortage (Display).

This gauge can alert us to changes in the supply chain more quickly than traditional data. The indicator spiked during the pandemic but appears to be stabilizing, albeit at extended levels. The most significant contribution to the spike was global shipping container prices, which are moving lower but are still highly elevated.

We also evaluate supply-chain pressures using natural language processing (NLP) analysis, a big-data solution that allows computers to understand written documents. We tracked mentions of the supply chain, logistics, freight and shipping in 4,000 quarterly US earnings transcripts since 2010. We tallied how often each was mentioned and assessed surrounding words to determine if the context was positive, neutral or negative. We found that management discussed supply issues more in 2020 and 2021 than at any other time in the last 10 years—and the negativity increased significantly. Year to date, the sectors most affected were autos, retail, technology, transportation services and materials. However, the drivers of supply-chain constraints differ.

Supply-chain constraints include logistics, supplier shortfalls and higher labor costs. The most significant constraints came from supplier shortfalls, specifically a shortage of components, making it difficult for companies to meet recovering demand with supply. An inability to restaff combined with an increase in the price of labor has been a significant challenge for transportation-related sectors and hotels, restaurants and leisure. Finally, logistics—the inability to get goods from point A to point B or a substantial increase in freight costs—have affected the retail and food retail sectors.

Tracking the Effects of Supply-Chain Disruption

Supply constraints remain a cloud over expected corporate margins, with estimates becoming considerably less optimistic as the year has progressed. However, the outlook for post-COVID-19 margins is still positive for most sectors, and expectations for 2022 are still above those for 2019 and 2020.

What do we make of the supply chain? The bad news is that the challenges associated with reopening from COVID-19 have had a clear effect on corporate margins and inflation. The good news is that households have enough cash on hand to continue to consume even as prices rise—at least for now. That means that supply-chain disruptions have not seriously impacted our overall growth outlook.

But we remain on the lookout for signs that the consumer has had enough. If these signs appear before supply chains get straightened out, the growth outlook could deteriorate. That’s why we believe it’s critically important to monitor the supply chain: the sooner it unsnarls, the smaller the risk to the economy.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein