Chief Economist Scott Brown discusses current economic conditions.

The November Employment Report was a mixed bag. Nonfarm payrolls rose less than anticipated, but the unemployment rate fell sharply. The shortfall in payrolls (relative to expectations) likely reflects the usual noise in the monthly data, it might reflect difficulties in hiring, but it certainly doesn’t reflect weak labor demand. The plunge in the unemployment rate suggests that tight labor markets are an issue – even as payrolls remain 4.1 million (2.7%) below where they were in February 2020. Fed Chair Powell testified that “it now appears that factors pushing inflation upward will linger well into next year.” In addition, “with the rapid improvement in the labor market, slack is diminishing, and wages are rising at a brisk pace.” Together with the broadening of price increases across sectors, the Fed will taper faster and raise rates sooner than was anticipated earlier.

The first thing to do when analyzing the job market data is to ignore the news reports. Headlines: “Hiring Slowed (WSJ); “Hiring was a bust” (NPR); “Companies were growing cautious” (NYTimes). What nonsense.

Prior to seasonal adjustment, the economy added 778,000 jobs last month, well above a typical pre-pandemic November. Retail added fewer jobs than usual, although the sector had added a lot of jobs over the three previous months and couriers (package deliveries) added more than in past Novembers. The three-month average for private-sector payrolls was 429,000, which is strong. Once again, payrolls for the two previous months were revised higher (+82,000), which is what we normally see in a strong job market.

Click here to enlarge

The unemployment rate sank to 4.2% from 4.6%, even as labor force participation finally picked up (61.8%, vs. 61.6% in October, little changed over the 12 previous months) – participation averaged 63.2% in 4Q19. The demographics (an aging population) implies that participation should be trending lower over time, but there is still a big gap relative to where we were before the pandemic. Early retirements and dependent care issues have been factors. There are some early signs of un-retirements (think those in their late 50s or early 60s), but childcare remains a significant issue (less available and more expense than before the pandemic).

Average hourly earnings rose 0.3% in November (+4.8% y/y). For production workers, the increase was 0.5% (+5.9% y/y). These aren’t reliable gauges of labor costs, but the direction is right: higher.

For the Fed, tight labor markets aren’t a concern by themselves. But in the current environment, with price increases broadening across sectors (in sharp contrast to the narrow inflation spike in the spring), the tight labor market can be expected to compound inflationary pressures. Fed officials, including Chair Powell have signaled an openness to accelerating the tapering of asset purchases. We are still short of making up the ground lost in nonfarm payrolls during the pandemic and are well below the pre-pandemic job trend. Those on the lower rungs of the economy have fared the worst and are slower to recovery, but conditions will get much worse if the Fed doesn’t act to get inflation back down. There is no easy path here.

Recent Economic Data

The Fed’s Beige Book noted that “robust demand for labor but persistent difficulty in hiring and retaining employees.” Wage increases were “widespread” across sectors of the economy. The November Employment Report was mixed. Nonfarm payrolls rose by 210,000 (median forecast: +550,000), with a net upward revision of 80,000 to the two previous months.

Click here to enlarge

The unemployment rate fell to 4.2%, vs. 4.6% in October, 6.7% a year ago, and 3.6% before the pandemic. The drop came despite an increase in labor force participation, which had trended flat over the previous 12 months.

The ISM Manufacturing Index edged up to 61.1 in November (little changed from November’s 60.8%), with activity restrained by ongoing supply chain issues. The ISM Services Index rose to another record high in November (69.1, vs. November’s 66.7). Comments from supply managers focused on labor issues, late deliveries and shortages, transportation and logistical issues, and rising input costs.

Factory orders rose 1.0% in October. Durable goods orders fell 0.4%, reflecting a drop in civilian aircraft orders. Orders for nondefense capital goods ex-aircraft rose 0.7%, while shipments rose 0.4%.

Click here to enlarge

Motor vehicle sales slipped to a 12.9 million seasonally adjusted annual rate in November, vs. 13.0 million in October and 19.0% below the year-ago pace. Weak sales reflect supply issues (the semiconductor shortage), rather than softer demand.

Gauging the Recovery

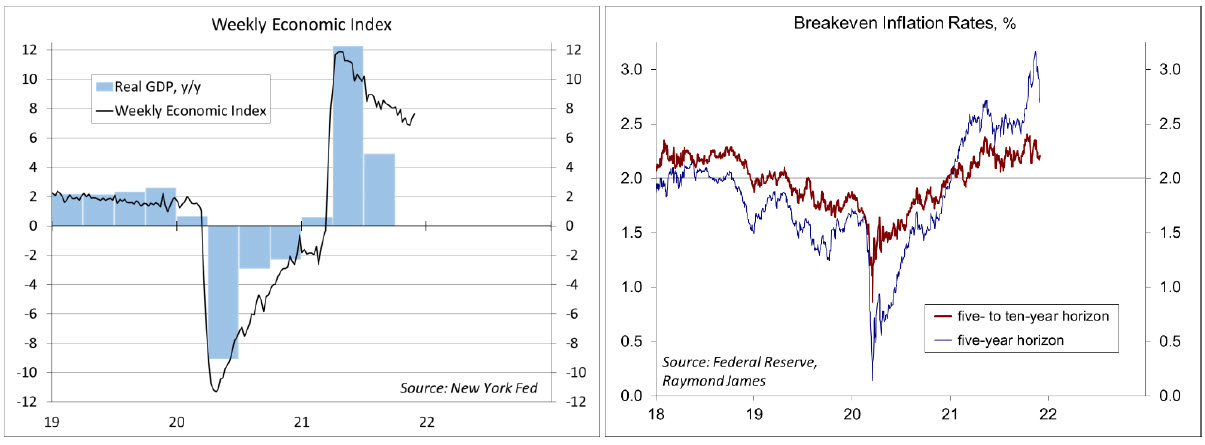

The New York Fed’s Weekly Economic Index rose to 7.65% for the week ending November 27, vs. +7.32% a week earlier (revised from 6.97%). The WEI is scaled to y/y GDP growth (+4.9% y/y in 3Q21).

Click here to enlarge

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries) for the 5-year horizon have fallen, reflecting a belief that the Fed will act to get inflation back down.

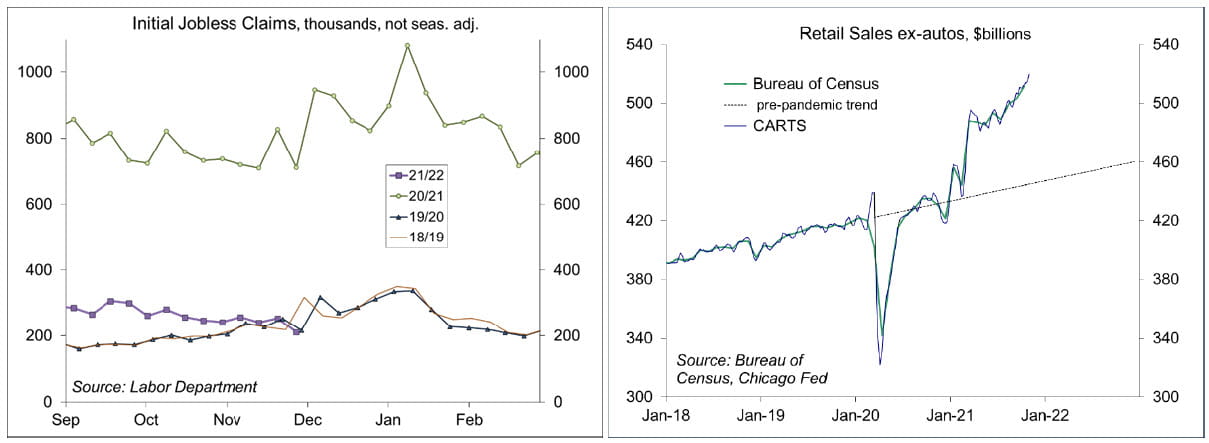

Jobless claims rose by 28,000, to 222,000 in the week ending November 27, following a 50-year low (194,000) in the previous week. Claims are now back to the pre-pandemic level, consistent with a tight labor market.

Click here to enlarge

Chicago Fed Advance Retail Trade Summary (CARTS): up 0.9% in the second week of November, following a 0.3% gain in the previous week. November retail sales (ex-autos) were projected to rise 1.9% from October.

The University of Michigan’s Consumer Sentiment Index fell to 67.4 in the full-month assessment for November (vs. 66.8 at mid-month and 71.7 in October), reflecting inflation concerns. The report noted a further increase in inflation expectations and “the roots of inflation have grown and spread more broadly across the economy.”

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James