Historically, fourth quarter tax loss selling of closed-end funds (“CEFs”) has been prevalent in the market. CEFs may be more susceptible to tax loss selling given they trade on a stock exchange and market prices (investor return) can deviate from underlying net asset values (“NAVs”) (fund return). Additionally, CEFs typically provide attractive income to shareholders through monthly distributions, which are paid out of the fund’s NAV. These dynamics may create an opportunity for the investor to realize a “tax loss”, even in situations where the investor’s total return is positive. This selling results in additional supply and may further reduce a fund’s market price. Selling may be amplified in asset classes that experience elevated levels of volatility in a given year.

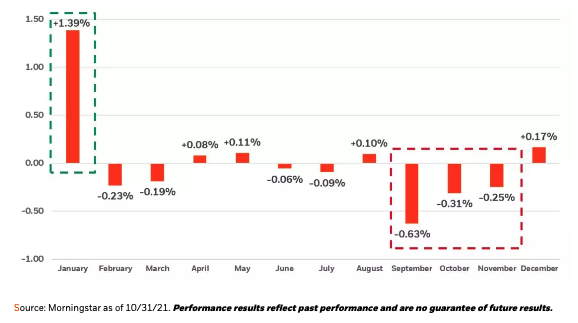

Exhibit 1 - The January effect

Average change in monthly premium/discount: 2001-2021

Based on historical trends, investors that have purchased CEFs in the latter part of the fourth quarter have generally realized the benefits of tax loss selling through the short-term effect of discount narrowing (market price outperforms NAV) most prevalent in the month of January. Notably, on average CEF discounts have narrowed in January in 16 out of the last 20 years. This consistency may be attributed to the ‘January Effect’. According to this theory, pent up demand following tax loss selling may be the factor driving the outperformance as investors re-enter the market after selling positions in prior months to harvest taxes and rebalance their portfolios. Based on historical trends, tax loss selling in 2021 may present an attractive entry point for long term investors to reap the rewards of a temporary mispricing in the CEF market.

A Look Ahead

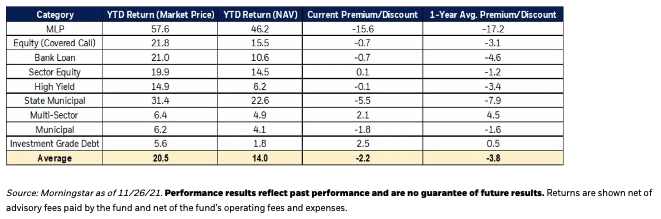

The CEF market has been strong in 2021, with market price returns and NAV returns positive across most sectors (Exhibit 2). Given this dynamic, tax loss selling should be muted in 2021. That being said, it’s also important to note that while a CEF could have a positive total return, a large portion of that return could be from distributions, potentially triggering some year-end tax loss selling if the investor’s cost basis is higher than the current price. While most CEF categories had positive returns on the year and have seen discounts reduced, certain sectors and select funds still trade at larger than average discounts, which could present a good long-term entry point.

Exhibit 2 – CEF returns and premium/discounts

Opportunities in the CEF space

While equities have performed well year to date, the BlackRock Investment Institute (“BII”) is still overweight the space given they expect the restart to re-accelerate and interest rates to remain low. BlackRock also believes there are a few ways that investors can take advantage of the CEF structure in the equity space: finding income and accessing differentiated streams of return through private investments.

Equity CEFs for income

Many equity CEFs, including all of BlackRock’s CEF equity products, use a managed distribution plan, in which the fund sponsor aligns the fund’s distribution rate with the long-term expected total return of the portfolio. A large portion of the distribution will be funded through capital appreciation (realized or unrealized capital gains), essentially “monetizing” total return in the form of a monthly distribution to investors. This allows equity CEFs to potentially pay out more than their ETF or mutual fund counterparts. The median annual distribution rate for equity CEFs is 6.7% compared to 1.6% for equity mutual funds, according to Lipper1.

1 Source: Lipper as of 10/31/2021 based on the entire universe of equity CEFs and mutual funds.

Just like investors can write off a certain amount of capital losses to lower their tax burden, so can CEFs. Many CEFs have embedded loss carryforwards that can be used to offset capital gains. As a CEFs seeks to regularly distribute short-term or long-term capital gains as a component of its managed distribution, such offsetting of gains by losses may reduce taxable earnings and result in a distribution of return of capital (“ROC”) for tax purposes. While ROC is generally not taxable to shareholders, the distribution of ROC typically requires that shareholders reduce the cost basis at which their shares are held by the amount of any ROC distribution received. This essentially acts as a tax deferral, not realizing the tax burden until the shares are sold (and often at a lower tax rate than dividend income). This can be beneficial to investors who hold these funds in taxable accounts.

Focusing on dividends

With yields low across the globe, investors looking for income could turn to high quality dividend paying stocks. High-quality companies in particular tend to have strong balance sheets, good earnings trends, and ample cash flow above ongoing business needs. These elements can provide companies with flexibility during periods of economic uncertainty and help them to endure and adapt to changing operating environments. Dividend growers specifically possess many of the quality characteristics noted above, as earnings growth and free cash flow are the fuel for increasing dividend payments over time.

Differentiated exposure in the equity space

Unlike other daily liquid funds, many closed-end funds can invest in private markets that may enhance returns by accessing the illiquidity premium. The concept of “harvesting the illiquidity premium” means investors of less liquid securities are generally compensated for this additional risk, which may boost returns relative to public market securities. BlackRock believes this is a unique way of taking advantage of the CEF structure while potentially enhancing investor income and returns.

Small Cap Innovation

While there has been volatility due to inflation and interest rate worries, BII is overweight U.S. small caps. They see potential in this segment of the U.S. equity market to benefit from the cyclical rebound in domestic activity brought about by an accelerated vaccination rollout. Moreover, BlackRock believes innovation is accelerating across sectors and this could increase opportunities in small and private companies.

Megatrends

We also believe sectors like healthcare and technology are underpinned by long-term structural trends:

Healthcare: Healthcare is supported by a number of long-term secular growth drivers. Aging demographics and elongated life spans should mean increased healthcare spending in the years to come. Innovation is happening across the industry, in areas such as drug development, digital technology and next generation medical devices. Emerging market countries are likely to increase their healthcare spending as their economies grow. All these factors may support long-term growth in the sector.

Technology: Technology has long been a driver of growth in investors’ portfolios. While technology stands alone as a sector, it permeates companies throughout the broader equity market. The use of technology is reshaping industries across the globe, creating unique growth opportunities and a strong structural backdrop for potential long-term growth in the sector.