Chief Economist Scott Brown discusses current economic conditions.

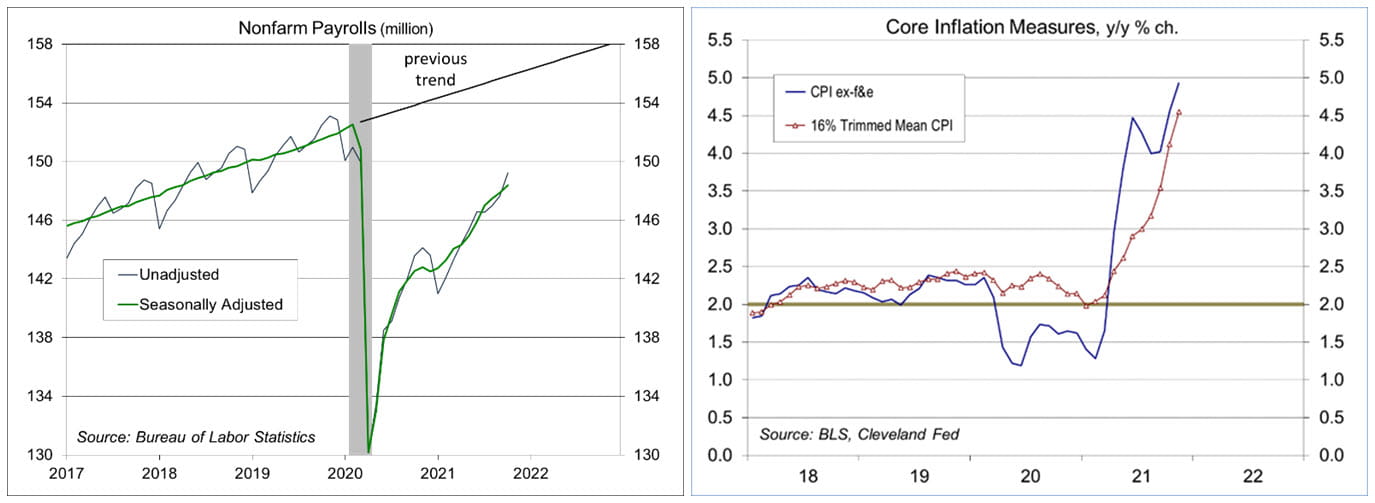

In his congressional testimony of November 30, Fed Chair Powell seemed to shift from cautious to hawkish. However, the evolution of the inflationary outlook had been underway for a while. The spike in inflation in the spring was narrow, the gain concentrated in a few categories. In contrast, the October Consumer Price Index report noted that the 0.9% increase in the headline figure was “broad-based.” The Trimmed-Mean CPI also reflected a wider range of component price increases, a sign that inflation was becoming more rooted. That is especially troublesome for Fed policymakers. The November CPI report reinforced the view that higher inflation has broadened out.

A month ago, financial market participants reacted to the stronger-than-expected CPI increase, but most missed the key point. It wasn’t that inflation was running higher than anticipated. The real concern is that higher inflation is becoming more rooted. Price hikes have broadened across categories. This was corroborated by the Fed’s Beige Book (December 1), which reported that “prices rose at a moderate to robust pace, with price hikes widespread across sectors of the economy.” In November, the CPI rose an additional 0.8% (+6.8% y/y), “the result of broad increases in most component indexes,” according to the Bureau of Labor Statistics.

The Beige Book noted “wide-ranging input cost increases stemming from strong demand for raw materials, logistical challenges, and labor market tightness, although “wider availability of some inputs, notably semiconductors and certain steel products, led to easing of some price pressures.” More troublesome, “strong demand generally allowed firms to raise prices with little pushback.” A lack of pricing power has been a long-standing fixture of the U.S. economy, and has been especially problematic for manufacturers (who have often faced higher input costs in recent decades and greater competition from cheaper imported finished goods). An increase in pricing power, as appears to be happening, would reinforce higher inflation.

The labor market is far from fully recovered, but labor market conditions are tight. Labor force participation is a major uncertainty in the 2022 economic outlook. We saw an uptick in participation in November, following little change over the 12 previous months. Dependent care issues (mostly childcare, but also elderly care) have been a constraint, and while we should see some improvement, this will continue to be a factor in 2022. Higher wages could help to keep older workers from retiring, but a gray wave is likely to continue regardless. We could be surprised, but labor force participation seems unlikely to return to pre-pandemic levels.

The inflationary impact on households appears mixed, but mostly negative. Many firms are not expected to raise wages at the same pace as the CPI. In the University of Michigan’s consumer sentiment survey through mid-December, a quarter of households indicated “an inflationary erosion in living standards.” A reduction in purchasing power may be a restraint on consumer spending growth in 2022. The UM’s survey also showed strong improvement in sentiment for those in the bottom third of income earners (while sentiment for middle-income and low-income households declined). Job hoppers stand to gain in the current environment and those at the lower end of the income scale (who are more likely to move from job to job) are more likely to see wage gains.

Over the last four decades, union membership has declined in the private sector and there is a greater concentration of large firms. Wage bargaining power has shifted from workers to businesses. However, the Beige Book noted “robust demand for labor but persistent difficulty in hiring and retaining employees.” Even before the pandemic, many firms had increased non-wage efforts to attract new workers, offering signing bonuses and increased perks in lieu of higher wages. Such efforts have expanded this year, but there are limits. Part of the recent push for labor unions at Northern New York Starbucks was precipitated by the fact that more-tenured workers were getting paid the same as new hires.

Needless to say, there are a lot of uncertainties in the labor market’s impact on inflation in 2022 and the outlook can shift quickly.

For the Fed, the broadening of higher inflation is worrisome. We can expect to see a faster tapering of the asset purchases (now likely to end in March, rather than in June), but that should already be factored into the markets. The focus is then on the next step. Fed officials are likely to pull forward their expectations for the lift-off in short-term interest rates. The Fed often employs Open Mouth Operations. Talking tough on inflation should push the markets to factor in tighter policy, before the Fed actually tightens.

Recent Economic Data

The Consumer Price Index rose 0.8% in November (+6.8% y/y), up 0.5% (+4.9% y/y) ex-food and energy. The report noted that the November increase reflected “broad increases in most component indexes, similar to last month.” Gasoline prices rose 6.1% (+2.8% before seasonal adjustment, +58.1% y/y, vs. -16.6% y/y a year ago). Food prices rose 0.7% (+6.1% y/y). Used vehicle prices rose another 2.5% (+31.4% y/y), while new vehicles rose 1.1% (11.1% y/y). Owner’s Equivalent Rent is tracking higher (a 5.6% annual rate over the last three months)

The Trimmed-Mean CPI, which excludes the 8% lowest and highest of monthly changes in CPI components rose 0.5% in November, up 4.6% y/y.

Real (inflation-adjusted) average hourly earnings fell 0.4% in November, down 1.9% y/y.

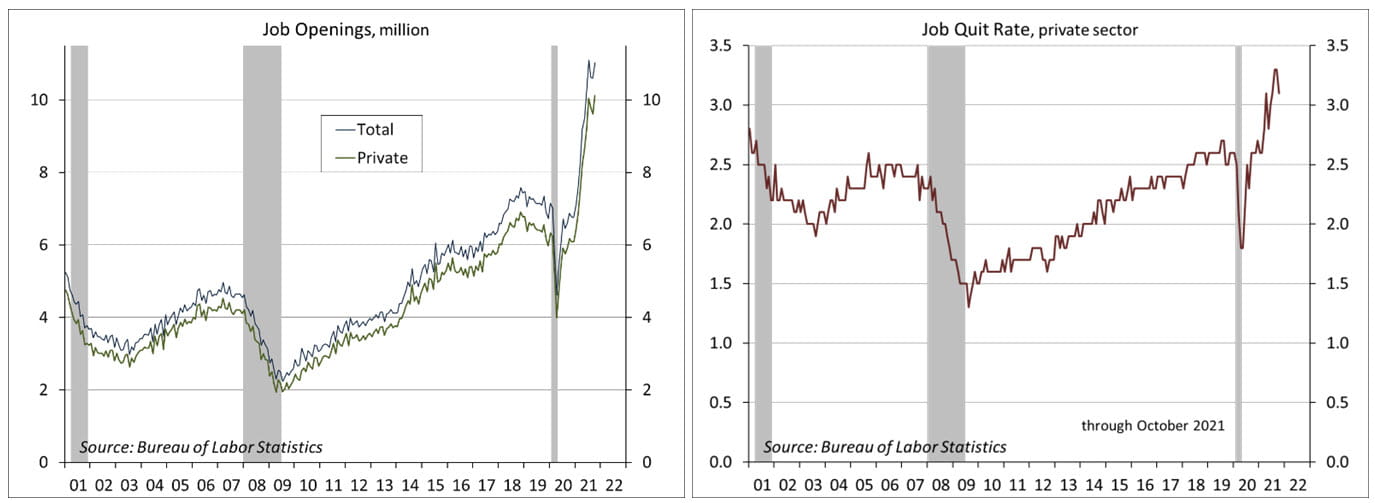

The quit rate edged back to 2.8% (3.1% for the private sector, still elevated and reflecting ongoing difficulties in retaining workers – 4.2 million quit their jobs in October.

The Job Opening and Labor Turnover Survey showed Job openings rebounded to 11.0 million in October (10.1 million for the private sector), following 10.6 million (9.6 million for the private sector) in September. Openings hit a record 11.1 million (10.0 million private sector) in July.

The U.S. trade deficit narrowed to $67.1 billion in October, vs. $81.4 billion in September.

Gauging the Recovery

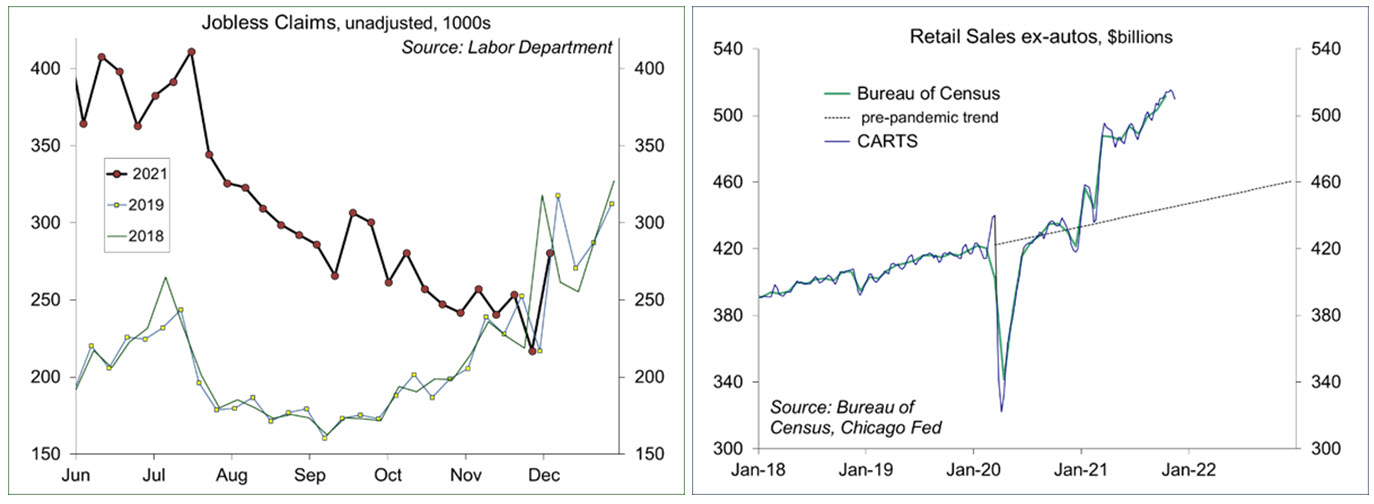

Jobless claims fell by 43,000, to 184,000 in the week ending December 4, the lowest since September 1969. Claims are now back to the pre-pandemic level, consistent with a tight labor market.

Chicago Fed Advance Retail Trade Summary (CARTS): down 0.8% in the fourth week of November, following a 0.2% drop in the previous week. November retail sales (ex-autos) were projected to rise 0.4% from October.

The New York Fed’s Weekly Economic Index fell to 7.28% for the week ending December 4, vs. +7.89% a week earlier (revised from 7.65%). The WEI is scaled to y/y GDP growth (+4.9% y/y in 3Q21).

Breakeven inflation rates (the spread between inflation-adjusted and fixed-rate Treasuries) suggest expectations of higher inflation in the near term, but moderate inflation over the long term.

The University of Michigan’s Consumer Sentiment Index rose to 70.4 in the mid-month assessment for December (vs. 67.4 in November and 71.7 in October), within the narrow range of the last several months. Those in the lower third of income earners reported strong gains, but sentiment for middle-income and upper- income households declined. A quarter of respondents noted “an inflationary erosion in living standards.”

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

© Raymond James

Read more commentaries by Raymond James