With the emergence of the omicron variant, the market narrative has once again shifted back to COVID case counts and transmission rates. This is understandable. Recent developments have the potential to upend the prevailing optimism for a slow return to normal. That said, stocks have been rattled by more than renewed fears of the pandemic. Investors are also contending with a surge in interest rate volatility. Going forward, the direction of rate volatility will likely be the other big driver, along with earnings, of equity market performance.

But while risky assets continue to advance, assets used to hedge risk are struggling. Unlike 2020, when stocks and bonds rallied together, this year hedges have cost you. Both Treasury bonds and gold are down as investors wrestle with inflation and the prospect of less benign monetary policy. To the extent this is likely to continue, I would reiterate my preference for a long dollar rather than long Treasury hedge.

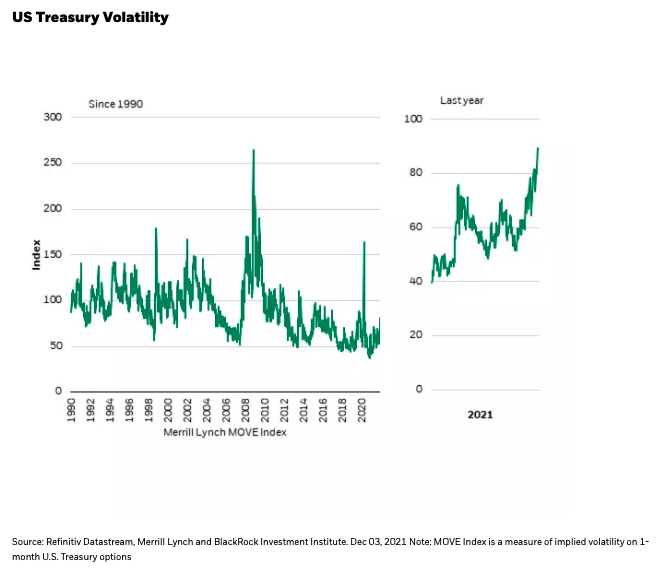

Unease in rate land

After fading last summer, rate volatility has once again surged. In recent weeks the MOVE Index, which tracks implied volatility on Treasury options, has risen by nearly 40% (see Chart 1). This is one of the reasons equities have struggled and speculative growth stocks, which tend to be hyper-sensitive to interest rates, fell more than 20% from their November peak.

US Treasury Volatility

As I discussed in September, while stocks can and often do rise in tandem with rates, violent spikes in interest rates are different. Investors tend to look past a gentle rise in bond yields, particularly when it is occurring against a backdrop of a strengthening economy. However, violent spikes in rates lower the premium investors are willing to pay for equities. Put differently, volatility that emerges in bonds tends to eventually spread to stocks.

Today equity investors are particularly sensitive to bond market machinations. Investors are struggling with the highest inflation in decades and a still evolving Federal Reserve reaction function. As a result, rate and equity volatility have become more correlated. In 2019, a year in which investors worried more about growth than inflation, the beta of equity volatility to bond volatility was roughly 0.60. This year, the beta has risen to 0.80. In other words, equity markets react with about one-third more volatility when rate volatility rises.

When rate volatility rises, pushing equity vol higher, this in turn hurts stocks by reducing the price investors are willing to pay for a stream of earnings. One way to measure this dynamic is to compare the equity risk premium (ERP), the premium investors demand in earnings yield compared to bond yields, to market volatility.

During the past year the two have become more intimately connected. Periods of higher volatility have increasingly correlated with a higher risk premium. Looking at the past year of data, changes in equity volatility have explained roughly 60% of changes in the ERP. In other words, when rising rate vol leads to higher equity vol investors demand a larger discount to buy stocks.

Maintain long dollar and high-quality cyclicals

For investors looking to hedge this risk, I’d offer two potential solutions: remain overweight the dollar and long high-quality cyclical names versus classic defensive stocks. The dollar’s positive correlation with rate volatility helps on days when interest rates spike. The long cyclical position puts you on the right side if inflation stays elevated and bond markets uncertain.

Russ Koesterich

Portfolio Manager

Russ Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and the lead portfolio manager on the GA Selects model portfolio strategies.

© BlackRock

Read more commentaries by BlackRock