The Price You Pay for Climate Policies: Understanding IMO 2020

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn January 2020, a little-known rule went into effect that today regulates the kind of fuel maritime shipping vessels are allowed to use. Conceived of by the United Nations’ International Maritime Organization (IMO), the rule, known as IMO 2020, caps the amount of sulfur in carriers’ fuel at 0.5%, dramatically below the previous limit of 3.5%.

Although not considered a direct “greenhouse gas” like carbon dioxide and methane, sulfur can contribute to the formation of aerosols, which are believed to affect the earth’s climate. (As some of you might remember, the U.S. effectively banned the use of chlorofluorocarbon (CDC) aerosol cans back in 1978 out of concern for the ozone.)

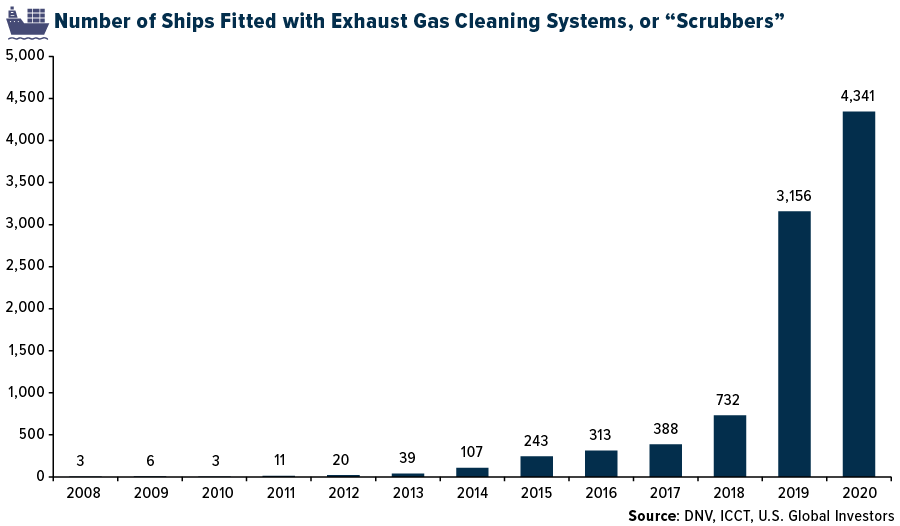

Under IMO 2020, vessels are permitted to use dirtier bunker fuel only so long as they have “scrubbers” installed, but these exhaust gas cleaning systems aren’t cheap. Depending on the ship’s age, they can cost anywhere between $2 million and $6 million per vessel.

That price tag doesn’t factor in the opportunity cost of having a vessel out of service while the scrubber is being installed, not to mention the ongoing maintenance and hassle of disposing of the waste chemicals, which ultimately end up in a landfill anyway.

Nevertheless, many cargo shipping companies are opting for the scrubbers to avoid having to buy the pricier 0.5% stuff. According to the U.S. Energy Information Administration (EIA), there’s currently a $20-per-barrel differential between very low sulfur fuel oil (VLSFO) and high sulfur fuel oil (HSFO), a not-insignificant amount. When you consider that a typical Panamax-class vessel can hold up to 2 million gallons of fuel, that extra $20 really adds up.

Good Intentions, Unintended Consequences

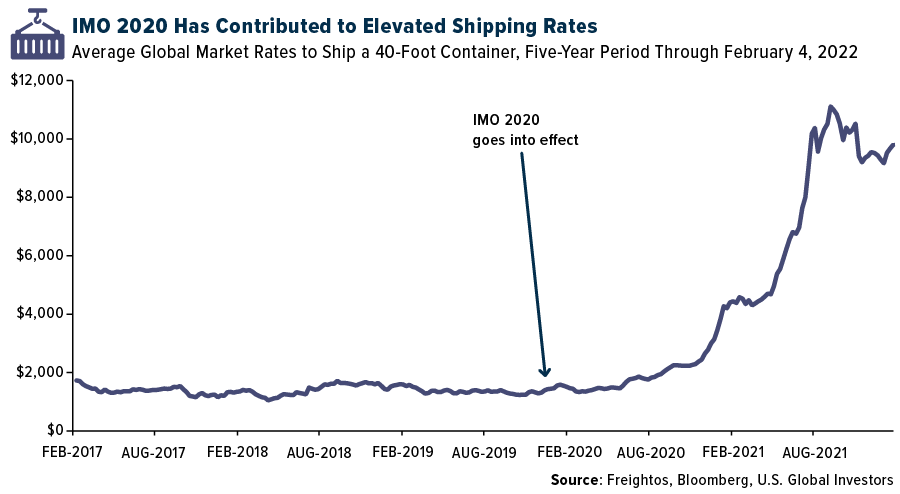

My reason for sharing this with you is that, as is often the case, policymakers’ intentions may be good, but there are always unintended consequences—including additional costs that get passed on to customers and eventually consumers. I believe IMO 2020 has contributed to shipping rates that have remained elevated for over a year now, the other contributors being the pandemic, consumers’ increased demand for goods and the ongoing semiconductor chip shortage.

As I’ve said before, there’s no free lunch on the periodic table. Cutting out carbon, sulfur and other potentially harmful elements is highly inflationary, and unfortunately it’s everyday families and small businesses that end up paying the price.

Just ask European households, who are facing record-high energy prices. Consumers in Poland right now are reportedly being told that their exorbitant electricity bills are the result of the European Union’s draconian climate policies.

And this could just be the beginning. Last year saw the fewest oil and gas discoveries in 75 years as investment has dried up, according to energy research firm Rystad Energy. Chevron CEO Mike Wirth believes $100-per-barrel oil could be right around the corner.

Interestingly, Germany’s insistence on closing its nuclear power plants—which have provided the country with clean, carbon-free energy for decades—has made the country even more reliant on natural gas, a fossil fuel, imported from Russia. Putin, a former KGB agent, need not fire a single shot in his feud with the West; his financing of foreign non-governmental organizations (NGOs) that focus on climate policy is an effective enough tool in sowing division and instability.

I’m not against the energy transition, but I worry it’s being undertaken without first bringing adequate technologies online to replace traditional fossil fuels. In many cases, climate laws and policies are written and enacted by officials, often unelected officials, who have little understanding of science and engineering.

Container Shipping Companies Notch Their Best Quarter Ever… But Not Everyone Is Thrilled

It’s not like we didn’t anticipate higher shipping rates as a result of IMO 2020. Before the rule went into effect, analysts at Wood Mackenzie predicted that rates would increase as “the marine sector uses more costly fuels, which has wide reaching consequences across the global economy. The impact could be felt from mid-2019 onwards and last for a few years, as the refining and shipping sectors adapt.”

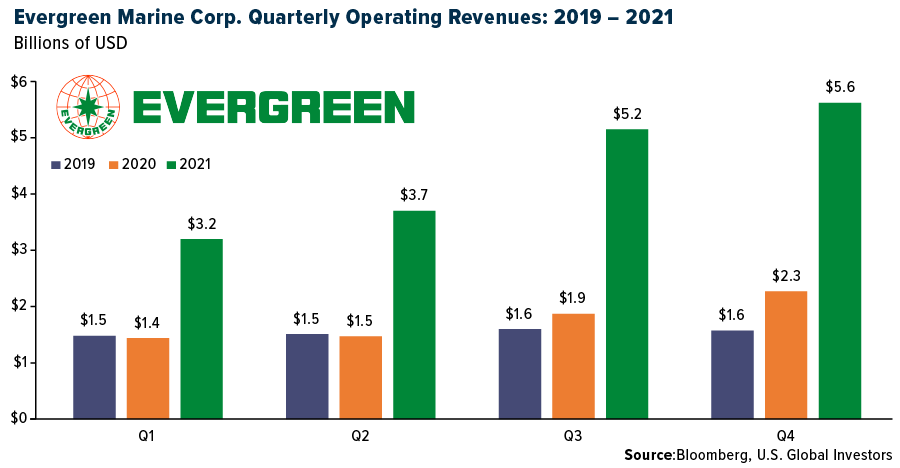

Due to higher rates, the global container shipping industry had its best quarter ever in the final three months of 2021, with massive gains recorded by industry leaders Maersk, Hapag-Lloyd, Evergreen, COSCO and others. Below you can see Taiwanese carrier Evergreen’s 2021 operating revenues compared to the two previous years.

For the full year, the group is estimated to have reached a combined $150 billion in net income, an unprecedented amount.

Amazingly, some business groups, activists and lawmakers are now taking aim at shipping companies’ profits, accusing them of charging “abusively high fees.” So in essence, the same people who helped create the conditions for higher rates oppose the idea of container companies profiting from those higher rates.

Their opposition looks even more misplaced when you find out what carriers are doing with those profits. As I shared with you last month, many of them are rewarding not just their executives but also their rank-and-file workers, with some employees seeing a year-end bonus that was 30 times their monthly salary.

Shouldn’t that be a thing to be celebrated?

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.05%. The S&P 500 Stock Index rose 1.80%, while the Nasdaq Composite climbed 2.38%. The Russell 2000 small capitalization index gained 1.81% this week.

- The Hang Seng Composite gained 4.23% this week, while Taiwan was down 2.99% and the KOSPI fell 7.64%.

- The 10-year Treasury bond yield rose 14 basis points to 1.92%.

Airline Sector

Strengths

- The best performing airline stock for the week was Aeromexico, up 34.2%. European airline bookings, as a percentage of 2019 levels, were broadly stable throughout the week but showed a double-digit increase overall. Intra-Europe net sales declined by three points to -59% versus 2019 levels (and versus -56% in the prior week) but increased by 11% this week. International net sales remained at -63% versus 2019 (and versus -63% in the prior week) and grew by 13% this week.

- Recent data shows that both domestic and international booking volumes improved to -27.4% versus 2019 levels (and versus -30.4% last week) and -39.7% versus 2019 levels (versus -44.0% last week), respectively. Similarly, domestic leisure (tickets sold through online channels) improved modestly to -16.1% versus 2019 levels (versus -17.7% last week). A positive sign is that pricing improved in the channels by 4-5% from last week, which is an optimistic sign after pricing dropped to start the new year.

- The Federal Aviation Administration (FAA) announced progress in expanding 5G service at airports. Late last week, the FAA announced that it reached an agreement with Verizon and AT&T on how to allow more aircraft to safely use key airports while also enabling more towers to deploy the new 5G service. According to the FAA, the two wireless companies provided more data about the exact location of wireless transmitters. The FAA was able to use this data to determine that it is possible to map the size and shape of the areas safely and more precisely around airports where 5G signals are mitigated, decreasing the areas were AT&T and Verizon are deferring their antenna activations.

Weaknesses

- The worst performing airline stock for the week was Skywest, down 21.1%. U.S. airlines’ trailing seven-day website visits were flat this week at -4%. Many U.S. carriers’ website traffic decelerated for the second straight week. With airline operations stabilized at this point and omicron case counts peaking, website visits will pick up ahead of spring/summer travel.

- Bank of America lowered its Ryanair 2023 estimated EBIT by 8% as the company cut its load factor to 91% for fiscal year 2023, in-line with comments in the earnings call. The bank forecast Ryanair’s 2023 fares in-line with fiscal year 2020. Omicron has negatively impacted January and February bookings, and Ryanair continues to price aggressively to support a recovery in loads, with a potential recovery from mid-February onwards.

- Airlines that aren’t currently hedging their fuel bills are set to lose a lot of money as a result of high oil prices, the head of Ryanair Holdings Plc said Monday. Brent crude is trading near $91 a barrel as surging global consumption pushes prices to a seven-year high. That’s problematic for fuel-consuming industries like airlines, where oil can make up their single biggest cost. Airlines typically use oil swaps and options to cap, or hedge, their fuel bills when crude prices surge. But many carriers lost billions of dollars in the oil market when the pandemic brought flying to a near-halt globally. There was little-to-no fuel demand to offset loss-making derivatives positions, and as a result some have either stopped hedging or scaled back their volumes.

Opportunities

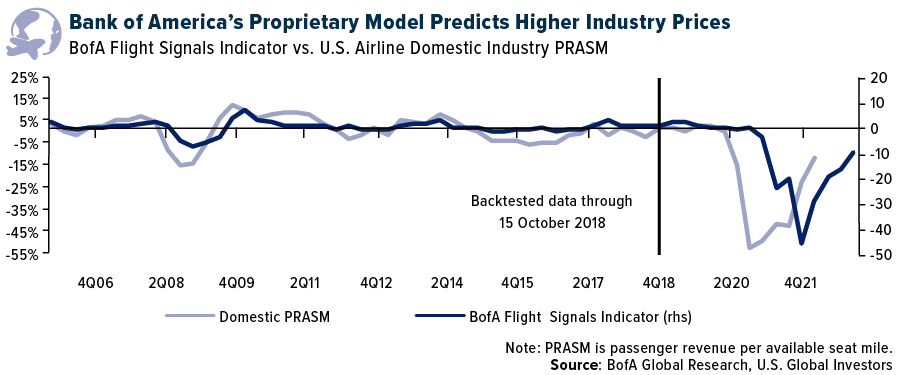

- Bank of America’s proprietary price indicator showed slower unit revenue growth in the first quarter of 2022, which is in line with airlines that have reported fourth quarter 2021 earnings and provided first quarter 2022 outlooks. This quarter, the bank’s latest forward indicator improved to -9.9 from -16.9 (and -19.8 in the second quarter of 2021), showing a stronger rebound in industry domestic unit revenues into the second quarter of this year.

- The U.K. government formally ended all travel restrictions for vaccinated arrivals last week after scrapping the requirement for day-2 antigen tests. This is the first time that no testing has been required since early 2020, which should boost U.K. bookings. The EU has advised member states to remove its country-based travel restrictions from February, re-introducing digital COVID certificates which supported a big recovery in travel last summer.

- Omicron case counts have peaked and the trough of the omicron impact on bookings data is past us as there have now been improvements for three straight weeks. System net sales are -54.8% versus 2019 for the week (versus last week at -60.3%) and seem to have troughed in early January. Demand should be driven by a strong consumer into the peak spring/summer travel season.

Threats

- All EU countries have agreed to use the same amount of time since a person’s last vaccination (270 days or nine months maximum) for them to be considered fully vaccinated. After nine months, people will need to receive a booster shot in order to keep their vaccinated status and travel freely within Europe. This will be enforced beginning February 1, 2022.

- The Nor’easter caused thousands of cancellations over the weekend. The Alpha Wise Flight Tracker indicated that 4,500 flights from nine of the major U.S. airlines were canceled from January 24 to January 30, which was 5% of scheduled flights (versus 2.1% the previous week). Unsurprisingly, most of these cancellations occurred over the weekend due to severe winter storms in the Northeast (6% of scheduled flights on Friday, 19% of scheduled flights on Saturday, and 7% of scheduled flights on Sunday were canceled). Overall, in the U.S., around 7,800 flights were canceled in the past week, 85% of which happened over the weekend.

- According to Bank of America, valuations across the group remain elevated versus history with all airlines trading in the upper end of historical valuation ranges, and multiples are a bit higher than the start of the year as estimates have come down due to higher fuel and other operating costs. However, airline multiples typically follow revenue momentum, and with omicron fading and travel demand recovering in the coming weeks/months, they believe this will be enough to support valuations towards the higher end of historical ranges.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was the Czech Republic, gaining 2.3%. The best performing country in Asia this week South Korea, gaining 4.0%.

- The Hungarian forint was the best relative performing currency in emerging Europe this week, losing 4.0%. The Pakistani rupee was the best performing currency in Asia this week, gaining 1.3%.

- January Manufacturing PMIs remain strong in Europe. The Eurozone reported Manufacturing PMI at 58.7, well above the 50 level that separates growth from contraction. Within central emerging Europe countries, the Czech Republic released the strongest PMI reading of 59.9.

Weaknesses

- The worst performing country in emerging Europe for the week was Turkey, losing 2.0%. The worst relative performing country in Asia this week was Malaysia, gaining 0.40%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 0.10%. The Taiwanese dollar was the worst performing currency in Asia this week, losing 0.4%.

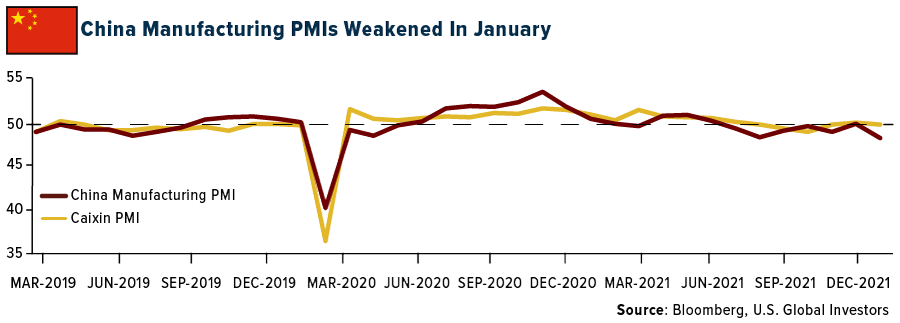

- Manufacturing activity in China has weakened. The Caixin Manufacturing PMI, which measures production among smaller private companies, crossed below 50, a level that separates growth from contraction. The China Manufacturing PMI, which measures production among larger state-owned enterprises, fell from 50.3 to 50.1.

Opportunities

- Thailand started allowing vaccinated travelers to visit the country, quarantine-free. Bangkok also lifted a nighttime curfew that was in place for four months and will now allow restaurants to serve alcohol. Thailand has become one of the first countries in Southeast Asia to reopen to tourists without requiring quarantine.

- Thailand’s $33 billion pension fund is planning to boost its equity investments in China and India. Chinese microchip manufacturers and renewable energy firms will be considered after the government listed the percentage of foreign equities in the fund from 40% to 60% last month.

- According to JPMorgan’s research team, covid cases are falling in four out of five EU5 countries, and brokers expect the rest of Europe to follow in the next months. Overall ICU occupancy is falling in France and Germany despite very high and rising case burdens. The milder Omicron variant and a high level of vaccination/boosting means that we are reaching the “endemic” phase of COVID-19 and a return to normal is possible, the broker explained.

Threats

- The Winter Olympic Games have started in Beijing. The long-awaited sporting competition that requires huge investments will not bring revenue as large as was expected. China stopped selling event tickets to the general public due to concerns about the spread of the virus. Instead, groups of spectators were invited on the site throughout the games and will be required to strictly comply with COVID-19 preventative measures and control requirements.

- Inflation keeps rising in Turkey. This week the government announced a price increase of 48.7% in January on a year-over-year basis. Core inflation spiked 39.5% year-over-year. Moreover, Turkey’s preliminary January trade deficit widened to 241% year-over-year. Peoples’ dissatisfaction with the deteriorating living conditions will likely lead to further disapproval of the ruling party.

- A growing number of Chinese companies are writing off assets or issuing profit warnings due to real estate developer problems. This week George Soros called China’s property market unsustainable, saying that its current condition could be the downfall on the country’s ruler.

Energy & Natural Resources

Strengths

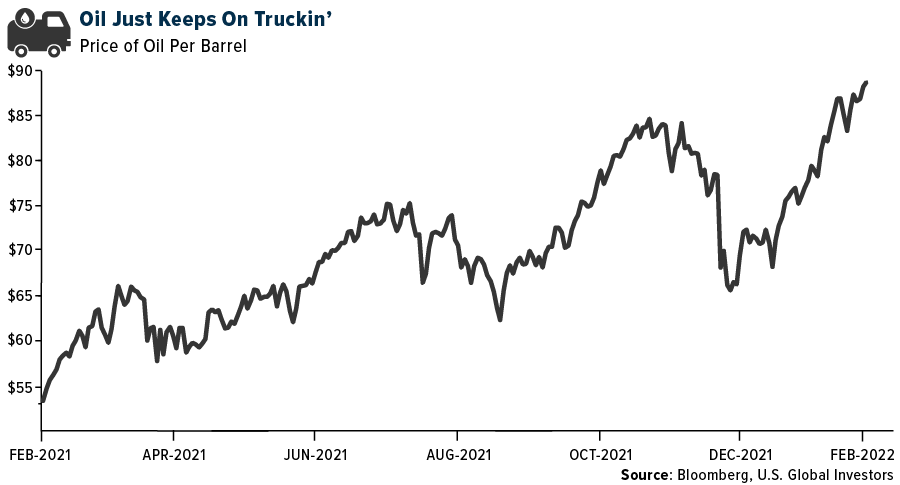

- The best performing commodity for the week was WTI crude oil, up 6.22%. Oil markets opened the week higher and were heading for the biggest January gain in at least 30 years, as robust demand outpaced fresh supply. WTI futures traded above $87 a barrel. Traders were greeted with a familiar set of drivers, from the weather to stockpiles. Low temperatures in the U.S. have been boosting demand for fuels, as Boston reported a daily snow record and New York’s Central Park saw more than eight inches fall.

- As covered in its Battery & Storage Conference, Bank of America says prices for lithium can continue momentum until late 2022. While current prices are unsustainable, the case can be made that reinvestment prices are now higher as well. This is particularly true as inflation is driving up the cost of investment, and projects are increasingly being sought further along the quality scale. The bank suspects the new long-term price is now closer to the mid-teens versus low double-digits per kilogram.

- The U.S. held the ranking for the world’s top exporter of liquefied natural gas (LNG) for a second month in a row, as Europe’s winter energy crisis draws more cargoes to the continent. U.S. LNG exports hit a record 7.3 million tons in January, taking the No. 1 spot away from Middle Eastern powerhouse Qatar for a second time since December. Europe, which is facing low winter inventories and high natural gas prices due to tensions between Russia and Ukraine, was a top destination for U.S. cargoes last month.

Weaknesses

- The worst performing commodity for the week was Bloomberg Powder River Basin 8800 Btu Coal Spot Price Fob/Gillette Wyoming, down 17.73%, as Department of Energy (DOE) data shows coal production up 11.6% for the state over the past year. European natural gas prices slumped as forecasts for milder weather and increased Norwegian flows helped calm fears of a supply crunch. The benchmark contract sank as much as 7.3% as traders expected less pressure on inventories that began winter at the lowest level on record. Warmer weather and higher flows from Norway — following an outage at the giant Troll field – will help relieve market tightness amid continuing jitters over a possible Russian invasion of Ukraine.

- Gazprom PJSC’s daily gas exports to its most important markets fell in January to the lowest since early 2015, despite higher production. Russia’s pipeline gas deliveries to Europe, which meet around a third of the continent’s demand, are in focus amid concern that flows to an already energy-starved region could be disrupted if geopolitical tensions over Ukraine escalate. The market is also closely watching for any potential sanctions that could be imposed on Gazprom’s controversial Nord Stream 2 pipeline, which is awaiting regulatory approval before it can begin operating.

- A rout in clean energy has set in, sending the iShares Global Clean Energy ETF down 11% in January. Suddenly, uranium stocks are the worst performers on the S&P/TSX Energy Index year-to-date, and all the companies in the index are down, some more than 10%, while the broader energy index is up 12%.

Opportunities

- Morgan Stanley remains bullish on energy and expects oil and gas markets to remain undersupplied for 2022 and beyond. The group suspects that by the middle of the year, the oil market will likely see three key factors simultaneously at low levels: 1) low inventories — these have fallen substantially in 2021 already, but on their estimates, will be lower still by end-2022; 2) low spare capacity — this has already come down from 6.5 mb/d a year ago to 3.4 mb/d at the moment, but they think it will likely drop below 2 mb/d by midyear; and 3) low investment, which is still close to the level of the IEA’s “Net Zero by 2050” scenario in which consumption and production are assumed to fall 30% by 2030, while actual demand shows no such trend.

- It has been a robust start to the year for U.S. large cap energy, with the XLE having outperformed the S&P by 2500 basis points on positive earnings revisions, a factor rotation and continued strengthening in the curve for oil/natural gas/refining margins. Goldman Sachs Research continues to have a bullish Brent oil view of $96/$105/$80 for 2022/2023/2024, which should support the sector earnings revisions story. In fact, the bank’s bottom-up estimates imply the energy sector will deliver 7% of the S&P’s earnings per share contribution in 2022, but currently represents only 3% of the market capitalization of the index.

- Oil output in the U.S. shale patch is “re-booming,” according to Lium LLC, as the group sees production soaring to more than 1 million barrels per day and would represent the largest expansion in output since 2018. According to Bank of America, oil may be near a short-term peak. The bank favors hedging/ trimming oil longs on rallies, or selling some covered calls, in favor of diversifying into small copper and gold longs.

Threats

- Iron ore futures in Singapore plummeted as China vowed to strengthen the oversight of prices, which surged last week to the highest level since September. The steelmaking material has been on a tear since the start of the year as expectations that China will boost infrastructure spending and further ease monetary policies brightened demand prospects. But the rally — which still puts iron ore on track to gain more than 12% in January — is starting to unnerve Beijing.

- Based on the latest annual data, approximately 60% of Russia’s merchandise exports come from oil and gas, which is only slightly less than Saudi Arabia and Iran and more than twice the level of Canada. Half of Russia’s federal budget is tied to oil and gas, leaving both the private and public sectors highly dependent on hydrocarbons exports. While Europe would suffer from a physical supply disruption that a Russia-Ukraine war would cause, Russia would take an even steeper economic hit.

- A proposal that opens the door to nationalizing some of the biggest copper and lithium mines in the world was approved in first instance by a committee as part of the drafting of a new constitution in Chile. Tuesday’s 13-to-6 vote by members of an environmental committee is the first of several hurdles that the controversial proposal would need to clear before becoming a reality. It would require support from two-thirds of the full assembly to become part of the draft charter that will be put to a referendum later this year.

Domestic Economy & Equities

Strengths

Strengths

Strengths- Initial jobless claims fell 23,000 week-over-week to 238,000, beating estimates for 255,000. Continuing claims for the week also fell 44,000 week-over-week to 1,628,000, slightly ahead of the 1,630,000 consensuses.

- Final Markit U.S. Manufacturing PMI was reported at 55.5 in January, above consensus. Service PMI was revised to the upside as well, coming in at 51.2 versus a reading of 50.9.

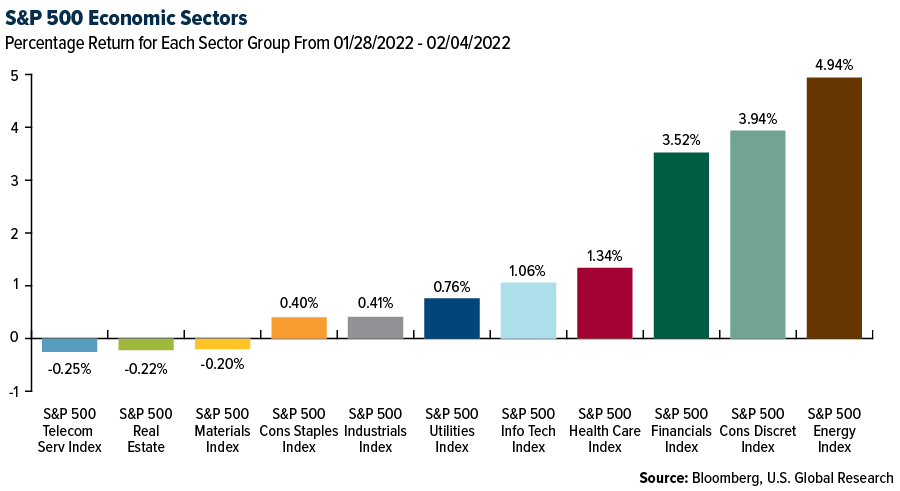

- DXC Technology, an information technology company, was the best performing S&P 500 stock for the week, increasing 22.5%. Shares gained after the company announced an earnings beat and guided for higher profits this year.

Weaknesses

- Technology stocks disappointed this week, reporting weaker quarterly results. Facebook missed fourth-quarter earnings per share and guided weaker first-quarter revenue. Shares of Facebook declined 27% on Thursday, erasing about $252 billion in market value. It was the biggest wipeout in market value for any U.S. company ever.

- According to ADP data released on Wednesday, the private sector in America has lost 301,000 jobs in the month of January. The data came as a surprise as Bloomberg economists were expecting 180,000 jobs to be added.

- PayPal Holdings, a technology platform, was the worst performing S&P 500 stock for the week, losing 22.9%. Shares declined sharply on Wednesday after the company announced disappointing earnings guidance.

Opportunities

- January nonfarm payrolls surprised to the upside despite broad expectations for a weak report reflecting Omicron drag. November and December numbers were also revised up by a net 709,000 jobs. The job market will likely continue to improve. The number of people collecting unemployment should continue to fall.

- Morgan Stanley, in a research paper entitled “The Great Inventory Rebuilding Has Begun,” said that last week’s GDP, trade, and inventories added to the mounting evidence that, while there is still a long way to go, we have moved past the worst in supply chain disruptions and inventories are meaningfully rebuilding. The rebuilding of inventories, in particular motor vehicles, is a major driver for the broker’s outlook for GDP growth in 2022.

- Bloomberg economists predict that the U.S. Michigan Sentiment index will increase to 67.6 in the preliminary February reading from 67.2 in January. The Index is a leading indicator of consumer confidence. Data will be released on February 11.

Threats

- The Bank of England hiked its rate again by 25 basis points to 50 points. Additional members of the bank are in favor of hiking rates in order to keep rising prices in check. A third hike could be next in line. The United States is preparing to shift its monetary policy as well.

- FactSet warned that earnings beat rates continue to lag recent quarters. Heading into Friday morning’s releases, nearly 55% of the S&P 500 has now reported. Just over 77% of reporters have exceeded consensus earnings per share estimates, well below the 84% four-quarter average, but largely in line with the five-year average.

- Bloomberg economists predict inflation to increase to 7.3% in January from 7.0% in December. Data will be released on February 10.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was MetaPay, rising 631.04%.

- Crypto exchange FTX has just completed another funding round that values it at $32 billion, according to Bloomberg. Founder and CEO Sam Bankman-Fried said that he does not believe there will be a long-term crypto bear market.

- After years of rejecting calls to write cryptocurrency accounting guidance because too few companies dabbled seriously in the digital asset space, the Financial Accounting Standards Board in December agreed to research the topic. The standard-setter plans to meet by mid-year to discuss the research, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Vive La Bouje, down 93.21%.

- Russia’s crypto-skeptic Central Bank appears ready to climb down over some aspects of its proposed crypto ban – but still want to ban mining, despite recent comments on the matter from President Vladimir Putin, writes CryptoNews.com.

- Bitcoin is closing out a rough month, with January declines putting the digital coin on pace for its worst start to a year since the dawn of the 2018 “crypto winter,” writes Bloomberg. According to data compiled by Bloomberg, Bitcoin has notched only 11 up days this month meaning that it has spent 65% of the month in decline.

Opportunities

- After years of wavering on its stance, India finally took a step closer to adopting cryptocurrencies. The Reserve Bank of India will launch its digital currency in the year starting April 1, said Finance Minister Sitharaman. The nation also plans to tax the income from the transfer of virtual assets at 30% she said, effectively removing uncertainties about the legal status of such transactions, writes Bloomberg.

- The Federal Reserve Bank of Boston and MIT’s Digital Currency Initiative published an open-source research software report on Thursday, according to Bloomberg. The report explains that the Boston Fed was able to develop “a core processing engine” for a general purpose CBDC that could support nearly 2 million transactions per second with high-speed settlement finality.

- Bitcoin gained the most in more than three months as investors show signs of renewed risk appetite following a volatile week across financial markets, reports Bloomberg. Bitcoin jumped as much as 7.6%, the most since October 15, and Ether climbed as much as 9%.

Threats

- Wormhole, a communication bridge between Solana and other decentralized finance blockchain networks, was hacked this week. Hackers may have drained as much as $315 million, according to blockchain forensics providers. If the amount is accurate, it would be one of the largest thefts from a DeFi protocol, writes Bloomberg.

- During the brutal crypto selloff last month volumes also tumbled. Total spot volume slumped to $1.8 trillion in January, a decline of more than 30% from the previous month, according to a report from CryptoCompare. This was the lowest turnover since the end of 2020.

- Decentralized Social token (DESO) tried to game the public into believing that it had just raised $200 million from investors like Andreesseen Horowitz and Coinbase Ventures. However, this is simply not true, reports Cryptoslate. Venture capital firms contributed less than half of the project funds, with the rest coming from retail buyers and industry insiders. Upon its listing on Coinbase, the price doubled, giving early investors an opportunity to dump the asset on unsuspecting retail investors.

Gold Market

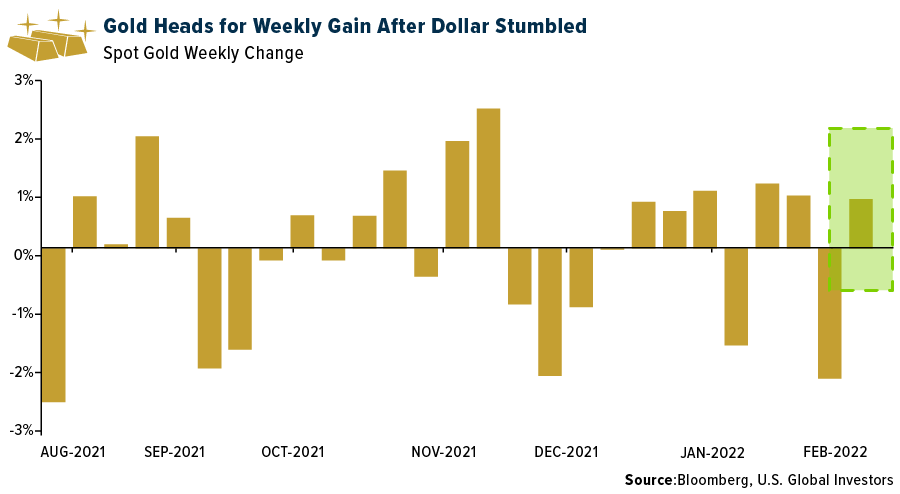

This week spot gold closed the week at $1,808.28, up $16.00 per ounce, or 0.89%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.27%. The S&P/TSX Venture Index came in up 1.93%. The U.S. Trade-Weighted Dollar slumped 1.87%.

| Date | Event | Survey | Actual– | Prior |

|---|---|---|---|---|

| Jan-29 | Caixin China PMI Mfg | 50.0 | 49.1 | 50.9 |

| Jan-31 | Germany CPI YoY | 4.4% | 4.9% | 5.3% |

| Feb-1 | ISM Manufacturing | 57.5 | 57.6 | 58.8 |

| Feb-2 | Eurozone CPI Core YoY | 1.9% | 2.3% | 2.6% |

| Feb-2 | ADP Employment Change | 180k | -301k | 776k |

| Feb-3 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Feb-3 | Initial Jobless Claims | 245k | 238k | 261k |

| Feb-3 | Durable Goods Orders | -0.9% | -0.7% | -0.9% |

| Feb-4 | Change in Nonfarm Payrolls | 125k | 467k | 510k |

| Feb-10 | CPI YoY | 7.3% | — | 4.0% |

| Feb-10 | Initial Jobless Claims | 235k | — | 238k |

| Feb-11 | Germany CPI YoY | 4.9% | — | 4.9% |

Strengths

- The best performing precious metal for the week was platinum, up 1.45% as hedge funds boosted their bullish futures positions to an 11-week high. Nornickel, the world’s largest producer of palladium and high-grade nickel and a major producer of platinum and copper, announced that the Global Palladium Fund, a metals distributor founded by Nornickel, has launched the GPF Physical Electric Vehicle Metals Exchange Traded Commodity (ETC). The Global Palladium Fund Physical Electric Vehicle ETC is being launched with $10 million of seed capital and listing initially on Borsa Italiana.

- SSR Mining’s fourth quarter production of 211,000 ounces of silver was up 13% from the previous quarter and 11% better than forecast. Estimated costs of $960 an ounce were 5% better than last quarter and 9% better than consensus. Full-year production of 794,000 ounces silver was at the high end of guidance, while 2021 costs of $982 an ounce were below the low end of revised guidance of $1,000 an ounce.

- Gold extended its gains as the dollar weakened after U.S. Federal Reserve officials played down prospects of aggressive rate hikes coming imminently. The dollar ticked lower amid the positive risk sentiment. Gold regained the psychologically important $1,800 an ounce mark, just above the level it averaged last year.

Weaknesses

- The worst performing precious metal for the week was palladium, down 3.57%, as hedge funds boosted their bearish futures positions to an 11-week low. AngloGold Ashanti Ltd. saw a drop in full-year earnings, hit by rising costs and lower gold sales, after it suspended activities at a key mine in Ghana following an underground incident. Headline earnings per share in the 12 months through December are likely to decline 36% to 42% year-on-year, the Johannesburg-based gold miner said. AngloGold expects total basic earnings per share will be down 32% to 39%, it said in a statement. The company’s earnings were eroded by lower gold sales, higher operating costs and an increase in sales costs due to lower grades. This was also worsened by “inflationary pressures and the continued impact of the Covid-19 pandemic on costs,” it said.

- According to Stifel, with inflationary cost pressures being reflected in higher 2022 cost guidance for most, if not all, mining companies, they have reviewed their operating and capital cost assumptions for several companies under coverage. For those companies for which adjustments were made, the net impact has been higher costs translating to a lower NAV per share, and in some cases a lower target price.

- Gold shipments from Europe’s key refining hub fell to 97.2 tons last month from 129.0 tons in November, according to the Swiss Federal Customs Administration. Shipments to China fell 63% to 14.5 tons. Sales to India slid 27% to 28.3 tons.

Opportunities

- Anglo American Platinum Ltd. said that it sold its 50% interest in the Kroondal and Marikana Pool-and-share Agreements to Sibanye-Stillwater Ltd. for one rand ($0.06). The South African miner said the conditional transaction will extend the project’s life-of-mine, and that Sibanye will take over all closure costs and rehabilitation liabilities. “By enabling Kroondal to mine through the boundary at Sibanye-Stillwater’s Rustenburg operations, we will extract our attributable share of the Kroondal reserves more quickly and efficiently than under the previous mine plan, unlocking greater value for Anglo American Platinum and Sibanye-Stillwater,” the company said.

- Perseus Mining announced it has acquired a 15% interest in Orca Gold, which owns 31.5% of Montage Gold. Perseus noted it has engaged in exclusive discussions with Orca to buy the company. In the press release, it stated, “Orca potentially provides Perseus with exposure to two highly prospective assets with significant resource bases and is consistent with Perseus’ strategy of building a platform of long life, highly profitable African gold assets.”

- A senior gold-mining executive sees the potential for a record year of mergers and acquisitions as companies turn to deals to prop up production at a time of rising bullion prices. An M&A cycle that kicked off with Barrick Gold’s 2018 takeover of Randgold followed by Newmont Corp.’s purchase of Goldcorp is only just beginning, said David Garofalo, the former Goldcorp boss who now oversees Gold Royalty Corp. In the past decade and a half, the industry has been focused on strengthening balance sheets and paying dividends, resulting in a depletion of reserves. To avoid that turning into a production slump, companies will scoop up more single-asset players, Garofalo said in an interview Monday. At the same time, the prospect of accelerating inflation and higher interest rates will drag money out of equity markets and into safe havens, with gold potentially reaching $3,000 an ounce as soon as this year from about $1,800 now, he said.

Threats

- From explosives experts to truck drivers, labor shortages are becoming an increasing challenge for mine operators across Western Australia after the state abandoned plans to end Covid-related border controls. The state’s resources industry, which is a crucial source of revenue for Australia, relies on flying in workers to remote sites. Many of the workers come from other states and it has become increasingly difficult for them to travel given border restrictions enforcing quarantine on arrival in Western Australia, which is more than three times the size of Texas and comprises of barren Outback.

- Resource Capital Funds (RCF), a 5.2% shareholder of IAMGOLD, has commenced an activist campaign, including the release of a critical letter sent to IAMGOLD’s Board and the nomination of at least three new directors. Impact: RCF’s actions seek to assert changes which could institute a framework for IAMGOLD’s turnaround and improve upon the company’s current and historical challenges. In their view, IAMGOLD’s asset base does not clearly outline a value proposition based upon current published technical information, and fundamental upside in a turnaround would be contingent upon the execution of the Cote Gold project development, an improvement or divestiture of IAMGOLD’s operating asset base, and elevated gold prices being sustained. RCF maintains a reputation of being an established technical mining private equity group, although public equities’ shareholder activism is atypical for the group.

- Diesel margins are surging around the world, as reported by Bloomberg, amid low stockpiles and supply pressures. Heavy industries, like gold mining, farming and rolling military gear in Eastern Europe, are all vulnerable to the shortages. Traders are also factoring in higher prices for forward prices too as the bottlenecks to production could tighten.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits