The start to the year has seen investors heading for the exits as an increasingly hawkish Federal Reserve begins winding down asset purchases and has signaled that it may start raising interest rates sooner and faster than expected. Selling has been widespread, but small caps have taken the brunt of the pain as some have speculated that larger companies would be better positioned to ride out the storm caused by higher interest rates.

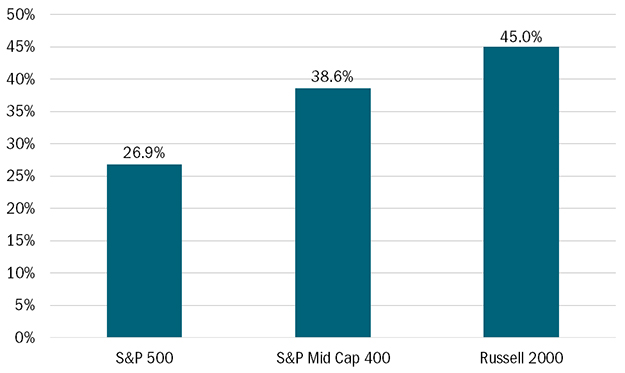

But is that the right move? If history is any guide, the answer may be not necessarily. The beginning of the last hiking cycle started in the fourth quarter of 2015. The initial move spooked investors and equities tumbled, bottoming in February 2016. What followed, as the chart below shows, was a watershed year for shares of smaller companies.

1-Year Total Return from February Lows 2016

Source: Standard & Poor’s and Heartland Advisors, Inc., from 2/11/2016 to 2/10/2017. The data in this chart represents the total return of the S&P 500, S&P Mid Cap 400, and Russell 2000 for one year starting in February of 2016. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

While rising rates don’t always trigger relative outperformance for small and mid-caps—the 1999 tightening cycle being the most recent example—we view valuations as adding fuel for a potential run. Profitable companies found in the S&P 400 and Russell 2000 indices are trading at discounts to the levels they were during the last tightening sell-off in early 2016. Conversely, in late January of 2022, counterparts in the S&P 500 were trading at a roughly 25% premium based on price/earnings than they were six years ago.