As investors look for ways to protect their investment portfolios from market shocks, finding the most efficient hedging instrument becomes a top priority. Clearly, hedging the risks of a 100 stocks portfolio with sector-based ETFs is more efficient than hedging it with single stock options or S&P 500 Index option/ETF.

Below we will present our analysis in support of the above statement.

We will start with reminding that ETFs are a composite of securities traded on the stock exchange and tracking underlying indexes posted on exchanges such as the Nasdaq, the New York Stock Exchange (NYSE), and others.

First, securing a portfolio through hedging each and every security in a portfolio is expensive. Let us assume, we have a portfolio of one hundred securities. First, such hedging is usually done by purchasing the put options. Thus, along with paying a commission for each transaction with these 100 securities, an investor pays the price of options relative to the price of the hedged securities, which, as a rule, is greater than the cost/price proportion for an ETF.

This is exactly the reason why hedging a portfolio of securities with options, or even hedging each individual portfolio security is not a feasible exercise. Therefore, we must examine why hedging portfolios with sectors-based ETFs is more effective than hedging with a general index such as SPY option.

Due to specific features of these financial instruments, it is almost impossible to collect easy-to-prove statistics on the historical series of an option on SPY and on sector-based ETFs. So, we will do our analysis based on the comparison of three portfolios of securities with similar long positions generated by portfolio visualizer with the start date 07.01.2016 and ending on 02.14.2022.

Portfolio 1 is a long-only, unhedged portfolio; long Portfolio 2 is hedged with SPY ETF Trust on 100% of long portfolio; and long Portfolio 3 is hedged with 6 sector-based ETFs, replicating the portfolio geometry of sector-based ETFs.

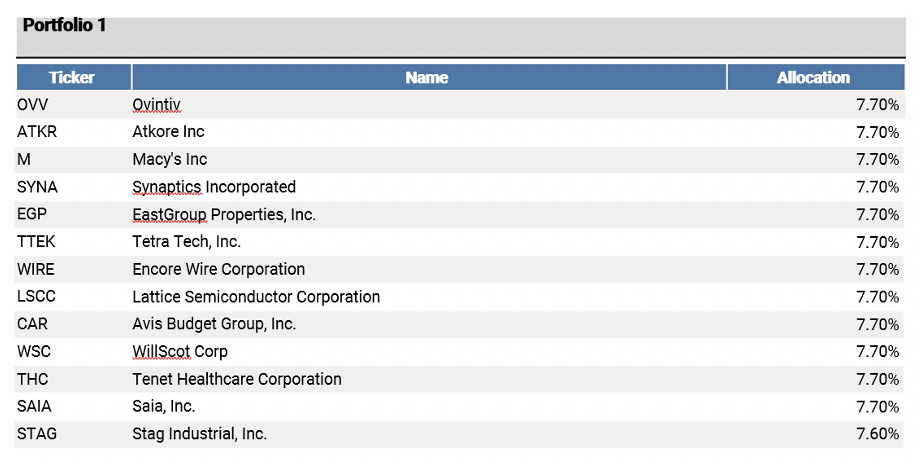

Chart 1: Equally weighted, long-only, unhedged portfolio table and diagram

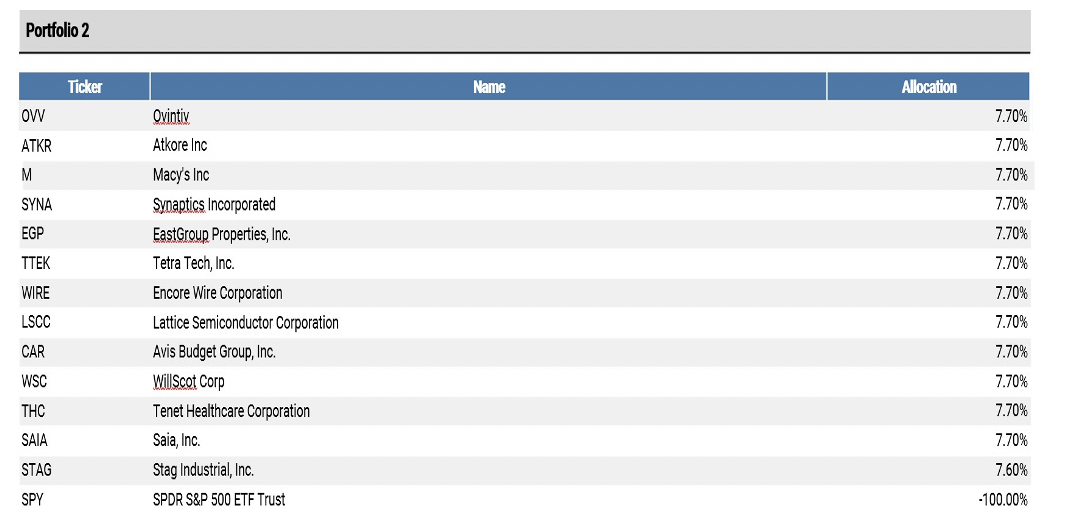

Сhart - 2: Portfolio 2 hedged with SPY ETFs

When we analyze Portfolio 2 calculation, it becomes apparent that:

- The sector structure followed by the senior global index differs from the sector structure of Portfolio 2.

- Types of businesses, their capitalization rate and capitalization weighted index covered by the senior global index are different from Portfolio

- Inconsistency also occurs because Portfolio 2 of securities from several sectors (let us say, health-care industrial and consumer) is hedged, for example, through options on the S& P500. Applying several industry-specific ETFs replicating the structure of such a portfolio becomes a more viable hedge in this case.

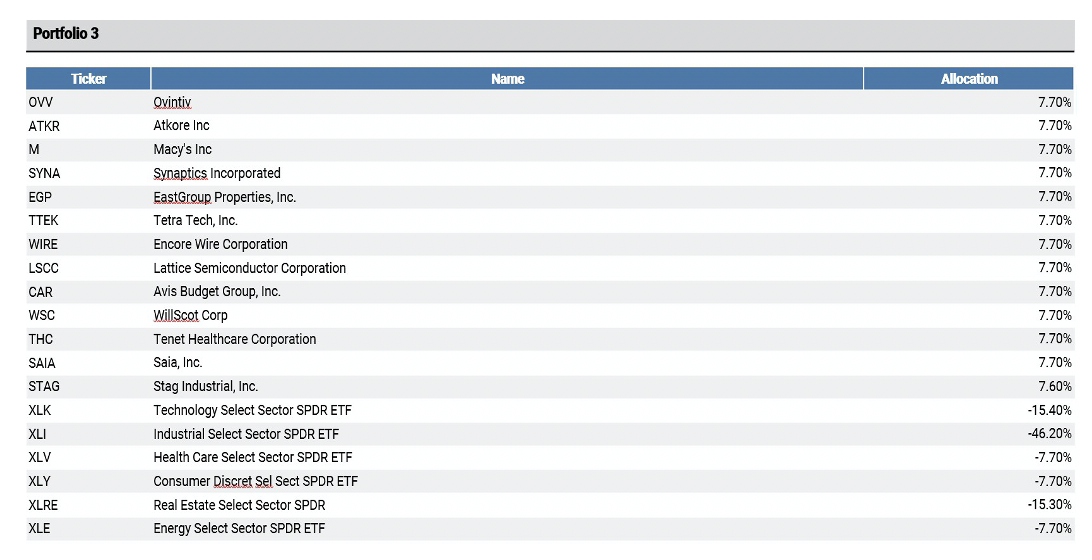

The third chart depicts a portfolio hedged with sector-based ETFs. The same securities forming long positions are assigned a specific weight factor in the portfolio.

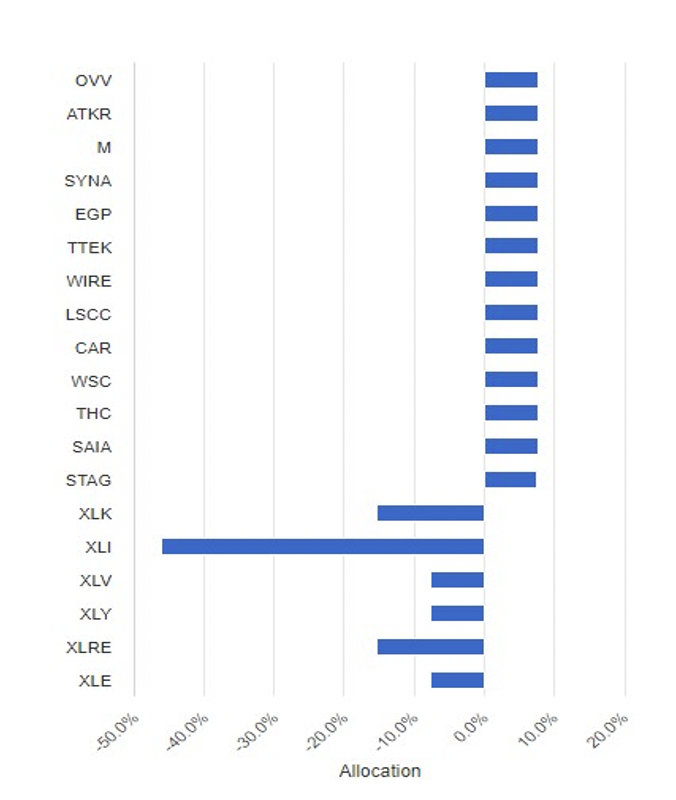

Chart 3 – Portfolio 3 hedged with sector-based ETFs

Thus, we get a chart with a breakdown of weights. For example, the technology sector is covered with -15.40%; health care industry with -7.70%; industrial sector with -46.20%; consumer industry with -7.70%; real estate sector with – 15.30%; and energy sector with -7.70%. We will single out the most liquid sector-based ETFs that correspond to the specific sectors. As we can see from the chart above, they are XLK, XLI, XLV, XLY, XLRE, and XLE.

And, now we will take, 10,000 US dollars allocated in our portfolio of long positions and calculate the portfolio performance by applying these ETFs weight ratios to the securities corresponding to each of six sectors. Thus, we will have built our long-hold portfolio based on ETF replication.

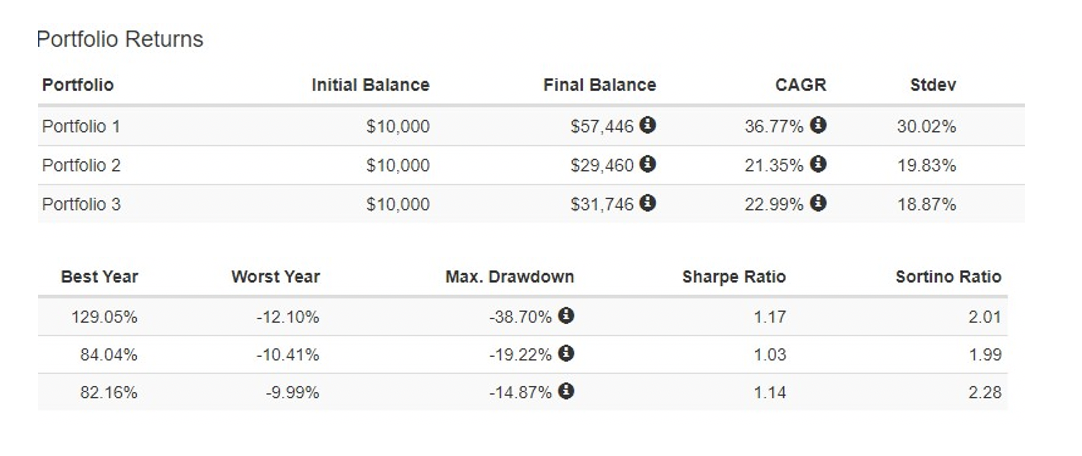

Chart 4 – Comparison of efficiency in hedging a securities portfolio with sector-based ETFs (Portfolio 3) versus an unhedged portfolio (Portfolio 1), and a portfolio hedged with SPY (Portfolio 2).

Based on the chart above, we can conclude that hedging our portfolio with sector-based ETFs in Portfolio 3 is more practical then hedging against S&P-500 ETFs. As can be seen, risk-adjusted evaluations such as Sortino ratio and Sharpe ratio both show the highest values in case of ETF-based hedging. To be precise, Sortino ratio that indicates risk-adjusted return inclusive of downside volatility is the highest in Portfolio 3. As for Sharpe ratio that designates risk-adjusted return inclusive of total volatility, it is also higher in Portfolio 3 than in Portfolio 2, although a little lower than in Portfolio 1. However, Portfolio 3 also has the lowest standard deviation, and maximum drawdown ratios.

Therefore, such risk ratio, as the beta ratio, and investment portfolio exposure to market risks not by the global S&P-500 index but use specific sector-based ETFs included in the portfolio.

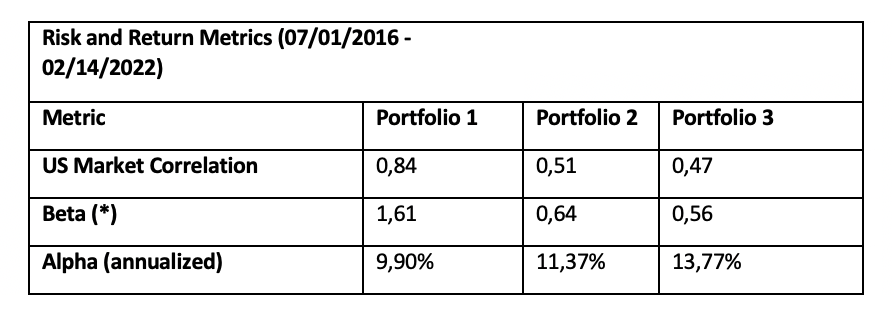

Also, based on the portfolio visualizer data and by comparing these three portfolios, we can see from the Chart 5 below that Portfolio 3 beta against the market equals 0,57 versus 0,65 for Portfolio 2, and 1,62 for the unhedged Portfolio 1. Portfolio 3 correlation with the US market is 0,47 versus 0,51 for Portfolio 2, and 0.84 for the unhedged Portfolio 1.

This indicates that not only is the portfolio hedged with replication of sector-based ETF structure (Portfolio 3) more correct and precisely follows the benchmark portfolio allocation but also generates a greater alpha on the managed accounts than the unhedged portfolio. Thus, alpha for the portfolio hedged with sector-based ETF (Portfolio3) equals 13,29%; hedged with SPY Portfolio 2 - 10,79%, and only 9,75% for the unhedged Portfolio 1.

Chart 5 – Comparing of beta, US market correlation, and alpha across three portfolios (based on visualizer data)

By using not only specific industry ETFs but also ETFs of companies with different business cycles, capitalization level and other parameters, we can arrive at a portfolio allocation close to the original one with just with 4-6 ETFs, as it has been exemplified above. This is the portfolio allocation that we are going to hedge instead of hedging every one out of the 100 securities included in it.

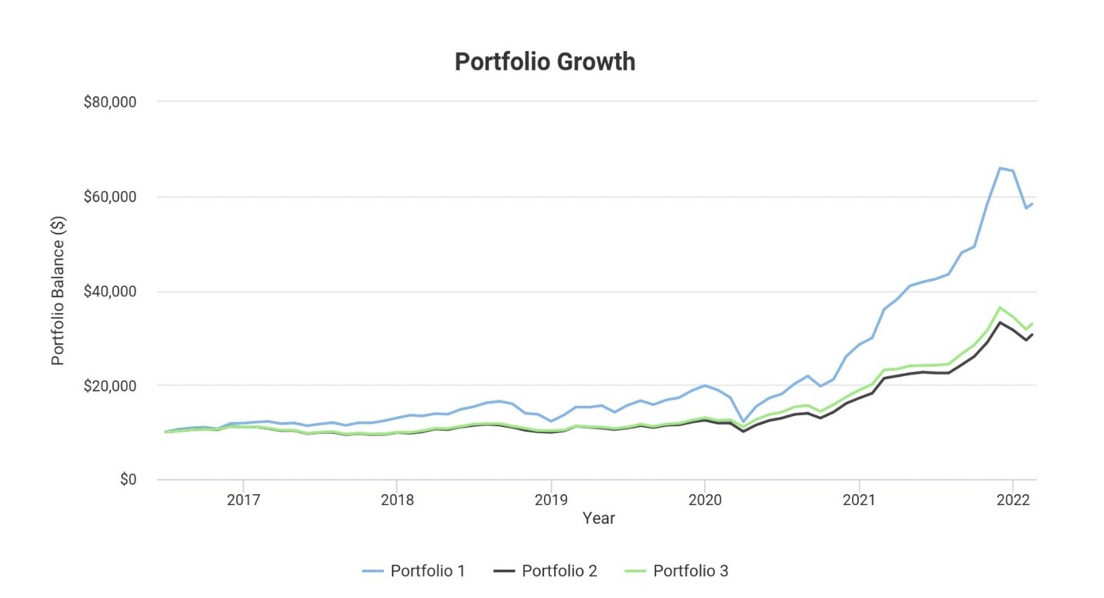

Chart 6 – Portfolio Growth

Thus, hedging individual securities’ positions in the portfolio is quite expensive, and applying specific seсtor-based ETF replication, would save investor’s costs.

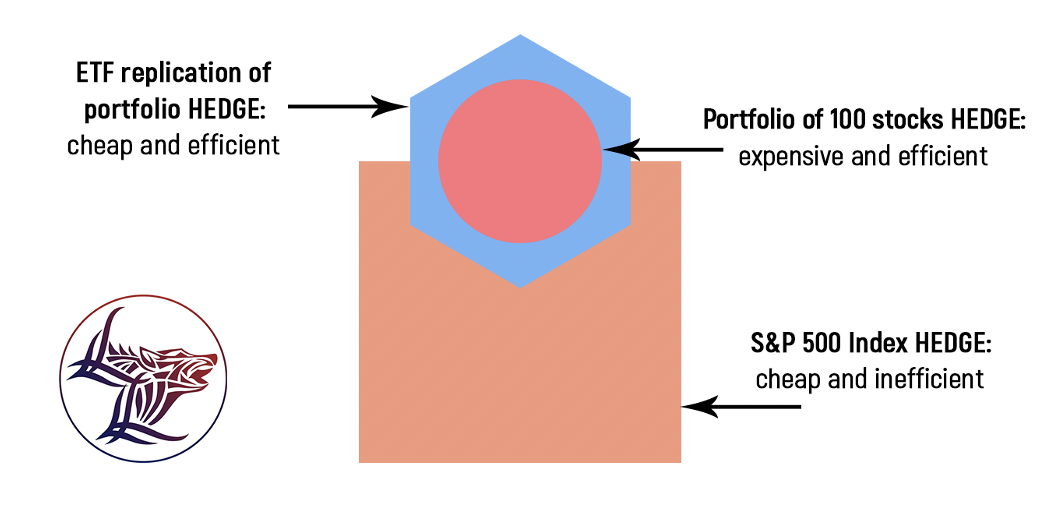

Chart 7 – Efficiency of hedging a portfolio through sector-based ETFs versus hedging with SPY Index or with an individual hedge against each stock in a portfolio of 100.

Choosing an optimal hedging strategy will help investors avoid paying high hedging costs and add a substantial degree of accuracy to hedging their portfolio risks. You can also gather this idea from the drawing depicted above.

Using ETFs to calculate market exposure risks is vital for the proper configuration of the investment portfolio and its hedging.

© Sigma Global Management

Read more commentaries by Sigma Global Management