"We abuse land because we regard it as a commodity belonging to us. When we see land as a community to which we belong, we may begin to use it with love and respect." -Aldo Leopold

Introduction

Welcome to the new, slimmer format of the Absolute Return Letter. As I mentioned last month, going forward, the monthly letter will be noticeably shorter. In the past, my self-imposed guideline has been 2,500-3,500 words per letter, which typically adds up to 8-10 pages including 5-10 charts. From this month, I will limit myself to about 1,000 words per letter. I will instead spend most of my time on the forthcoming launch of our first climate change fund and the research associated with that. As you may already be aware, all our research, whether linked to one of 'our' six megatrends or not, is made available to subscribers of ARP+ which you can find on our website here.

Why a quandary?

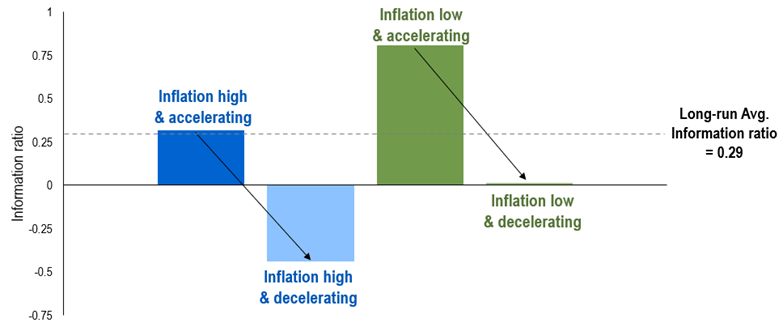

Long-only investors use the information ratio as a proxy for the risk-adjusted return and, as you can see in Exhibit 1 below, commodities often deliver negative information ratios (i.e. poor risk-adjusted returns) when inflation is high and decelerating. In other words, although commodities do well when inflation is accelerating, once central banks decide to go to war against it, you do not want to hold too many commodities in your portfolio. That has at least been the case historically.

The predicament investors are up against at present is that the current commodities cycle is unlike anything we have ever seen before because of the ongoing transition to green energy forms. It is therefore not unreasonable to expect certain commodities to behave rather differently this time around.

Exhibit 1: Commodity information ratios in different inflation regimes

Source: PGIM Wadhwani

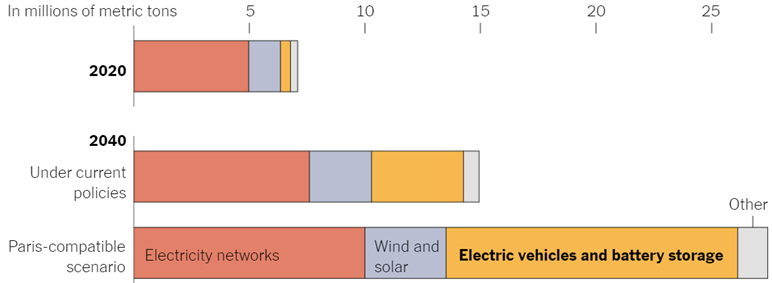

Demand for those commodities used when producing EVs and battery storage solutions will be particularly strong, but there are other investment opportunities too. For example, the electricity grid will have to expand to provide the energy required, and wind and solar’s share of total energy supplies will continue to increase (Exhibit 2).

Exhibit 2: Demand for green metals and minerals

Sources: New York Times, International Energy Agency

And the winners are…

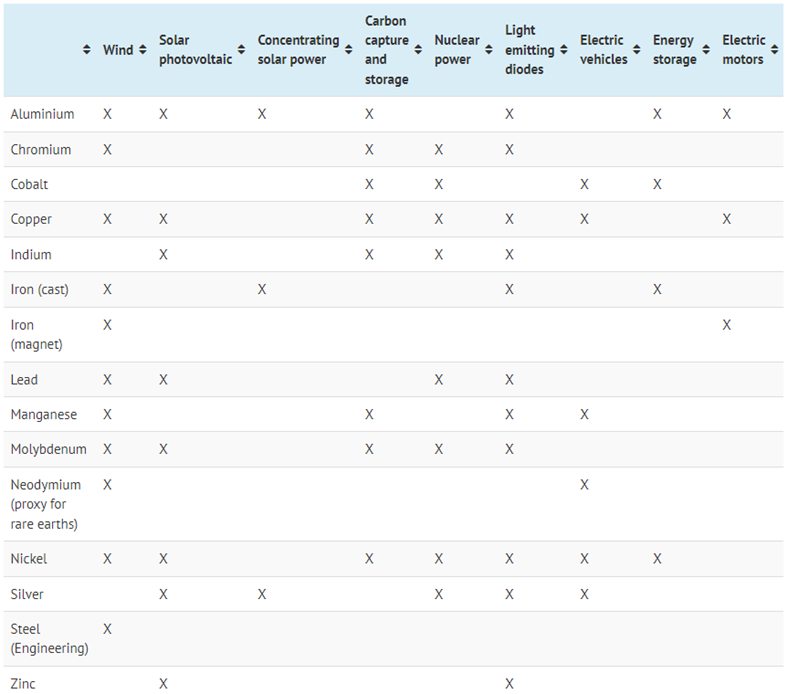

Next, the obvious question: which commodities will be most in demand in the years to come, given the ongoing energy transition? Many metals stand to benefit but, as you can see in Exhibit 3 below, some metals are ‘greener’ than others. According to carbonbrief.org, six metals stand out, assuming the main objective is to reduce CO2 emissions.

Copper is a big beneficiary. It is used in wiring everywhere and is a sublime conductor. With the introduction of wind, solar and EVs, demand for copper has risen dramatically as copper is used extensively in all three, and this is still early days. Copper mining takes place all over the world, but most of it is mined in South America with Chile being the top producer.

Lithium is a critical ingredient in lithium-ion batteries which are used to power smartphones, laptop computers and EVs. It is also worth noting that, when fusion energy is eventually commercialised, demand for lithium will be even stronger. Australia is the biggest producer, but Chile is by far the biggest exporter of lithium.

Cobalt, mostly a by-product when mining copper and nickel, is an essential component of the cathode in lithium-ion batteries. It is also used in various industrial and military applications. Globally, the Democratic Republic of Congo dominates cobalt mining with a 70% market share.

Exhibit 3: Source of need for green metals and minerals Sources: carbonbrief.org

Nickel is another key ingredient in batteries and is expected to form an ever-larger proportion of future batteries. It is widely used in other applications too, notably in stainless steel production. Mining is spread all over the world with South-East Asia accounting for about half of global nickel mining.

Manganese is another metal used in batteries and in steel. It is also widely used elsewhere, for example in animal feed. One-third of global manganese mining takes place in South Africa with China being a distant second.

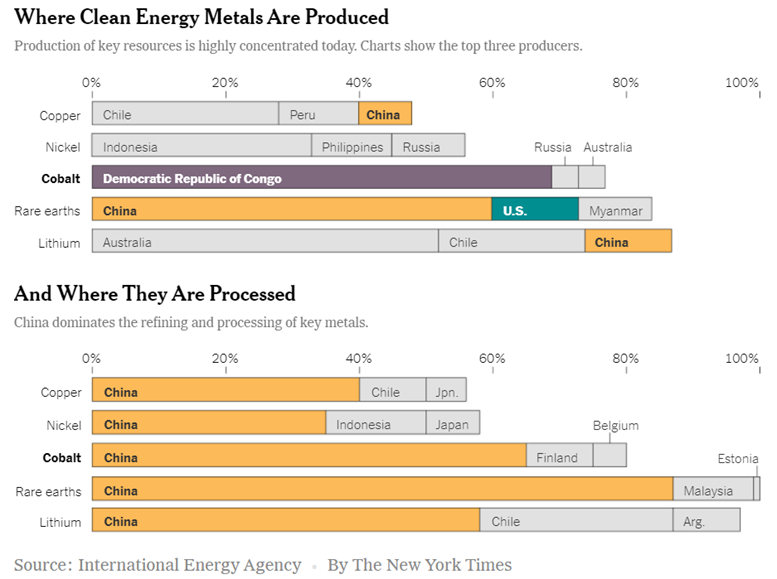

Rare-earth metals are a group of 17 chemically similar elements. Each has unique properties, making them important components in a wide range of technologies from low-energy lighting and catalytic converters to the magnets used in wind turbines, EVs and computer hard drives. Most rare earth comes from China (Exhibit 4).

I am somewhat concerned about being dependent on an unstable regime like the Democratic Republic of Congo for our cobalt supplies. As it happens, researchers at University of Texas have found that they can achieve the same results with a mix of nickel, manganese and aluminium as they can with cobalt. Furthermore, a mix of those three minerals will meaningfully reduce battery costs, so a switch away from cobalt may not be far away. For that reason, aluminium deserves to be added to the list of green metals.

Graphite should also be added, as it is the raw material behind a new, ground-breaking material called graphene. Graphene is capable of transferring electricity 140 times faster than lithium, while being 100 times lighter than aluminium. Just one gram of a single layer of graphene covers the equivalent of two football pitches. This translates into an improvement in the power density of a smartphone battery of 45%, which is why Samsung has begun to produce smartphones based on this technology.

Samsung has stated that, when the technology is fully developed, the charging time of smartphones from 0% to 100% should be reduced to 12 minutes. Turkey, China and Brazil (in that order) are in possession of the largest graphite reserves worldwide. ARP+ subscribers can read more about this in a research paper from August 2020 which can be found here.

Exhibit 4: Demand for green metals and minerals Sources: New York Times

All these metals will be in strong demand for many years to come. Therefore, one cannot assume that more hostile central banks in large parts of the world will necessarily result in falling prices on green metals. Consequently, if you invest in commodities (and you should), green metals should dominate your portfolio.

Concluding remarks

Through a long life in finance, I have learnt that, the more concentrated production (in this case mining) is, the more likely it is that, sooner or later, a problem will occur which will lead to supply shortfalls in large parts of the world. In that context, cobalt and the Democratic Republic of Congo stand out. I have no idea what could cause it, but it is never a good sign when about 70% of global supplies come from a country that is not known for being politically stable. That is why aluminium should be added to the list of green metals.

The biggest winner of all the green metals longer term, though, is probably going to be graphene. It is a material with a huge number of unique properties. It is extraordinarily strong, very flexible, lightweight, and its conductivity is exceptional. In fact, it stands out as the most disruptive of all the green metals. I would go even further and call it a disruptive technology. Other materials and technologies will be blown out of the water by graphene over the next ten years, and ARP+ subscribers will benefit from the work we do on this material in the months and years to come.