Credit Suisse Says It May Be Time to Go Long Shipping Freight Rates

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA provocative report by Credit Suisse’s Zoltan Pozsar that was making the rounds in certain corners of Twitter this week suggests that the Russia-Ukraine conflict could be a strong tailwind for shipping freight rates.

The report features a lot of big thoughts, shipping rates being just one of them, so I’ll try to keep things as simple as possible.

According to Pozsar, Credit Suisse’s head of short-term rate strategy, the global commodities market is facing a crisis due to the conflict in Eastern Europe and the international sanctions that have been piled onto Russia, one of the world’s biggest suppliers of everything from natural gas to nickel to wheat. The price of commodities traded outside of Russia are now surging on a sanctions-triggered supply shock; meanwhile, those traded inside Russia have stalled in many cases, and crashed in others, since many of these materials have effectively been unplugged from the rest of the world economy.

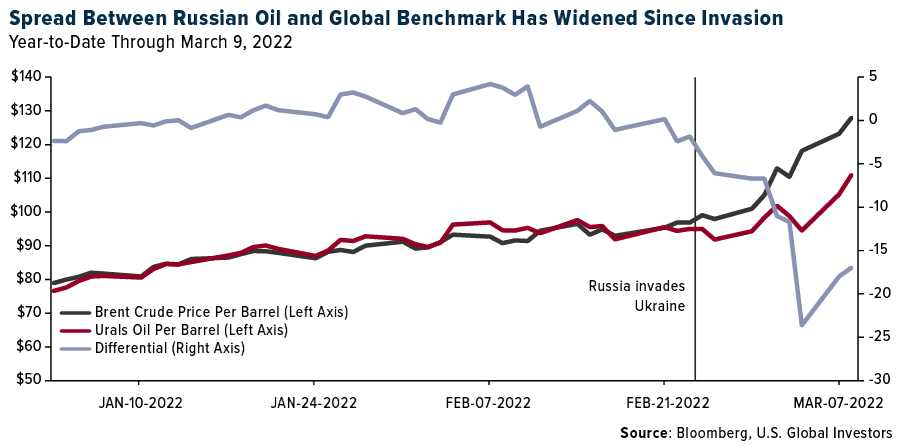

Here’s one such example. Historically, the spread between a barrel of Brent crude oil (the global benchmark) and Russian Urals crude has been very tight, often differing no more than a couple of dollars per day. Ever since Russia invaded Ukraine, however, the spread has widened as Brent has skyrocketed much more dramatically than the price of Urals.

As Pozsar points out, a buyer must come in to support cratering prices and close the spread between Russian and non-Russian commodities. The problem, though, is that Western nations are unable to do so since it’s their very own sanctions that have created this crisis. Despite attractive prices, as much as 70% of Russian oil lacks buyers at the moment, according to Lloyd’s List.

So then who’s the buyer? Pozsar believes the most likely answer is the People’s Bank of China (PBoC), which has vowed to continue normal trade relations with Russia and may be interested in gobbling up cheap Russian commodities to support its currency, the yuan. (Remember, China, like Russia, has gradually been shifting away from the U.S. dollar as a reserve currency.)

What does this have to do with shipping rates? China may not have enough storage capacity on land for all the Russian commodities bought at a deep discount, and this could force the country to store them on floating vessels. As Pozsar writes, “the price the PBoC will be paying to lease ships to fill them up with Russian commodities can in theory rise as much as the collapse in the price of Russia commodities: a lot.”

Spot Earnings Are Already Spiking

Now you may think there are too many “ifs” and “maybes” in Pozsar’s thesis, but actual events appear to be playing out as described.

For one, Bloomberg reports that China is already considering buying big stakes in distressed Russian energy and commodity companies, including oil producer Gazprom and aluminum producer United Company RUSAL. The two countries have been strengthening ties, “with President Xi Jinping and Vladmir Putin last month signing a series of deals to boost Russian supply of gas and oil, as well as wheat,” the article reads.

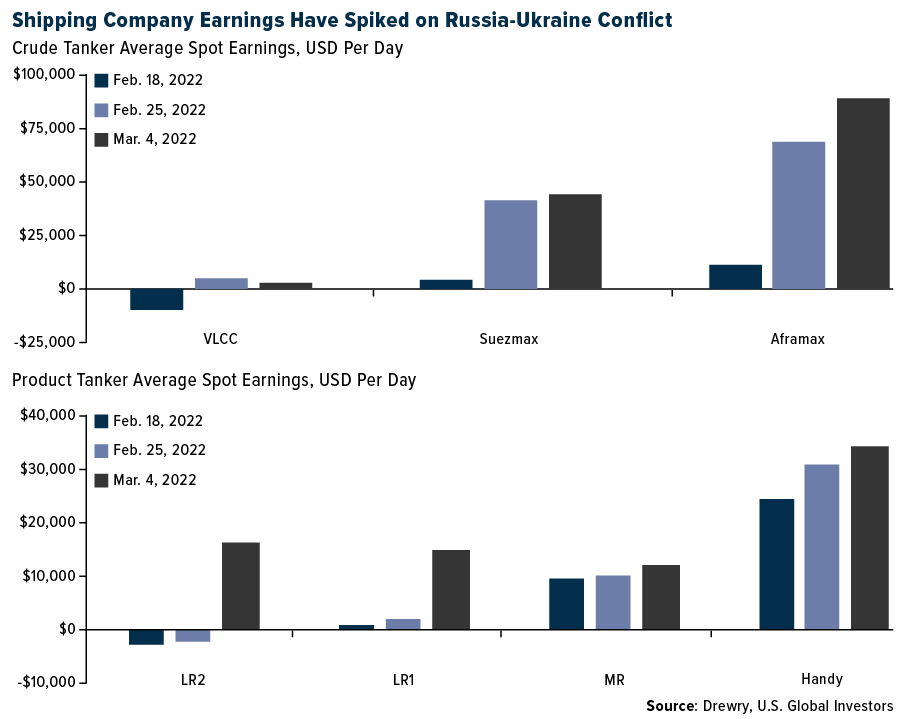

In addition, daily average earnings for crude tankers and “product” tankers, which carry gasoline and other refined petroleum products, have surged since Russia’s invasion. In a report dated March 9, Drewry analysts Nikesh Shukla and Santosh Gupta write that spot earnings have increased due to a vessel shortage as traders rushed to lock in carriers and some operators were unwilling to sail into the Black Sea region. Earnings for smaller-class vessels—which, unlike very large crude carriers (VLCCs), can access canals and ports of all sizes—have seen among the biggest jumps from February 18, before the invasion, to March 4.

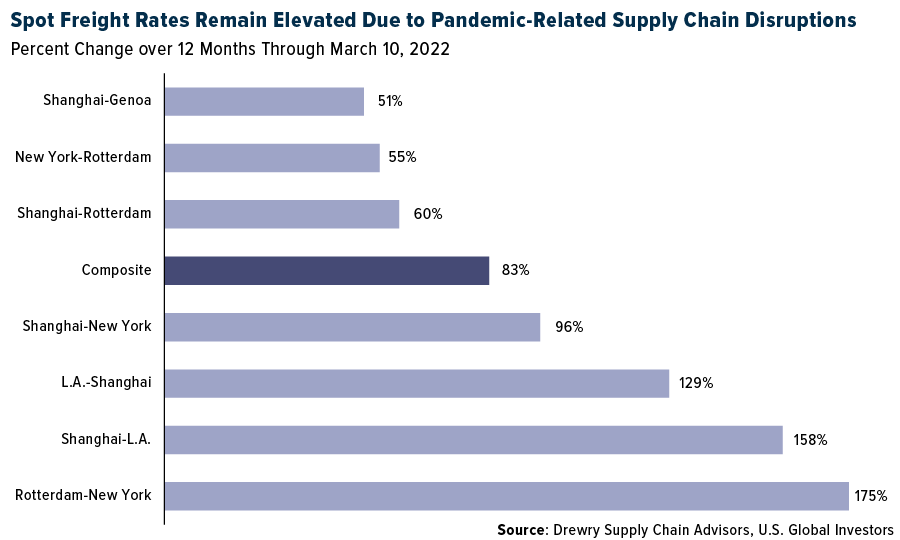

Remember, shipping freight rates are already highly elevated due to the pandemic-related supply chain imbalances. Spot prices are up 83% on average from the same week last year, according to Drewry. To ship a container from Shanghai to Los Angeles costs exporters 158% more than it did a year ago; the Rotterdam-New York route is as much as 175% more expensive.

Investors have taken notice. Compared to the broader market, which has fallen into correction or even bear territory since the start of the conflict, shares of many shipping and logistics companies have popped. Among the biggest movers between February 24 and March 10 are Japanese carriers including Mitsui O.S.K. Lines (up 26.7%), Kawasaki Kisen Kaisha (up 20.9%) and Nippon Yusen Kabushiki Kaisha (up 20.0%). Taiwan’s Evergreen Marine (up 10.3%) and Yang Ming Marine Transport (up 10.2%) have also jumped.

Bitcoin Could Also Benefit

The other point I’d like to highlight from Pozsar’s report is that the conflict could bring about the end of the global monetary system that’s been in place since 1971, when President Nixon ended commodity-based money. This system “crumbled,” Pozsar asserts, “when the G7 seized Russia’s FX reserves.”

He’s referring, of course, to wealthy countries’ decision to freeze all assets belonging to the Central Bank of the Russian Federation, a move historically reserved for true pariah states such as North Korea, Iran and Venezuela.

At the other end of this crisis, the Chinese yuan’s value could be a lot higher (thanks to the discounted Russian commodities) and the dollar’s value a lot lower.

As a result, “Bitcoin… will probably benefit from all this,” Pozsar writes.

I agree. Unlike fiat currency, Bitcoin is private property. No person or government entity can “freeze” it.

Many investors, regardless of how they feel about this geopolitical conflict, see the severity of the economic sanctions against Russia and conclude that Bitcoin is an escape hatch from the monetary system that makes such seizures possible.

Index Summary

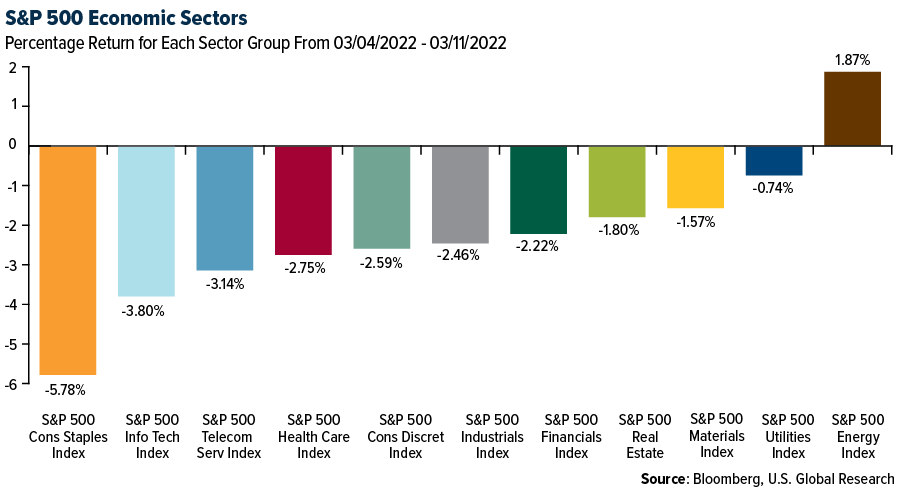

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.00%. The S&P 500 Stock Index fell 2.65%, while the Nasdaq Composite fell 3.53%. The Russell 2000 small capitalization index lost 0.82% this week.

- The Hang Seng Composite lost 6.65% this week; while Taiwan was down 5.24% and the KOSPI fell 10.62%.

- The 10-year Treasury bond yield rose 26 basis points to 1.993%.

Airline Sector

Strengths

- The best performing airline stock for the week was Lufthansa, up 14.6%. Intra-Europe net sales were up by eight points to -24% versus 2019 (and versus -32% in the prior week) and increased by 1% this week. International net sales increased by 11 points to -34% versus 2019 but grew by 3% this week. This led to a 10-point increase in system-wide net sales for flights booked in Europe. Bookings have now reached their highest level since the beginning of the pandemic, surpassing a previous peak in November.

- Azul Airlines is seeing the strongest booking trends since the pandemic began. Fuel surcharges and greater price inelasticity allow the company’s cargo segment (10% of revenues) to respond more quickly to the sharp rise in fuel prices.

- LATAM Airlines reported better-than-expected results for the quarter, delivering positive operating profit for the first time since the start of the pandemic. In summary, yields performed better than expectations, while demand was also stronger, leading top line, and consequently EBIT, to consensus.

Weaknesses

- The worst performing airline stock for the week was Aeromexico, down 23.9%. Global capacity was pulled by 1% for April and May this week to 80% and 85% versus 2019 respectively, while June remained at 87%. For April and May, there were 1% reductions from APAC and Europe while Latin America reduced April by 2% and May by 1%.

- Regarding geopolitical events in Eastern Europe, lessors will be negatively impacted most directly. Many believe that lessors will not be able to repossess aircraft from Russian airlines and that insurance claims under war policies held by lessors will need to be litigated over several years given sanctions on insurance by the EU, the U.K., and U.S.

- Domestic and international volumes decelerated to -16.7% versus 2019 (versus -14.6% last week) and -28.4% versus 2019 (versus -26.4% last week), respectively. However, both channels saw 2-3 points of improvement on pricing. As demand has rebounded, the strong pricing is nice to see given the recent spike in fuel prices.

Opportunities

- JPMorgan updated its estimates for Azul and Copa after the fourth quarter of 2021 and remain neutral on both stocks. Both carriers suffered in early January with the Omicron variant while oil prices spiked. Meanwhile, yields are at high levels, helping to mitigate the cost pressure. Azul continues to benefit from faster ASK recovery and fleet upgrading, while Copa maintains the soundest balance sheet in the region combined with competitive unit cost and privileged geographical position.

- WestJet Airlines is acquiring Sunwing Airlines, reports the Canadian Press, as competition in the Canadian travel market heats up. On Wednesday, WestJet confirmed the news in a statement, adding that “the transaction will bring together two distinctly Canadian travel and tourism success stories.”

- Given the minimal near-term capacity changes this month, competitive capacity across the board for March is the same. For second quarter 2022, Delta Air Lines remains the best positioned out of the network carriers as it faces only mid-single digit competitive capacity relative to 2019 versus American Airlines and United Airlines face low-to-mid-double digit competitive capacity. Alaska Air still has the least amount of increased competitive capacity and is not expected to face 2019 levels of competition until third quarter 2022.

Threats

- According to Seaport Global, energy market chaos tied to the Russian/Ukraine war and a supply/demand dynamic poorly calibrated for the industry’s new cost structure prompted capitulation on weaker balance sheet stories. The group downgraded American Airlines, GOL, and Azul Airlines to “neutral” due to a reduced earnings outlook. It is unclear where oil prices go from here, but airlines need to begin planning for a worse oil shock, implying more capital raises to shore up weaker balance sheets. Pent-up demand remains great, the capital markets are open, and airlines simply need to cut 10%-15% points of capacity from 2022 capacity plans to gain the kind of pricing power needed to offset the worse oil shock.

- United Airlines cited that the industry has historically captured 60% of fuel increases via higher ticket prices and that in 2019 the company passed through 100% of higher jet fuel. The typical lag has been about one quarter until higher fuel is passed through. However, the current environment is unusual, and management was unsure how much they would be able to pass through. Importantly, United does not plan to change its no hedging policy. In terms of liquidity, United has about $19 billion of liquidity today and had hoped to bring this down over time, but now this liquidity provides a cushion as oil rises.

- Jet fuel is up over 90% year to date, impacted by the Russia/Ukraine war. Airlines have been implementing higher fares. Nonetheless, the net/net this is still negative, which might lead to lower earnings.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 6.4%. The best performing country in Asia this week was India, gaining 1.5%.

- The Polish zloty was the best performing currency in emerging Europe this week, gaining 2.5%. The Indonesia rupiah was the best performing currency in Asia this week, gaining 0.64%.

- China set up an ambitious gross domestic product (GDP) target of 5.5% that will require monetary support and sustainable macro polices. Last year, China’s GDP grew 8.1%, beating the government’s target of over 6%.

Weaknesses

- The worst performing country in emerging Europe for the week was the Czech Republic, losing 0.27%. The worst performing country in Asia this week was Hong Kong, losing 6.4%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 7.8%. The Thailand baht was the worst performing currency in Asia this week, losing 2.1%.

- This week Greece reported higher inflation. Inflation spiked to 7.2% in February, up from 6.2% in January. It may accelerate even faster due to the ongoing war in Europe, food supply concerns, and spiking commodity prices.

Opportunities

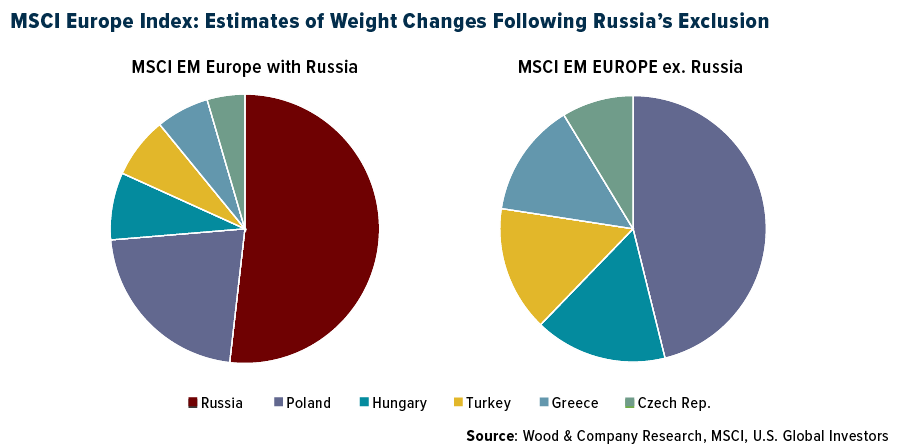

- Last week the FTSE removed Russian holdings from its indices and this week the MSCI followed FTSE’s move. As expected, Russian assets were in large scale replaced by Poland, Turkey, Hungary, the Czech Republic, and Greece. Inflows may not follow in the short-term, but investors may be reluctant to buy Russian assets for a while and will be looking for new markets.

- FactSet reported that the European Union (EU) currently gets 40% of its gas supply from Russia, and in light of current geopolitical tensions, has recently pledged to cut Russian gas imports by two-thirds before the end of the year and cease Russian fossil fuel imports by 2030 (five years earlier than previously planned). This will present opportunities for the EU to push for expansion in renewable energy projects.

- South Korea has a new president, returning conservatives to power. CLSA, an Asian broker, says this should be a positive event for equites. South Korea’s new president, Yoon Suk-yeol, pledged to support the private sector. It’s worth noting, however, that he won by a narrow margin, (45.56% versus 47.82%), showing the country’s deep division.

Threats

- The European Central Bank (ECB) surprised markets by accelerating plans to wind down stimulus, signaling that it is more concerned about price increases than the war hitting growth. Officials ramped up their 2022 inflation forecast to 5.1% from 3.2% previously. The central bank will slow bond buying to 30 billion euros in May and 20 billion in June and may halt the program in the third quarter. It tempered that by making a subsequent rate hike less automatic, (though money markets are now betting on a quarter-point increase in October, instead of December).

- This week’s Ukraine-Russia talks went nowhere. Sergei Lavrov told Ukrainian counterpart Dmytro Kuleba that a cease-fire isn’t on the table, gave no commitments on humanitarian corridors and denied that Moscow had invaded its neighbor. Russia has destroyed about $100 billion of Ukrainian assets and infrastructure, Volodymyr Zelenskiy’s chief economic adviser said.

- The Moscow Stock Exchange was closed this week, but the central bank of Russia is not opposed to reopening the exchange on Monday or Tuesday. When it opens, investors who did not exit Russia could see huge losses. BlackRock suspended all purchases of Russian securities on February 28, four days after Russia attacked Ukraine, and when Russian assets were valued around only $1 billion. As of the end of January, BlackRock had $18.2 billion in client held Russian assets, losing $17 billion in just a few weeks.

Energy & Natural Resources

Strengths

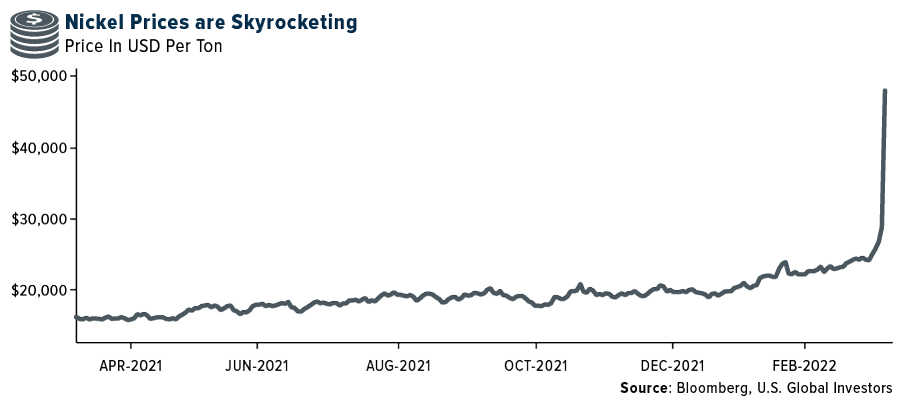

- The best performing commodity for the week was nickel, up 62.93%. Trading was suspended on Monday as prices doubled within hours as fears over Russian supplies left buyers exposed to a historic short squeeze. Nickel, used in stainless steel and lithium-ion batteries, added more than $17,000 to trade at an almost 15-year high above $40,000 a ton, in the biggest-ever daily dollar gain in the 35-year history of the contract.

- Urea prices continued to move higher across global benchmarks as the market deals with the ongoing impacts from the Russia/Ukraine conflict. On Friday, global values pushed above $800 per ton following news that the Russian Ministry of Industry and Trade recommended suspending exports of fertilizers from Russia. Brent crude fluctuated at the end of a volatile week, reports Bloomberg. Prices had earlier dipped as Putin noted “positive movement” in talks with Ukraine, but then headed higher after Iranian nuclear negotiations were halted in Vienna.

- Peruvian copper and tin production improved year-on-year in January, while zinc and lead output were both down on an annual basis, the country’s Minister of Energy and Mines Minem said. Peru produced 199,255 tons of copper in January, a 12.7% year-on-year increase from 176,737 tons.

Weaknesses

- The worst performing commodity for the week was the Bloomberg Powder River Basin 8800 Btu Coal Spot Fob/Gillette Wyoming, down 22.63%. Demand for thermal coal in the U.S. appears satiated but the rest of the world’s energy demand is gyrating as they try to unplug from Russia. European utilities are increasingly turning to coal as they may be forced to in the future.

- According to data from China Customs, in the first two months of 2022, China imported 27bcm of natural gas (piped and LNG), -4.5% versus last year. The average gas import price was $13.65/MMBtu, up 85% year-over-year. In the first two months of 2022, China imported 10.5mbday of crude oil, -4.9% year -over-year, as teapot refiners cut run rates in February during Chinese New Year and Winter Olympics.

- Fastmarkets recently reported that some U.S. steel mills are running extremely low on raw materials, and some have cancelled HRC order flow owing to lack of scrap availability. Given the moves in U.S. imported pig iron (65% sourced from Russia / Ukraine) and seaborne billet / coking coal, they may be continued upward pressure on U.S. scrap prices into April, when steel demand seasonally accelerates.

Opportunities

- According to Morgan Stanley, despite the year-to-date strength, valuations across its energy-specific coverage remain compelling. On consensus estimates, U.S. earnings and profits still trade at a 60% enterprise value/EBITDA discount to the S&P 1500, wider than the five- and 10-year average discount of 50% and 40%, respectively. Intrinsically, the group estimates that the sector is only pricing $64 per barrel WTI, creating room for a further catch-up trade versus the commodity.

- LME inventories for copper remain at multi-year lows, and there have not been dramatic drawdowns over the last 10 days. China inventories are lifting broadly in-line with seasonal patterns and are at normal levels for aluminum, but copper inventories remain at multi-year lows. Whilst significant anxiety and tightness exists in the world ex-China, indicators in China do not point to material physical tightness.

- This is by far the most dynamic situation that exists since Fukushima in the uranium space, with big spot moves by uranium physical trust buying, catalyzed by speculative money bidding up the Trust to a NAV premium. This follows talk of a Russian export ban potentially including nuclear fuel and potentially U.S. sanctions against Rosatom. Rosatom supplies nuclear fuel to many global buyers. Russia has minor uranium mine production equal to around 5-6% of global uranium supply but controls more 40% of global enrichment capacity.

Threats

- As reported by Bloomberg, JPMorgan Chase & Co. is the largest counterparty to the Chinese tycoon who holds an unprecedented short position in the nickel market that has been the subject to a squeeze. With JPMorgan holding 50,000 tons of the 150,000-ton short position of Xiang Guangda, the group is expecting a margin payment of about $1 billion next Monday. JPMorgan is leading discussions with Xiang and around 10 other banks to resolve the multi-billion-dollar liquidity issue.

- S. President Joe Biden announced this week that the U.S. would impose an immediate ban on the import of crude oil, oil products, LNG, and coal from Russia. U.S. Secretary of State Antony Blinken had said over the weekend that the U.S. was now actively discussing such a ban with European partners, contributing to the sharp move up in crude prices. The executive order also bans new U.S. investment in Russia’s energy sector and prohibits Americans from financing companies or enabling foreign companies that are making investment in Russian energy.

- Russia threatened to cut natural gas supplies to Europe via the Nord Stream 1 pipeline as part of its response to sanctions imposed over the invasion of Ukraine, a move that could heighten the turmoil in energy markets and drive consumer prices even higher. European energy prices roared to records after the U.S. said it was considering curbs on all imports of Russian oil, a move that would add to supply fears across commodity markets. In some of the most chaotic trading the market has ever seen, benchmark gas futures leaped 79% to the equivalent of more than $600 a barrel of oil. The surge is likely to lead to large margins calls, which in turn could end up driving futures even higher as companies buy exchange contracts to avoid paying up cash to cover their trades.

Domestic Economy & Equities

Strengths

- S. consumer net worth is strong. Increasing home prices and strong homebuilding activities are offsetting a good part of the recent decline in stock prices. Household net worth jumped to a fresh record, increasing by $5.3 trillion in the fourth quarter, or 3.7%, according to a Federal Reserve report from Thursday. The fourth-quarter advance pushed net worth to more than $150 trillion.

- Mortgage applications jumped 8.5% for the week ending March 4, as mortgage rates dropped for the first time in three months as a result of Russia’s war in Ukraine, the Mortgage Bankers Association (MBA) reported on Wednesday.

- Baker Hughes, provider of oilfield services & equipment, was the best performing S&P 500 stock for the week, gaining 14.30%. U.S. energy firms this week added oil and natural gas rigs for the ninth time in 10 weeks after Russia’s invasion of Ukraine drove crude prices to their highest since 2008.

Weaknesses

- February’s consumer price index (CPI) inflation rose 0.8% month-over-month, ahead of estimates and January’s 0.6% monthly pace. Year-over-year inflation increased to 7.9%, recording the fastest annual pace since 1982.

- Weekly initial jobless claims rose 227,000, above consensus for 214,000 and the prior week’s upwardly revised 216,000. Continuing claims were reported at 1,494,000, ahead of forecasts for 1,470,000 and the prior week’s downwardly revised 1,469,000.

- Etsy Inc. was the worst performing S&P 500 stock for the week, losing 18.55%. Deutsche Bank reinstated coverage of Etsy, with a recommendation of hold and a price target at $145, implying a 5.9% increase.

Opportunities

- Global markets remain very sensitive to Ukraine-related headlines. On Friday, Vladimir Putin said that he sees “certain positive shifts” in talks with Ukraine; however, it was not confirmed by Ukraine. In case of a rapid de-escalation in tensions, equites are expected to bounce sharply.

- Republicans and Democrats agreed on a spending package, made up of 12 separate bills. The legislation contained $730 billion in non-defense funding to boost health, education and science programs and $782 billion in defense spending. Both represented modest increases from the past fiscal year and the measure would keep the government’s doors open through September 30, the end of the current fiscal year.

- Bloomberg economists predict the Empire State Manufacturing Index to rise to 7.8 in March from 3.1 in February. The data is based on a monthly survey of manufacturers in New York State conducted by the Federal Reserve Bank of New York, and it will be released next week, March 15.

Threats

- S. inflation hit a new 40-year high in February and it’s going to rise even more. The CPI climbed to an annualized 7.9% from 7.5% in January, with the core inflation spiking to 6.4%. Most of the impact from the surge in oil hasn’t been felt yet. Economists are predicting a peak in the rage of 8%-9% next month or so. On Thursday, stocks and bonds fell on inflation concerns. Ten-year Treasury yields spiked above 2%, and the 30-year rate rose to the highest since May 2021.

- According to BBH Global’s currency strategy team, the Fed is on track to start the tightening cycle with a 25 basis points hike next week. This small increase in a repo rate is fully priced in. Looking ahead, 175 basis points of tightening is priced in over the next 12 months. However, they continue to believe that the terminal Fed Funds rate will have to be much higher.

- The sanctions-related surge in commodity prices will translate into higher costs and lower profits for many domestic and international companies. Oil reached almost $140 per barrel but retreated later in a week, ending the week at $109 per barrel.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Vangold, up 3,429%.

- Ukraine has already spent $15 million of the donations it received in cryptocurrencies on military supplies, including bulletproof vests that were delivered Friday, Alex Bornyakov, deputy minister of Digital Transformation of Ukraine, told Bloomberg news. The Ukrainian government anticipates doubling the $50 million of crypto donated so far in the next two or three days, the article continues.

- Bain Capital, one of the world’s biggest startup-investment firms, is launching a $560 million fund focused exclusively on crypto-related efforts, reports Bloomberg. The fund is expected to invest in 30 companies ranging from crypto start-ups to decentralized autonomous organizations (DAO) in layer 1 blockchains and storage.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Purfect Network, 99.92%.

- Ukraine’s vice prime minister publicly asked all major cryptocurrency exchanges to freeze accounts in a bid to further challenge Russians’ resources and stop the war. Kraken CEO fired back, however, saying he believes crypto should enforce individualism, rather than nationalistic alliance to a country. He added that if they were going to voluntarily freeze financial accounts of residents unjustly attacking and provoking violence, step one would be to freeze all U.S. accounts, writes Fortune.

- Coinbase CEO Brian Armstrong said that the cryptocurrency exchange will block transactions from IP addresses that might belong to sanctioned individuals or entities. However, it will not pre-emptively ban all Russians from using Coinbase, he said on Twitter.

Opportunities

- A decentralized autonomous organization (DAO) has been established with the aim to pool $4 billion and buy the NFL team the Denver Broncos, writes Crypto News. The crypto enthusiasts, dubbed “BuyTheBroncosDao,” aims to collect the necessary funds to submit a bid for the franchise with Sean O’Brien, a former lawyer for Cisco leading the bid.

- South Korea’s cryptocurrency market grew to $45.9 billion in 2021 despite stringent regulations in the region, writes CoinTelegraph. South Korea is considered among the strictest crypto markets in terms of regulatory policy implementations and made regular headlines throughout 2021 for its new Travel Rule and KYC requirements.

- Bitcoin has been trading below its 200-day moving average for 70 consecutive days, one of the longest such streaks on record. And though the popular coin is still well below the long-term threshold, once it breaks above it, the performance one week to three months out is stronger than average.

Threats

- As reported by Crypto News, the crypto community has once again been thrown into a debate about the need for more decentralization. This comes after both the NFT marketplace OpenSea and Ethereum wallet MetaMask recently blocked users based on their geographic location.

- The People’s Bank of China (PBOC) disclosed a continued crackdown on virtual currency transactions in a video conference late last week. Beijing carried out one of the most comprehensive crackdowns on crypto trading and mining last May, Bloomberg reports, forcing major crypto exchanges and mining companies out of the country.

- A finance professor at the Wharton School of the University of Pennsylvania is urging the U.S. Federal Reserve to raise the interest rates and shield the dollar from Bitcoin, writes InsideBitcoins.com. Professor Jeremy Siegal says that Bitcoin could “take over” the U.S. dollar; hence the Fed needing to step in and protect the fiat currency from devaluation.

Gold Market

This week going into the close, gold futures were at $1,988.10, up $21.50 per ounce, or 1.09%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.31%. The S&P/TSX Venture Index came in off 0.11%. The U.S. Trade-Weighted Dollar rose 0.48%.

| Mar-10 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Mar-10 | CPI YoY | 7.9% | 7.9% | 7.5% |

| Mar-10 | Initial Jobless Claims | 217k | w227k | 216k |

| Mar-11 | Germany CPI YoY | 5.1% | 5.1% | 5.1% |

| Mar-15 | Germany ZEW Survey Expectations | 5.0 | — | 54.3 |

| Mar-15 | Germany ZEW Current Situation | -23.0 | — | -8.1 |

| Mar-15 | PPI Final Demand YoY | 10.0% | — | 9.7% |

| Mar-16 | FOMC Rate Decision (Upper Bound) | 0.50% | — | 0.25% |

| Mar-17 | Eurozone CPI Core YoY | 2.7% | — | 2.7% |

| Mar-17 | Housing Starts | 1,700k | — | 1,638k |

| Mar-17 | Initial Jobless Claims | 218k | — | 227k |

Strengths

- The best performing precious metal for the week was silver, up 1.36% on the good gold tape. Gold climbed to a 19-month high above $2,000 an ounce amid mounting concerns over inflation and continued geopolitical tension between Russia and Ukraine. Bullion had earlier extended its biggest decline in 14 months, reports Bloomberg, on hopes that talks between the countries’ foreign ministers could lead to a solution. However, as talks failed to make progress, gold erased those losses.

- The London Bullion Market Association said on Monday it was removing all six Russian gold and silver refineries from its good delivery list. This amounted to a de facto ban on new bars from Russia being traded in the London market.

- Russia’s central bank is unlikely to sell its gold holdings to support a drop in the ruble amid sanctions, reports Goldman Sachs. The difficulty involved with liquidating gold reserves and the presence of a large current account surplus means Russia will focus on capital account restrictions to manage the ruble exchange rate. Historically, capital restrictions are a more effective tool at managing a tumbling currency than gold sales.

Weaknesses

- The worst performing precious metal as we close out the week was palladium, down 6.30%. Palladium surged to an all-time high on mounting concerns that exports from top producer Russia could be disrupted by sanctions. Prices are so high, in fact, that thefts of the parts that use the metal in cleaner automobiles (catalytic converters), have risen sharply in the U.S. and elsewhere, reports Bloomberg. The metal did slide back as much as about 9% mid-week, however, after reaching its high price.

- Sibanye-Stillwater said the biggest unions at its gold mines gave notice that their workers will go on strike from Wednesday after talks over a new wage deal failed, reports Bloomberg. The strike threat comes as the South African company faces soaring costs at some of the world’s deepest and oldest gold mines. Sibanye’s three gold mines employ over 30,000 workers, the article continues.

- Royal Bafokeng Platinum reported disappointing fiscal year 2021 results as highlighted in the company’s trading statement. Its fiscal year 2021 underlying EBITDA missed consensus by 23% due to a combination of lower-than-forecast production volumes and revenue realizations, and higher-than-forecast unit costs, (with fiscal year 2021 EBITDA margins seven points lower than consensus).

Opportunities

- JPMorgan recommends increasing exposure to gold. Last week saw the highest inflation in commodity prices in 60 years (up 12% last week). Inflation risks are also severe due to the immediate supply shock to Russian commodity exports, along with the unfolding impact to downstream supply chains. JPMorgan believes extreme geopolitical risks could extend dovish monetary policy and the duration of negative real yields. Against this backdrop, there are clear macro tailwinds for South African-listed gold producers, which collectively trade at discounted equity multiples to their global gold peers.

- Shares in mining companies could outperform over the next three years as a result of consensus earnings upgrades and a re-rating of equity valuations, Jefferies says. Underinvestment in new mine capacity, combined with decarbonization-driven demand and cyclical consumption growth, should lead to tighter markets and higher prices for some key commodities between now and 2025, the U.S. bank says.

- According to Goldman Sachs, the recent rally across commodities and rising global geopolitical uncertainty means that its upside scenario on gold investment and central bank demand is now becoming the base case. At the same time, gold consumer demand continues to accelerate, driven primarily by buyers in Asia. The group now expects all three major components of gold demand to increase strongly in 2022. The last time Goldman saw all major demand drivers accelerate simultaneously was in 2010-2011 when gold rallied by almost 70%.

Threats

- The London Platinum and Palladium Market has decided not to revoke the accreditation of Russian refineries, allowing them to continue supplying precious metals to the trading hub. Following a meeting of the management committee, no changes will be made to its good delivery list, according to a spokesperson. There are currently two Russian refineries with accreditation to mint platinum and palladium for the London market.

- Kinross Gold announced that it is suspending Russian operations. The company’s Kupol mine was expected to produce 35,000 ounces which represents about 13% of total production. This week, in response to foreign companies exiting Russia, the government announced a plan whereby they would transfer the assets to external managers to preserve property and employees.

- Russia’s invasion of Ukraine could further shift investment from palladium to platinum if Russian supplies remain off the market. South Africa is one of the few countries that would benefit near term from the shift in markets.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All