At its March 10 meeting, the European Central Bank (ECB) surprised the market by announcing an acceleration of its tapering program—wrapping up securities purchases earlier than anticipated. Most investors had expected the ECB to delay any changes to its purchases until at least the next policy meeting, especially after comments from senior members suggesting the need for patience.

Was an Accelerated Taper Premature?

The ECB characterized the decision as taking a middle ground between two extremes: 1) doing nothing and waiting to see how the crisis plays out or 2) reacting more aggressively to the runup in inflation that’s about to get worse. Inflation is the crux of the ECB’s mandate, and the central bank wants to have all options open as the year progresses.

There’s no doubt that this is a challenging juncture for formulating monetary policy. But in our view, the ECB wouldn’t have foreclosed any of its options by doing nothing last week and waiting another policy meeting cycle. By being hawkish at last week’s meeting, the ECB risks worsening an economic situation that’s already deteriorating rapidly.

Unsurprisingly, the market reaction to the hawkish surprise saw interest rates rise, peripheral spreads widen and equities fall. Those developments represent a tightening of financial conditions that we believe is inappropriate for the current economic situation. Easy financial conditions have been a key pillar of growth both in Europe and globally over the last several quarters and, as conditions tighten, the forward growth outlook will deteriorate. Rising peripheral spreads, in particular, threaten the ability of governments to support populations facing a massive shock to real incomes from rising energy prices.

Risk of Euro-Area Recession Has Increased

While there’s still much uncertainty, we believe that the Russian invasion of Ukraine, combined with less monetary policy support from the ECB, pushes the risk of a recession in the euro area above 50%. In fact, a recession in the next few quarters is now our base case for several reasons.

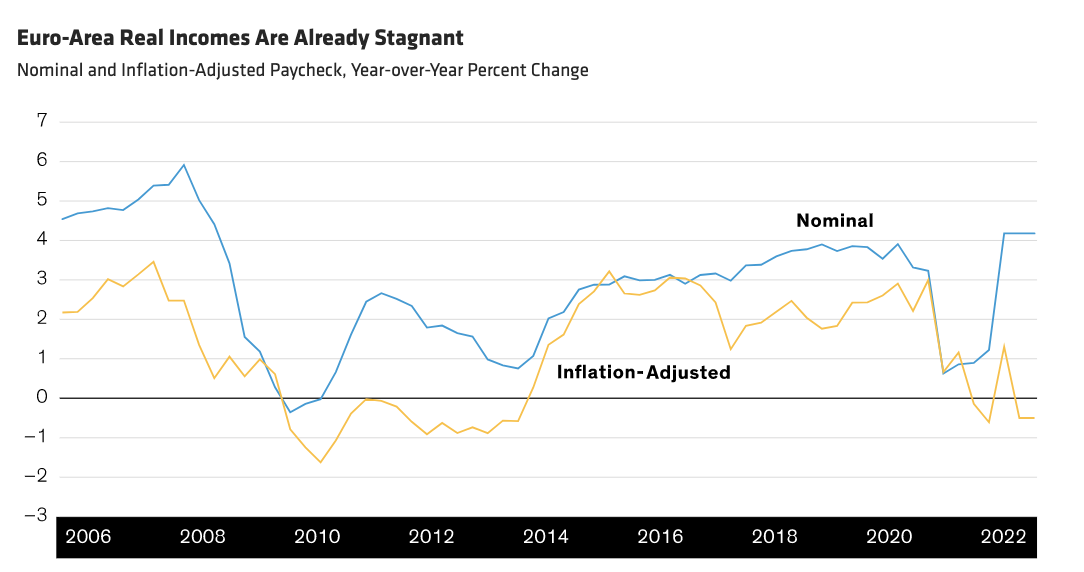

1. Even before the invasion, euro-area consumers were already struggling to keep pace with rising prices as the real, or inflation-adjusted, aggregate paycheck had started to shrink (Display).

2. Unless the spike in energy prices reverses almost immediately, it will push inflation higher and real incomes lower—a grim outlook for euro-area consumers.

3. There’s the possibility of rationing for energy and other commodities that Europe typically imports from Russia or Ukraine.

4. Economic sentiment could be hurt by the combination of supply shortfalls, rising prices and—of course—the war itself.

Past performance does not guarantee future results.

Through February 28, 2022

Source: Refinitiv Datastream

We see the euro area facing an imminent demand shortfall, which we think calls for dovish—not hawkish—monetary policy. The situation today in many ways parallels the one prevailing around the 2011 ECB rate hike, in which policymakers responded to an energy shock by raising rates, only to see the economy turn downward. By the end of that year, the ECB was again cutting rates.

The Path from Here

A recession isn’t a certainty at this point. Hostilities could cease in short order and trade flows resume, presumably accompanied by falling energy prices. Or euro-area leaders could agree on a significant fiscal package to support consumers (though the recent rise in interest rates would make that package more expensive). And, of course, the ECB has made it clear that rate hikes aren’t inevitable.

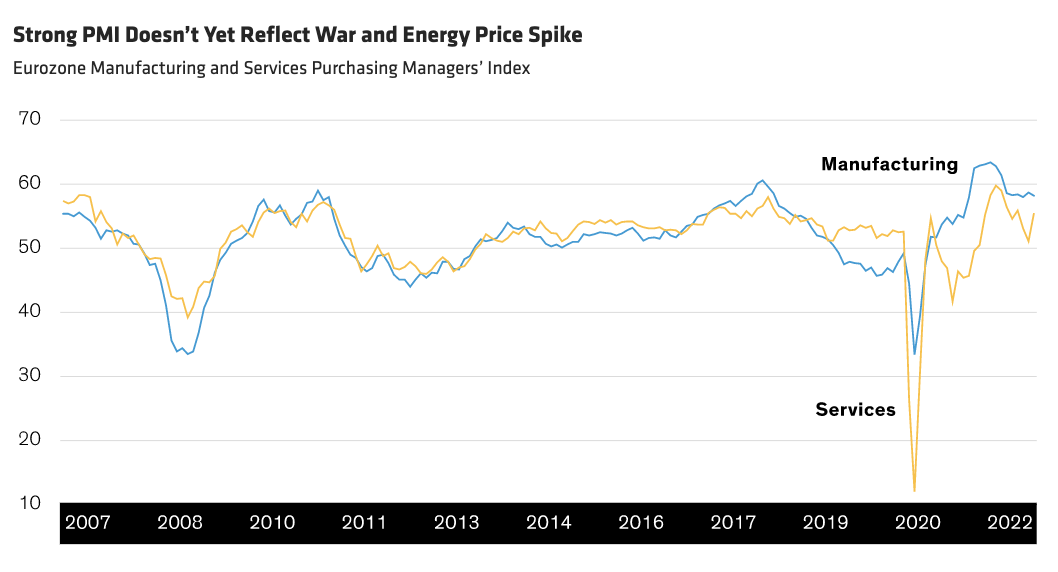

The euro area’s economic starting point is relatively robust, based on Purchasing Managers’ Index (PMI) surveys, the best indicator of euro-area growth (Display). However, the latest readings predate both the war and the rise in energy prices. We expect PMIs to fall sharply over the next few weeks, and the European economy to slide in line with that signal.

Past performance does not guarantee future results.

Through February 28, 2022

Source: Refinitiv Datastream

Ongoing negotiations among European leaders could, of course, change the picture. For instance, a fiscal innovation would likely offset some of the negativity in the current economic environment. Failing that, we’ll have to wait and watch for improvement in the geopolitical situation before becoming more optimistic about the euro area’s economic outlook.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein