In June of 2021, KCR’s Equity Research Team wrote a brief but pointed review of the legendary treatise on value investing, A Margin of Safety by Seth A. Klarman. With only 5,000 copies of the book in circulation, we hold our copy close but wish to share the wisdom of the billionaire author freely as he intended. Like the work of Benjamin Graham and Warren Buffett, we believe Mr. Klarman’s teachings are a critical underpinning to successfully preserving and compounding wealth.

As the world grapples with a supply chain crisis, dire shortages of fertilizer that put the world at risk of famine, the crisis and fall-out from the attack on the Ukraine and rising interest rates, we believe the benefits of a margin of safety approach have never been more important than today.

In our August 2021 missive, we noted since the start of 2017 Growth had outperformed Value in Large Cap by a significant margin. Specifically, the Russell 1000G rose over 184% while the Russell 1000V rose “only” 118%. This phenomenon is more pronounced in the Russell 2500 Growth and Russell 2500 Value Indexes.

In this piece, we will walk through the following:

- The trailing five year returns to Growth, Core, and Value to explain the analogs to the dot.com mania

- Highlight the severity of current risks we believe are underappreciated by investors

- Offer a very simple way to build a margin of safety into your investment process

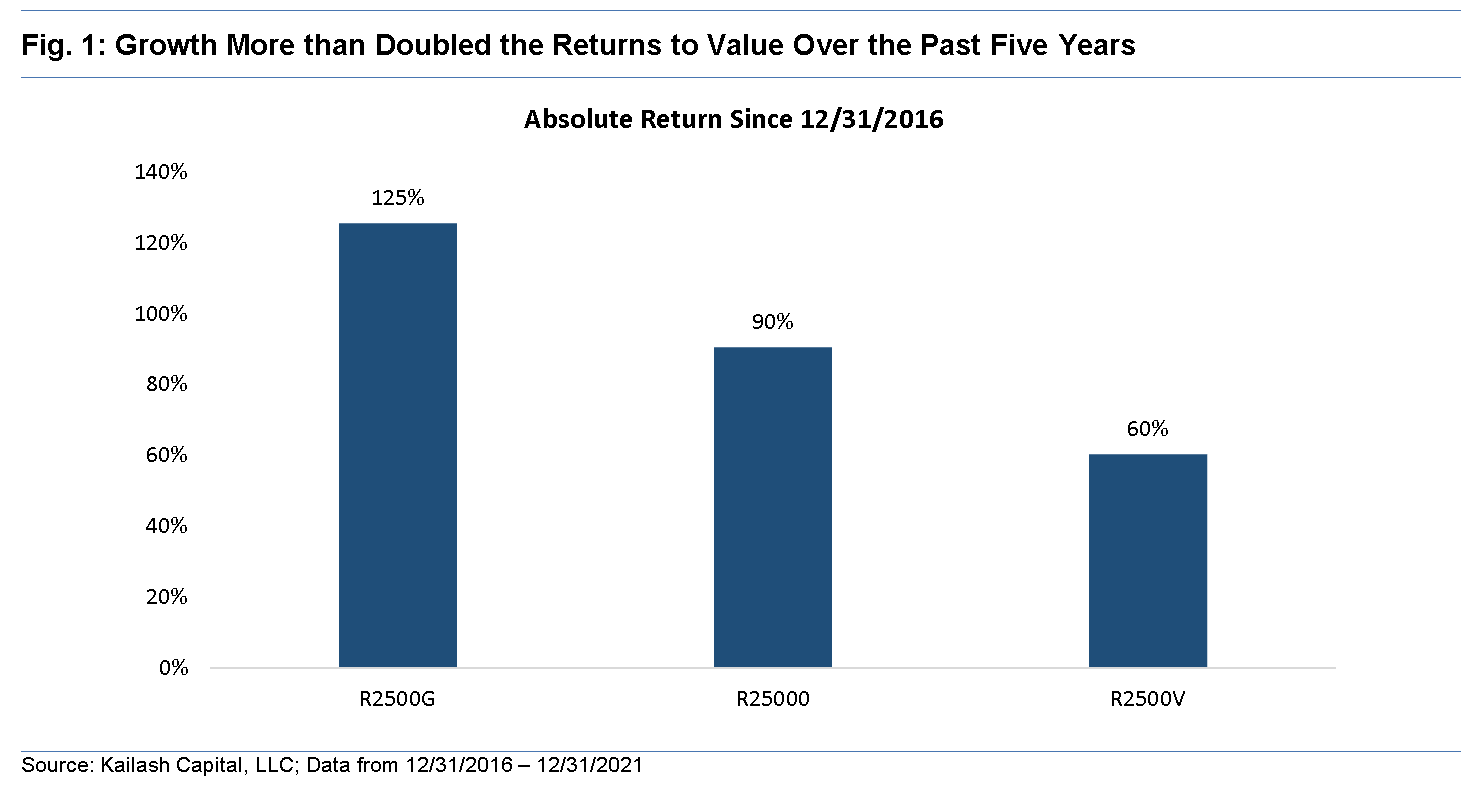

Figure 1 below shows the trailing five-year returns to the Russell 2500 Growth, Core, and Value Indexes. Growth rose 125%, trouncing the 60% return to Value by more than two to one. In an environment of loose credit and low-interest rates, we were not surprised to see a speculative fervor grip the nation.

If the Past is Prologue: Why A Margin of Safety in Investments Matters Now

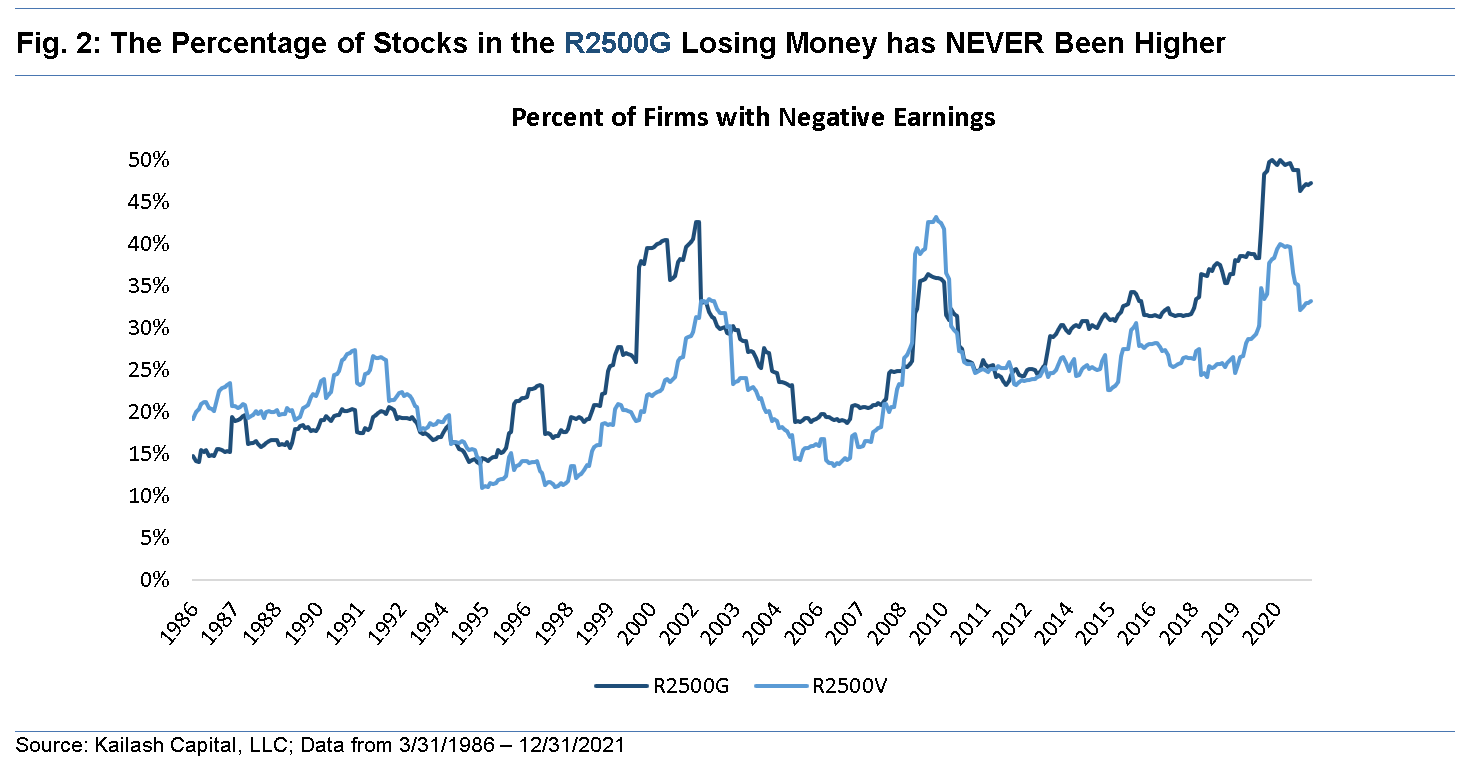

The chart below shows the percentage of stocks in the Growth and Value indexes that lose money. The percentage of stocks in the Growth Index losing money is just shy of 50%, a level above that seen at the peak of the dot.com mania. The Value Index is also elevated but far below the level seen in the Growth Index.

As we will show, history suggests the prevalence of loss-makers in the growth index will inflict severe damage on investors in the Growth index.

Will Value Offer a Greater Margin of Safety Compared to Growth?

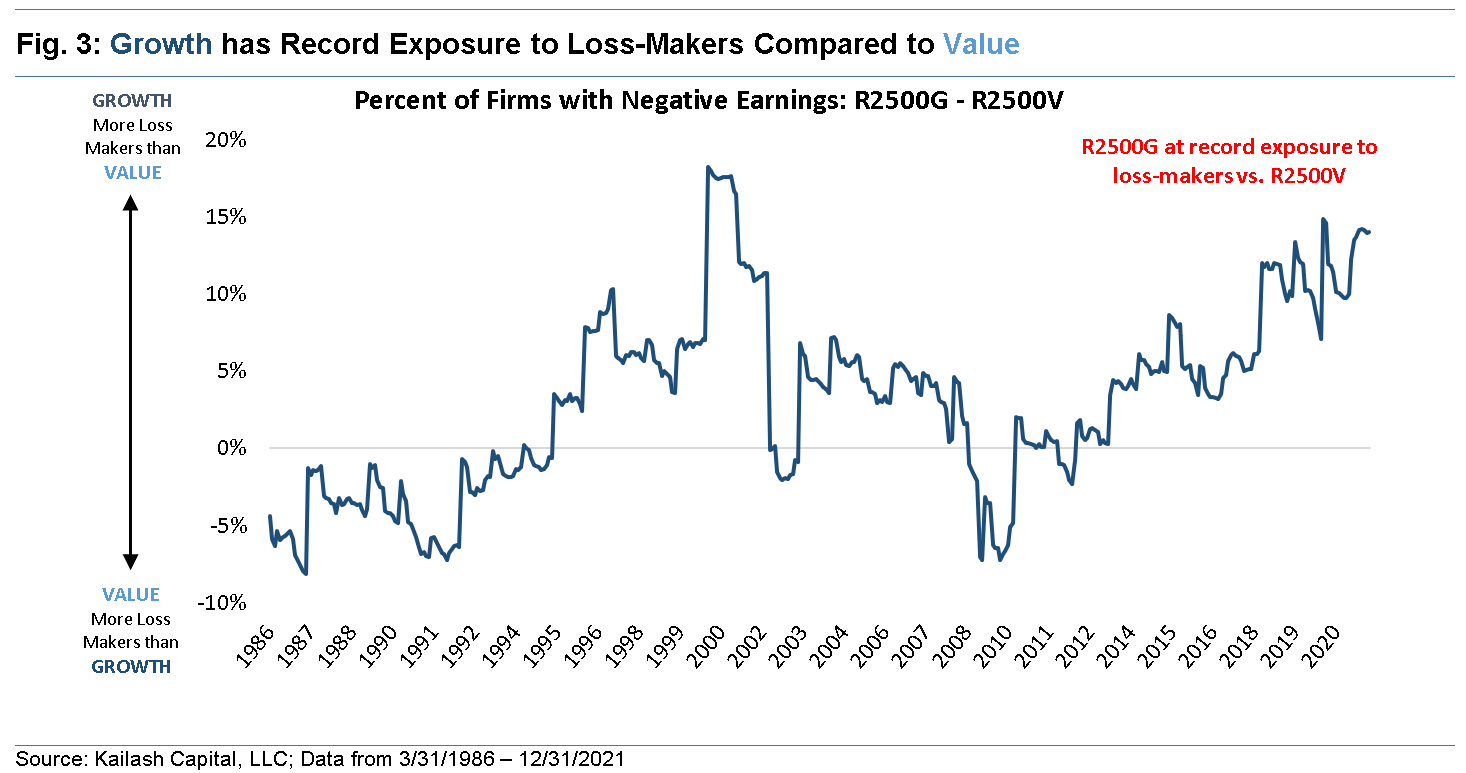

The chart below simply subtracts the navy-blue line from the light blue line from Fig. 2 above. So the line in Fig. 3 below shows how many more loss-making firms Growth has compared to Value.

Fig. 3 below in three bullets:

- When the line is positive, it means Growth has more exposure to loss-making firms than Value

- When the line is negative, it means Value has more exposure to loss-making firms than Growth

- Only at the peak of the internet bubble have investors in the Growth Index carried more exposure to loss-makers when compared to the Value Index.

Bailouts & Euphoria: When Loss-Makers Thrive

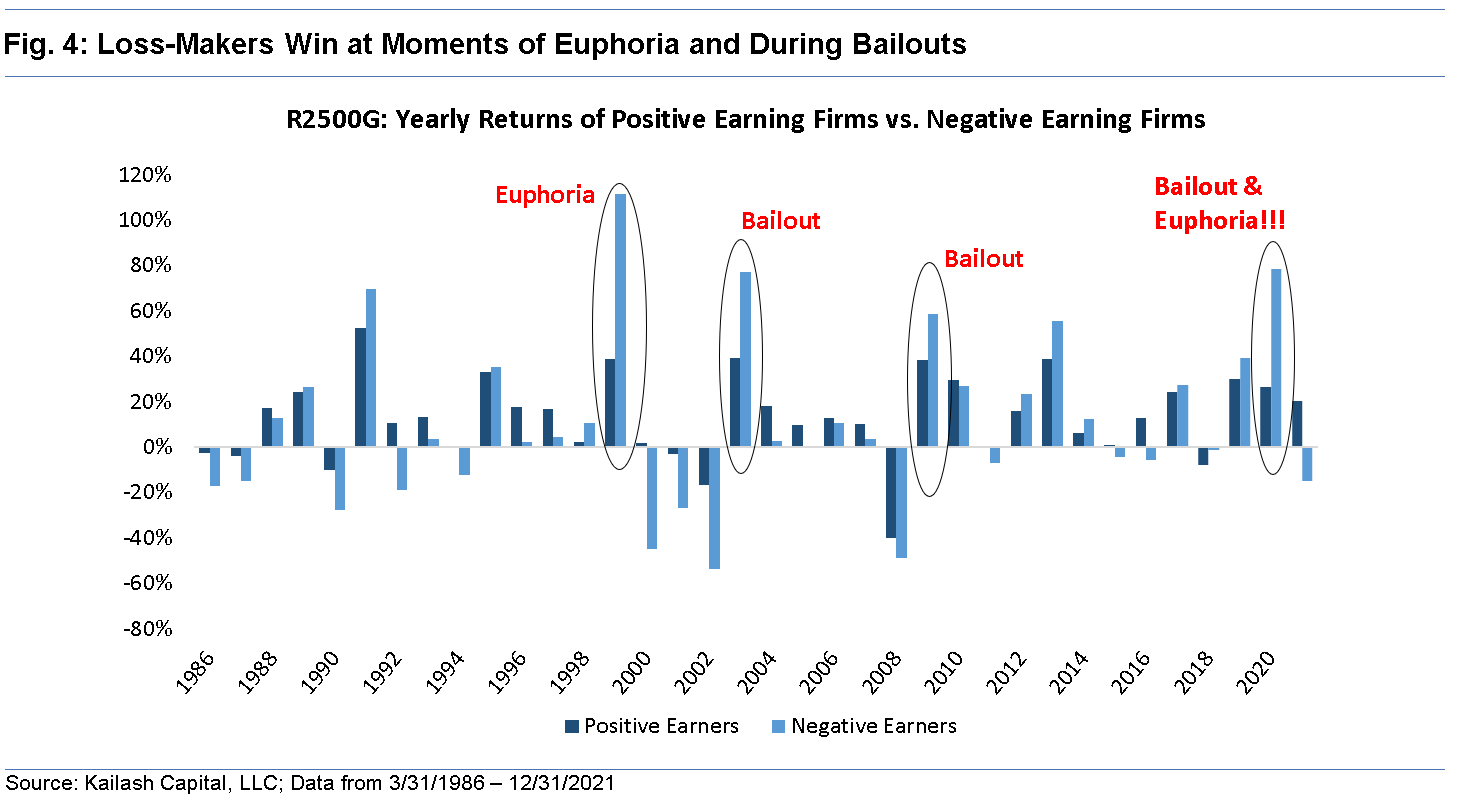

The navy-blue bars are the annual returns to stocks in the R2500G that make money. The light blue bars are the annual returns to stocks in the R2500G that lose money.

Loss-making companies tend to soar at speculative peaks and after big bailouts by the government. But the backlash is severe when the music fades.

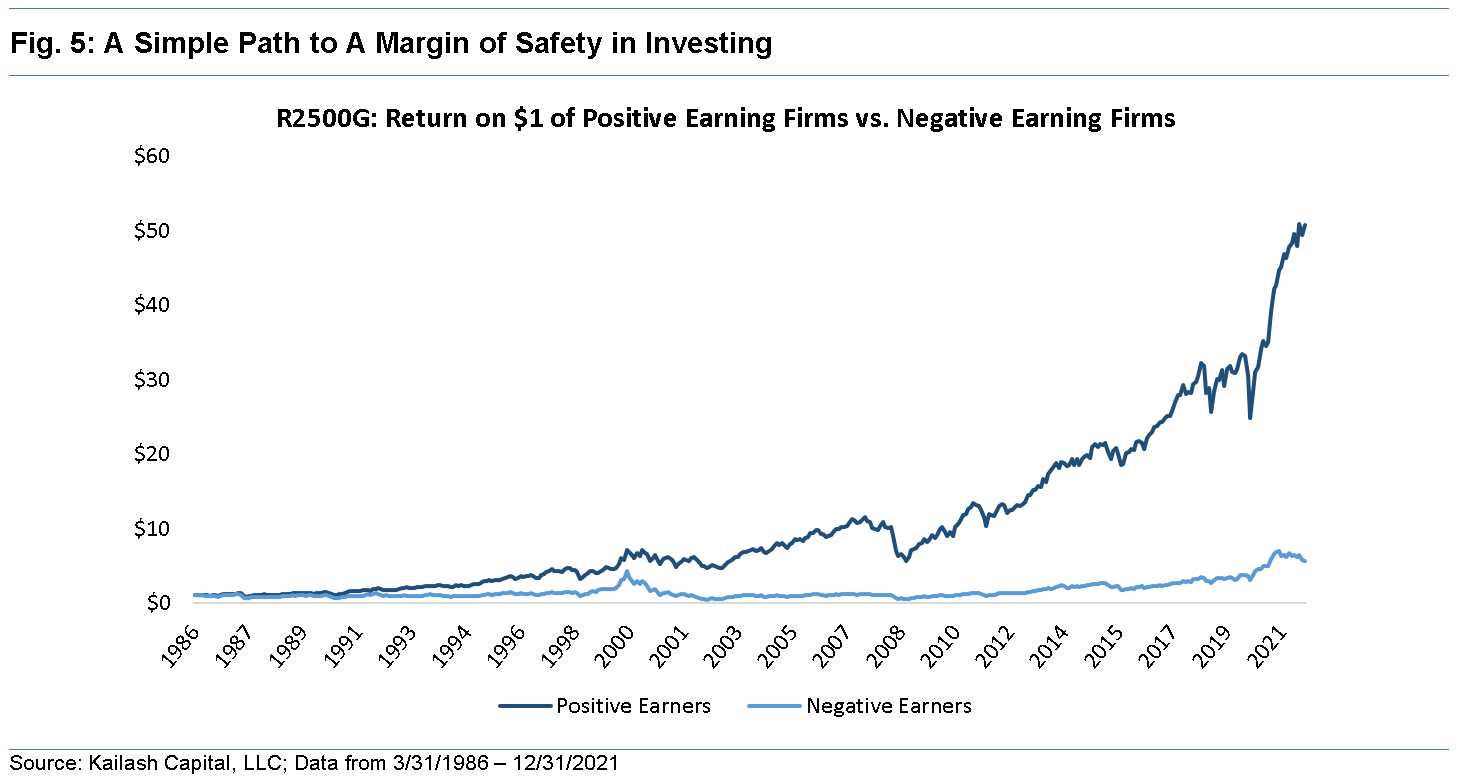

A Margin of Safety Made Easy: Avoid Indexes Loaded with Money Losing Stocks

The navy-blue line represents the compound returns since 1986 if you bought just the stocks in the Growth Index that made money. The light blue line shows the results if you bought only the firms that lost money. We believe this is as intuitive as it is obvious.

Over the long haul, companies that lose money underperform their profitable peers by a wide margin.

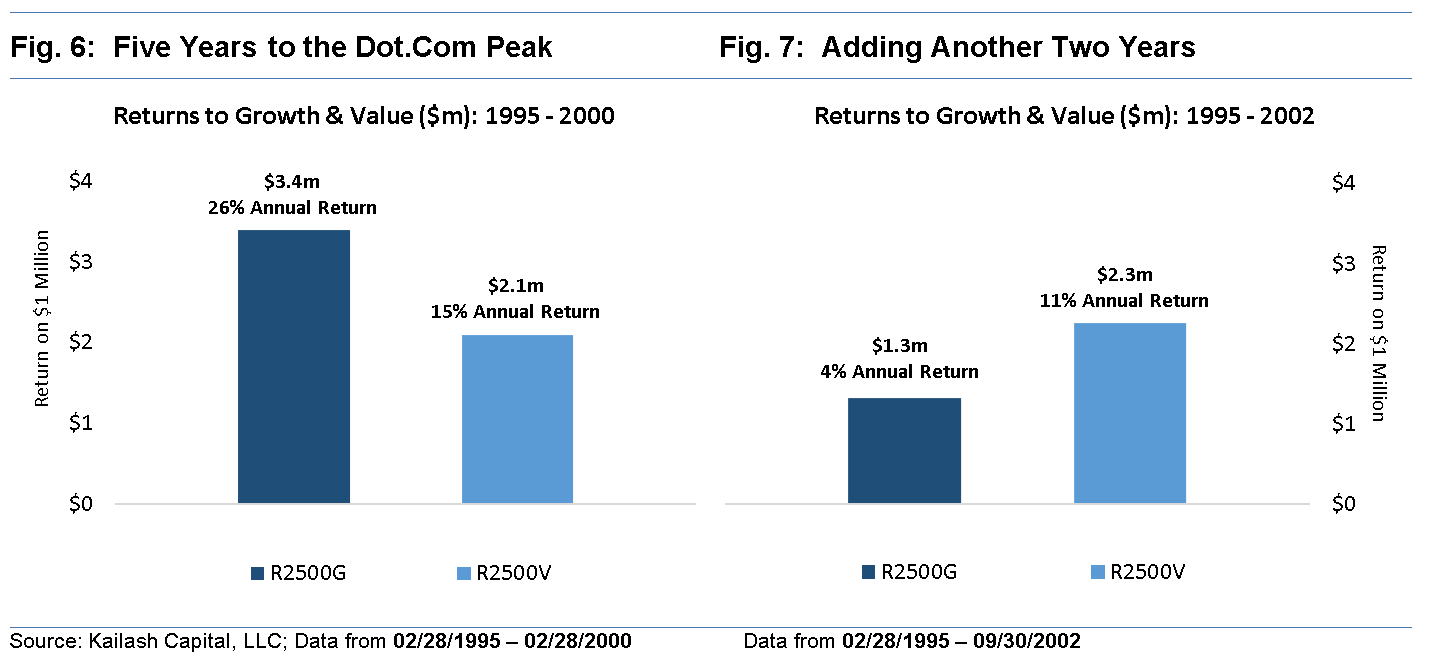

The two charts below show that shifting money from a Growth to Value Index might mitigate some of these risks. Figure 6 on the left shows what happened if you invested $1,000,000 in the Growth and Value Indexes, respectively, in the five years from February of 1995 to the peak of the dot.com mania in February of 2000. The money in the Growth Index would have grown to a staggering $3.4ml. The money in the Value Index grew to “only” $2.1ml.

The chart on the right, Fig. 7, simply extends the investment horizon through the full cycle and shows how that same million invested in February of 1995 fared if you just stayed invested through September of 2002. The results are stunning. The investor in the Growth Index saw their investment collapse by $2ml+ while the investor in the Value Index kept compounding higher, overtaking the investor in the Growth Index!

Conclusion:

- Do not overstay your welcome in an expensive growth index loaded with loss-making firms

- Embrace investing with a margin of safety sooner rather than later

- Consider engaging with a cost-efficient active manager with a track record of investing in proven and profitable firms at reasonable prices

About KCR:

Kailash Concepts is an equity investment research firm that has been in the industry for the past 12 years. The research team has 70 years of combined experience. The company provides the most rigorous, credible, and easy-to-use investor insights into market opportunities and also manages assets via SMAs, private funds and mutual funds through their sister firm, L2 Asset Management.

Copyright, Kailash Capital, LLC

© Kailash Concepts Research

Read more commentaries by Kailash Concepts Research