Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

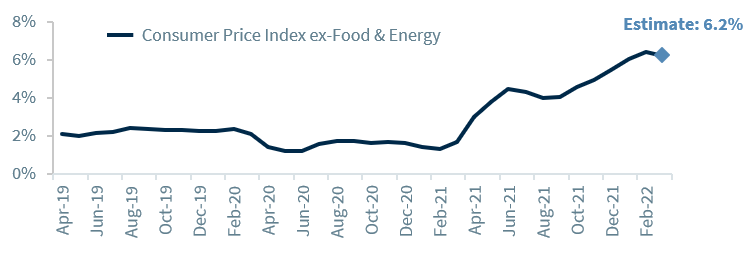

- Core inflation may have reached its peak

- Job & wage gains may counteract pricing pressures

- Earnings environment will normalize this year

Play ball! Opening Day is a day of optimism for baseball fans across the country. The crowds return to the stadiums to enjoy America’s pastime knowing every team is starting with a fresh record and renewed hopes of contending for a championship. With the excitement of what’s ahead, the losses from the prior season become a distant memory. Contrary to this mindset, many investors entered this year with the expectation that the successes of last year would carry into 2022. Instead, geopolitical hotspots came out of ‘left field’ and the start of Fed tightening to combat soaring inflation rattled the financial markets. With next week the ‘big leagues’ in terms of potential market moving events, we are ‘covering all of the bases’ of what will be released and our expectations moving forward.

All expressions of opinion reflect the judgment of Raymond James & Associates, Inc., and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. There is no assurance any of the trends mentioned will continue or that any of the forecasts mentioned will occur. Economic and market conditions are subject to change. Investing involves risk including the possible loss of capital. International investing involves additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. Past performance may not be indicative of future results.

© Raymond James

Read more commentaries by Raymond James