Quarterly Review and Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDisaster

Disaster is a strong but appropriate word that applies perfectly to the state of U.S. monetary policy. Consider the following:

A) The Fed, in reaction to the COVID-19 crisis, dropped the Fed funds rate to 0.25 bps and expanded total reserves of the depository institutions by an average of 63% in 2020 and 2021. This unprecedented growth was achieved by increasing total U.S. Treasury and other securities held outright by $4.5 trillion, equaling 70% of the $6.4 trillion increase in total Treasury securities outstanding. Consequently, the commercial bank deposit component of M2 (that accounts for about 78% of the M2) surged by a record 20.5% over the past two years. This fact reveals the massive coordination of monetary and fiscal policy as government checks were directly funded by monetary largesse. In the face of an unsurpassed breakdown in product delivery systems, this money creation caused a massive imbalance between the demand and supply of goods.

B) The result of the coordinated monetary and fiscal actions was a 5.7% increase in real GDP last year, the best rise since 1984 and a 10.1% rise in nominal GDP, the highest since 1984. With the aggregate demand curve shifting outward and the aggregate supply curve shifting inward, the headline CPI inflation rate jumped from 2.3% in the twelve months ending in December 2019 to 8.5% in the twelve months ending March 2022, the fastest such increase in forty years. Reversing the past monetary and fiscal excess liquidity error will take time and persistence by the Fed.

Harm of Favoring Employment Over Inflation

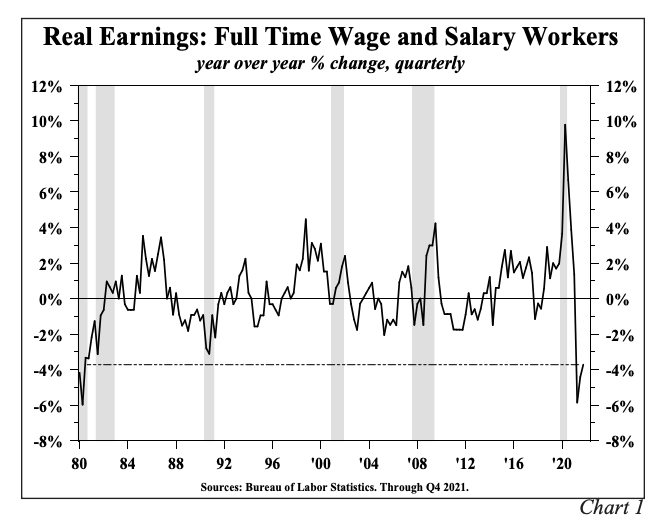

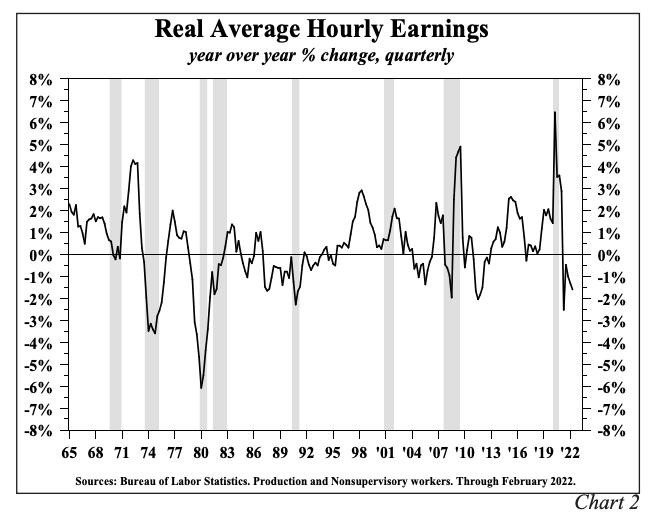

Most Americans have suffered a substantial fall in their standard of living over the past twelve months. In the latest available twelve-month change, 116.2 million American wage and salary workers suffered a 3.7% decline in their inflation adjusted paychecks, the largest drop since 1980 (Chart 1). This alone more than offsets the gain in income going to the 6.5 million newly employed in latest twelve months. In addition, salary workers suffered a larger loss in standard of living than hourly employees (Chart 2).

Inflationary damage to the 70 million retired Americans cannot be calculated in precise terms, but qualitatively the situation is not good. Those covered by Social Security received a 5.9% cost of living adjustment (COLA), however most private pensioners do not have COLAs.

A rough estimate is that approximately 50 million or more retirees’ real income has been seriously eroded by the forty year decade high inflation rate. Summing those whose income trailed price increases (116.2 + 50) yields a figure of approximately 170 million Americans. The sizeable adverse impact of inflation is consistent with a decline in real disposable personal income in 11 of the 13 latest months. Eighty five percent of U.S. households make under $150,000 a year, with many living from paycheck to paycheck or on steady salaries. The imbalance between those who benefitted and those who were harmed from the monetary and fiscal policies pursued over the last two years is abundantly clear. The 8.5% inflation rate has dramatically lowered the standard of living of over 170 million individuals. When this circumstance is compared with the accomplishment of the objective by monetary and fiscal authorities to lower the unemployment rate from a recession high of 14.7% in April of 2020 to 3.6% today, the fallacy of twin mandates is abundantly clear. The lowering of the unemployment rate reflected the creation of 20.4 million new jobs. Is it a fair balance to help 20 million individuals at the expense of permanently harming 180 million?

The Fed's Mandate

The greatest students of the Fed, like Milton Friedman and Alan Meltzer (author of Fed’s most detailed history), as well as former Fed Chairman Paul Volcker would not be surprised that the Fed backed themselves and the economy into a huge hole by trying to balance competing mandates from Congress. John Taylor and John Cochrane, both Stanford Professors and renowned monetary experts, foresaw the untenable position the Fed was putting themselves in the summer of 2021 by not addressing the inflationary surge that was evident.

Under the Federal Reserve Reform Act of 1977, the Fed expanded its role to “the goals of maximum employment, stable prices, and moderate long-term interest rates.” Ironically, these goals have come to be known as the Fed’s “dual mandate” even though there are three goals. The flawed dual mandate of inflation and unemployment stems from the basic fact that no stable trade-off exists between wage increases and the unemployment rate. To make matters worse, in practice the Fed has allowed the dual mandate to morph into a single mandate centered on the Phillips Curve. The 1977 Act does not spell out the nature of the trade-off between the unemployment rate and the inflation rate nor does it say how the Fed should act if the mandates are at odds in terms of the policy approach (neither does the 1978 Humphrey Hawkins Full Employment Act). Two considerations indicate the influence of the Phillips Curve should have ended long ago: (1) critical theoretical arguments from great monetary theorists, and (2) empirical evidence.

The Great Theorists

In a 1967 peer-reviewed paper, Edmund Phelps challenged the theoretical structure of the Phillips Curve, and Milton Friedman, independently of Phelps, came to similar conclusions. In the view of Friedman and Phelps (Economics Nobel Prize winners in 1976 and 2006, respectively), real wages would adjust to make the supply of labor equal to the demand for labor and no trade off would exist.

In a paper presented at the 2014 Federal Reserve Bank of Chicago conference, Alan Meltzer summarized the root cause of the Fed’s policy errors and long record of failed forecasts as follows: “The Fed’s error was to rely on less reliable models like the Phillips Curve … that ignore or severely limit the role of money, credit, and relative prices.” By focusing on the Phillips Curve, Meltzer contended that the Fed overemphasizes information in very short monthly and quarterly data periods while giving insufficient information about persistent trends in money and credit, which are the very aggregates that the Fed supplies. In short, by relying on the Phillips Curve, the Fed avoids developing a strategic view of its role and the complex world in which it operates. Volcker explained publicly and to the Fed staff that the Phillips Curve was unreliable and not useful. Alan Greenspan was less outspoken, but he also rejected Phillips Curve forecasts as unreliable. After Greenspan left the Fed, the staff re-established the focus on the Phillips Curve, one of the central dogmas of Keynesian economics.

John Taylor invented a now very famous interest rate forecasting model, which was outlined in his 1993 study, “Discretion versus policy rules in practice.” This model, commonly referred to as the “Taylor rule,” suggests how central banks should change interest rates to account for inflation and other economic conditions. The Taylor rule indicates that the Fed should raise rates when inflation is above target or when real GDP growth is too high and above potential real GDP. The rule also suggests that the Fed should lower rates when inflation is below the target level or when real GDP growth is too slow and below potential real GDP. Taylor, like Friedman and Meltzer, developed this rule because of the repeated failures of discretionary monetary policy. Since the Fed’s founding in 1913, monetary tightening has resulted in hard landings in all but about 10 % of the cases. Some of the soft landings avoided a U.S. recession but still caused a financial crisis.

Here are Taylor’s prophetic words in the August 12, 2021 issue of Harvard’s Project Syndicate: “Despite a sharp increase in the rate of money growth, the central bank is still engaged in a large-scale asset-purchase program (to the tune of $120 billion per month), and it has kept the federal funds rate in the range of 0.05 to 0.1%. That rate is exceptionally low compared to similar periods in recent history. To understand why it is exceptional, one need look no further than the Fed’s own July 9, 2021, Monetary Policy Report, which includes long-studied policy rules that would prescribe a policy rate higher than the current actual rate. One of these is the “Taylor rule,” which holds that the Fed should set its target federal funds rate according to the gap between actual and targeted inflation.” Later he writes, “If you plug in the current inflation rate over the past four quarters (about 4%), the gap between GDP and its potential for the second quarter (about -2%), a target inflation rate of 2%, and a so-called equilibrium interest rate of 1%, you get a desired federal funds rate of 5%.”

In the Fed’s Monetary Policy Report sent to Congress in late February 2022, the Fed did not include the section on policy rules that had been included in its reports since July 2017, when Janet Yellen was Fed Chair. Taylor wrote, “This omission is significant. It occurred at the same time the Fed has gotten well behind the curve, and inflation has risen as a result.”

Also in Harvard's Project Syndicate on Sept. 17, 2021, John Cochrane takes Taylor’s concept a step further and identifies the trap the Fed gets caught in when it declares that inflation is transitory. According to Cochrane, inflation can be stabilized with little risk of recession if people really believe the policy will be seen through. But, if the Fed’s attempt is viewed as subject to a quick reversal, the associated downturn will be worse. The Fed does not have the luxury to wait to see if inflation is transitory or not. Here is Cochrane’s compelling argument: “Fighting inflation is much easier if inflation expectations do not rise. Our central banks insist that inflation expectations are “anchored.” But, by what mechanism? Well, by the faith that those same central banks would, if necessary, reapply the harsh Volcker medicine of the 1980s to contain inflation.”

Another outstanding economist, the late Stanford Professor Ronald McKinnon, analyzed the consequences of policies that are tolerant of inflation and government intervention in credit allocation. For McKinnon when inflation is tolerated, it undermines growth and leads to increased calls for government intervention, thereby pushing countries further in the direction of command-and-control economies. The share of the government sector, with its negative multipliers, increases, while the share of the private sector, with its positive multipliers, declines. This reinforces the upward trend of inflation, perpetuating the cycle.

Empirical Evidence

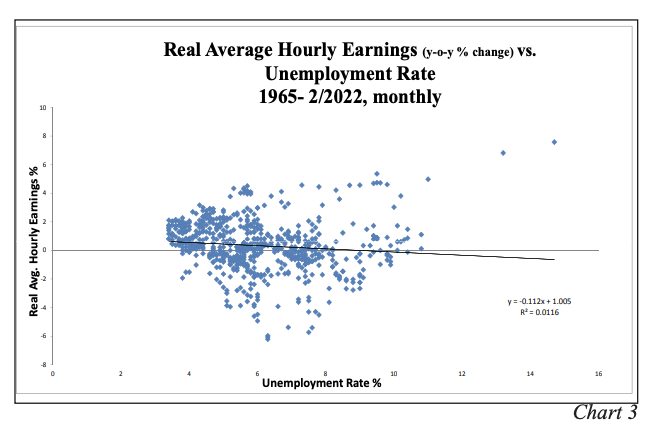

Substantial empirical evidence supports the theory. Chart 3, is the scatter diagram of the year over year percent change in real average hourly earnings against the unemployment rate, using monthly data from 1965 through February of this year. As the chart indicates, the result is virtually a flat horizontal line, nothing close to resembling a negatively sloped trade-off curve.

Policy Constraints

Monetary restraint has resulted in recessions in all but 10% of the cases since the Fed’s founding in 1913. Though rare in occurrence, achieving a soft landing or even a mild recession may be a hollow victory. In 1966, the Fed, under Chairman Mechesney Martin caused a credit crunch to try to contain inflation resulting from the Vietnam War. But, under serious pressure from the Johnson administration, the Fed reversed course and avoided a recession in 1967. However, the war inflation surged further out of control. The Martin Fed did induce a recession as a result of a serious credit crunch in 1969. This recession was extremely mild but caused the failure of the largest issuer of commercial paper (Penn Central Railroad) which resulted in a major financial crisis in May 1970. This led the Fed, now under chairman Arthur Burns, to speed up the easing of monetary conditions, including taking the extraordinary step of cutting the margin requirement on stocks. Then, after a severe auto industry strike, GM agreed to a highly inflationary wage settlement with the UAW. In the 1971 recovery, inflation showed little, if any, improvement and the rebound was extremely tepid. Facing a Presidential election in 1972, the Nixon administration simultaneously closed the gold window, engineered a massive devaluation of the dollar and instituted wage and price controls to hold inflation in check while the Burns Fed accelerated money growth at time when money velocity was stable. Growth was fast in 1972 and inflation was contained but, when the wage and price controls were lifted in 1973, inflation surged rapidly, and the Burns Fed was forced to adopt far more restrictive conditions than had been seen in 1966 and 1969. In 1973- 75 a very deep recession followed. The Vietnam War/Nixon inflation was not resolved until after three years of severe monetary restraint under the Volcker Fed and deep recessions in the early 1980s. As these historical cases indicate, failure to knock out inflation may achieve better shortrun economic performance but a terrible longerterm loss.

Restraints on Growth

Major debt and demographic strains remain a significant restraint on U.S. economic growth. This problem is exacerbated by deteriorating economic conditions around the world. Scholarly work indicates the massive surge in government spending in the past two years has pushed its multiplier deeper into negative territory, resulting in a fiscal drag of major proportions in 2022 and 2023 as deficits will have reversed from over $3 trillion to slightly under $1 trillion, according to the Congressional Budget Office. Tracking models currently estimate that real economic growth is slightly positive, indicating that the Fed will be tightening into what is an already unfolding slowdown. Thus, the Hobson’s choice for the Fed is do they accept even more pronounced economic weakness to bring inflation into their target range? Considering the historical record of imbalance where millions of people are affected by either higher inflation or higher unemployment, the Fed has no choice but to allow the unemployment rate to rise. Higher unemployment, while harmful to some, would benefit many more millions, if inflation is contained just reversing the pattern that was experienced during the past year of accelerating inflation. Restoring real wage and salary growth, in turn, would restore positive momentum.

Bond Market

The war in Ukraine has lifted bond yields by a quick 50 basis points, elevating it to nearly one full point above the year-end level of 1.9%. At this current level, the long-end treasury market has value considering the impending recessionary conditions which have always reduced inflation and interest rates. The economic data suggesting negative growth ahead include the following factors 1) the largest twelve month decline in real weekly earnings of 3.3% since this series began in 2000 which covers 72 million people. 2) Real per capita disposable income now stands 1.8% below one year ago levels and has fallen for seven consecutive months. 3) The composite index of the NFIB Small Business Survey sank to 93.2 in March the lowest since April of 2020. 4) Interest rate sensitive sectors such as housing and autos are already declining. 5) Inventories are rising rapidly and will accelerate further with any softness in demand causing cutbacks in production. 6) Fiscal policy turns restrictive in 2022 and there is just a hint of early restraint in Fed policy as total reserves declined by $425 billion since December and the main component of M2, other checkable deposits, has shown just 3.7% growth over the last three months.

These and many other harbingers of recession constitute a favorable environment for long-term bond investors. However, should the Federal Reserve cease in their efforts to calm inflation before it has been fully restrained, bond investors should be wary.

Hoisington Investment Management

Disclosures The Bloomberg U.S. Aggregate Bond Index represents securities that are SEC-registered, taxable and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities and asset-backed securities. The Bloomberg U.S. Treasury index covers the performance and attributes of all U.S. Treasury securities except for treasury bills and STRIPS. CPI is the Consumer Price Index as published by the Bureau of Labor Statistics. S&P 500 is the Standard & Poor's 500 capitalization weighted index of 500 stocks. You cannot invest directly in any index. The Bloomberg indices, CPI and S&P 500 are provided as market indicators only. Hoisington Investment Management Company (HIMCo) in no way attempts to match or mimic the returns of the market indicators shown, nor does HIMCo attempt to create portfolios that are based on the securities in any of the market indices shown. Returns are shown in U.S. dollars and net of management fees and include the reinvestment of all income. The current management fee schedule is as follows: .45% on the first $10 million; .35% on the next $40 million; .25% on the next $50 million; .15% on the next $400 million; .05% on amounts over $500 million. Minimum fee is $5,625/quarter. Existing clients may have different fee schedules. Past performance is not indicative of future results. There is the possibility of loss with this investment. Hoisington Investment Management Company (HIMCo) is a federally registered investment adviser located in Austin, Texas. HIMCo is not registered as an investment adviser in any other jurisdictions and is not soliciting investors outside the U.S. HIMCo specializes in the management of fixed income portfolios and is not affiliated with any parent organization. The Macroeconomic Fixed Income strategy invests solely in U.S. Treasury securities. Information herein has been obtained from sources believed to be reliable, but HIMCo does not warrant its completeness or accuracy; opinions and estimates constitute our judgment as of this date and are subject to change without notice. This memorandum expresses the views of the authors as of the date indicated and such views are subject to change without notice. HIMCo has no duty or obligation to update the information contained herein. This material is for informational purposes only and should not be used for any other purpose. Certain information contained herein concerning economic data is based on or derived from information provided by independent third-party sources. Charts and graphs provided herein are for illustrative purposes only. This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of HIMCo. To receive more information about HIMCo please call (800) 922-2755, or write HIMCo, 6836 Bee Caves Road, Building 2, Suite 100, Austin, TX 78746.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All