It's extremely difficult to watch the news and not feel overwhelmed by the avalanche of negative headlines. Some of them, such as the war in Ukraine, are heartbreakingly negative, outright terrifying, and tragic. Others – inflation, Fed hikes and extreme volatility—are clearly linked, but, at the same time, add to the sense of gloom that pervades the current U.S. equity markets.

Despite this glut of negativity, there are reasons to be constructive on market performance for the remainder of 2022. We’re at peak pain in the market and in an extreme risk-off investing environment. The news is never great at the bottom of a sell-off, so what is the path forward?

Let’s start with the on-going war in Ukraine. Clearly what is happening there is a human tragedy on a level that is hard to find adequate words for. Further, it’s clear that it has had a negative effect on the market for a litany of reasons. Setting aside the incredible human cost, what effects are likely to impact the market for the remainder of 2022?

While the war is disrupting energy and food supplies and casting a scary pall over the market, it is not the first nor the last “bad news” event that in the moment feels like a headwind that can never be overcome.

If what’s past is prologue, then referencing previous market-shaking events could be instructive. For example, looking back to March of 2020 at the onset of the Pandemic, was the market convinced at that time that the market would be materially higher over the next 18 months? No. Circumstances change and markets evolve. Similarly, it seems reasonable that the current war alone should not be enough to keep the market negative.

What about inflation and the corresponding rate hikes? The CPI release on May 11, 2022, was just the most recent data point reflecting high inflation and the necessity for rate hikes (with the first 25 basis points of tightening occurring on March 16, 2022, and an additional 50 basis points on May 4, 2022).

A strong case can be made that small cap equities historically experience strong performance following the first Fed rate hike in a cycle. The chart below shows the potential for positive market performance of small cap stocks over the rest of 2022 despite the looming rate hikes.

Not surprisingly, war and inflation lead to high volatility. This is to be expected. However, historically this kind of volatility has both presented buying opportunities and has not normally resulted in negative annual returns for the U.S. equity markets. Despite average peak to trough drops of 14.1%, the market has had a positive annual return in 31 of 41 years.

not possible to invest directly in an index.

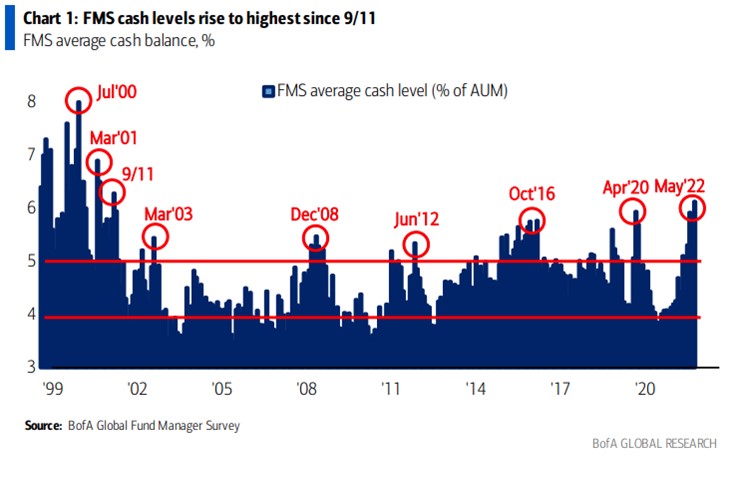

Another possible bullish silver lining to consider… as the following chart shows, instutitional cash levels have risen to the highest level since September 2011, which indicates everyone is bearish.

By far, the most fundamental reason to maintain a positive outlook on U.S. equities for the remainder of 2022 is that the U.S. economy remains strong and is expected to grow, and a strong U.S. economy means continued earnings growth.

Further, the war, inflation and volatility should ultimately be overwhelmed by strong earnings growth, which currently most analysts believe that we will continue to see. Investing in companies that can navigate through these myriad issues and grow their earnings has historically been a winning formula.

Investor fear—starting with the November Omicron outbreak—has driven the market lately, reversing gains made during the pandemic and causing markets to sell off very quickly on any hint of bad news. More important, the rapid market drop has likely provided a floor to market sell offs as nervous investors have likely already taken steps to manage downside risk given the jitters that they are experiencing.

Kevin M. Rendino is CEO and Daniel B. Wolfe President of of 180 Degree Capital.

© 180 Degree Capital

Read more commentaries by 180 Degree Capital