What You Need to Know

High inflation and the consequences of attempts to curb it are a top concern for today’s investors. We believe that, by hiking rates, policymakers can eventually slow demand enough to subdue price pressures, even in an environment of constrained supply. But this process takes time. In this paper, we describe the path we expect inflation to follow and the forces at play, from a shift in consumer spending to a cooling housing market, and we discuss the five major investment takeaways that will allow investors to survive—and thrive—in this challenging environment.

Inflation remains front of mind for investors and policymakers alike. Prices are rising at a rate not seen in generations, confounding expectations that a broader reopening of the global economy would ease pressures. Instead, a perfect storm of disruption has impacted the supply side of the global economy, pushing prices higher.

Those disruptions are resistant to forecasting, making it impossible to project near-term inflation. We don’t know when Chinese lockdowns will end, helping the global supply chain to heal. And we don’t know when the war in Ukraine will end, easing pressure on tight global commodity markets.

Given these uncertainties, why are we increasingly confident that prices will eventually moderate? Because while we lack visibility on the supply side of the global economy, developments on the demand side are coming into clearer view.

Monetary Policy Affects Demand

Prices reflect the interaction between supply and demand. When demand outstrips supply, prices must rise to re-equilibrate the economy. Supply-side constraints, such as Chinese lockdowns or war-induced commodity shortages, are beyond the purview of monetary policy—central banks can’t solve those issues by changing interest rates.

What they can do is slow demand such that, even in an environment of constrained supply, price pressures abate. That means tightening monetary policy to slow growth to a rate consistent with the ability of the supply side of the economy to keep pace.

And that is exactly what central bankers are doing. The US Federal Reserve has raised rates 75 basis points since March and is likely to add another 150–200 basis points of hikes later this year. Central banks in Canada, Australia and New Zealand are also hiking, and the European Central Bank appears poised to do the same in the next few months. Only the Bank of Japan and the People’s Bank of China are unlikely to raise rates due to idiosyncratic developments in their countries. Even so, the global trajectory is clearly toward higher rates.

The catch is that monetary policy works with a lag. Once rates rise, it takes time for the economy to feel the full effect. We shouldn’t expect higher policy rates to translate immediately into lower demand, slower growth and an easing of inflationary pressures. But, as the year progresses, we expect growth to slow, bringing inflation gradually lower.

Consumers to Rotate Spending from Goods to Services

As part of that growth slowdown, we expect consumers to increasingly spend on services rather than goods. Much of this upcoming rotation is simply making up for lost time. During the height of the pandemic, many services were unavailable, compelling households to rotate their purchases into goods. We estimate that Americans bought more than US$1 trillion of “excess” goods beyond the long-term trend.

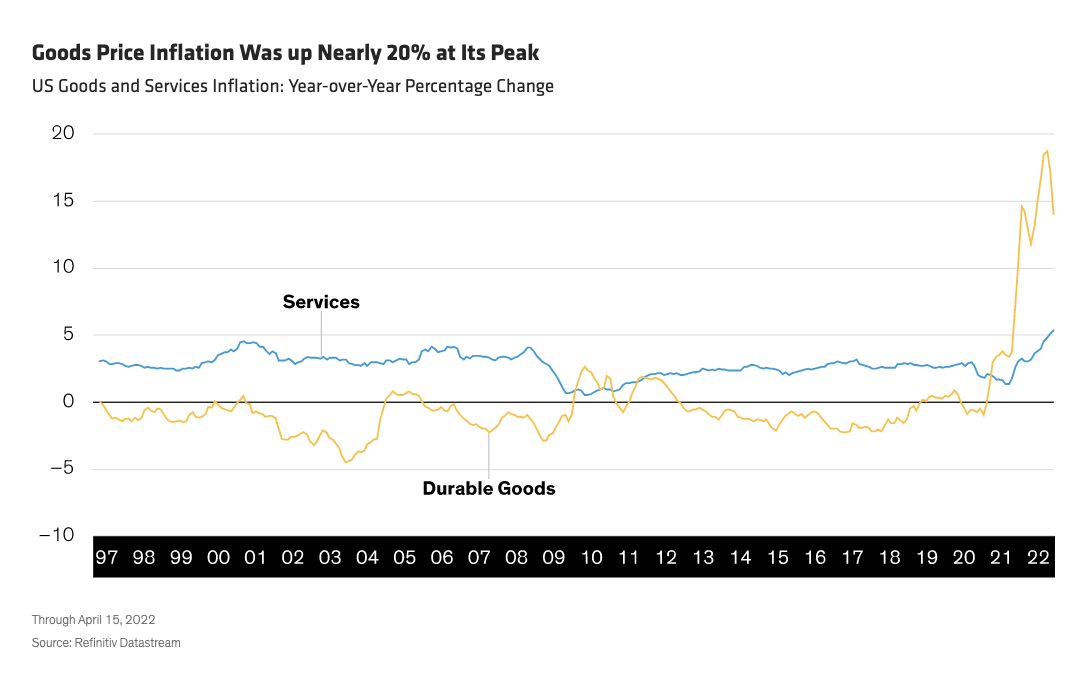

Another part of the upcoming rotation is a natural re-equilibration in an environment of higher prices. Because demand for goods has been so robust, and because goods trade has been particularly impacted by supply-chain disruptions, goods price inflation has soared—up nearly 20% year over year at its peak in the US (Display). That has made services comparatively affordable and thus more attractive, and we expect consumers to adjust their behavior accordingly.

Prices don’t have to fall for inflation to decelerate—inflation measures the rate of change in prices rather than the price level. So even if prices simply rise at a slower pace, inflation will turn lower. We are already seeing that for broad goods prices, which are off their peak, and in price declines for some categories that were particularly affected by COVID, such as used car prices.

What does that mean for inflation? We think it means that, over time, goods prices and services prices will converge, and that goods inflation will eventually fall below services inflation, as was the case before the pandemic.

Pushing goods price inflation lower will make a big difference in overall inflation, though it won’t entirely solve the problem. After all, services inflation is itself running at roughly 5% right now. That, too, will have to come down for inflation to return to target. That process is going to be slow, however, and we expect that inflation is likely still to be around 5% in late 2022 and early 2023, and it may be 2024 before it falls back to the Fed’s 2% target.

A Cooler Housing Market Will Help

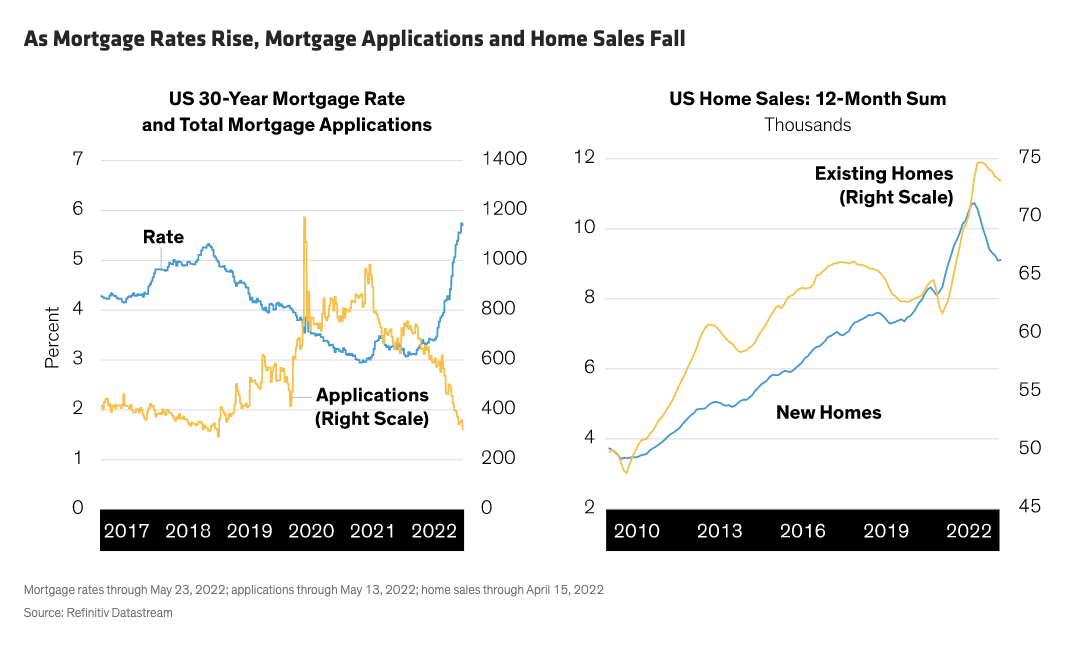

One of the biggest categories within services inflation is “owner-equivalent rent,” which is how the consumer price index captures the cost of housing. And housing is the part of the economy most sensitive to monetary policy.

Mortgage rates in the US have soared, rising above 5% for the first time in more than 10 years. Between that and the rise in housing prices over the past few years, affordability is extremely low. Not surprisingly, mortgage applications have fallen sharply, and sales of both new and existing homes have turned lower (Display).

This suggests that home prices are likely to slow their rate of increase, which should eventually bring services inflation lower too.

Monitoring Progress on Inflation

Because this process will take time, we don’t expect inflation to return to the Fed’s target in the near term. In our view, US core inflation is likely to be slightly above 5% at the end of 2022 and to remain at least modestly above 2% at the end of 2023, assuming that the Fed continues to raise rates and that rate hikes are effective at slowing growth—both of which we believe to be the case.

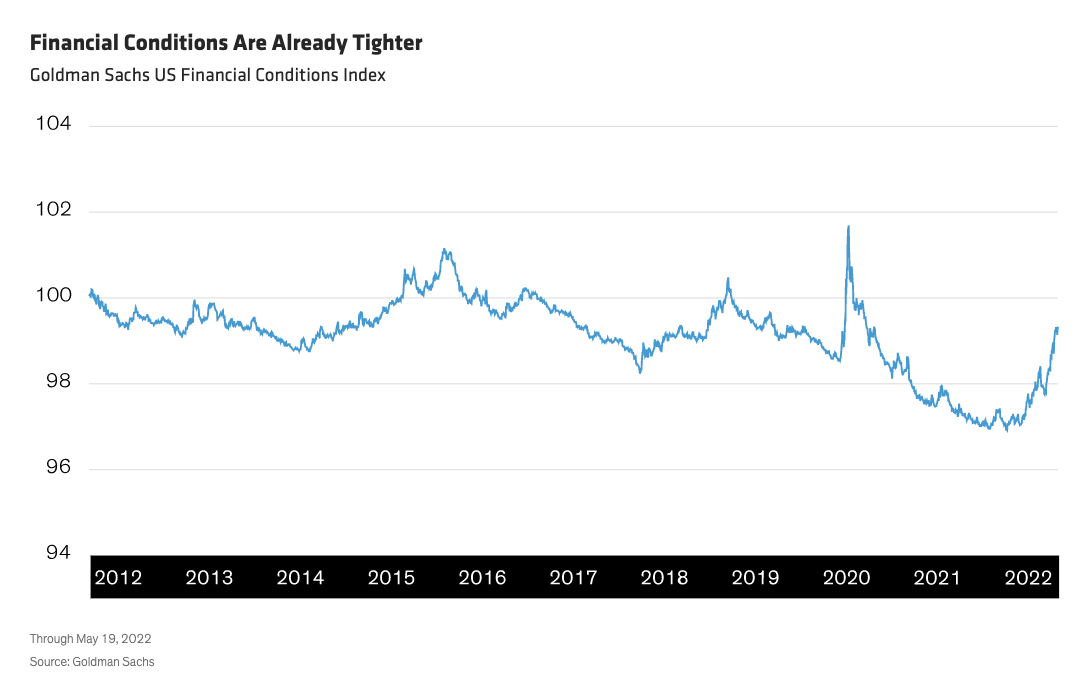

The best way to monitor progress toward that outcome is through a broader assessment of financial conditions. Things like lower equity prices, wider credit spreads and higher Treasury yields all work to slow demand by transmitting monetary policy from the central bank to the economy.

While there is no perfect measure of financial conditions, all credible metrics show a significant tightening of conditions (Display) since central banks made clear that they would respond to persistent inflation with tighter policy. That gives us confidence that an economic slowdown is in motion and will, in turn, bring inflation lower.

Is a Recession Inevitable?

Does a slowdown mean a recession is inevitable? We don’t think so. If central bankers have learned from past cycles, they may be able to thread the needle between a slowdown and a contraction to generate a soft landing.

It helps, too, that the starting point is good: household and corporate balance sheets are both in very good shape, and the labor market is strong. This suggests that the economy can withstand tighter conditions without rolling over.

The key question over the medium term is how aggressively central banks will tighten policy once evidence of slowing growth mounts. Inflation tends to lag the cycle, staying high even after growth slows. If central banks remain aggressive during that interval, the risks of a recession rise sharply. If, however, they take heed of history and slow the pace of rate hikes later in the cycle to allow their earlier moves time to take effect, the coming slowdown need not deteriorate into something more sinister.

Our forecasts capture this outcome—we expect growth to slow in every major economy and worldwide this year and into 2023, but then to stabilize as central banks slow the pace of rate hikes.

Implications for Investors

Uncertainty has weighed on asset valuations and generated extreme volatility. As the market lurches from fear of out-of-control inflation to fear of recession, investors are parsing every datapoint to divine the future. So what does it all mean for investors? We see five major implications:

1) Adopt inflation protection. Because inflation is likely to remain elevated for some time before it falls back to target, inflation protection can play a useful role in portfolios. In addition, inflation is more likely to rise again in future cycles, as disinflationary forces such as globalization recede. This makes central banks less likely to intervene to stabilize markets in future. Higher inflation thus poses a risk to markets, making explicit inflation protection an effective hedge.

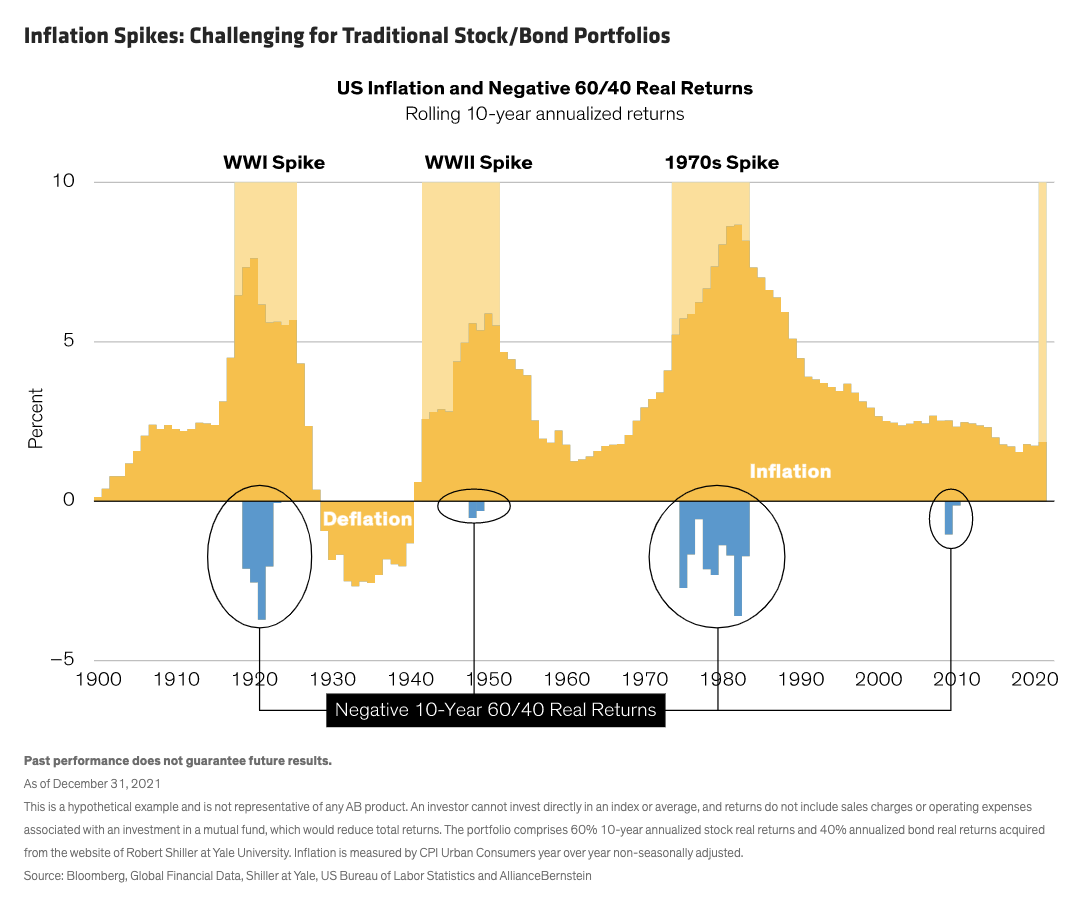

2) Be active, not passive. Active management is far more adept at navigating shifting trends than a passive strategy, which can take a beating. For instance, during past periods of high inflation—such as during World Wars I and II and in the 1970s—a classic 60/40 strategy failed, delivering negative real returns over rolling 10-year periods (Display).

More recently, government bonds failed to provide the anchor to windward against stock volatility that investors expect, with correlations between US Treasuries and equities—typically negative—foraying into low positive territory. While we expect negative correlations to prevail over time, stocks and government bonds may continue to flirt with positive correlations until we achieve some clarity around inflation and central banks return to normal footing. Only active investors can respond nimbly to such fluctuations.

3) Take advantage of the interplay. Forward-looking measures such as long-dated breakeven rates show that markets remain confident that central banks will eventually prevail in their battle to return to target inflation levels. However, the path will likely be a volatile one. And in their efforts to tame inflation, central banks can deploy not just policy rates but balance-sheet normalization. That means that the interplay between yields, volatility and the shape of the yield curve could create investment opportunities in rate markets and among securitized assets.

4) Consider higher-yielding bonds. Most US Treasury real yields (nominal yield minus expected inflation) have turned positive, and credit spreads are now at or above average. Today’s higher yields and wider spreads are beginning to attract investors. And no wonder: that extra yield can compensate for both elevated inflation and uncertainty. In this environment, “carry”—essentially, clipping the bond’s coupon—rules the day.

5) Broaden your horizon. Inflation may be higher globally, but it varies by region and country. For example, North America, Europe and Australia have seen much bigger surges in inflation than have China and Japan. And inflation hit emerging markets such as Brazil, Mexico and the Central and Eastern European countries especially hard, compelling their central banks to take aggressive policy action to bring inflation back in line with targets and in advance of their G10 counterparts.

Global bond investors can take advantage of this range of opportunities—the broadest it’s been for two decades—to enhance return potential through country and currency selection.

Adaptation Is Key in Higher Inflation Regime

Subduing inflation takes time, and the path may be rocky. But those who adopt a flexible mindset will have the upper hand. By staying nimble, bond investors can survive—and thrive—in the new landscape.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein