Are We Headed for Recession? Gold and Bitcoin Could Offer Some Cover

Membership required

Membership is now required to use this feature. To learn more:

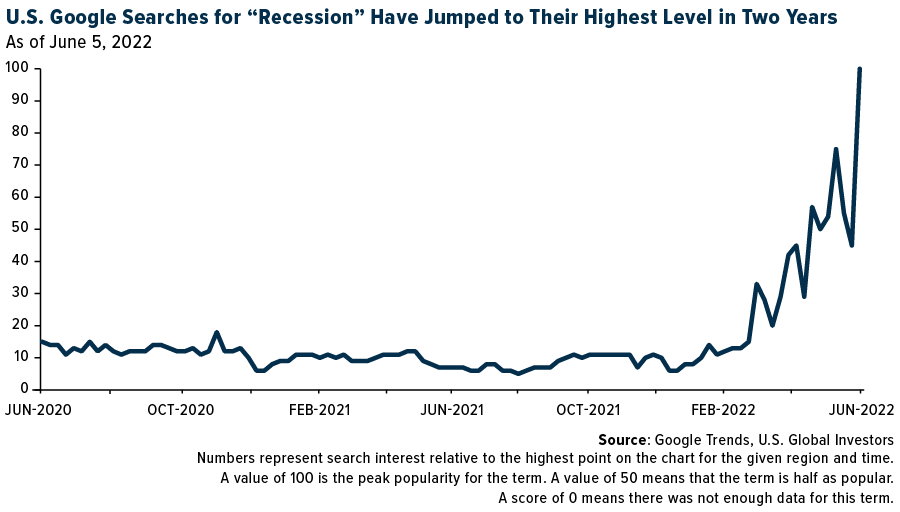

View Membership BenefitsThere’s no way of knowing for certain whether a recession is imminent, but for many Americans, it’s sure starting to feel that way. According to Google, more people in the U.S. searched for the term “recession” than at any other time in the past two years.

This was the case even before Thursday’s consumer price index (CPI) report showing that inflation rose at a scorching annual rate of 8.6% in May, the highest reading since 1981. If we’re measuring inflation using the 1980s methodology, though, the figure is closer to 17%.

Slowdown Driven by Commodity Price Shock

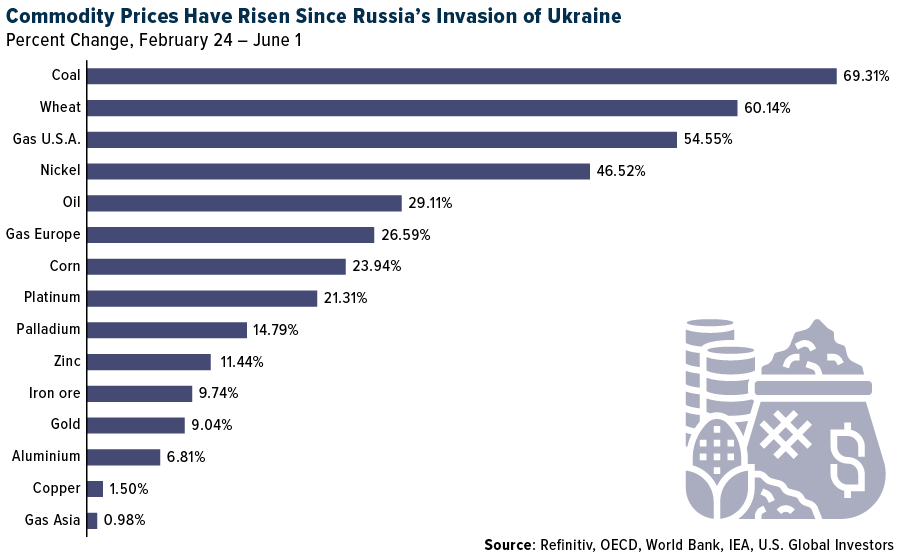

The CPI report followed dreary economic projections by the World Bank and Organization for Economic Co-operation and Development (OECD), both of which see growth being kneecapped by the conflict in Ukraine, which in turn has caused the price of nearly every global commodity, from coal to wheat to oil, to skyrocket. Russia and Ukraine together account for about 30% of the total world wheat exports, according to the OECD, suggesting the price of food may remain elevated for a longer period of time.

In its flagship June report, the World Bank significantly slashed its earlier global economic growth projection of 4.1% in 2022 to 2.9%. “For many countries, recession will be hard to avoid,” says World Bank president David Malpass. Other countries could be looking at 1970s-style stagflation, the toxic result of highly elevated inflation and unemployment.

The OECD’s forecast,, while not so dire, nevertheless sees growth subdued on account of supply chain disruptions caused by the conflict in Ukraine.

Gold More Defensive, Bitcoin More Aggressive

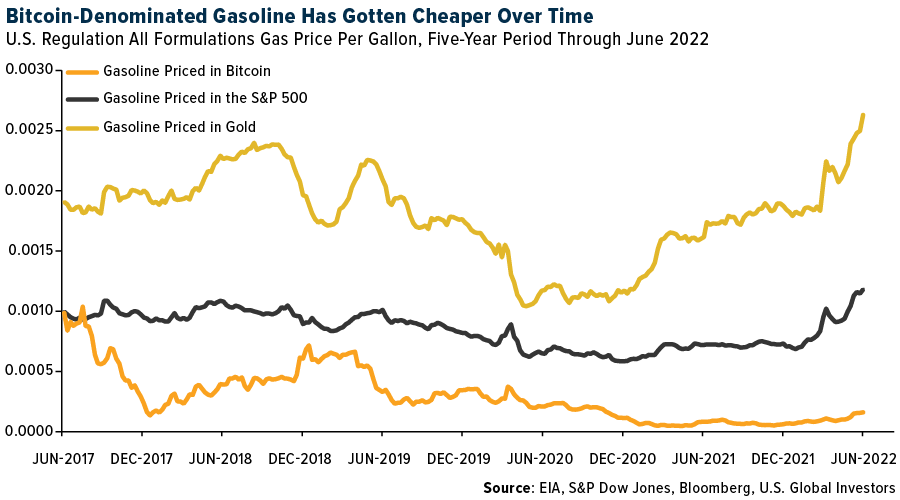

If we are indeed headed for a slowdown, and if it’s triggered primarily by a commodity price shock, it might make sense to price a key commodity—gasoline—in gold, Bitcoin and S&P 500 stocks to see which one has been the best at offering protection from rising prices over time.

I got this idea, in fact, from the St. Louis Fed, which posted a surprising blog this week in which it compared the price of a dozen eggs priced in the U.S. dollar versus eggs priced in Bitcoin. The reason for doing this was to show that, although Bitcoin may buy you more eggs in the long run than the dollar, its value is much more volatile. (The blog post fails to mention, however, that the U.S. dollar has lost nearly all of its purchasing power since the Fed was created a little over 100 years ago.)

The average cost of gasoline in the U.S. is now above $5 a gallon for the first time ever. But what if it were priced in gold, Bitcoin and the S&P 500? Below you can see the results.

Among the three, Bitcoin-denominated gasoline is the only one that has gotten cheaper over the past five years. S&P 500-denominated gas and gold-denominated gas have both gotten slightly more expensive over the past five years.

This may appear to show that Bitcoin is better than stocks and gold at providing cover from the effects of higher commodity prices. But there’s a few considerations to make before moving everything into the digital asset.

The biggest consideration is that stocks and, to a much greater extent, gold have been around a lot longer than Bitcoin. They have a track record of how they performed in times of high inflation, high interest rates, and everything in between.

Bitcoin, by comparison, has only been around for 13 years. If it were a person, it would just now be starting puberty. Since being created, rates haven’t been above 2.5%. We simply don’t know how its price action will perform in a high-interest rate environment.

That’s why I often say that gold is ideal for investors who seek a tried-and-true defensive position, while Bitcoin is ideal for someone who wants a more aggressive asset.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 4.58%. The S&P 500 Stock Index fell 5.05%, while the Nasdaq Composite fell 5.60%. The Russell 2000 small capitalization index lost 4.40% this week.

- The Hang Seng Composite gained 2.65% this week; while Taiwan was down 9.65% and the KOSPI fell 12.82%.

- The 10-year Treasury bond yield rose 22 basis points to 3.16%.

Airline Sector

Strengths

- The best performing airline stock for the week was Spirit, up 7.4%. Domestic booked traffic ended May at down 12%, as bookings slowly return to 2019 levels. Booked revenue finished just a touch below 2019 levels at -1% as yields finished the month at up 12%.

- China’s domestic air traffic recovery remained tepid at 28% of 2019 levels in the second half of May, slightly up from 23% in the first half of May. Shanghai and Beijing underperformed with domestic traffic only at 0-10% of 2019 levels in May, while Guangzhou and Hainan witnessed more of a recovery at 36-42% of 2019 levels. Domestic airline yields rose sharply to 120% of 2019 levels in May, given higher fuel surcharges, driving mild improvement in unit revenues to 86% of normal in the second half of May.

- The Evercore ISI Airlines Survey moved up from 65.0 to 66.3 in its latest release. The Index has steadily climbed, rising in 16 of the past 20 weeks, and is currently at its highest level since July 2012. As restrictions ease and consumers have become more comfortable with booking international travel, the international portion of the Index increased from 52.5 to 55.0.

Weaknesses

- The worst performing airline stock for the week was WIZZ Air, down -20.0%. Goldman revised down its China domestic air passenger traffic forecasts for 2022, now assuming recovery to 57% of 2019 levels for the full year (versus 72% previously). The revised outlook comes after factoring in the Omicron impact during the past two months and the stricter travel restriction policies across China.

- On Tuesday, ISS urged Spirit Airlines shareholders to vote “no” on the proposed Frontier/Spirit merger, noting “shareholders may question the board’s failure to negotiate a reverse termination fee with Frontier.” Frontier modified the agreement to include a $250 million breakup fee if regulatory approval could not be obtained. Subsequently, Glass Lewis recommended a Spirit shareholder vote in favor of Frontier. As of June 8, Spirit announced it is postponing its shareholder meeting, previously scheduled for Friday, until June 30.

- Bank of America looks at airline data on a trailing two-week basis, which shows system net sales were down 3.6% versus 2019 for the two weeks ending May 29, versus down 2.8% for the week ending May 15 (two weeks ago before holiday timing issues). In all channels, volumes on a trailing two-week basis are below the pre-holiday levels, but pricing is higher than it was pre-holiday.

Opportunities

- American Airlines published its Investor Update this week noting a materially improved revenue outlook, which is offsetting higher fuel costs, slightly lower capacity, and higher unit costs to drive an improved pre-tax margin outlook (now 4% to 6% versus 3% to 5% previously). RASM (revenue per available seat mile) is now expected to be up an impressive 20% to 22% versus up 14% to 16% previously.

- Alaska Airlines now expects second quarter revenue to be up 12-14% versus 2019) on capacity down 7-9%. CASM-ex fuel is unchanged, up 16-19% but fuel cost per gallon was raised to $3.65-3.68 from $3.25-3.30. The new guide implies an operating margin of 13%.

- Morgan Stanley believes Chinese airline share prices will rise in absolute terms over the next 15 days, as the group expects air travel demand in the Asian nation to recover following Shanghai’s reopening and with the recent pandemic resurgence in many cities coming under control. This should trigger positive market sentiment on air travel-related stocks.

Threats

- According to JPMorgan, The Sunday Times reported that London Heathrow has ordered airlines to cut passenger numbers by around a third until July 3. British Air previously announced capacity cutbacks of 10% between April and October. Recently a heightened number of flights are being cancelled at short notice for a variety of reasons (airline staffing shortages, airport bottlenecks, IT system failures, etc.).

- With travel restrictions still in place in Beijing, the domestic recovery looks likely to be slower than previous COVID rebounds despite Shanghai’s reopening. This view is consistent with comments from Chinese airlines and airports. There are downside risks to the second half of 2022 domestic traffic forecast at 70% of 2019 levels.

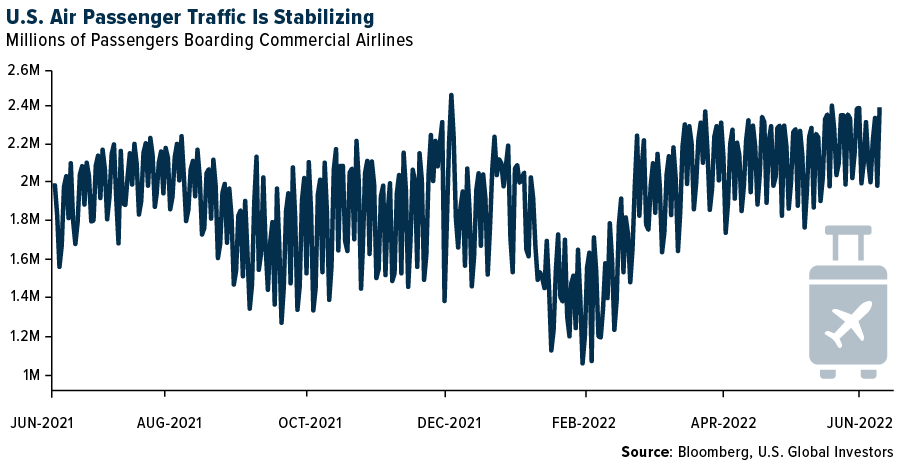

- As of now, the airline industry is not seeing any signs of demand slowdown or price resistance (Delta Air Lines mentioned summer prices could be up 25-30%), but the market is clearly concerned given recent share price underperformance. Peak summer travel seems very strong but there is uncertainty among investors as to how the fall season progresses. Ultimately, U.S. domestic traffic remains positive and has stabilized, as seen in the number of passengers screen by the TSA in the chart below.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 0.86%. The best performing country in Asia this week was Hong Kong, gaining 3.72%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 8.22%. The Vietnamese dong was the best performing currency in Asia this week, gaining 0.08%.

- China´s exports, in dollar terms, surged 16.9% in May, twice the expected increase of 8%. Imports were reported at 4.1% versus the consensus of 2%. The trade surplus now stands at $78.76 billion, up from $51.12 billion in April. January-May exports to Russia rose 7.2% and imports jumped 46.5%.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 5.65%. The worst performing country in Asia this week was South Korea, losing 5.23%.

- The Hungarian forint was the worst performing currency in emerging Europe this week, losing 5.61%. The South Korean won was the worst performing currency in Asia this week, losing 2.28%.

- The European Central Bank (ECB) raised its inflation projections and cut its growth forecast. The ECB now expects the prices to rise by 6.8% in 2022, well above the 5.1% predicted in March. Gross domestic product for the Eurozone in 2022 was revised down to 2.8% from 3.7%.

Opportunities

- According to FactSet, foreign investors are returning to China’s stock and bond market thanks to China’s efforts to stimulate its economy after months of lockdowns. Foreign investors bought a net $2.5 billion worth of beaten-down China-listed shares in May, which was the most significant inflow in the previous four months. Investors are regaining confidence in China. Goldman Sachs said that even with Covid rules, China is the world’s second-biggest equity market, where investors are always looking to invest.

- The National Press and Publication Administration of China, the country which is considered the world´s largest mobile entertainment arena, and as an action on its way to normalization after lockdowns, (and as a reactivation economy measure), approved 60 new games, after 45 approved in April. The two biggest gaming companies (Tencent Holdings Ltd. and NetEase Inc.) are not included in these approvals, so it could mean the approval process is getting smoothed out in order for different players to participate in one of the main industries in China.

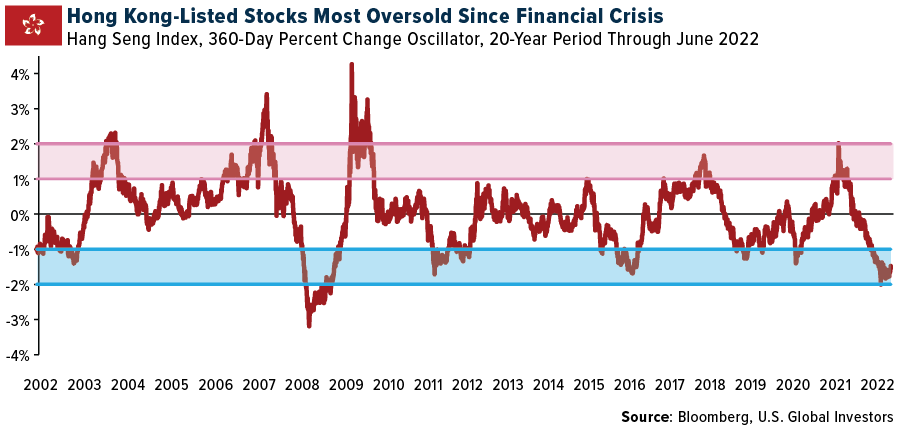

- Chinse equites have been falling for more than a year, since a peak back in February of 2021. Despite recent news emerging that reopening in China may not be as smooth as expected, equites are due for a bounce. Our 20-year oscillator, based on 1-year price change, shows the Hang Seng Index is in oversold territory.

Threats

- The risk of lockdowns in China is back already. After the recent end of lockdowns which lasted two months, this weekend Shanghai will lockdown seven districts once again for massive Covid testing, with residents of the Minhang district undergoing testing first. If any Covid infections are detected, the government will order a two-week lockdown, according to China’s Zero-Covid policy. This could have a significant impact on the worldwide supply chain, and we may see short-term price reversals in equites.

- This week, the ECB announced its plan of a 25-basis points rate hike in July; the rate increases could be higher in September if inflation levels continue increasing. The bank also shared its decision of ending its bond-buying. The decision was taken by the ECB´s 25 governing council members to fight against inflation in the Eurozone, which had risen to 8.1% in May, a record number; the target was 2%.

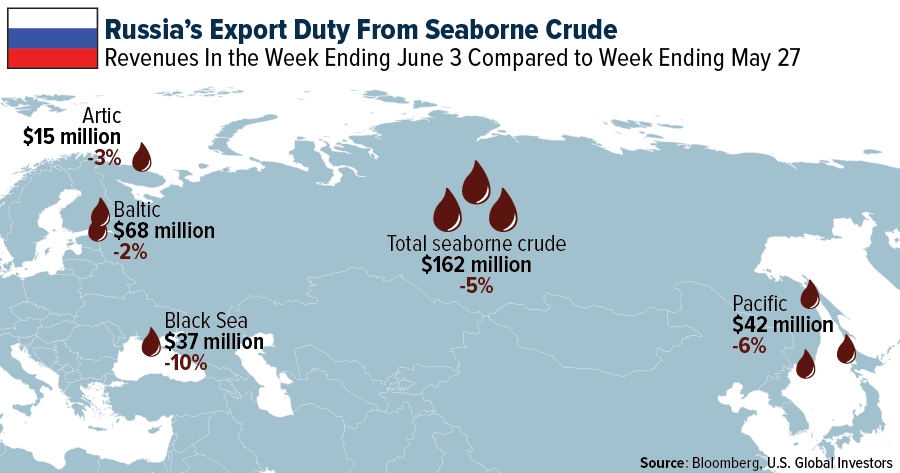

- Based on a Business Insider article, once the Eurozone’s ban on Russian seaborne petroleum starts, Russian oil production could fall around 18% to 9.3 million barrels per day by next year, based on EIA expectations. According to Bloomberg, the total Russian revenue from oil exports fell 5% in May, representing an increase of 15% in the price of Brent crude, reaching $120 a barrel. A decrease in Russia’s oil production could increase the combustible price considerably, increasing the operational cost of different industries. Higher oil prices will be transferred to the final consumer.

Energy & Natural Resources

Strengths

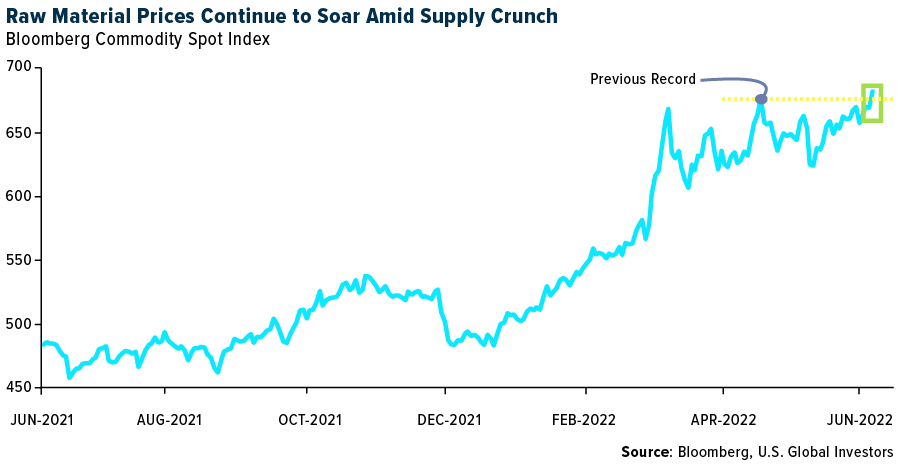

- The best performing commodity for the week was tin, up 5.16%, likely on China reopening after two months of lockdowns. Raw materials have soared since bottoming out in the early days of the pandemic, reports Bloomberg, driven by massive stimulus spending, production cuts and widespread bottlenecks across supply chains. The move, fueling the highest inflation in four decades and prompting central banks to raise interest rates, was exacerbated by Russia’s invasion of Ukraine, the article continues, which further disrupted energy and grain supplies.

- Goldman is updating its supply and demand expectations, now forecasting that Brent prices will need to average $135/bbl in the second half of 2022 through the first half of 2023, for inventories to finally normalize by late 2023. This represents summer retail prices reaching levels normally associated with $160/bbl crude to achieve the additional 0.5 mb/d of price-induced demand destruction required to rebalance the market next year in addition to: 1) global GDP growth excluding China slowing to 2%, 2) record output from Saudi/UAE/Iraq and 3) Iran/Venezuela/Libya production rising 1.3 mb/d.

- U.S. natural gas futures extended gains after hitting the highest level since 2008 as blistering heat in the southern half of the country is poised to boost demand for air conditioning and power plant fuel. Futures for July delivery were up 0.6% to $9.375/MMBtu on Nymex.

Weaknesses

- The worst performing commodity for the week was lumber, down 10.80%. According to Random Lengths (“RL”), the Framing Lumber Composite decreased $95 this week to $699, making for a two-week drop of $202, while in OSB markets, the OSB Composite decreased by $88 this week to $665. The Framing Lumber Composite and OSB Composite are now down 47.6% and 53.5%, respectively, since March 11.

- The Chilean Copper Commission (Cochilco) reported copper production of 420 kt in April, implying a decline of 9% year-over-year and 8% month-over-month. Year-to-date 2022 copper production in Chile currently totals 1.70 Mt, 7% below levels seen in 2021.

- U.S. hot-rolled coil prices dropped $10 per ton as steel service centers and mills negotiated on a lower price. Prices were last seen at the same level on March 9 when prices just turned around following the initial Russian invasion of Ukraine. A Midwest service center source said that lead times were better than advertised.

Opportunities

- Bank of America reported that a majority of its NGL coverage universe reported strong first quarter beats that should only continue into the remainder of the year. While NGL prices are flattish mid-week versus the first quarter, natural gas prices averaged $4.63/Mcf in the first quarter, while quarter-to-date and the forward curve through year-end 2022 are averaging about $9/Mcf, which should provide further earnings improvement through year-end.

- U.S. President Biden is authorizing the use of the Defense Production Act (DPA) to accelerate domestic production of clean energy technologies – unlocking new powers to meet this moment. Specifically, Biden is authorizing the Department of Energy to use the DPA to rapidly expand American manufacturing of five critical clean energy technologies.

- The Biden administration is also pushing lawmakers to support a $4.3 billion plan to buy enriched uranium directly from domestic producers to wean the U.S. off of Russian imports of the nuclear-reactor fuel, according to a person familiar with the matter. Shares of uranium companies surged. Energy Department officials have met with key congressional staff, who say such funding is urgently needed, according to an individual with access to the information.

Threats

- Paul Singer’s Elliott Investment Management is seeking $456 million in damages from the London Metal Exchange, reports Bloomberg. This comes over its decision in March to cancel billions of dollars’ worth of nickel trades after a massive short squeeze. The move by the activist investor ratchets up pressure against the LME, the article continues, which has been widely criticized for its handling of the crisis in nickel. The exchange is also facing a review by U.K. regulators, while the nickel market has been stuck in an extended limbo of low liquidity and volatility.

- India is looking to double down on its Russian oil imports with state-owned refiners eager to take more heavily discounted supplies from Rosneft, as international players turn down dealings with Moscow over its invasion of Ukraine. State processors are collectively working on finalizing and securing new six-month supply contracts for Russian crude to India, said people with knowledge of the companies’ procurement plans.

- Paul Singer’s Elliott Investment Management is seeking $456 million in damages from the London Metal Exchange, reports Bloomberg. This comes over its decision in March to cancel billions of dollars’ worth of nickel trades after a massive short squeeze. The move by the activist investor ratchets up pressure against the LME, the article continues, which has been widely criticized for its handling of the crisis in nickel. The exchange is also facing a review by U.K. regulators, while the nickel market has been stuck in an extended limbo of low liquidity and volatility.

Luxury Goods

Strengths

- Eurozone’s investor confidence has continued to improve. In May, a gauge of investor confidence in the EU was reported at -22.6, the lowest level since June 2020. In June, the gauge came in at -15.8 above the expected -20.0.

- Luxury stores in major Chinese cities have seen a surging number of customers and record sales both online and offline after Shanghai eased its Covid restrictions. Long lines were seen in front of some luxury stores in Plaza 66, a mall in Shanghai, as consumers waited to shop for luxury items.

- Sand China, a developer and owner of resorts/casinos and retail malls, was the best performing equity in the S&P Global Luxury Index this week, gaining 9.10%. Performance of casinos/hotels and malls were positively impacted by China relaxing its Covid restrictions.

Weaknesses

- The European Central Bank (ECB) raised this year’s average inflation projection to 6.8% from 5.1% in March. In addition, the ECB expects GDP growth to reach only 2.8% versus the previously expected growth of 3.7%.

- Initial jobless claims unexpectedly increased in the United States. The weekly data shows that the number of people collecting their first unemployment check increased to 229,000 from 202,000. Bloomberg economists were expecting a small weekly increase in initial jobless claims of 206,000 (versus the actual 229,000).

- Cettire, an online retailer, was the worst performing stock in the S&P Global Luxury Index this week, losing 29.3%. On Friday, the company recorded a 52-week low, losing 86% of its market shares in a year.

Opportunities

- In Europe, investor confidence data improved this week, and could continue to move higher as the market is coming back to normal operations after the pandemic. Travel is expected to rise during the summer months as many countries have eliminated travel restrictions that were imposed previously due to Covid, paving the way for an increase in luxury spending. This week the United States ended the requirement for air travelers to test negative for Covid before entering the country.

- French luxury group, Kering, is aiming to increase sales of its eyeglasses division to about 2 billion euros ($2.1 billion) with earnings before interest and taxes (EBIT) margin of more than 15% in the medium term. In addition, Kering outlined plans to grow Gucci sales to 15 billion euros in the mid-term. The company held a two-day investor presentation this week.

- According to Bloomberg, Ferrari plans to significantly expand its factory in northern Italy as part of its electrification strategy. The company will most likely highlight the project during its June 16 capital market day, when the Chief Executive Officer Benedetto Vigna is expected to provide information on Ferrari’s electric vehicle strategy, laying down business plans for the next four years.

Threats

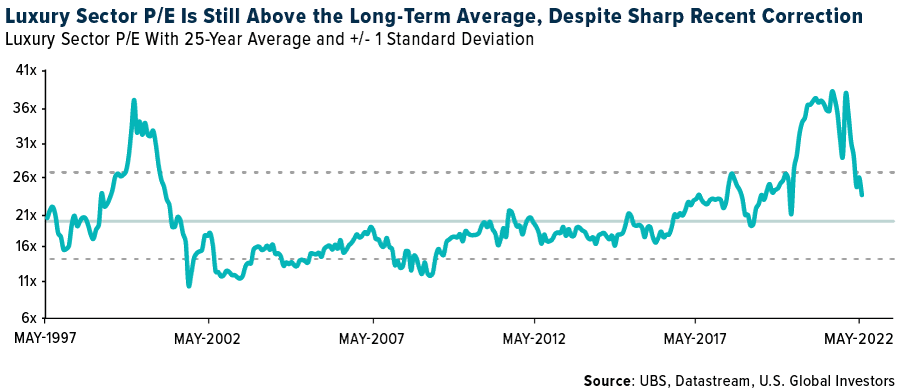

- Despite a year-to-date correction in luxury goods equites, more downward pressure could follow. According to UBS research, the luxury sector is trading on one-year forward earning per share of 23.6, still above its 25-year average of 20.2. Relative to the MSCI Europe Index, the luxury sector is trading on a 66% premium versus the 25-year average of 40%.

- Residents in Singapore are paying the highest amount in decades for the right to own a premium car, official data shows. The cost of the most exclusive certificates of entailment (COE), which residents must obtain before they are allowed to purchase a car, breached six figures in June for the first time in at least 20 years. Singaporeans have been paying high fees for COEs, which were introduced to curb traffic. The price of these certificates can exceed the cost of a typical vehicle, not allowing middle-income residents to own a car.

- Shanghai has locked down some parts of the city again. While it is a “mini” lockdown in the city, China is still a crucial market for the luxury goods industry. Covid worries in the mainland have been impacting the performance of luxury equites, and if China’s reopening process is not smooth it could further hinder luxury goods sales.

Blockchain and Digital Currencies

Strengths

- PayPal will let users transfer certain cryptocurrencies to other customers, exchanges, and external wallets, in a new service that’s part of the company’s effort to boost usage of its app. PayPal also said that the New York Department of Financial Services granted the company a “BitLicense” which governs businesses working with virtual currencies, reports Bloomberg.

- Citigroup plans to hire more than 4,000 tech staff to help move its institutional clients online in the wake of the pandemic. More than 1,000 of the recruits will join the markets technology team as part of an aggressive growth strategy, Jonathan Lofthouse, head of markets and enterprise risk technology, said in an interview, as reported by Bloomberg.

- Ken Griffin’s Citadel Securities is willing to make markets in exchange-traded funds that hold cryptocurrencies, if regulators allow, reports Bloomberg. Griffin has called for the SEC to pivot from just talking about regulating crypto to actually establishing rules.

Weaknesses

- A sweeping bill from a bipartisan Senate duo would buttress rules pertaining to some of the hottest issues facing the crypto industry, including sanctions compliance, stablecoin oversight and energy usage. The legislation introduced Tuesday by Wyoming Republican Cynthia Lummis and New York Democrat Kirsten Gillibrand, is one of the most ambitious attempts to regulate the volatile asset class, writes Bloomberg.

- The speculative darlings of the easy-money era (technology stocks and cryptocurrencies) are acutely vulnerable now that the Federal Reserve is shrinking its nearly $9 trillion balance sheet, writes Bloomberg. At the same time, central bankers from Canada to Europe are about to test the resilience of global markets as they follow hawkish U.S. policy makers on a liquidity-sapping mission to unwind the pandemic bond-buying spree. That’s the broad outlook for Wall Street, the article continues.

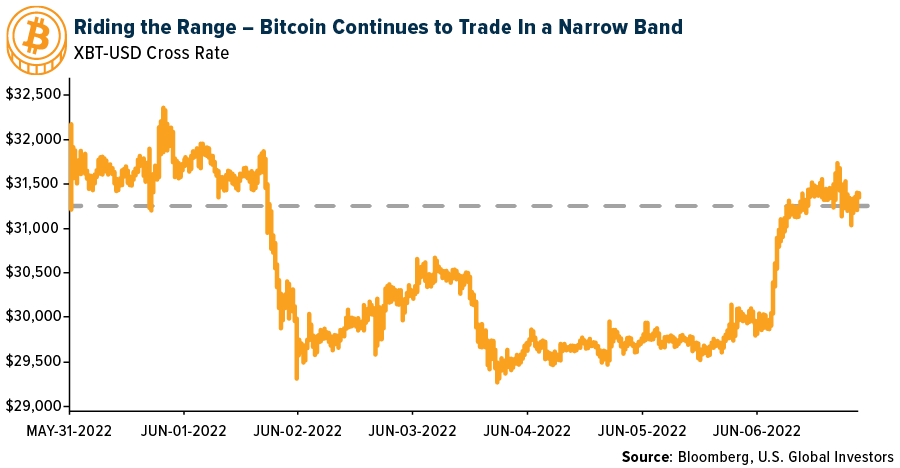

- Bitcoin fell back below $30,000 on Tuesday, dropping 6% to around $29,500 and wiping out the previous three days of gains, ending Bitcoin’s second brief break above $31,000 over the past three weeks, writes Bloomberg. The declines for crypto came as the dollar extended gains and a jump in Treasury yields late Monday fueled concerns that rising borrowing costs could induce a recession.

Opportunities

- Bitcoin has been trading around the $30,000 level for weeks now, defying predictions of a potential further decline but also struggling to gain upward momentum. The crypto market could get a boost from U.S. CPI data later this week. If inflation is indeed coming down, there’s a good chance the Federal Reserve will ease up on the market conditions, writes Bloomberg.

- Binance.US, the American arm of the world’s largest cryptocurrency exchange, has launched a blockchain staking product promising high yields on staked crypto, with the aim of out-flanking similar offerings from rival U.S.-based exchanges. The staking service where users lock-in assets to support proof-of-stake networks, enables users to earn up to 18% annual percentage yield on certain tokens, the company announced Tuesday.

- The regulatory cloud looming over cryptocurrency and other digital assets is good for business at law firm Winston & Strawn. Surging interest in digital assets and growing scrutiny from a wide range of regulators are fueling demand for legal work, particularly during a volatile stretch. Winston is among several Big Law firms increasingly focusing on the practice area, according to Bloomberg.

Threats

- OpenSea, one of the highest-profile crypto start-ups, is facing a backlash over stolen and plagiarized nonfungible tokens. Chris Chapman used to own one of the most valuable commodities in the crypto world: a unique digital image of a spiky-haired ape dressed in a spacesuit, which he listed on OpenSea to sell for $1 million. Two months later, Chapman got a notification form OpenSea that the ape had been sold for roughly $300,000. A crypto scammer exploited a flaw in OpenSea’s system to buy the ape for significantly less than its worth, explains Bloomberg. Mr. Chapman is one of many crypto enthusiasts who have raised questions about OpenSea.

- Binance coin (BNB) price dropped by nearly 7.3% on June 7, to below $275, its lowest level in three weeks. The coin could drop another 25%-40% in 2022 as its parent firm, Binance, faces allegations of breaking securities rules and laundering billions of dollars in illicit funds for criminals, according to Bloomberg. The SEC is investigating whether the ICO of BNB tokens in 2017 was sales of securities that should have been registered with them. This could put downward pressure on BNB’s price, which has already lost more than half of its value after peaking in May 2021 at around $700.

- Crypto exchange Gemini Trust Co. lacked proper safeguards, resulting in retirement-account holders losing around $36 million in Bitcoin and Ether when the master key got hacked, IRA Financial Trust said in a lawsuit. Gemini made false representations about two-factor authentication and other protections that were supposed to safeguard customer accounts, according to a complaint that IRA filed Monday in the U.S. District Court for the Southern District of New York, writes Bloomberg.

Gold Market

This week gold futures closed at $1,876.30, up $26.10 per ounce, or 1.41%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.75%. The S&P/TSX Venture Index came in off 2.14%. The U.S. Trade-Weighted Dollar jumped 2.00%.

| Jun-9 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jun-9 | Initial Jobless Claims | 206k | 229k | 202k |

| Jun-10 | CPI YoY | 8.3% | 8.6% | 8.3% |

| Jun-14 | Germany CPI YoY | 7.9% | — | 7.9% |

| Jun-14 | Germany ZEW Survey Expectations | -26.8 | — | -34.3 |

| Jun-14 | Germany ZEW Survey Current Situation | -31.5 | — | -36.5 |

| Jun-14 | PPI Final Demand YoY | 10.8% | — | 11.0% |

| Jun-14 | China Retail Sales YoY | -7.1% | — | -11.1% |

| Jun-15 | FOMC Rate Decision (Upper Bound) | 1.50% | — | 1.50% |

| Jun-16 | Housing Starts | 1709k | — | 1724k |

| Jun-16 | Initial Jobless Claims | 215k | — | 229k |

| Jun-17 | Eurozone CPI Core YoY | 3.8% | — | 3.8% |

Strengths

- The best performing precious metal for the week was gold, up 1.41% after the market digested the Friday CPI print of 8.3%. India’s gold imports for May jumped 677% in one year, the highest surge seen on a yearly basis. The rise in imports comes on the back of a correction in prices just before Akshaya Tritiya, a key festival for Hindus and Jains celebrated in the first week of the month. Wedding season also boosted sales of retail jewelry.

- Vox Royalty Corp. announces that it has executed a binding royalty sale and purchase agreement with an individual prospector residing in Canada. The agreement would be to acquire the rights to three Canadian gold royalties for total consideration of up to C$1,800,000. “We are very excited to add these rapidly advancing Canadian gold royalties to the Vox portfolio, which offer significant near-term exploration and development catalysts for shareholders,” said Vox CIO Spencer Cole.

- Data from the U.S. Mint shows that sales of American Eagle and Buffalo gold coins totaled $365 million (or 199,000 ounces) in May, reports the World Gold Council. Sales rebounded from the April 2022 lows to slightly higher than the year-to-date average. Sales are on pace to have the strongest year in terms of U.S. coin sales since 1999, the report continues.

Weaknesses

- The worst performing precious metal for the week was platinum, down 4.32%. Gold ETF net outflows totaled 53 tons in May, reports the World Gold Council, with year-to-date inflows of 262 tons. All regions experienced outflows during the month with North American funds leading the way, with 34 tons of outflows, followed by European funds, the report continues. Weaker momentum and positioning are noted as driving these outflows.

- Victoria Gold Corp. last week had the biggest increase in short interest relative to tradable shares among Canadian companies, according to data from financial analytics firm S3 Partners. U.S. diesel prices continued to climb this week with a substantial pick up in European demand being supplied by U.S. domestic production. This is driving up fuel costs and hitting the earnings of companies that rely on trucking and mining.

- Gold has edged up since mid-May on more troubling signs in the global economy, reports Bloomberg, although an uptick in the dollar and bond yields has weighed on prices. Still, bullion held Tuesday’s gains, with warning signs of slowing world economic growth amid a surge in inflation bolstering its appeal as a haven asset. Gold was largely capped for the week, as markets awaited the CPI print that came in higher than expected. This prompted some economists to call for a 75-basis points hike at the next Fed meeting. Gold sold off initially but closed the week with a gain.

Opportunities

- Rio Tinto, a leading global mining company, make a $10 million strategic equity investment in Nano One, a clean technology innovator in battery materials. This agreement falls on the hills of Nano One acquiring the LFP battery production facilities of Johnson Matthey in Quebec along with their team. In addition, BASF recently partnered with Nano One on developing their process with reduced byproducts. What the purchase of the Quebec facilities will do is allow Nano One to produce its patented cathodes on scale in the thousands of tons versus its Vancouver facility, which can now be devoted to testing new battery chemistries and the integrity of the crystals produced.

- Weddings continue to be great for diamond sales. In fact, sales rose more than 60% in 2021, according to Bain & Co., while production increased by just 5%. This shows that diamonds have been getting more expensive, with global prices up 21%. Supply from diamond mines declined every year from 2017 to 2020, with the total sliding from 152 million carats to 111 million. Bain & Co’s research says production will likely grow by just 1% to 2% annually over the next five years. De Beers recently raised its prices for small stones as Russian supplies have disappeared.

- According to Stifel, Chris Jordaan joined Superior Gold (SGI) as CEO in May 2021 and has led the company through a turnaround. The operations side of the business has delivered, with seven consecutive quarters of increasing gold production. Management has also delivered a new reserve and resource statement with a 66% jump in reserves. Stifel maintains a positive view of the long-term potential of the SGI portfolio during this time.

Threats

- According to RBC, the bear case for Gold Fields is as follows: 1) it is tough for existing and new investors to own the GFI ADR trading in the U.S. and/or the South African listing, creating further forced selling pressure from Yámana shareholders pre/post-deal close, 2) South African headquarters makes it a tough sell to some investors, with potentially less management access, 3) perhaps skeletons in either miners’ portfolios, which is a headwind on both the pro-forma story and standalone GFI story, and 4) the multiple re-ratings due to size may take some time to be realized. That’s the bear case clearly stated. The market will vote with its dollar.

- Barrick Gold said on Tuesday it has sold its entire 8.5% stake in Perpetua Resources Corp. for gross cash proceeds of $21.73 million. Perpetua, which fell 8.5% in Canada trading on Monday, also said the Stibnite Gold Project in the U.S. is progressing into the later stages of the permitting process.

- U.S. inflation hit a 40-year high in May, signaling to some that the Fed needs to get even more aggressive on interest rate hikes. The 10-year TIP yield climbed to 0.37 basis points after the 8.3% CPI print. There is a long gap between real rates and inflation and the Fed will have to avoid any policy mistakes as it attempts to tap down prices. Investors can potentially help balance the volatility of their overall portfolio with a 10% allocation to precious metals and mining companies.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All