In the light of multiple discussions raised in AP community about strategies that help investors through market downturns, we would like to share a perspective on advantages of an active asset management approach or so-called actively traded hedge-fund strategy based on the example of a classic long-short US equity strategy.

The stock market indices are currently down 25-40%, and many investors are panicking trying to get rid of value-shedding portfolio assets. Is there anything investors can do to protect their funds and spare themselves an unnecessary nerve-wracking experience? The answer is yes, actively traded long-short hedging approaches can generate sustainable positive returns over the entire short-term to a mid-term lifetime of an investment portfolio.

What sets a robust, efficient, actively traded global investment portfolio strategy apart from other portfolio management strategies is the ability to generate a stable return on the managed assets in times of market turmoil and decline while bringing down the associated risks to a minimum.

Consider the following: when markets are bullish it is not difficult to get a good return and paying steep management fees to a fund manager may seem like a waste of money. However, the bullish bonanza eventually passes, and markets go into decline, which typically happens every 2-3 years, and sometimes even more often. And when the plunging bear market sets in investors face a risk of losing all their earnings gained over the years.

Conversely, an actively traded long-short approach would earn smaller returns than S&P and other major indexes’ returns in a rallying bullish market, but it would also protect investors’ earnings from a potential partial or a complete wipeout when the markets hit the slump keeping the funds’ drawdown losses to a minimum.

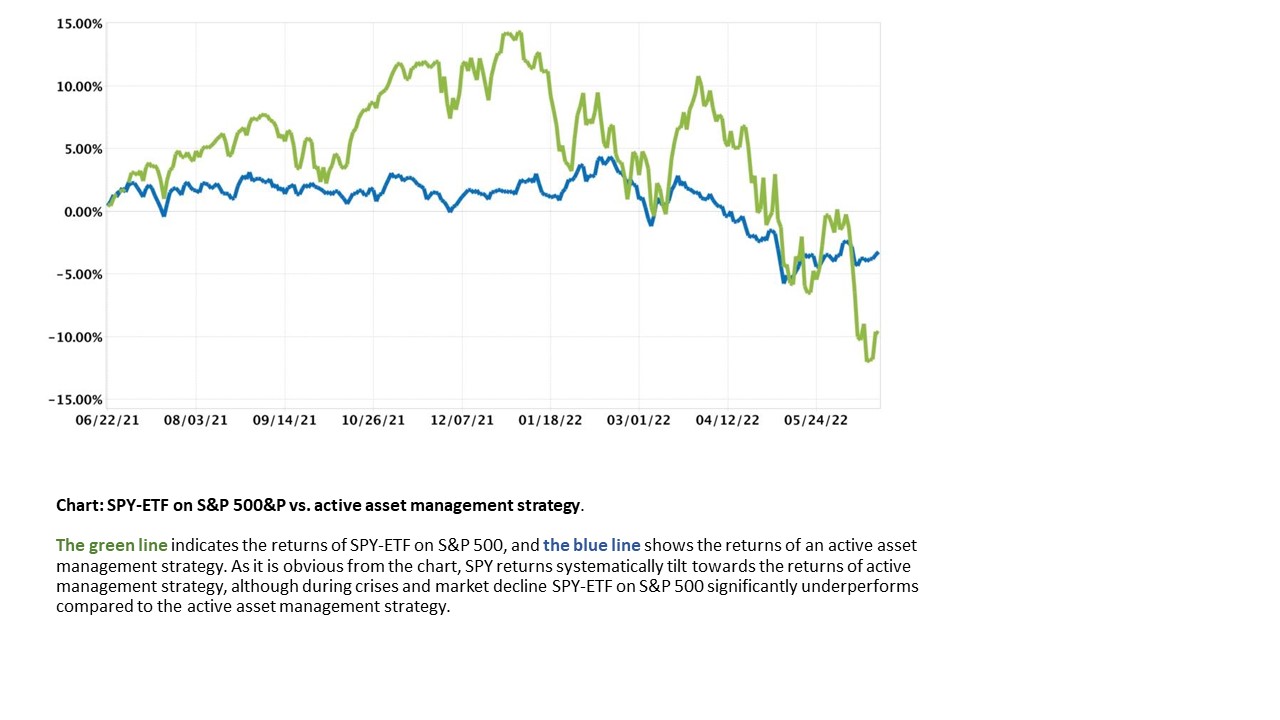

What you can see in the chart below is that in certain periods the returns of the S&P or the Nasdaq outperformed the returns of active asset management strategy. But in the end, the average annual returns of American stock indexes and the returns generated by our long-short strategy worked out the same.

Moreover, since January 03, 2022, the indices fell by 25-40%, however, the maximum drawdown of a long-short equity strategy used by a hedge fund over this time till May 2022 has been only about -5%. And while the markets have kept declining in June, as of the beginning of the month the active equity management strategy has boosted the managed funds ‘returns in the positive zone.

In addition, the results of actively traded long-short strategies challenge a popular and widely debated argument that paying commissions to hedge funds or asset managers to manage investors’ funds is futile and senseless because passive investment strategy would generate the same returns anyway.

Let us take a closer look at this statement with an example: some investors entered on the long-short strategy on January 1, 2022, and others invested in a passive fund, such as an ETF on an index fund. At the current moment of a market decline investors urgently need money.

In a current market decline investors in passive funds could exit the market incurring a loss of -20% or more, whereas in the best-case scenario if the market starts recovering their losses would just be less than -20%. On the contrary, investors in long-short strategies would be able to exit their positions with some positive return. Thus, throughout June, a long-short hedge fund strategy has already posted a +0,5% return as opposed to strong negative performance of the main stock indexes.

To wrap it up, I would like to summarize the purpose of actively traded long-short strategies and the very meaning of active management that makes fund managers’ fees a worthwhile expense for investors. In most cases, long-short strategies do not target beating the market year after year over the long term. They do not earn more than the market can offer over a mid to long term, but in the event of global market decline, these strategies do level out most of the losses.

As we have observed, while the crisis unravels and stock market indices hit the trough, the investors embarking on long-short strategies receive better returns, than passive investors or investors with zero-hedging. The applied skill of the fund manager is somewhat blinded when the markets rally in a bullish frenzy. It is the bear market crisis that puts a fund manager’s skill to a real test, and when the hedging strategy shows positive returns amidst pervasive negative growth in the markets, the question of why we pay the manager a commission receives the most definitive and eloquent answer. It is the premium paid for a fund manager’s skill to lead investors’ funds to a positive return through declining markets.

© Sigma Global Management

Read more commentaries by Sigma Global Management