We believe index funds have immensely contributed to investors by permitting them to capture beta inexpensively. Yet, even ardent index fund supporters concede that the rapid growth of index funds raises some concerns.

As we demonstrate below, investing in US Large Caps using only an S&P 500 index fund mandates ownership of stocks that are so expensive, the historical evidence indicates they may cost investors money. Empirical evidence suggests prudent long-term investors will be well served to own portfolios that exclude expensive stocks like these.

The Price to Sales ratio

The Price to Sales ratio (P/S ratio) is defined as a formula “that compares a company’s stock price to its revenues. It is an indicator of the value that financial markets have placed on each dollar of a company’s sales or revenues.”

The formula used to calculate the P/S ratio is:

While the P/S ratio has limitations, when it gets beyond 10x price to sales, the empirical evidence for avoiding these stocks becomes secondary to simple common sense.

An important observation

In April 2002, Scott McNealy, the founder and CEO of Sun Microsystems, addressed a group of investors. His talk took place almost one year after the burst of the dot.com bubble, costing investors trillions of dollars.

Investors who bought Sun Microsystems when the P/S ratio of the company was at 10x lost 95% of their investment. McNealy wasn’t surprised by this outcome:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero costs of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realise how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

We bring up the dangers of owning stocks at 10x P/S because owners of S&P 500 Index Funds have record levels of exposure to these stocks.

Current valuations

In our recent piece Tesla Price to Sales Ratio & The Coming Tax on Index Funds, we noted the top 10 stocks in the S&P 500 represent 29.7% of the index. Nearly a third of every dollar you invest in that index goes into just ten stocks. The value-weighted average price to sales ratio is 7.3x sales.

Tesla’s P/S ratio is the number one contributor to this concerning valuation metric. Its P/S ratio was an alarming 14.5x, with a 2.44% weight in the index.

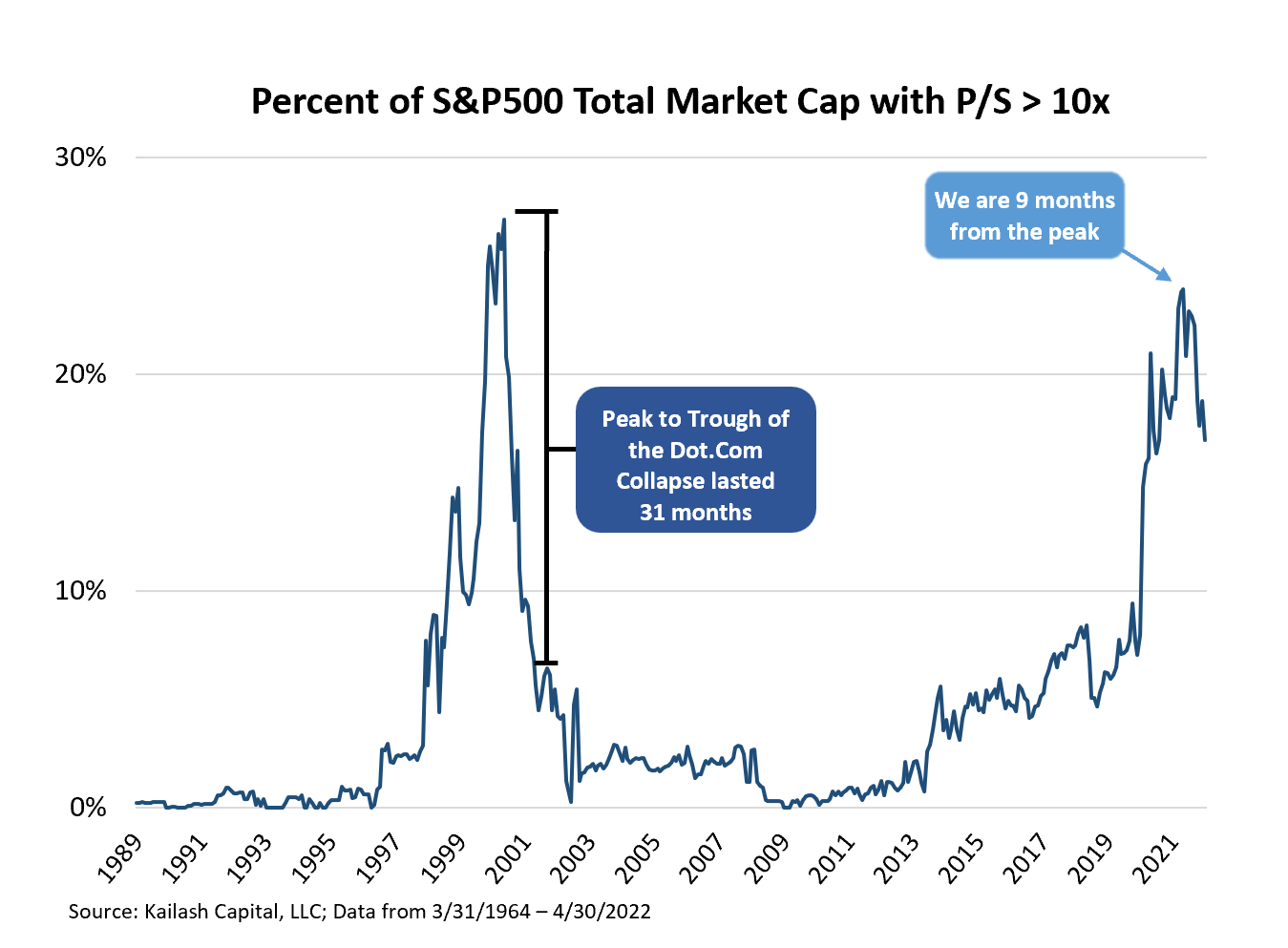

We were at the highest level of P/S ratios since the dot.com collapse, as indicated by this chart, with almost 20% of the stocks in the index with a P/S ratio of over 10x.

In our view, there’s little precedent for those stocks in the S&P 500 index with a P/S ratio of 10x or more to generate durable returns. Investors should not be burdened with them in their portfolios.

Troubling history

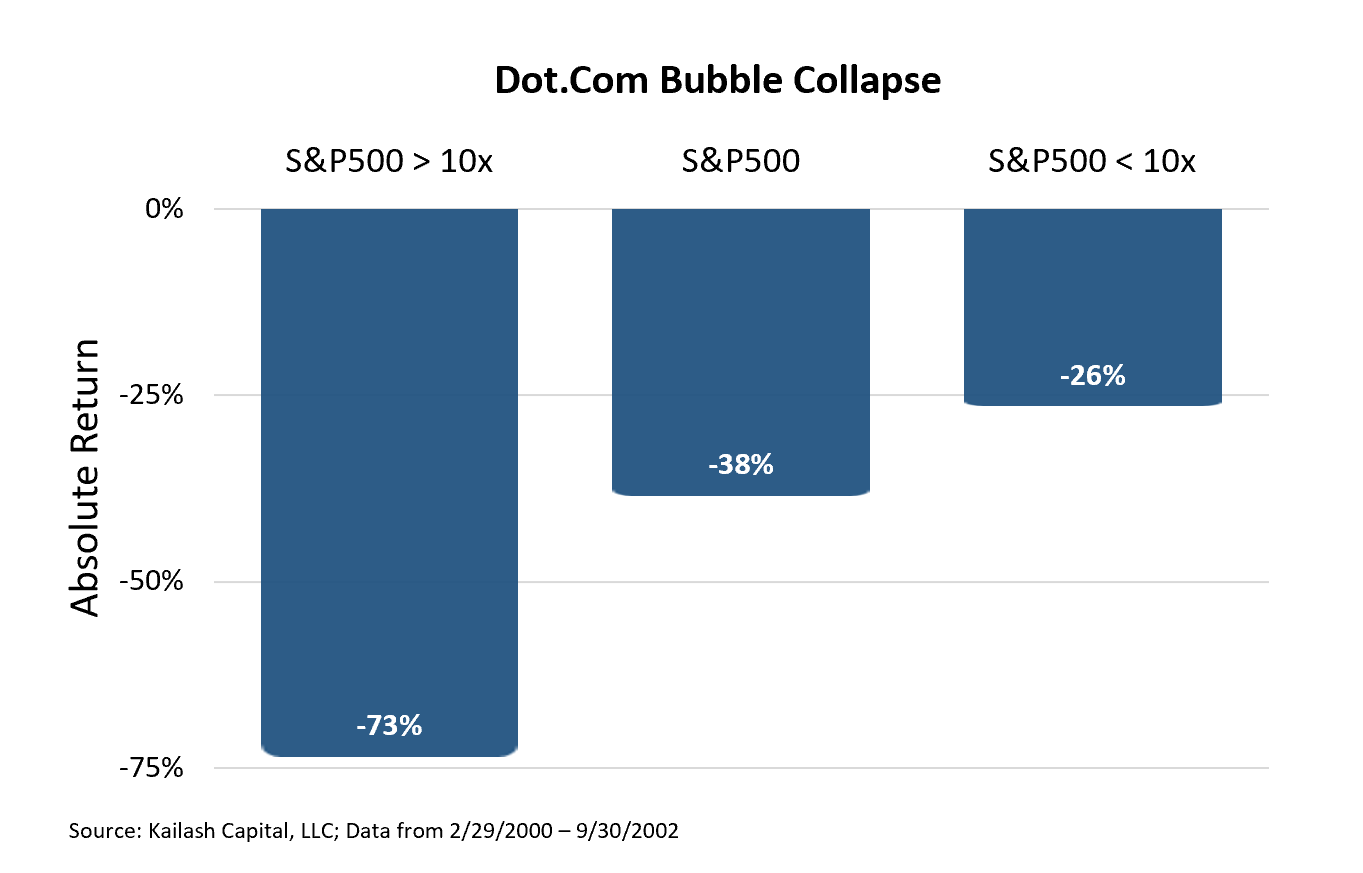

The dot.com collapse provides insight into the fate of stocks in the S&P 500 index with a P/S ratio of over 10x. As indicated in the chart below, for the period from February 29, 2000-September 30, 2002, those stocks lost 73% of their value. Stocks in the same index with a P/S ratio under 10x lost only 26% of their value.

Our approach

Over the long-term, investors have been well served to avoid chasing glamour stocks like Tesla where the fundamentals simply do not justify the price. For a wonderful explanation of this, we encourage people to read Bloomberg writer Gary Smith’s terrific piece “Tesla May Be Driving Itself Out of the Running.” In that piece, Mr. Smith, who owns two Teslas, explains how the stock looks like the much-vaunted British bicycle stocks in the 1800s. The piece is as clear as it is entertaining and informative.

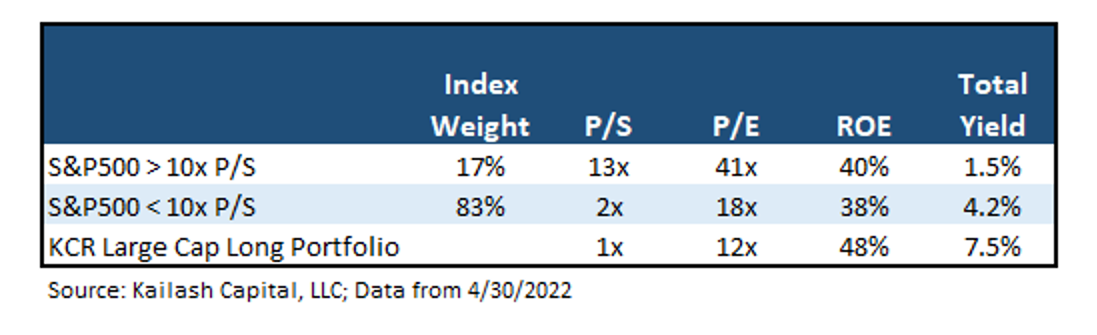

The first two rows in the table below break the S&P 500 Index into two model portfolios. The first row creates a portfolio of only the stocks valued at over 10x price to sales. The second row creates a portfolio using all the stocks in the S&P 500 valued below 10x price to sales. Comparing the first and second rows, you can see that just omitting the Index Funds’ most expensive stocks (row two) gives you a portfolio that is less expensive and has a much higher Total Yield.

The decision to build a portfolio excluding the most expensive stocks in the S&P 500 allows you to pay less and get more.

The third row in the exhibit is our Large Cap Strategy’s fundamentals. You can see that investors in our strategy own even less expensive stocks (P/S and P/E), with higher returns on equity (ROE) and higher Total Yield. Our strategy gives prudent safety-oriented investors an opportunity to pay less for higher-quality companies that offer attractive yields for investors.

The time-tested academic research underpinning our process indicates that our investors will be well-served buying high-quality companies at reasonable to low valuations.

Index funds should remain an important component of a well-diversified portfolio. But blindly accepting the risks of owning all stocks in a particular index, regardless of valuations and profitability, while ignoring the powerful historical evidence strikes us as unreasonable. We see no basis for recommending that 20% of invested funds be allocated to stocks with a P/S ratio of 10x or more, given the dismal track record of stocks at those valuations.

For the patient investor looking for a margin of safety, working with a low-cost, tax efficient, and highly disciplined active manager may be equally, if not more important, than any time in history.

Dr. Sanjeev Bhojraj is a portfolio manager and co-founder of L2 Asset Management. He is widely published in journals in finance and accounting and specializes in behavioral finance. Dr. Bhojraj is a Chaired Professor in Asset Management and the co-director of the Parker Center for Investment Research at Cornell University’s Business School. He has a Ph.D, ACA, ACMA and B.Com.

Matt Malgari is a portfolio manager, the Managing Member and co-founder of L2 Asset Management. Matt spent 14 years at Fidelity Investments as an Assistant Portfolio Manager on its $70 billion Diversified International Fund, sector analyst, diversified analyst and trader. In 2010, Matt became the Managing director of Equity Research for Knight Capital Group. He received is MBA from Cornell University and a BA from Middlebury College.

© Kailash Concepts Research

Read more commentaries by Kailash Concepts Research