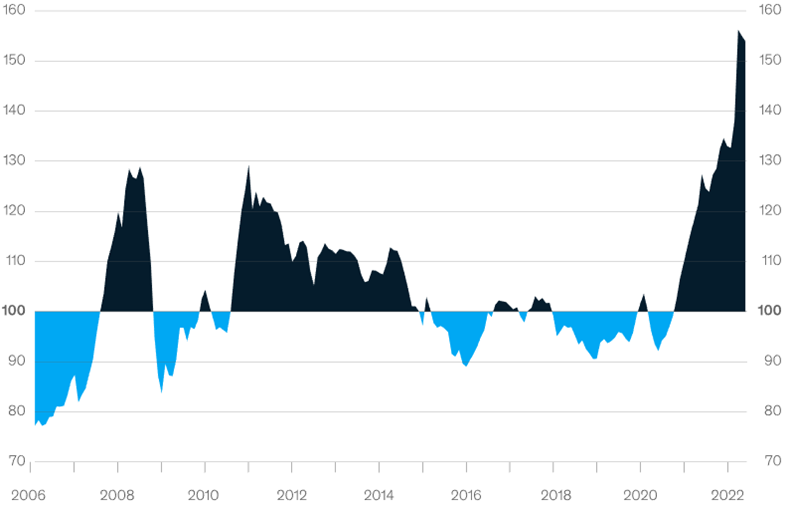

Sri Lanka is in turmoil. The mob have stormed the residence of the country’s president, who has subsequently agreed to step down. The catalyst was sharply rising food prices, a phenomenon we see pretty much everywhere (Exhibit 1). Therefore, one is entitled to ask the question – is Sri Lanka ‘just’ the canary in the coal mine, telling us what to expect in many other countries in the months to come?

The simple answer to that question is “no”, although things are not that simple. I will explain later why the case of Sri Lanka is not an isolated incident, but let me start with Sri Lanka. Rising food prices have indeed acted as a catalyst, but they are not the root cause. Years of fiscal mismanagement and corruption, endless borrowings (mostly from China), large fiscal deficits and a tendency to fund those deficits by printing money are the true underlying causes of the current mayhem. The fact that the tax rate has been lowered (rather indiscriminately, I may add) has only made an already difficult situation worse.

Exhibit 1: Real Global Food Price Index , 2014-16 average = 100 Source: McKinsey & Company

Why we shouldn’t ignore what is happening in Sri Lanka

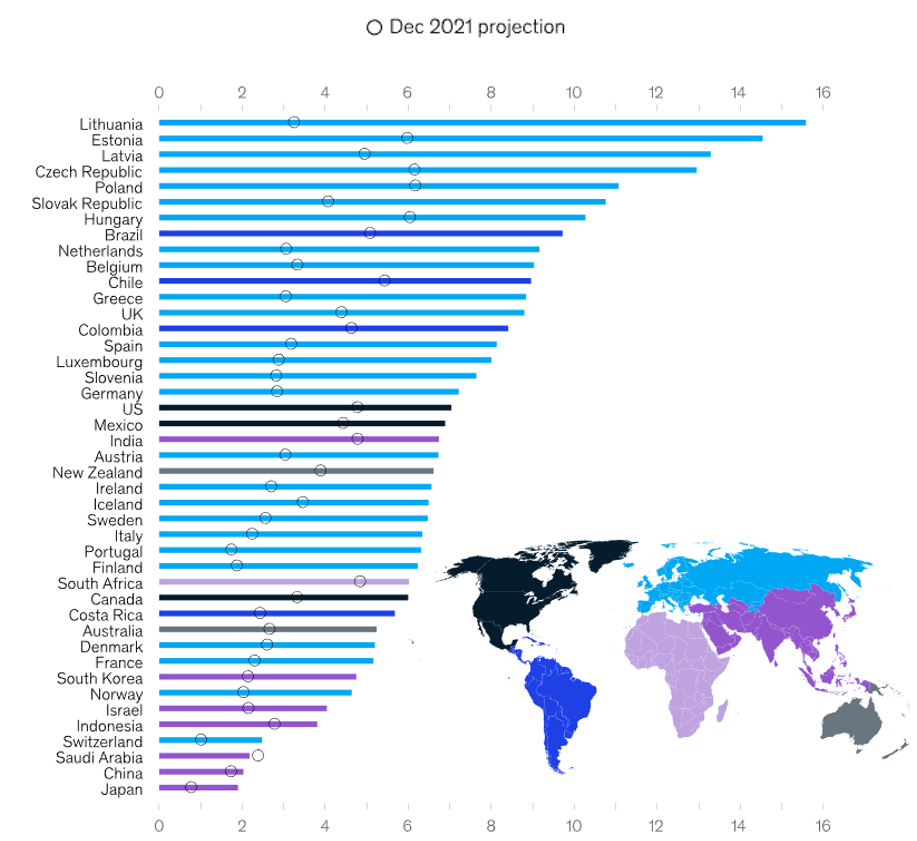

That said, it would be a great mistake to conclude that, in our part of the world, there is nothing to worry about. Inflation is doing damage everywhere and, in Europe, more so than in most other parts of the world (Exhibit 2). As you can see, in most countries in the table below, inflation is now more than twice the level projected only six months ago.

Exhibit 2: Inflation in June 2022, % change year-on-year Source: McKinsey & Company

Although I do not expect anything like what is currently unfolding in Sri Lanka to happen in Europe, less can still do much damage. Only days ago, the German Minister of Economics warned of a Lehman-like moment to unfold, should Russia cut off natural gas to Europe. Given Germany’s dependence on Russian gas, his warning should not be taken lightly.

Another risk one shouldn’t ignore is the fact that Sri Lanka is far from the only EM country which has sought IMF’s help. Pakistan, Argentina, Venezuela, Zambia, Lebanon and Laos (and probably quite a few more) are all in a dialogue with the IMF, as they look for some sort of bailout. As interest rates rise, the US dollar continues to strengthen (many EM loans are in US dollars) and the EM debt mountain continues to grow, the list of countries in trouble can only grow. At some stage that will begin to negatively affect the wealthier nations too.

One group of countries in the firing line is the old Eastern Bloc – countries such as the three Baltic Republics, the Czech Republic, Poland, Slovakia and Hungary. All these countries are knocking on the door to the club of wealthy nations, but they are, as you can see in Exhibit 2, particularly badly affected by the current episode of high inflation with CPI currently in the teens in all of those countries.

The coming winter could be brutal in those countries, and it won’t be much better in the rest of Europe. Putin is toying with the idea of playing his best card – the ability to turn people in western democracies against their own governments by switching off gas supplies to all of Europe. If he does that, continental Europe will almost certainly enter a recession over the next 6-9 months.

With the UK also likely to experience recessionary conditions over the coming winter (if the downturn hasn’t already begun there), and with the US not being far behind the UK in terms of the likelihood of a recession occurring soon, most of the OECD could experience negative GDP growth later this year or early next. Given how dramatically earnings estimates stand to be reduced, should that happen, we have little appetite for much equity beta in our portfolios at present.