On Friday July 15 the University of Michigan reported a modest drop in near-term and a more substantial drop in longer-term term US consumer inflation expectations. Equity and bond markets rallied, apparently concluding that expectations haven’t become “unanchored” after all. This verdict may be premature.

How expectations are formed is important: anchored expectations—that is, the belief that inflation will revert to a fixed number belief—imply merely higher inflation. But “adaptive” expectations imply increasing inflation when output (or employment) is above potential. The less anchored expectations, the larger the required economic sacrifice, in terms of employment and GDP cost, to reset them. This was the lesson of the 1970s, when expectations changed from fixed and stable to adaptive and unstable, and later periods when expectations were seemingly quite stable. A key question for money managers and investors concerned about recession severity is, have expectations-formation changed again?

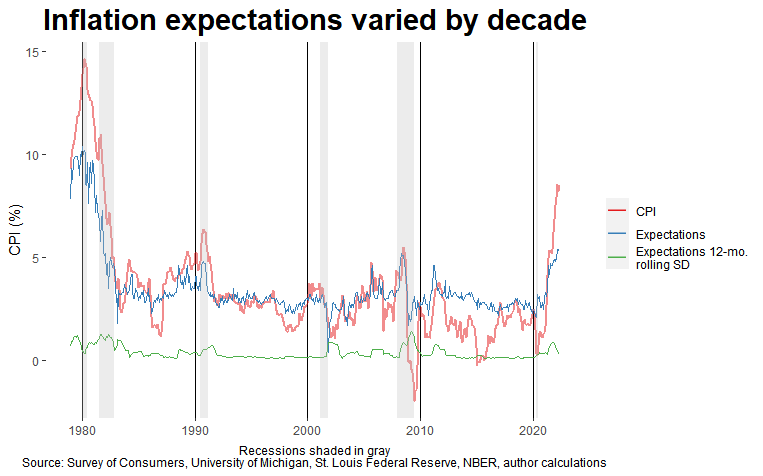

The chart below shows three time series: inflation as measured by the 12-month change in the Consumer Price Index (CPI—the red line), the median expected inflation rate in the next 12 months as reported in the University of Michigan Survey of Consumer Expectations (the blue line), and its 12-month standard deviation (the green line). [1]

After moving with inflation in the very late 1970s through the early 1990s, expectations settled down: moves in CPI were generally not matched by changes in expectations except for the mid-2000s. The 2010s, like the 1990s, were characterized by stable expectations which, combined with their indifference during the financial crisis, marked the end of the tyranny of the “accelerationist” Phillips curve to some. [2] The smoothed standard deviation series makes expectations-regime changes, and their possible strong reaction to oil price shocks (not shown), clearer.

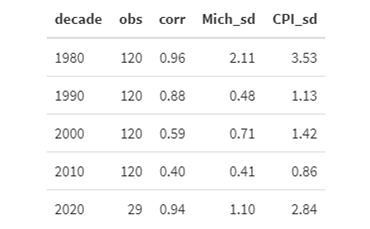

Another way to see how the “great moderation” in economic measures played out in inflation and expectations—and how things may have shifted—is by looking at the correlation between inflation and expectations, as well as volatility (standard deviation). The association between year-over-year inflation and one-year-ahead inflation expectations (the “corr” column) weakened in the decades following the 1980s—until, that is, the 2020s. The volatility (the last two columns) of both series is also higher in the current decade than in the past three.

Another way to see how the “great moderation” in economic measures played out in inflation and expectations—and how things may have shifted—is by looking at the correlation between inflation and expectations, as well as volatility (standard deviation). The association between year-over-year inflation and one-year-ahead inflation expectations (the “corr” column) weakened in the decades following the 1980s—until, that is, the 2020s. The volatility (the last two columns) of both series is also higher in the current decade than in the past three.

Inflation and expectations: correlation and volatility

Source: Survey of Consumers, University of Michigan, St. Louis Federal Reserve, author calculations

Analysis points toward the same conclusion. Regressions of expectations on contemporaneous CPI and various controls yield gradually declining estimated sensitivities (i.e., coefficients, all strongly significant) from the 1980s through the 2010s, with a break in the 2020s. These results are robust to the inclusion of various lags of CPI and expectations, and to different definitions of inflation (e.g., the personal consumption expenditures deflator). And tests of whether past inflation can predict expectations better than past expectations alone—tests of “Granger causality”—suggest that inflation helped improve expectations forecasts in the 1980s and 1990s and again the 2020s. But not in the decades in between.

At the very least, it’s unlikely that expectations became more sensitive to CPI during the great moderation decades. Arguably the evidence indicates the opposite. It also shows that the relationship isn’t stable, and that it may have shifted again.

This may be wrong—the decade is young, and our observations are few. Deflationary economic forces may reassert themselves and the Fed seems determined to regain control over inflation. While more data and better analysis is needed, early evidence isn’t encouraging.

The latest survey results are mildly reassuring. But the question of whether expectations are as firmly anchored as they were in the 2010s seems far from settled. And this is partly why it’s hard to say how severe an effective inflation-fighting recession might be.'

[1] Surveys of Consumers, University of Michigan, University of Michigan: Inflation Expectation© [MICH], retrieved from FRED, Federal Reserve Bank of St. Louis https://fred.stlouisfed.org/series/MICH/, (Accessed on July 15 2022).

[2] An accelerationist or expectations-augmented Phillips curve implies that low unemployment leads to an increasing inflation rate or, equivalently, an accelerating price level. In its original form the Phillips curve suggested that lower unemployment could be achieved at the cost of higher—but not necessarily increasing—inflation.

The author is an applied economist at Armstrong Advisory Group in Needham Massachusetts

ARMSTRONG ADVISORY GROUP – SEC REGISTERED INVESTMENT ADVISOR

The information contained herein including any expression of opinion, has been obtained from or is based upon, sources believed to be reliable, but is not guaranteed as to accuracy or completeness. This is not intended to be an offer to buy, sell or hold or a solicitation of an offer to buy, sell or hold the securities, if any referred to herein.

© Armstrong Advisory Group

Read more commentaries by Armstrong Advisory Group

Another way to see how the “great moderation” in economic measures played out in inflation and expectations—and how things may have shifted—is by looking at the correlation between inflation and expectations, as well as volatility (standard deviation). The association between year-over-year inflation and one-year-ahead inflation expectations (the “corr” column) weakened in the decades following the 1980s—until, that is, the 2020s. The volatility (the last two columns) of both series is also higher in the current decade than in the past three.

Another way to see how the “great moderation” in economic measures played out in inflation and expectations—and how things may have shifted—is by looking at the correlation between inflation and expectations, as well as volatility (standard deviation). The association between year-over-year inflation and one-year-ahead inflation expectations (the “corr” column) weakened in the decades following the 1980s—until, that is, the 2020s. The volatility (the last two columns) of both series is also higher in the current decade than in the past three.