Costly Lessons Re-Learned

The Federal Reserve Acts were created to make the central bank of the United States a lender of last resort, not spender of last resort, a role Chair Powell confirmed in announcing the Pandemic response program April 9, 2020. Constructed to prevent the central bank of the United States from acting like a banana republic central bank, the logic of the Federal Reserve Acts writers was impeccable. Converting Fed liabilities into a medium of exchange was well understood to be highly inflationary. Paying the U.S. government’s fiscal obligations with Fed liabilities sends demand for goods and services higher without an increase in the supply of goods and services to consume, the very definition of inflation.

Remarkably, Fed's low rate policy was very slow to change even though the actual increase in their preferred inflation measure surged to more than triple the upper limit of their target. Thus, the Fed continued to create demand, i.e., to shift the Aggregate Demand curve outward, while doing nothing to lift the Aggregate Supply (AS) curve upward. Indeed, supply chain disruptions from the pandemic, aggravated by the Russian invasion of Ukraine, shifted the AS curve inward, exacerbating the monetary induced price surge. This mountain of liquidity, the largest except for possibly an isolated event related to the end of WWII, played a major role in allowing price hikes from various supply chain disruptions to be passed on to beleaguered consumers who suffered from a much faster rise in prices than wages.

This situation has essentially morphed into a cost-of-living crisis. Real income for full time hourly and salaried workers has dropped by the fastest pace since 1980, and nominal disposable personal income has grown only 0.8% thus far in 2022. Considering that the average age in the United States is 38, more than half of U.S. citizens were not alive at the time of the last such crisis. No wonder the most properly constructed of all the consumer attitude surveys (University of Michigan) reports that sentiment is at a record low for readings that go back to 1952.

The Fed’s most pressing concerns are to not only reverse its monetary excess and misjudgment of inflation, but also to instill confidence that they will follow important provisions of the Federal Reserve Acts. These Acts were set up with the clear intent to keep the Fed free and independent with regards to fiscal policy. The Pandemic response was similar to President Nixon’s New Economic Program of 1971 that also blended the Fed and fiscal policy together. After a major dollar devaluation that resulted from closing of the Gold Window, the Fed committed to an acceleration in monetary growth. As such, the Fed reinforced the inflationary impact of the dollar devaluation. Further, wage and price controls were established, which included a complete compromise of the Fed’s independence when Fed Chair Arthur Burns was made chair of the Committee on Interest and Dividends. Now, like in the early 1970s, the Fed alone must unwind a combined monetary/fiscal policy failure. Thus, once again the architects of the Fed Acts showed their wisdom when they tried to establish the Fed’s independence, an insight apparently lost by today’s practitioners.

Destabilizing Effects of Monetary Accelerations and Decelerations

As much as the Fed would like to think that their actions during the Pandemic have stabilized the business cycle, the long historical record indicates that massive policy swings have often aggravated the magnitude of business cycles. For the Nobel Laureate Milton Friedman, the two key metrics were the degree of acceleration in monetary growth from the cyclical trough to the cyclical peak, and the ensuing deceleration from the peak to the trough. As such, the Fed has often boomed booms and slumped slumps. They have made expansions more inflationary and recessions deeper and longer lasting. To correct these failures, Friedman advocated that monetary growth should be contained in a relatively narrow range that allows for population growth and technological change. Friedman argued that there is an optimal range for monetary growth based upon the aggregate production function which relates real per capita GDP growth to technology interacting with the three factors of production – capital, labor and natural resources.

Based on the production function of that time, Friedman calculated that the broad money stock should be limited to a growth rate range of 4% to 6%. Real GDP per capita has risen by 1.4% per annum since the late 1990s. Since this is 0.8% per annum lower than from 1870 until 1997, the upper ceiling of monetary growth based on Friedman’s work suggests that annual growth should be 5%, with the lower range at 3%. Over 2020 and 2021, the pace of M2 quadrupled the ceiling rate, posting a 18% two-year average rate of increase. Friedman’s great book, The Optimum Quantity of Money, originally published in 1969, is still a highly recommended read. The great Stanford economist John Taylor documented the same problems as Friedman as did Karl Brunner and Alan Meltzer. Taylor offered a different rule than Friedman, but the key concept was recognizing the past failure of discretionary Fed policy. Fed spokesmen and their supporters have strongly opposed the adoption of rules on a variety of grounds, the most notable of which is that discretionary decisions must surely be better than some arbitrary rule.

As the 2020/21 episode demonstrates, the poor results of the Fed’s stewardship have continued. Ostensibly, this is confirmed by the Fed’s absolute refusal to allow for audits of monetary policy operations. Ironically, the argument is that this would impinge on their independence, which they surrendered in the Pandemic for two long years.

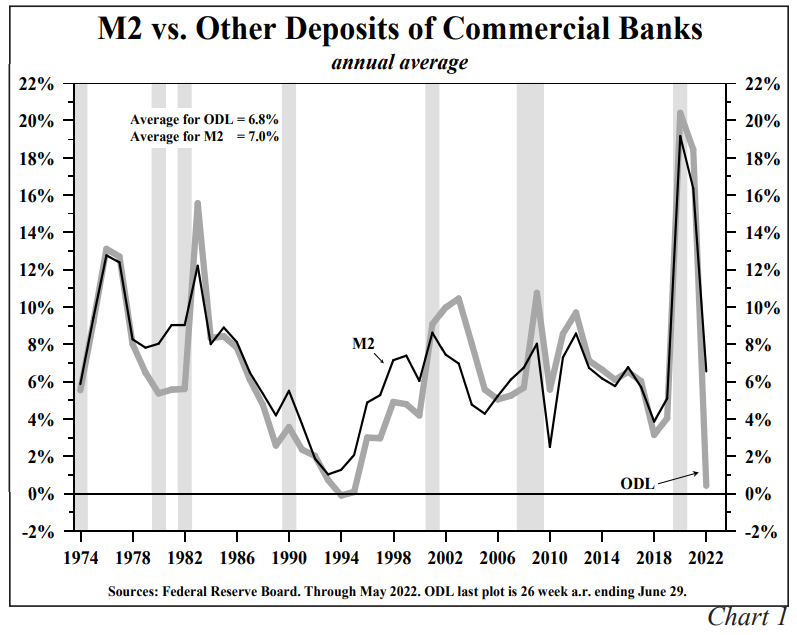

Reversing the massive deposit growth of 2020/21 will add to the list of policy failures because of the largely unprecedented degree to which deposits grew in these years and the needed magnitude of the deceleration that is already becoming apparent. By Friedman’s evidence, the likelihood for a successful outcome of a soft-landing for the Fed and thus the United States is low. In 2020/21, other deposit liabilities (ODL), which comprises about 80% of M2, and is the energizing component of M2, increased by an average of 19.6% (Chart 1). The difference between M2 and ODL is currency in circulation and money market mutual funds held by individual investors. Examination of the critical monetary relationships indicate that ODL is, at a minimum, of equal importance as M2 and most likely of even greater value in terms of cyclical economic analysis.

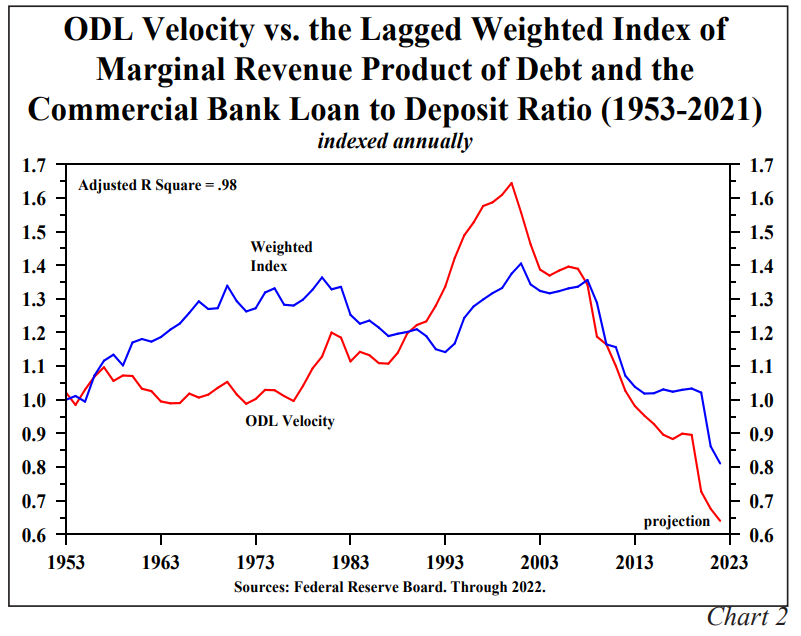

ODL and M2 movements must be evaluated along with deposit velocity (Chart 2). An equally weighted average of the marginal revenue product of debt and the loan to deposit ratio of the commercial banks leads deposit velocity by a year (with an impressive coefficient of correlation of 0.98).

ODL and M2 movements must be evaluated along with deposit velocity (Chart 2). An equally weighted average of the marginal revenue product of debt and the loan to deposit ratio of the commercial banks leads deposit velocity by a year (with an impressive coefficient of correlation of 0.98).

In the past 26 weeks, ODL has risen at an extremely slow .4% annual rate. Thus, as things recently stood, this would be one of the largest decelerations in deposit growth in nominal and real terms, with the sole exception of the Great Depression when nominal M2 fell by one-third between 1929 and 1933 and a special situation that arose at the end of World War II. The weakness in deposit velocity will serve to reinforce the extreme contraction in deposit growth. At the point the Fed shifts to a traditionally easier monetary policy, the effectiveness would be impeded by declining deposit velocity, thus making monetary policy asymmetric.

Complicating Issues

Complicating Issues

Two additional disconcerting issues go beyond Friedman’s findings. First, his research largely pertained to the time span from 1951 (or when the Fed and Treasury accord allowed Treasury yields to float freely) until the early 1980s. During that time velocity was stable. It was not constant, but changes were generally small and or quickly self-reversing. Velocity is likely to fall in 2022, compared with 2021, meaning that the slowdown in deposit growth will be reinforced by an endogenous factor that the Fed does not control. We are unaware of any continuing and significant research by the Federal Reserve on the effects of the monetary aggregates on the economy. No mention of monetary statistics has been made in Fed Chair press conferences for years.

Second, Friedman did not address the matter of the length of time that monetary accelerations lasted. An unsurpassed pool of liquidity has been created over the course of the prior two years. Since the end of 2019, through late June of this year the deposit growth averaged 18%, almost triple the average growth in ODL from 1952 to 2021. ODL would need to remain very depressed for the rest of this year and 2023 for the four-year average growth to fall within the upper limit of the optimum growth band consistent with Friedman’s analysis.

Outlook

A long list of pre-recessionary indicators is already present. These include declines in the volume of retail sales in five of the last seven months, a steep drop in new and existing home sales, housing starts, building permits and mortgage applications; vehicle sales at levels quite depressed from the 2019 level, severe erosion in the NFIB small business survey, flat trucking volumes thus far in 2022, and an outright decline in rail freight. New weekly unemployment claims have been working higher since the beginning of April. Manufacturing, at best, has plateaued, but indications of a downturn have been increasing along with signs of moderation in capital expenditures. Inventory investment, the main driver of growth in 2022, could slow and pose a major restraint on economic growth well before year end. International economic conditions do not always line up with the U.S. business cycle, but conditions are extremely poor around the globe.

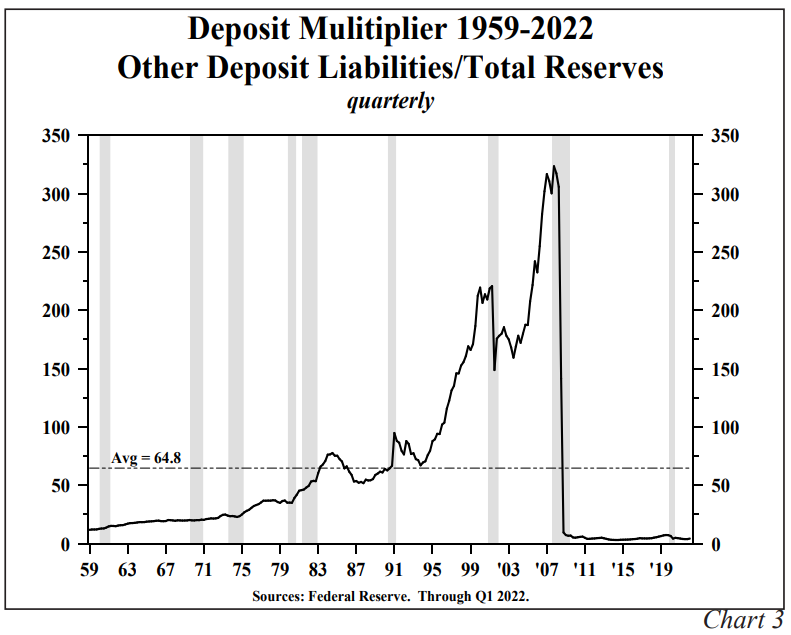

Two additional monetary indicators supplement this list of economic indicators. First, portions of the Treasury yield curve have flattened significantly and inverted at times. Second, ODL is linked to monetary policy by the deposit multiplier, which is defined as ODL divided by total reserves, which is referred to as 'd'. The deposit multiplier has turned down again (Chart 3), indicating the Fed’s ability to stimulate economic activity under the 'lender of last resort' regime is diminishing and monetary policy’s capabilities are becoming increasingly asymmetric. Recently, d was 4.3, close to its record low, and dramatically lower than the 64.8 average from 1959 to date. A low d indicates the demand for money is weak and that the banks are having difficulty pricing all their costs, including the risk premium that is most likely rising alongside the deterioration in business prospects.

Tentative recessionary indicators have entered the picture. The National Bureau of Economic Research (NBER) bases business cycle turning points on nonfarm employment, real personal income less transfer payments, industrial production and the volume of business sales. A downturn in several different indexes of leading economic indicators suggest the coincident indicators, which includes the NBER’s four variables, could soon reverse a trend that so far remains upward.

Tentative recessionary indicators have entered the picture. The National Bureau of Economic Research (NBER) bases business cycle turning points on nonfarm employment, real personal income less transfer payments, industrial production and the volume of business sales. A downturn in several different indexes of leading economic indicators suggest the coincident indicators, which includes the NBER’s four variables, could soon reverse a trend that so far remains upward.

Conclusion

Monetary considerations coupled with these real side indicators point to recession and a reduction in inflation and long-term Treasury bond yields. If the Fed stays within the scope of the Federal Reserve Acts, they will have difficulty in containing the recession and fostering a recovery. But that situation puts us on alert to the possibility that the Fed returns to a Pandemic type of response that generated an inflation rate far above their target, as the experience of the past two years has so painfully taught. The economy might recover temporarily, but the expansion would be interrupted by another cost-of-living crisis and the Fed would not achieve either of its mandates for employment or inflation.

© Hoisington Investment Management